Private Equity Market Size, Share & Industry Analysis, By Type (Leveraged Buyouts (LBOs), Venture Capital, Real Estate Private Equity, Distressed and Special Situations, and Others), By Industry (Technology, Healthcare, Consumer & Retail, Financial Services, and Others), and Regional Forecast, 2026 - 2034

KEY MARKET INSIGHTS

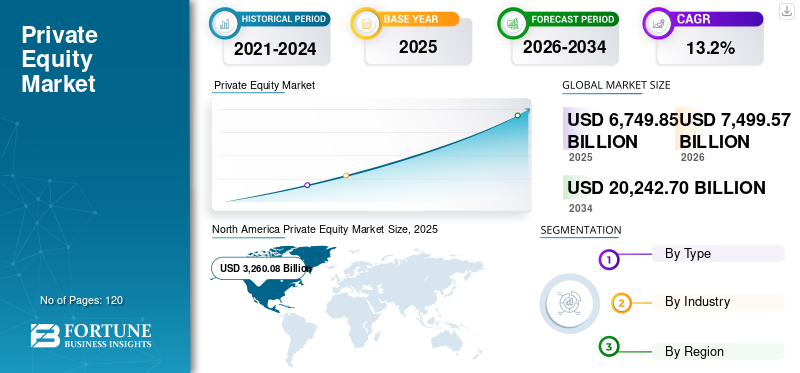

The global private equity market size was valued at USD 6,749.85 billion in 2025 and is projected to grow from USD 7,499.57 billion in 2026 to USD 20,242.70 billion by 2034, exhibiting a CAGR of 13.2% during the forecast period. North America dominated the global private equity market, accounting for 48.3% of the market share in 2025. Industry growth is driven by institutional capital expansion, digital value creation strategies, regulatory evolution, and increasing cross-border investment activity across developed and emerging economies.

The global private equity market continues to expand as a central component of alternative investments, supported by sustained institutional capital inflows and evolving portfolio allocation strategies. Total assets under management (AUM) are estimated to exceed USD 7 trillion in 2025, reflecting long-term growth across buyout, growth equity, and adjacent strategies.

Institutional investors remain the primary capital providers. Pension funds, sovereign wealth funds, and insurance companies are steadily increasing allocations to private equity, often targeting 10%–20% of total portfolios. This shift is driven by the search for yield, diversification benefits, and the ability to capture illiquidity premiums relative to public markets.

Fundraising activity has moderated compared to peak cycles but remains structurally resilient. Larger, established managers continue to attract disproportionate capital, while emerging managers face longer fundraising timelines. This concentration reflects investor preference for proven track records and operational capabilities.

The private equity (PE) industry is witnessing steady growth, supported by a growing supply of private capital seeking higher returns than public markets. Institutional investors such as pension funds, sovereign wealth funds, and insurers have continued to increase allocations to private assets to meet long-term return targets. This sustained capital inflow enhances PE firms' ability to fund buyouts, growth investments, and sector roll-ups across industries. At the same time, it supports more specialized strategies such as secondaries and private credit-linked deals, broadening overall market activity.

- For instance, in 2025, A survey of insurance CIOs (conducted by Goldman Sachs) found that about 62% of insurers plan to increase private markets allocations.

Furthermore, several industry players such as Blackstone, KKR & Co., Apollo Global Management, The Carlyle Group, and TPG are focusing on scaling diversified private markets platforms and expanding investment into high-growth, resilient sectors such as technology, healthcare, infrastructure, and private credit-linked opportunities. These firms are also strengthening value creation capabilities by building in-house operating teams, digital transformation units, and sector-specialist groups to improve portfolio performance.

Download Free sample to learn more about this report.

Private Equity Market Key Takeaways

- 2025 Market Size: USD 6,749.85 Billion

- 2026 Market Size: USD 7,499.57 Billion

- 2034 Forecast Market Size: USD 20,242.70 Billion

- CAGR: 13.20% from 2026–2034

- North America dominated the private equity market with a 48.3% share in 2025.

- Leveraged buyouts (LBOs) accounted for the largest share of the market by type in 2025.

- Technology held the largest industry segment share in the global market in 2025.

North America

North America dominated the private equity market with a 48.3% share in 2025.

Europe

Europe reached USD 1,628.83 billion in 2025 and is projected to grow at a CAGR of 12.5%.

Asia Pacific

Asia Pacific recorded a market value of USD 1,285.72 billion in 2025 and remained the third-largest regional market.

U.S.

The market was valued at approximately USD 2,796.14 billion in 2025, accounting for around 41.0% of global revenue

Japan

The market reached approximately USD 164.18 billion in 2025, representing about 2.0% of global revenue.

Read More

Private Equity Market Trends:

Increasing Convergence of Private Equity and Private Credit is a Prominent Trend Observed in the Market

The convergence of private equity and private credit is becoming a prominent market trend as PE sponsors increasingly rely on non-bank lenders to finance acquisitions, refinancings, and add-on deals. Private credit has expanded beyond mid-market direct lending into large-cap LBO financing and refinancing of syndicated loans, intensifying competition with public markets and reshaping deal structures. At the same time, sponsors and lenders are building custom capital stacks (unitranche, PIK notes, holdco debt) to support longer hold periods and delayed exits. This overlap is also driving growth in credit secondaries and continuation-style solutions, enabling liquidity for LPs and portfolio management for GPs in a slower exit environment.

- For instance, in February 2025, according to the Proskauer survey, 91% of respondents expect deal activity to increase over the next 12 months, reflecting strong momentum for direct lending and sponsor-backed financing, including acquisition and refinancing activity. This supports the point that PE sponsors are increasingly relying on private credit as deal-making expands.

The private equity market is undergoing a clear transition toward operationally driven value creation. Historically, returns were supported by multiple expansions and leverage optimization. Under current conditions, general partners (GPs) are prioritizing margin improvement, pricing discipline, and revenue acceleration within portfolio companies.

Holding periods are extending modestly. Exit timing has become more dependent on market windows rather than predefined investment cycles. As a result, continuation vehicles and secondary transactions are increasingly used to manage liquidity while preserving exposure to high-performing assets.

Sector specialization is becoming more pronounced. Funds are concentrating capital in areas where domain expertise enables differentiated underwriting. Technology, healthcare, and business services continue to dominate, supported by structural growth drivers and recurring revenue models. Co-investment structures are expanding. Limited partners (LPs) are seeking greater control over capital deployment and reduced fee burdens. This shift is influencing fund economics and reinforcing alignment between investors and managers.

Data integration is reshaping investment processes. Advanced analytics are now embedded in deal sourcing, due diligence, and portfolio monitoring. Firms are leveraging proprietary datasets to enhance decision accuracy and identify operational inefficiencies early in the investment lifecycle. Environmental, social, and governance considerations are increasingly standardized. ESG integration is no longer discretionary and is being incorporated into investment committees, risk frameworks, and reporting structures.

Download Free sample to learn more about this report.

Key Market Dynamics

Private Equity Market Growth Factors:

Growth of Secondaries and Continuation Funds Improving Liquidity and Propelling Adoption for Private Equity

In a slower exit environment, many LPs seek liquidity to rebalance portfolios, manage over-allocations, or meet cash flow needs, and the secondary market provides a direct pathway to achieve this. Continuation funds, typically GP-led transactions, allow a sponsor to transfer a high-performing asset from an older fund into a new vehicle, enabling existing investors to either cash out or roll over their stake. This mechanism supports longer value creation timelines, especially for assets that still have growth runways but are not ideal to exit immediately. Overall, the expansion of secondaries and continuation funds strengthens the private equity ecosystem by easing liquidity constraints, improving capital recycling, and supporting continued fundraising momentum.

- For instance, in January 2025, Jefferies’ Global Secondary Market Review stated that global secondary volume surged to a record high in 2024, driven by a strong desire from both LPs and GPs to generate liquidity and accelerate distributions, alongside improving secondary pricing and high levels of dedicated capital.

Institutional capital allocation continues to underpin growth in the private equity market. Large asset owners are increasing exposure to alternative assets as part of long-term portfolio construction strategies. This reallocation is driven by the need for higher returns and diversification beyond public equities and fixed income. The expansion of private markets is also linked to structural changes in corporate financing. Companies are remaining private for longer durations, increasing the available investment universe. This trend allows private equity firms to participate in earlier growth stages while maintaining influence over strategic direction.

Operational capabilities within private equity firms have strengthened materially. Many firms now employ dedicated operating teams with expertise in digital transformation, procurement optimization, and revenue management. These capabilities support more predictable value creation across portfolio companies. The development of private credit markets has enhanced deal execution flexibility. Alternative lenders provide customized financing solutions, reducing reliance on traditional banking systems. This enables transactions to proceed even under constrained credit conditions.

Emerging markets contribute additional growth momentum. Rising middle-class populations, increasing digital adoption, and favorable demographics create attractive conditions for capital deployment. These regions offer higher growth potential, albeit with increased execution complexity.

Restraining Factors:

Valuation Gaps between Buyers and Sellers Restricting Market Growth

Valuation gaps between buyers and sellers are restricting the private equity market growth as many sellers continue to anchor expectations to the higher multiples seen during the low-interest-rate period, while buyers are underwriting deals using today’s higher cost of capital and more conservative growth assumptions. This mismatch widens the bid-ask spread, causing more deal processes to stall or take longer to close.

As a result, PE firms become selective and focus on only the highest-quality assets or situations with clear operational upside. The valuation gap also limits exit activity, since sponsors may delay selling portfolio companies until pricing improves. Overall, persistent pricing friction reduces transaction volume, slows capital deployment, and delays liquidity for investors.

Macroeconomic volatility continues to influence private equity market dynamics. Inflation uncertainty, interest rate fluctuations, and geopolitical instability complicate valuation assumptions and delay investment decisions. These factors introduce variability in both entry pricing and exit outcomes. Higher borrowing costs have reduced the attractiveness of leveraged buyouts. Debt financing is less accessible and more expensive, limiting the effectiveness of traditional capital structures. Sponsors are increasingly required to deploy higher equity contributions, which can dilute return profiles.

Public market volatility has constrained initial public offering activity, while strategic buyers exhibit greater caution in acquisition decisions. As a result, holding periods are extending, and liquidity realization is becoming less predictable. Regulatory pressure is increasing across multiple jurisdictions. Authorities are focusing on transparency, tax structures, and market concentration. Compliance requirements are becoming more complex, particularly for multinational transactions.

Competitive intensity within the private equity industry has increased. A large number of funds are targeting similar assets, driving up entry valuations and compressing potential returns. This is particularly evident in high-growth sectors such as technology and healthcare. Talent availability represents an additional constraint. Experienced investment professionals and operating partners are limited in supply, increasing costs, and potentially affecting execution quality.

Market Opportunities:

Digitization and AI-Led Operational Transformation to Offer Market Growth Opportunities

PE firms are increasingly using AI and advanced analytics to improve core levers such as pricing, demand forecasting, procurement, and working capital management across portfolio companies. Automation and AI-driven workflows also reduce operating costs by improving productivity in back-office functions such as finance, HR, and customer support. In customer-facing areas, digital tools help enhance lead conversion, improve retention, and personalize offerings, which supports revenue growth and stronger margins.

AI is also being applied in diligence and portfolio monitoring to identify risks earlier and speed up decision-making. For fragmented industries, digitization enables scalable integration of add-on acquisitions, improving consistency and synergies in roll-up strategies. Thus, the ability to drive measurable operational gains through digital and AI initiatives is becoming a key differentiator for PE funds, propelling new deal interest rates and creating major market opportunities.

The private equity market presents significant opportunities in the mid-market segment, where inefficiencies are more pronounced. Companies in this segment often lack scale, operational sophistication, or access to capital, creating clear pathways for value creation through strategic and operational improvements. Digital transformation remains a central opportunity. Private equity firms are increasingly investing in companies that enable automation, data analytics, and cloud-based solutions. Additionally, sponsors are deploying digital tools across portfolio companies to enhance efficiency and scalability.

Infrastructure and energy transition investments are gaining importance. The global shift toward decarbonization is creating demand for renewable energy assets, grid modernization, and sustainable infrastructure. These investments offer long-term, stable cash flows and portfolio diversification benefits. Healthcare continues to provide attractive opportunities due to demographic trends and increasing demand for services. Investments in healthcare delivery, medical technology, and life sciences are supported by consistent demand and innovation-driven growth.

Secondary markets are expanding, providing liquidity solutions and portfolio optimization options. Investors can access mature assets with established performance profiles, reducing risk compared to primary investments. Emerging markets remain underpenetrated, offering long-term growth potential. Economic development, urbanization, and digital adoption are driving investment opportunities across multiple sectors.

Segmentation Analysis

By Type

Rising Need for Leveraged Buyouts that Support Structured Debt Financing Propelled Segmental Growth

Based on the type, the market is divided into leveraged buyouts (LBOs), venture capital, real estate private equity, distressed and special situations, and others.

Leveraged buyouts (LBOs) accounted for the largest private equity market share due to a strong fit with mature, cash-generative businesses that can support structured debt financing and deliver predictable returns. LBOs remain the preferred strategy for many sponsors as they enable control ownership, allowing PE firms to implement operational improvements, cost optimization, and strategic add-on acquisitions more effectively. North America and Western Europe have a large pipeline of mid-market and carve-out opportunities that are well-suited to buyout models. Even when financing conditions tighten, buyouts continue to dominate as investors value their relatively stable cash flows and clear value creation levers compared to higher-risk early-stage strategies.

Venture capital is anticipated to rise with a CAGR of 16.9% over the forecast period, driven by the accelerating commercialization of AI, cloud software, and deep-tech innovations that are creating new high-growth startup categories.

Leveraged buyouts (LBOs) continue to represent the largest segment within the private equity industry, accounting for a significant share of total deal value. These transactions typically involve acquiring mature businesses using a combination of equity and debt. However, the role of leverage has evolved. With higher borrowing costs, value creation increasingly depends on operational improvements rather than financial engineering. Sponsors are focusing on revenue growth initiatives, cost optimization, and strategic repositioning. Mid-market LBOs are gaining prominence due to more attractive entry valuations and lower competitive intensity compared to large-cap deals.

Venture capital remains a critical segment, targeting early-stage and high-growth companies. This segment is inherently volatile, reflecting shifts in valuation cycles and funding conditions. Despite short-term corrections, long-term investment themes remain intact. Capital continues to flow toward sectors such as artificial intelligence, fintech, and enterprise software. Venture investors are placing greater emphasis on unit economics, path-to-profitability, and capital efficiency, marking a shift from growth-at-all-costs strategies observed in prior cycles.

Real estate private equity operates within a distinct investment framework, combining asset-backed strategies with operational enhancements. Investment approaches range from core income-generating assets to opportunistic development projects. Market dynamics are influenced by interest rate movements, urbanization patterns, and shifts in demand for commercial and residential spaces. Industrial and logistics assets continue to attract capital, supported by e-commerce expansion and supply chain reconfiguration. Office and retail segments, in contrast, require more selective underwriting due to structural demand changes.

Distressed and special situations investments have gained renewed relevance amid economic uncertainty. This segment targets companies facing financial distress, liquidity constraints, or operational underperformance. Investors deploy capital alongside restructuring expertise to stabilize and reposition assets. The opportunity set expands during periods of market dislocation, when asset prices diverge from intrinsic value. Successful execution requires deep sector knowledge, legal expertise, and operational capabilities.

Other private equity strategies include growth equity, infrastructure, and private credit. Growth equity focuses on companies with established business models that require capital for expansion. These investments typically involve lower leverage and emphasize revenue scaling. Infrastructure investments provide stable, long-duration cash flows linked to essential services such as energy, transportation, and utilities. Private credit complements equity strategies by offering flexible financing solutions, often tailored to specific transaction requirements. Collectively, these strategies contribute to diversification within private equity portfolios.

By Industry

To know how our report can help streamline your business, Speak to Analyst

Rising Clear Value Creation Levers by Technology Industry to Boost Segment Growth

Based on industry, the market is segmented into technology, healthcare, consumer & retail, financial services, and others.

In 2025, the technology dominated the global market. Private equity firms continued to prioritize scalable, asset-light business models that deliver recurring revenues and strong margins, particularly in enterprise software, cybersecurity, and AI-enabled platforms. Technology deals also remained attractive due to clear value creation levers such as digital transformation, product expansion, and cross-border market penetration, which support faster growth and premium exit multiples.

- For instance, in January 2025, Blackstone and Vista Equity Partners completed the acquisition of Smartsheet, calling it an “AI-enhanced enterprise work management platform,” which highlights how large PE sponsors are prioritizing scalable software assets with recurring revenue models.

Healthcare is projected to grow at a CAGR of 17.0% over the forecast period due to rising demand for healthcare services from aging populations, increasing chronic disease burden, and sustained spending on specialized care and outpatient services.

Technology remains the dominant industry segment within the private equity market, both in terms of deal volume and value. Investments span software, cybersecurity, semiconductors, and digital platforms. The sector benefits from strong secular growth drivers, including digital transformation, cloud adoption, and automation. Private equity firms focus on scaling recurring revenue models, improving customer retention, and enhancing product innovation. Technology investments often command premium valuations, necessitating disciplined underwriting and clear value creation plans.

Healthcare represents a structurally resilient segment, supported by demographic trends and consistent demand for services. Investment areas include healthcare providers, pharmaceuticals, medical devices, and biotechnology. The sector offers defensive characteristics, with relatively stable cash flows across economic cycles. However, regulatory complexity and reimbursement frameworks require specialized expertise. Private equity sponsors are increasingly building sector-focused teams to navigate these dynamics effectively.

Consumer and retail investments have undergone a significant transformation. Changing consumer preferences, digital adoption, and evolving distribution channels are reshaping the sector. E-commerce, direct-to-consumer brands, and experiential retail concepts are key areas of focus. Private equity firms are driving value through supply chain optimization, digital marketing strategies, and brand positioning. The ability to adapt to shifting consumer behavior is critical for sustained performance.

Financial services represent another important segment, encompassing fintech, insurance, asset management, and payment systems. The sector is experiencing rapid disruption driven by technological innovation and regulatory change. Private equity investors are targeting platforms that improve efficiency, enhance customer experience, and enable scalable growth. Fintech, in particular, continues to attract significant capital due to its potential to transform traditional financial systems.

Geographic diversification is also influencing segmentation trends. Firms are allocating capital across developed and emerging markets to optimize risk-return profiles. Emerging markets offer higher growth potential but require localized expertise and risk management capabilities. Developed markets provide stability, transparency, and established exit pathways.

Another notable trend is the integration of data analytics into segmentation strategies. Firms are leveraging data to identify sector-specific opportunities, assess competitive positioning, and track performance metrics in real time. This analytical approach enhances decision-making and supports more precise capital allocation.

The interaction between type and industry segmentation is becoming increasingly important. For example, venture capital is heavily concentrated in technology, while buyout strategies dominate in industrial and business services sectors. Similarly, infrastructure investments intersect with energy and utilities, reflecting broader thematic alignment.

Environmental, social, and governance considerations are also shaping segmentation. Investors are allocating capital toward sectors and strategies that align with sustainability objectives. This includes renewable energy, healthcare access, and socially responsible business models. ESG integration is influencing both investment selection and portfolio management practices.

Private Equity Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America Private Equity Market Analysis:

North America Private Equity Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 3,008.84 billion, and also maintained the leading share in 2025, with USD 3,260.08 billion. The North America market growth is driven by the region’s deep pool of institutional capital, including pension funds, insurers, and sovereign investors, which continues to support strong fundraising and deployment. A mature ecosystem of private equity firms, advisors, and financing partners also enables higher deal activity across buyouts, growth investments, and add-on acquisitions. In addition, a large base of mid-market companies and ongoing consolidation in sectors such as technology, healthcare, and business services provides a steady pipeline of attractive targets.

North America remains the largest private equity market, supported by deep capital pools and institutional maturity. The region benefits from strong deal origination capabilities and advanced financing ecosystems. Sector concentration is evident in technology and healthcare. Operational value creation frameworks are well established. Competitive intensity is high, particularly in large-cap transactions, driving increased focus on mid-market opportunities and differentiated sourcing strategies across industries.

U.S Private Equity Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2,796.14 billion in 2025, accounting for roughly 41.0% of global Private Equity sales. The United States dominates global private equity activity, driven by a diversified corporate base and strong investor participation. Mid-market buyouts are increasingly favored due to valuation discipline. Technology, healthcare, and business services lead sector allocation. Exit activity remains linked to capital market conditions. Sponsors continue to emphasize operational improvements, supported by advanced analytics and experienced operating teams across portfolio companies.

Europe Private Equity Market Analysis:

Europe is projected to record a growth rate of 12.5% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1,628.83 billion by 2025. The European market growth is driven by a steady pipeline of mid-market businesses, particularly in countries such as the U.K., Germany, and France, where succession-led ownership transitions and consolidation opportunities remain strong. Increasing corporate carve-outs and divestitures across Europe are also creating attractive entry points for sponsors, supported by clear operational value creation levers.

Europe’s private equity market demonstrates stability, supported by regulatory consistency and cross-border investment flows. The region offers balanced exposure across industrial, consumer, and healthcare sectors. Currency volatility and macroeconomic variability require disciplined underwriting. Institutional participation remains strong. Funds are increasingly pursuing pan-European strategies, leveraging regional integration while adapting to local market conditions and regulatory frameworks across jurisdictions.

United Kingdom Private Equity Market:

The U.K. market in 2025 reached a valuation of around USD 429.63 billion, representing roughly 6.0% of global Private Equity revenues. The United Kingdom remains a leading financial hub for private equity activity. London continues to attract global capital and talent. Key sectors include financial services, technology, and consumer markets. Legal infrastructure supports complex transactions and cross-border deals. Despite macroeconomic adjustments, the market maintains strong deal flow, supported by institutional investors and established fund managers.

Germany Private Equity Market:

Germany’s market reached a valuation of approximately USD 278.15 billion in 2025, equivalent to around 4.0% of global Private Equity sales. Germany represents a core market within Europe, characterized by a strong industrial base and mid-market opportunities. Family-owned enterprises provide a consistent pipeline for buyout transactions. Investors focus on operational efficiency, automation, and export competitiveness. Regulatory stability supports investor confidence. Growth remains steady, though less aggressive than emerging markets, reflecting the country’s mature economic structure.

Asia-Pacific Private Equity Market Analysis:

Asia Pacific reached a valuation of USD 1,285.72 billion in 2025 and secured the position of the third-largest region in the market. In the region, India and China have both reached a valuation of USD 351.99 billion and USD 302.64 billion, respectively, in 2025. Asia-Pacific is the fastest-growing private equity region, driven by economic expansion and digital adoption. Growth equity and venture capital dominate investment activity. Emerging markets present significant opportunities alongside regulatory complexity. Investors focus on technology, consumer, and healthcare sectors. Long-term growth prospects remain strong, supported by favorable demographics and increasing capital formation across key economies.

Japan Private Equity Market

The Japanese market in 2025 reached a valuation of around USD 164.18 billion, accounting for roughly 2.0% of global private equity revenues. This growth is attributed to increasing corporate governance reforms and shareholder pressure that are encouraging companies to divest non-core assets and improve capital efficiency, creating more carve-out and turnaround opportunities for private equity. In addition, a large base of cash-rich but under-optimized mid-sized companies is supporting buyout activity, particularly where sponsors can drive operational modernization and digital transformation in Japan.

Japan’s private equity market is evolving, supported by corporate governance reforms and succession challenges among aging business owners. Buyout opportunities are increasing, particularly in mid-sized enterprises. Investors emphasize operational restructuring and efficiency improvements. The market remains conservative but offers stable returns. Strong industrial capabilities and technological expertise support long-term investment potential.

China Private Equity Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues reaching a valuation of USD 302.64 billion, representing roughly 4% of global Private Equity sales. China continues to attract private equity investment, particularly in technology and consumer sectors. Government policies play a significant role in shaping market dynamics. Regulatory oversight requires careful navigation. Despite geopolitical considerations, growth potential remains substantial. Investors are focusing on domestic consumption trends and innovation-driven sectors to capture long-term value creation opportunities.

India Private Equity Market

The Indian market in 2025 reached a valuation of USD 351.99 billion, accounting for roughly 5% of global Private Equity revenues.

Latin America, Middle East & Africa Private Equity Market Analysis:

Latin America offers selective private equity opportunities, supported by growing consumer markets and infrastructure needs. Economic volatility and currency risks require disciplined investment strategies. Local expertise is critical for execution. Sectors such as consumer, financial services, and energy present growth potential. The region remains underpenetrated, providing long-term opportunities for experienced investors.

The Middle East and Africa private equity market is driven by economic diversification and infrastructure development initiatives. Sovereign wealth funds play a central role in capital deployment. Market fragmentation and regulatory variability create challenges. However, sectors such as energy transition, logistics, and financial services offer long-term investment opportunities supported by structural economic reforms.

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market reached a valuation of USD 219.48 billion in 2025. owing to rising investor interest in diversification and the gradual expansion of local private capital ecosystems, supported by sovereign-backed funding and regional institutional participation.

In South America, opportunities are expanding in consumer services, agribusiness, fintech, and energy transition themes, supported by under-penetrated private equity markets and consolidation potential. In the Middle East, economic diversification programs and increasing investment into infrastructure, logistics, healthcare, and technology are creating attractive deal pipelines for private equity. In the Middle East & Africa, the GCC reached a valuation of USD 157.81 billion in 2025.

Competitive Landscape

Key Industry Players

Focus on Geographic Expansion and Cross-Border Sourcing by Key Players to Propel Market Progress

Key private equity players are increasingly focusing on geographic expansion and cross-border sourcing to access larger deal pipelines and reduce dependence on any single market cycle. By establishing regional offices and local investment teams, they can identify more attractive mid-market targets earlier and build stronger networks with founders, corporates, and advisors. Cross-border acquisitions also enable sponsors to scale their portfolio companies into new geographies, diversify revenue streams, and enhance resilience against local economic slowdowns. In addition, global sourcing enables firms to invest in high-growth sectors such as technology, healthcare, and infrastructure across multiple regions, thereby improving return potential. Overall, this expansion strategy increases deployment opportunities and accelerates market progress by enabling broader capital allocation and faster portfolio scaling.

The private equity market is characterized by a concentrated yet evolving competitive structure. Large global asset managers dominate fundraising and large-cap transactions, leveraging scale, brand credibility, and diversified investment platforms. These firms operate across multiple strategies, including buyouts, growth equity, infrastructure, and private credit, enabling flexible capital deployment and risk diversification.

Established players maintain a competitive advantage through proprietary deal sourcing networks and long-standing relationships with institutional investors. Their ability to execute complex transactions and provide operational support at scale reinforces their market position. Fundraising trends indicate continued capital concentration among top-tier managers, reflecting investor preference for consistent performance and governance standards.

Mid-sized and specialist firms are gaining traction by focusing on sector-specific strategies. These firms differentiate through deep industry expertise, enabling more precise underwriting and targeted value creation. Healthcare, technology, and industrial niches are particularly conducive to this approach. Smaller firms also demonstrate agility in sourcing proprietary deals, especially within the mid-market segment.

Partnership structures are becoming increasingly important. Co-investments and strategic alliances allow limited partners to participate directly in transactions while reducing fee burdens. At the same time, general partners benefit from additional capital flexibility and alignment with investors. Technology adoption is reshaping competitive dynamics. Firms are investing in advanced analytics, automation tools, and digital due diligence capabilities. These investments improve deal evaluation accuracy, enhance portfolio monitoring, and support operational interventions.

LIST OF KEY PRIVATE EQUITY COMPANIES PROFILED

- Blackstone (U.S.)

- KKR & Co. (U.S.)

- Apollo Global Management (U.S.)

- The Carlyle Group (U.S.)

- TPG (U.S.)

- Bain Capital (U.S.)

- Warburg Pincus (U.S.)

- Thoma Bravo (U.S.)

- Vista Equity Partner (U.S.)

- EQT (Sweden)

- CVC Capital Partners (Luxembourg)

- Advent International (U.S.)

- Permira (U.K.)

- Ardian (France)

- Hellman & Friedman (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Tata Consultancy Services (TCS) announced a strategic partnership with TPG, a global alternative asset management firm, to support the growth of its AI data center business, HyperVault. TCS’s HyperVault will be funded through a mix of equity from TCS and TPG, and debt.

- September 2025: Goldman Sachs and T. Rowe Price announced a strategic collaboration aimed at delivering a range of diversified public and private market solutions designed for the unique needs of retirement and wealth investors.

- August 2025: Achmea Investment Management introduced a new investment fund under the name Achmea IM PE Partnership Fund – Healthy People & Planet 2025. The fund offers Dutch pension funds and other institutional investors cost-efficient access to private equity investments that work for healthy people in a healthy society.

- August 2025: Blackstone entered into a definitive agreement to acquire Enverus, a premier data analytics energy intelligence platform, from Hellman & Friedman and Genstar Capital. With this acquisition, Blackstone’s private equity strategy for individual investors is expected to invest in Enverus.

- May 2024: Capital Group and KKR today announced a strategic partnership to bring new ways for investors to incorporate alternative investments into their portfolios. Capital Group and KKR intend to make hybrid public-private markets investment solutions available to investors across multiple asset classes, geographies, and channels.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.2% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Industry, and Region |

|

By Type |

· Leveraged Buyouts (LBOs) · Venture Capital · Real Estate Private Equity · Distressed and Special Situations · Others |

|

By Industry |

· Technology · Healthcare · Consumer & Retail · Financial Services · Others |

|

By Region |

· North America (By Type, By Industry, and Country) o U.S. o Canada o Mexico · Europe (By Type, By Industry, and Country) o Germany o U.K. o France o Spain o Italy o Russia o Benelux o Nordics o Rest of Europe · Asia Pacific (By Type, By Industry, and Country) o China o Japan o India o South Korea o ASEAN o Oceania o Rest of Asia Pacific · South America (By Type, By Industry, and Country) o Brazil o Argentina o Rest of Latin America · Middle East & Africa (By Type, By Industry, and Country) o Turkey o Israel o GCC o South Africa o North Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6,749.85 billion in 2025 and is projected to reach USD 20,242.70 billion by 2034.

In 2025, the market value stood at USD 3,260.08 billion.

The market is expected to exhibit a CAGR of 13.2% during the forecast period of 2026-2032.

By industry, the technology is expected to lead the market.

Growth of secondaries and continuation funds is improving liquidity and propelling the adoption of private equity.

Blackstone, KKR & Co., Apollo Global Management, The Carlyle Group, and TPG are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us