Primary Flight Display Market Size, Share & Industry Analysis, By System (Primary Flight Displays, Electronic Flight Display, Head-Down Cockpit Displays, Head-Up Displays), By Application (Commercial Transport Aircraft, Regional Aircraft, Business Aviation, Civil Rotorcraft, Military Aviation, and Military Rotorcraft), By Technology (TFT LCD / AMLCD, LED-backlit LCD, High-resolution LCD, OLED, MicroLED, and Legacy Technologies), By End User (Aircraft OEMs, Business and Private Operators, Helicopter Operators, Defense and Government Customers), and Regional Forecast, 2026-2034

Primary Flight Display Market Size and Future Outlook

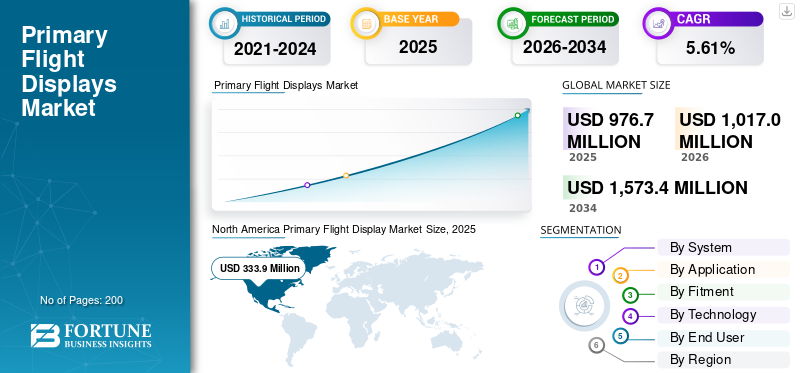

The global primary flight display market size was valued at USD 976.7 million in 2025 and is projected to grow from USD 1,017.0 million in 2026 to USD 1,573.4 million by 2034, exhibiting a CAGR of 5.61% during the forecast period. North America dominated the primary flight display market with a market share of 34.18% in 2025.

A Primary Flight Display (PFD) is a screen-based aircraft instrument that integrates key flight data like attitude, airspeed, altitude, heading, and vertical speed, replacing traditional analog gauges. It typically features an LCD or CRT screen showing graphical representations of these metrics for enhanced situational awareness, often with synthetic vision. PFDs are used in commercial, military, and general aviation cockpits to streamline pilot monitoring and boost safety. Market growth drivers include rising air traffic, glass cockpit retrofits, and avionics advancements for automation.

Leading players Collins Aerospace develops advanced primary flight displays like the AFD-3210, a MOSA-compliant 9-inch LCD touchscreen for military aircraft primary flight and mission data, enhancing integration and pilot awareness, Thales Group focuses on avionics upgrades and defense contracts, including IFF systems for naval vessels and support deals like ABSOLU for French forces' communication gear, Honeywell international which innovates integrated PFDs with synthetic vision, as in Primus Epic for Gulfstream jets, targeting business aviation with enhanced vision certification and so on.

Download Free sample to learn more about this report.

Primary Flight Display Market Key Takeways

- 2025 Market Size: USD 976.7 million

- 2026 Market Size: USD 1,017.0 million

- 2034 Forecast Market Size: USD 1,573.4 million

- CAGR: 5.61% from 2026–2034

- North America dominated the primary flight display market with a 34.18% share in 2025.

- The large-area / panoramic cockpit displays segment is expected to witness the fastest growth during the forecast period.

- The business aviation segment is projected to register strong growth throughout the forecast period.

North America

North America remained the leading regional market, with an estimated valuation of USD 333.9 million in 2026.

Europe

Europe is projected to grow at a 5.33% CAGR during the forecast period, reaching USD 287.1 million in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 288.6 million in 2026, maintaining its position as the third-largest regional market.

U.S.

U.S. The market is estimated to reach approximately USD 210.1 million in 2026, supported by continued investments in advanced avionics technologies.

Japan

Japan The market is projected to reach approximately USD 40.8 million in 2026, expanding at a 6.18% CAGR during the forecast period.

Read More

PRIMARY FLIGHT DISPLAY MARKET TRENDS

Integration Of Synthetic Vision Systems (SVS) Is A Market Trend

Integration of Synthetic Vision Systems (SVS) into primary flight displays represents a pivotal market trend in aviation, combining GPS, terrain databases, and high-resolution 3D rendering to deliver environmental views regardless of weather or visibility. This enhances pilot situational awareness by depicting terrain, obstacles, runways, and traffic in real-time, slashing Controlled Flight Into Terrain (CFIT) risks and easing low-altitude operations. SVS unburdens cognitive workload during demanding phases like approaches, enabling faster hazard detection, and proactive decisions. Adoption surges in glass cockpits across commercial, general, and military fleets, driven by maturing databases and certification standards.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Mandates for Enhancing Aviation Safety Is Anticipated To Drive Market Growth

Regulatory mandates from FAA and European Union Aviation Safety Agency (EASA) is driving market growth by enforcing airworthiness standards for synthetic vision and glass cockpits to enhance aviation safety. FAA Advisory Circulars AC 20-167A and AC 20-185A outline certification pathways for SVS integration, mandating compliance for Part 23/25 aircraft to mitigate CFIT risks in low visibility operations. Furthermore, National Transportation Safety Board (NTSB) recommendations are pushing for mandatory backups and training for digital displays following incidents like blackouts and among others. Similarly, the EASA guidelines on EFVS/SBAS further accelerate retrofits in Europe. These rules spur fleet upgrades amid rising traffic, prioritizing intuitive PFDs for workload reduction.

MARKET RESTRAINTS

High Initial Costs to Act as a Market Growth Restraint

High initial costs act as a primary restraint for primary flight display market growth as such costs limit the total capital used in fleet expansion and daily operations and divert them towards investing in PFDs, posing acute challenges for smaller general aviation operators and airlines in developing regions. Furthermore, upfront investments in advanced LCD/OLED screens, sensors, wiring, and software integration often exceed the aircraft's value, delaying retrofits and prioritizing essential maintenance over safety upgrades. This financial barrier slows PFD penetration despite mandates, as revenue-generating downtime avoidance take over long-term benefits.

MARKET OPPORTUNITIES

Global Fleet Modernization To Generate Market Growth Opportunity

Global fleet modernization accelerates opportunities for the market as airlines extend legacy aircraft lifespans amid OEM delivery delays, prioritizing avionics retrofits for efficiency and compliance. For instance, Airbus forecasts 18,930 replacements that are a trend toward 95% of the fleet being new-generation aircraft by 2044. The replacement aims for a 25% fuel-burn reduction, which increases the necessity for advanced cockpit system technologies, including Synthetic Vision Systems (SVS).

MARKET CHALLENGES

Cybersecurity Vulnerabilities In Networked PFDs to Act As A Market Challenge

Cybersecurity vulnerabilities in networked primary flight displays to challenge the market growth by exposing critical avionics to remote hacks via Wi-Fi, satellite links, or maintenance ports, potentially spoofing altitude/speed data or triggering false alerts. EASA's ED-202A and FAA Special Conditions mandate PISRA assessments for connected systems, complicating certifications with encrypted architectures and intrusion detection that inflate timelines by 12-18 months. Exploits like TCAS II flaws (CVE-2024-11166) underscore risks, delaying PFD deployments as operators prioritize air-gapped legacy systems over vulnerable glass cockpits.

Segmentation Analysis

By System

Obsolescence and Reliability Issues Due to Aging Fleets to Boost the Primary Flight Displays (PFDs) Segment Growth

Based on the system, the market is segmented into Primary Flight Displays (PFDs), Electronic Flight Display / EFIS suites, head-down cockpit displays, standby electronic flight displays, Head-up displays (HUD) / head-up guidance systems, large-area / panoramic cockpit displays, and others.

The Primary Flight Displays (PFDs) segment is anticipated to account for the largest market share. As aircraft fleets age, analog cockpit instruments increasingly face reliability issues and obsolescence. Consequently, operators are upgrading to digital PFDs to reduce maintenance costs, improve safety through enhanced situational awareness, and ensure regulatory compliance.

The large-area / panoramic cockpit displays segment is anticipated to rise with a high CAGR of 6.34% over the forecast period.

By Application

Commercial Transport is the Leading Application With Booming E-Commerce Sector

Based on application, the market is segmented into commercial transport aircraft, regional aircraft, business aviation, general aviation, civil rotorcraft, military aviation, and military rotorcraft.

In 2025, the commercial transport aircraft segment dominated the global market due to rising middle-class urbanization and a booming e-commerce sector which are recording a high demand for commercial transport aircraft.

The business aviation segment is projected to grow at a high CAGR of 6.14% over the forecast period.

By Fitment

Retrofit Segment To Dominate Owing To Sustainability Mandates

Based on the fitment, the market is segmented into line-fit / forward-fit, retrofit, fleet modernization, STC / certified aftermarket installation, replacement / spares, mission upgrade packages, and others.

Retrofit segment is anticipated to witness a dominating market share over the forecast period. Stringent global sustainability mandates are compelling transport operators to reduce carbon footprints. This has triggered a surge in the fitment segment, as upgrading existing vehicles with cleaner, efficient technologies offers a cost effective path to regulatory compliance.

The fleet modernization segment is projected to grow at a high CAGR of 6.24% over the forecast period.

By Technology

Rise In Rapid Digitalization is Bolstering The TFT LCD / AMLCD Segment

Based on technology, the market is segmented into TFT LCD / AMLCD, LED-backlit LCD, High-resolution LCD, NVIS-compatible display technology, OLED / AMOLED / micro-OLED, MicroLED, and legacy technologies / others.

TFT LCD / AMLCD segment dominated the market share as rapid digitalization of vehicle interiors drives demand for TFT LCD and AMLCD upgrades. As consumers prioritize modern infotainment and flight safety displays, vehicle aging causes original screens to fail or become obsolete.

The MicroLED segment is projected to grow at a high CAGR of 6.40% during the study period.

By End User

To know how our report can help streamline your business, Speak to Analyst

rapid Surge in Air Travel Has Placed Aircraft OEMs as the Leading End User

Based on end user, the market is segmented into aircraft OEMs, business and private operators, helicopter operators, defense and government customers, MROs / retrofit centers / authorized dealers.

Aircraft OEMs segment dominated the segmental market share. As global tourism rebounds, soaring passenger volumes have forced airlines to modernize aging fleets and expand capacity. This surge in air travel has led to a massive spike in orders for aircraft OEMs.

MROs / retrofit centers / authorized dealers are projected to grow at a high CAGR of 6.51% during the study period.

Primary Flight Display Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Primary Flight Display Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 322.7 million, and also maintained the leading share in 2025, with USD 333.9 million. North America continues to dominate the market due to mature aviation infrastructure and FAA cybersecurity mandates under the 2024 Reauthorization Act, requiring IUEI risk assessments for networked avionics.

U.S Primary Flight Display Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 210.1 million in 2026, growing at a 5.84% CAGR during the forecast period. The U.S. dominates with FAA NPRMs targeting PFD vulnerabilities, mandating software screening and encryption for transport aircraft certifications. Honeywell and Collins Aerospace are investing heavily in DO-178C compliant PFDs for commercial fleets.

Europe

Europe is projected to record a steady growth rate of 5.33% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 287.1 million by 2026. Europe advances via EASA's ED-202A cybersecurity guidance and initial airworthiness rules, spurring PFD upgrades in Airbus A320 fleets. Thales Group leads in R&D for integrated displays amid SESAR NextGen initiatives.

U.K Primary Flight Display Market

The U.K. market in 2026 is estimated at around USD 96.5 million, growing at a CAGR of 5.65% over the forecast period. The U.K. emphasizes PFD cybersecurity post-Brexit, aligning with EASA via CAA directives on networked avionics resilience with BAE Systems developing secure displays for Tempest fighter programs.

Germany Primary Flight Display Market

Germany’s market is projected to reach approximately USD 84.9 million in 2026. Germany invests in aerospace R&D despite declining BERD ratios, focusing on glass cockpits for Eurofighter upgrades. Airbus Defence in the country contributes in PFD innovations through Ottobrunn facilities.

Asia Pacific

Asia Pacific region is estimated to reach USD 288.6 million in 2026 and secure the position of the third-largest region in the market. The region is also expected to be the fastest growing during the forecast period as it is expanding quickly due to increased air traffic, major fleet modernization projects, and use of cutting-edge digital cockpit technologies.

Japan Primary Flight Display Market

The Japan market in 2026 is estimated at around USD 40.8 million, expanding at roughly 6.18% of CAGR during the forecast period. Japan integrates PFDs in Mitsubishi SpaceJet programs, focusing on JAXA-led cybersecurity standards. Kawasaki Aerospace in Japan is known for developing advances displays for Boeing 787s.

China Primary Flight Display Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 97.0 million. China pushes PFD integration in C919 narrow-bodies under CAAC oversight, emphasizing domestic avionics security. AVIC in the country is investing in R&D in SVS for military transports.

India Primary Flight Display Market

The India market in 2026 is estimated at around USD 85.3 million. India modernizes HAL Tejas fighters with indigenous PFDs amid Make-in-India initiatives. Boeing supports GA upgrades via Hyderabad MRO hubs

Rest of the World

The rest of the world includes Middle East and Africa and Latin America. Latin America retrofits Boeing 737s in Brazil via Embraer facilities, Middle East upgrades Gulfstream jets under GCAA rules, and Africa modernizes via South African DENEL are boosting the market growth in the regions. The Middle East & Africa and Latin America market is set to reach a valuation of USD 56.0 million and USD 38.0 million, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Alliances in the Market is Enhancing the Positions of the Prominent Players

The competitive landscape in the market remains moderately consolidated, dominated by established avionics specialists and aerospace integrators driving glass cockpit advancements. Key players include Collins Aerospace, Honeywell International, Thales Group, Garmin Ltd., L3Harris Technologies, and Elbit Systems Ltd., among others. Strategic partnerships is accelerating PFD innovation as Boeing and Airbus collaborate with avionics leaders to integrate synthetic vision, AI analytics, and cybersecurity-compliant displays into NextGen platforms, meeting FAA/EASA mandates for enhanced situational awareness. Retrofit specialists partner with MRO providers to upgrade legacy fleets with modular LCD/OLED PFDs, addressing surging air traffic via SESAR/NextGen compliance. Military programs are fueling joint ventures Collins with Lockheed for F-35 displays, Thales with Dassault for Rafale, and Garmin targeting GA retrofits. These alliances blend sensor fusion, DO-178C software, and encrypted networks, capturing commercial, defense, and urban air mobility demand through 2030.

LIST OF KEY PRIMARY FLIGHT DISPLAY COMPANIES PROFILED

- Collins Aerospace ((U.S.)

- Honeywell International (U.S.)

- Thales Group (France)

- Garmin Ltd. (U.S.)

- L3Harris Technologies Inc. (U.S.)

- Elbit Systems Ltd. (Israel)

- Universal Avionics (U.S.)

- Genesys Aerosystems (U.S.)

- Aspen Avionics (U.S.)

- Astronautics Corporation of America (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Innovative Aerosystems announced that it has signed a perpetual license and asset purchase agreement with Honeywell International Inc. for program assets, aftermarket parts, and intellectual property related to a few legacy Honeywell avionics product lines that support the world's fleet of Part 23 aircraft.

- December 2025: A 10-year, USD 425 million indefinite-delivery/indefinite-quantity contract to update and modernize cockpit displays for the U.S. Air Force F-16 fleet was awarded to V2X. V2X will provide center display unit complete kits, shop, and line-replaceable units along with associated support hardware as part of the award.

- June 2025: Borsight Inc. has been given a contract for up to USD 2.18 billion by the U.S. Air Force to replace the avionics in all of its T-6 Texan II trainers.

- October 2024: The U.S. Army, via the Defense Logistics Agency, has awarded Honeywell a USD 103 million contract to install its Next-Generation APN-209 Radar Altimeter (Next Gen APN-209) system on a range of Army aircraft.

- June 2023: Saab, a Swedish aerospace and defense corporation, has agreed to sell its Heads-Up-Display (HUD) assets to Honeywell International for use in a range of Honeywell avionics products. Saab and Honeywell will collaborate to expand and improve Saab's HUD product line as part of the acquisition agreement.

REPORT COVERAGE

The global primary flight display industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, Porter’s five forces analysis, company profiles and regional analysis. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The global market report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.61% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By System, Application, Fitment, Technology, End User, and Region |

| By System |

|

| By Application |

|

| By Fitment |

|

| By Technology |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 976.7 million in 2025 and is projected to reach USD 1,573.4 million by 2034.

In 2025, the market value stood at USD 333.9 million.

The market is expected to exhibit a CAGR of 5.61% during the forecast period.

By system, the PFDs segment is expected to dominate the market.

Regulatory mandates are anticipated to drive market growth.

Collins Aerospace (U.S.), Honeywell International (U.S.), Thales Group (France), Garmin Ltd. (U.S.), L3Harris Technologies Inc. (U.S.), and Elbit Systems Ltd. (Israel) are the key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us