Robotaxi Market Size, Share & Industry Analysis, By Level of Autonomy (Level 4 (L4) and Level 5 (L5)), By Vehicle Type (Passenger Cars and Shuttles/Vans), By Propulsion Type (Battery Electric Vehicle (BEV) and ICE/Hybrid), By Service Type (Ride-Hailing, Station-Based, and Rental-Based), By Application (Public Mobility and Private Mobility), and Regional Forecast, 2026–2034

(Offer valid till 15th Jun 2026)

KEY MARKET INSIGHTS

The global robotaxi market size was valued at USD 0.61 billion in 2025. The market is projected to grow from USD 1.27 billion in 2026 to USD 96.31 billion by 2034, exhibiting a CAGR of 71.9% during the forecast period. North America dominated the robotaxi market with a market share of 54.09% in 2025.

A robotaxi is a fully autonomous, driverless vehicle that provides on-demand ride-hailing services, using advanced sensors, AI, and connectivity to transport passengers safely without human intervention. Market growth is driven by rising demand for autonomous mobility, advancements in AI and sensor technologies, supportive regulations, urbanization, cost efficiency, and increasing investments from automotive and technology companies.

Major players in the market include Waymo, Baidu, NVIDIA Corporation, Pony.ai, WeRide Inc., and Tesla, competing through large-scale deployments, advanced AI capabilities, strategic partnerships, and continuous innovation in autonomous driving technologies and mobility services.

Download Free sample to learn more about this report.

Robotaxi Market Key Takeaways

- 2025 Market Size: USD 0.61 billion

- 2026 Market Size: USD 1.27 billion

- 2034 Forecast Market Size: USD 96.31 billion

- CAGR: 71.9% from 2026–2034

- North America dominated the robotaxi market with a 54.09% share in 2025.

- The station-based segment is projected to grow at the fastest CAGR of 106.7% during the forecast period.

- The shuttles/vans segment is anticipated to expand at a CAGR of 99.2% over the study period.

North America

North America led the global market in 2025, supported by advanced autonomous driving infrastructure, strong investments, and early commercial robotaxi deployments.

Asia Pacific

Asia Pacific held the second-largest market share, driven by strong government support, rapid urbanization, and increasing investments in autonomous mobility solutions.

Europe

Europe is projected to be the fastest-growing region during the forecast period, supported by stringent emission regulations, smart mobility initiatives, and expanding autonomous vehicle pilot programs.

U.S.

The U.S. robotaxi market is estimated at around USD 0.67 billion in 2026, driven by strong commercialization efforts and the presence of major autonomous technology companies.

Japan

Japan’s market is estimated at approximately USD 0.001 billion in 2026, supported by smart mobility initiatives, autonomous testing programs, and growing demand for mobility solutions for an aging population.

Read More

ROBOTAXI MARKET TRENDS

Expansion of Pilot Programs and Commercial Deployments to be the Prominent Market Trends

One of the key market trends is the expansion of pilot programs into commercial deployments across major cities. Companies such as Waymo, Cruise (General Motors), Baidu, and others are transitioning from controlled testing environments to offering paid ride services in select urban areas. This shift indicates increasing confidence in autonomous driving technologies and their readiness for real-world applications. Cities are gradually allowing broader operational areas, longer operating hours, and fully driverless services. These deployments are also generating valuable real-world data, which helps improve system performance and safety.

- In March 2026, Wayve and Nissan unveiled self-driving taxis ahead of a planned pilot in Tokyo, Japan, integrating AI-first autonomous driving with camera-based perception systems. The vehicle driving leverages deep learning and real-time data processing to navigate complex urban environments, supporting scalable deployment of driverless mobility services.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Advancements In Autonomous Driving And AI Technologies Are Expected To Fuel Market Growth

Rapid advancements in autonomous driving technologies and artificial intelligence serve as a primary driver of the market. Improvements in AI algorithms, sensor fusion (LiDAR, radar, and cameras), and real-time data processing have significantly enhanced a vehicle’s ability to perceive surroundings, make decisions, and navigate complex urban environments safely. These technological developments are reducing system errors, improving reliability, and enabling higher levels of autonomy (Level 4 and beyond), which are essential for fully driverless operations.

- In February 2026, Wayve advanced its AI-first autonomous driving approach, focusing on camera-based perception and deep learning models to enable driverless vehicles. The company emphasizes scalable, data-driven systems that learn from real-world environments, supporting efficient deployment of self-driving taxis and next-generation autonomous mobility solutions.

Government Support and Smart City Initiatives to Propel Market Growth

Government support and smart city initiatives play a critical role in driving the market expansion by creating a favorable ecosystem for deployment. Autonomous vehicles require regulatory approvals, infrastructure readiness, and controlled testing environments, all of which depend on government policies. For instance, Beijing approved new autonomous vehicle regulations in January 2025, effective April 1st, 2025, explicitly supporting Level 3+ autonomous vehicle innovation, infrastructure planning, traffic management, and safety assurance.

- In March 2026, WeRide entered Slovakia through a partnership with ELEVATE Slovakia, launching the country’s first autonomous driving program. Initial testing will begin in Bratislava, expanding to Košice and the High Tatras, deploying self-driving taxis and other AVs using AI-driven perception, multi-sensor systems, and real-time data processing.

MARKET RESTRAINTS

High Development and Deployment Costs May Hamper the Product Adoption

High development and deployment costs remain a major restraint for the market. Autonomous vehicles require expensive component type such as LiDAR sensors, high-performance computing systems, advanced software stacks, and redundant safety systems to ensure reliable operation. In addition to vehicle costs, companies must invest heavily in research and development, simulation testing, real-world validation, and fleet management infrastructure.

MARKET OPPORTUNITIES

Growth of Shared Mobility and Urban Transportation Demand to Create New Growth Opportunities

The increasing demand for shared mobility and efficient urban transportation presents a significant growth opportunity for the market. Rapid urbanization, rising traffic congestion, and the need for cost-effective mobility solutions are driving consumers toward on-demand transportation services. For instance, as reported by the United Nations’ Department of Economic & Social Affairs, urban populations are expected to account for approximately 68% of the global population by 2050, increasing demand for efficient mobility solutions.

- In March 2026, Pony.ai and Chenqi Mobility launched a joint robotaxi fleet in China with over 100 Gen-7 vehicles, featuring upgraded autonomous driving systems, LiDAR radar, and AI-driven perception. The deployment supports large-scale fleet operations, real-time data processing, and accelerated commercialization of driverless ride hailing services.

MARKET CHALLENGES

Regulatory Uncertainty across Regions Challenges the Market Advancement

Regulatory uncertainty across regions significantly hampers the global robotaxi market growth by delaying deployment, increasing costs, and limiting scalability. Autonomous vehicle regulations differ widely across countries and even in the regions. For instance, in the U.S., laws are set at the state level, creating a fragmented regulatory landscape that forces companies to expand city by city rather than nationwide, henceforth, slowing commercialization.

Segmentation Analysis

By Level of Autonomy

Commercial Deployments across Urban Environments Drives L4 Segment’s Growth

Based on level of autonomy, the market is segmented into Level 4 (L4) and Level 5 (L5).

Level 4 autonomy dominates the market as L4 is witnessing rapid expansion driven by commercial robotaxi deployments across urban environments. Companies such as Waymo and Baidu are scaling operations with level 4 autonomous vehicle, supported by regulatory approvals and advancements in AI perception systems. Increasing investments, fleet expansion, and partnerships with mobility providers are accelerating adoption, particularly in North America and the Asia Pacific markets.

- In October 2025, Stellantis partnered with NVIDIA, Uber, and Foxconn to launch a global Level 4 robotaxi program, integrating NVIDIA’s AI-powered DRIVE platform, advanced sensor fusion, and high-performance computing, Stellantis’ vehicle architectures, Foxconn’s scalable manufacturing, and Uber’s fleet operations. The collaboration focuses on autonomous driving software, real-time data processing, and cloud connectivity to accelerate commercialization, enhance safety, and reduce deployment costs of driverless mobility services.

The Level 5 segment currently does not hold any market share. This segment remains in the conceptual and developmental stage, with no commercial deployments due to technological and regulatory complexities. Achieving full autonomy across all environments without human intervention requires breakthroughs in edge-case handling, computing power, and safety validation, which are still under research and testing phases.

By Vehicle Type

Fleet Scalability and Strong Demand for Urban Mobility Solutions Boosts Passenger Cars’ Leadership

Based on vehicle type, the market is segmented into passenger cars and shuttle/vans.

The passenger car segment holds the largest market share as they form the backbone of self-driving taxi deployments due to their suitability for urban ride-hailing applications. Leading robotaxi operators including Waymo, Baidu, and Cruise are primarily utilizing passenger vehicles to scale autonomous mobility services. Their cost efficiency, passenger comfort, and compatibility with existing infrastructure are driving widespread adoption across key metropolitan regions globally.

- In March 2026, Uber partnered with Rivian to launch an SUV-style robotaxi service in San Francisco, integrating advanced Level 4 autonomous driving systems with Rivian’s electric vehicle The collaboration leverages AI-powered perception, sensor fusion, and cloud-based fleet management to enhance safety and efficiency. Designed for urban ride-hailing, the service focuses on reducing emissions, optimizing vehicle utilization, and lowering operational costs while supporting scalable deployment of driverless mobility solutions.

Shuttles/vans are projected to grow at the fastest-growing CAGR of 99.2% over the forecast period. The segment is gaining traction in shared mobility and last-mile transportation use cases, particularly in controlled environments such as campuses, airports, and business districts. Their higher passenger capacity and operational efficiency make them suitable for high-density routes, supporting growing demand for cost-effective group transportation solutions in urban and semi-urban areas.

By Propulsion Type

Advancements in Battery Performance and Charging Infrastructure Expansion Drives Battery Electric Vehicle (BEV) Segment Growth

Based on propulsion type, the market is segmented into Battery Electric Vehicle (BEV) and ICE/hybrid.

The Battery Electric Vehicle (BEV) segment dominates the market and is estimated to grow with the fastest-growing CAGR over the forecast period. BEVs are the primary propulsion choice for robotaxi fleets due to their zero-emission capabilities, lower operating costs, and seamless integration with autonomous driving technologies. Waymo, Tesla, and Baidu are focusing on fully electric fleets, supported by advancements in battery performance, charging infrastructure expansion, and government incentives promoting clean mobility solutions globally.

- In March 2026, Nissan partnered with Wayve and Uber to launch a Level 4 robotaxi program using BEV platforms, integrating AI-driven autonomous software with camera-first perception systems. The collaboration focuses on scalable self-driving technology, real-time data learning, and cloud connectivity to enhance urban mobility, reduce emissions, and enable cost-efficient deployment of driverless ride-hailing services across global markets.

The ICE/hybrid segment is projected to grow at a CAGR of 32.2% over the forecast period. They serve as transitional solutions in the market, particularly in regions with underdeveloped charging infrastructure. These vehicles provide extended driving range and operational flexibility, allowing companies to deploy autonomous technologies without full reliance on electrification while supporting early-stage commercialization strategies.

By Application

Increasing Urbanization and Demand for Cost-Efficient Transportation Boost Public Mobility Segment Demand

Based on application, the market is segmented into public mobility and private mobility.

Public mobility applications dominate the market as they align with shared transportation models and urban mobility demands. Waymo, Baidu, and Uber focus heavily on ride-hailing and shared autonomous services, leveraging high utilization rates and optimized fleet operations to maximize revenue generation across densely populated cities.

- In March 2026, Waymo announced plans to launch its Level 4 robotaxi service in Dallas, deploying fully autonomous vehicles equipped with LiDAR, radar, and AI-driven perception systems. The service will leverage Waymo’s advanced driverless technology and fleet management platform to enable safe, scalable urban mobility, expand geographic coverage, and support commercial adoption of autonomous ride-hailing solutions in the U.S. market.

The private segment is estimated to expand with the fastest-growing CAGR of 100.6% over the forecast period. Private mobility is emerging as a high-growth segment driven by increasing interest in autonomous personal transportation solutions. Consumers are gradually adopting self-driving vehicles for personal use, supported by advancements in autonomous technology, improved safety systems, and growing confidence in driverless mobility solutions.

By Service Type

To know how our report can help streamline your business, Speak to Analyst

Ride Hailing Segment’s Dominance is Sustained by Advancements in Autonomous Driving Systems and Increasing Urban Congestion

Based on service type, the market is segmented into ride-hailing, station-based, and rental-based.

The ride hailing segment holds the largest market share. Ride-hailing growth is supported by increasing urban congestion and rising demand for cost-effective mobility solutions. Continuous advancements in autonomous driving systems and expansion into new geographies are further strengthening its dominance in the market.

- In March 2026, Tesla rolled out a robotaxi app update for Android users, enhancing user interface, ride-booking functionality, and real-time vehicle tracking. The update integrates Tesla’s Full Self-Driving (FSD) software, leveraging AI-based perception, neural networks, and over-the-air updates to improve autonomous ride-hailing performance, system responsiveness, and user experience in emerging operations.

The station-based segment is estimated to expand at a fastest-growing CAGR of 106.7% over the forecast period. Station-based services are gaining traction in structured environments such as airports, business parks, and transit hubs. These models enable predictable routing, efficient fleet management, and reduced operational complexity, making them attractive for early-stage deployments and integration with public transportation systems.

Robotaxi Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Robotaxi Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the robotaxi market share, supported by advanced technological infrastructure, early adoption of autonomous driving technologies, and significant investments from leading companies. The U.S. leads with large-scale commercial deployments and a strong presence of key players including Waymo and Tesla. Favorable regulatory developments in select states and increasing partnerships between tech firms and automakers are accelerating commercialization. High consumer awareness and demand for innovative mobility solutions further strengthen the region’s leading market share.

- In January 2026, Tesla launched robotaxi rides in Austin without human safety drivers, deploying vehicles powered by its Full Self-Driving (FSD) system. The service utilizes AI-based neural networks, camera-only vision systems, and over-the-air updates to enable real-time decision-making, marking a major step toward fully autonomous, scalable ride-hailing operations while improving cost efficiency and commercial viability.

U.S. Robotaxi Market

The U.S. market in 2026 is estimated at around USD 0.67 billion, accounting for roughly 53.1% of global market revenues. Growth is fueled by early commercialization, strong investments, and the presence of leading autonomous technology companies.

Asia Pacific

Asia Pacific holds the second largest share in the market, driven by strong government support, rapid urbanization, and increasing investments in autonomous mobility solutions. China and Japan are leading due to favorable regulatory frameworks and large-scale pilot deployments. The region’s high population density and rising demand for efficient urban transportation are accelerating adoption. Additionally, collaborations between technology firms and automotive OEMs are propelling innovation, contributing to steady regional market growth, and expanding commercialization opportunities.

- In December 2025, DiDi Autonomous Driving launched a 24/7 fully driverless robotaxi pilot in Guangzhou’s Huangpu district, integrating app-based dispatch, remote support, and dynamic routing. The service operates across dense urban scenarios, leveraging unmanned testing licenses and advanced AI-driven perception systems.

China Robotaxi Market

The China market in 2026 is estimated at around USD 0.56 billion, accounting for roughly 44.0% of global market revenues. Growth is driven by strong government support, large-scale pilot programs, and rapid AI advancements.

Japan Robotaxi Market

The Japan market in 2026 is estimated at around USD 0.001 billion, accounting for roughly 0.1% of global market revenues. Growth is supported by aging population needs, smart mobility initiatives, and increasing autonomous testing.

Europe

Europe is projected to be the fastest-growing region in the market, registering a CAGR of 190.3% over the forecast period. Growth is supported by stringent emission regulations, increasing focus on sustainable mobility, and strong public-private partnerships. Germany, France, and the U.K. are actively investing in smart mobility infrastructure and autonomous vehicle testing. Regulatory advancements and pilot programs across urban centers are enabling rapid deployment, while rising consumer acceptance is further fueling the regional market demand and long-term expansion.

- In June 2025, Wayve partnered with Uber to plan a Level 4 robotaxi launch in London, leveraging AI-first autonomous driving technology and camera-based perception systems. The initiative follows accelerated U.K. regulatory support, aiming to enable scalable, data-driven deployment of driverless ride-hailing services across urban environments.

U.K. Robotaxi Market

The U.K. market in 2026 is estimated at around USD 0.0006 billion, accounting for roughly 0.05% of global market revenues. Growth is driven by regulatory support, urban mobility demand, and smart city investments.

Rest of the World

The Rest of the World is witnessing gradual growth in the market, driven by increasing urban mobility challenges and growing interest in autonomous transportation. Middle East and Latin America are exploring pilot projects and smart city initiatives to integrate autonomous vehicles. Government investments in digital infrastructure and transportation modernization are supporting early adoption. Although still in nascent stages, rising awareness and strategic collaborations are expected to contribute to future market expansion.

- In March 2026, WeRide and Uber launched their first commercial Level 4 robotaxi service in downtown Abu Dhabi, UAE, deploying autonomous vehicles equipped with LiDAR, radar and AI-driven perception systems. The service leverages real-time data processing and fleet management platforms to enable safe, efficient urban mobility, and accelerate large-scale commercialization of driverless ride-hailing services.

COMPETITIVE LANDSCAPE

Key Industry Players

Collaboration, Innovation, and Rapid Commercialization Amongst Key Market Players is Driving Market Competition

The global robotaxi market features a hybrid competitive landscape of operators, technology providers, and OEM-backed platforms. It is in a scaling phase where leadership depends on deployment scale, AI capability, and regulatory approvals. Waymo and Baidu lead through large-scale operations, while NVIDIA supports the ecosystem with computing platforms. Emerging players such as Pony.ai and WeRide are expanding globally, contributing to increased competition and accelerating innovation in the market. The market remains highly dynamic, with collaboration, innovation, and rapid commercialization driving competition.

- In March 2026, Pony.ai expanded its robotaxi partnership with OnTime Mobility, deploying over 100 Gen-7 autonomous vehicles based on GAC Aion V. The system utilizes its AI Virtual Driver Level 4 platform, enabling scalable fleet operations, real-time dispatching, and large-scale commercialization.

LIST OF KEY ROBOTAXI COMPANIES PROFILED

- Waymo (U.S.)

- Tesla (U.S.)

- Baidu – Apollo Go (China)

- ai (China)

- WeRide (China)

- AutoX (China)

- Zoox (U.S.)

- Cruise (U.S.)

- Motional (U.S.)

- May Mobility (U.S.)

- DiDi Autonomous Driving (Didi Chuxing Technology) (China)

- ai (China)

- Mobileye (Israel)

- NVIDIA (U.S.)

- Hyundai Motor Company (South Korea)

- Wayve (U.K.)

- Avride (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Hyundai accelerated U.S. robotaxi expansion by mass-producing IONIQ 5 robotaxis, exporting 20 units from its Singapore plant and supplying additional vehicles domestically. Integrated with NVIDIA DRIVE Hyperion, the platform supports scalable Level 4 autonomy, while Motional’s Las Vegas pilot validates deployment, targeting fully driverless operations by late 2026.

- March 2026: Qualcomm and Wayve partnered to deliver a production-ready ADAS/AD system integrating Wayve’s AI Driver with Snapdragon Ride SoCs. The platform enables hands-off to eyes-off driving, reduces integration complexity, and supports scalable deployment, including future Level 4 robotaxi applications. February 2026: Waymo expanded its self-driving taxi service to select riders across four additional U.S. cities, accelerating its commercial rollout. The service leverages the Waymo Driver Level 4 autonomous system, combining LiDAR, radar, and vision sensors with AI-based perception and real-time decision-making.

- January 2026: Baidu launched a fully driverless robotaxi service in Abu Dhabi via Apollo Go, deploying sixth-generation RT6 vehicles. The system uses Level 4 autonomy with LiDAR, radar, and AI-based perception, operating without safety drivers in a commercially approved urban zone.

- December 2025: Uber partnered with Baidu to initiate robotaxi trials in the U.K., deploying Apollo autonomous driving technology. The system integrates AI-based perception, high-definition mapping, and sensor fusion including LiDAR and cameras to enable Level 4 autonomous ride-hailing operations.

- November 2025: Zoox launched its robotaxi service in San Francisco, offering free rides using purpose-built, bidirectional vehicles without steering wheels. The rollout included limited neighborhoods and waitlisted users, supporting validation before paid operations and scaling toward planned 10,000-vehicle annual production.

- October 2025: NVIDIA reportedly began developing a robotaxi using its DRIVE AGX Thor platform, leveraging a single continuous neural network approach. Its end-to-end stack integrates AI hardware, software, and simulation tools, supporting scalable autonomous driving and advanced ADAS development.

- November 2024: DeepRoute.ai secured USD 100 million C1 funding to advance mass-production autonomous platforms, robotaxi commercialization, and VLA model development. Leveraging NVIDIA Thor chips, it enhances semantic reasoning, enabling scalable, cost-efficient self-driving taxi deployment using production vehicles with reduced operational constraints.

REPORT COVERAGE

The global robotaxi market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 71.9% from 2026 to 2034 |

| Unit | Value (USD billion) & Volume (Units) |

| Segmentation | By Level of Autonomy, By Vehicle Type, By Propulsion Type, By Service Type, By Application, and By Region |

| By Level of Autonomy |

|

| By Vehicle Type |

|

| By Propulsion Type |

|

| By Service Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

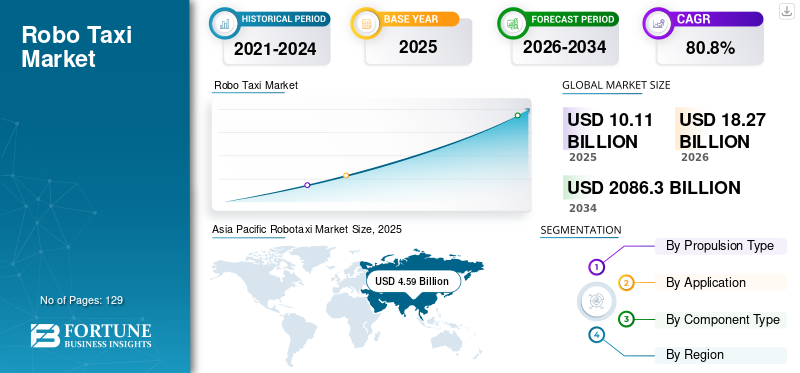

Fortune Business Insights says that the global robotaxi market size was USD 10.11 billion in 2025 and is projected to reach USD 2086.3 billion by 2034.

Fortune Business Insights says that the global market value stood at USD 0.61 billion in 2025 and is projected to reach USD 96.31 billion by 2034.

In 2025, the North American market value stood at USD 0.33 billion.

The market is expected to exhibit a CAGR of 71.9% during the forecast period.

The ride-hailing segment leads the market in terms of service type.

Advancements in autonomous driving and AI technologies are expected to fuel market growth.

Major players in the market include Waymo, Baidu, NVIDIA Corporation, Pony.ai, WeRide Inc., and Tesla.

North America holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 223

-

(Offer valid till 15th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us