Product Design & Development Services Market Size, Share & Industry Analysis, By Service Type (Product Design & Concept Development, Mechanical Engineering Services, Electronics & Embedded Systems Design, Software & Firmware Development, Prototyping & Testing Services, and Product Lifecycle Management Services), By Deployment Model (Onshore Services, Offshore Services, & Hybrid Delivery Models), By End-Use Industry (Automotive, Aerospace & Defense, Healthcare & Medical Devices, Consumer Electronics, Industrial Machinery, Energy & Utilities, and Others), and Regional Forecast, 2026-2034

Product Design & Development Services Market Size and Future Outlook

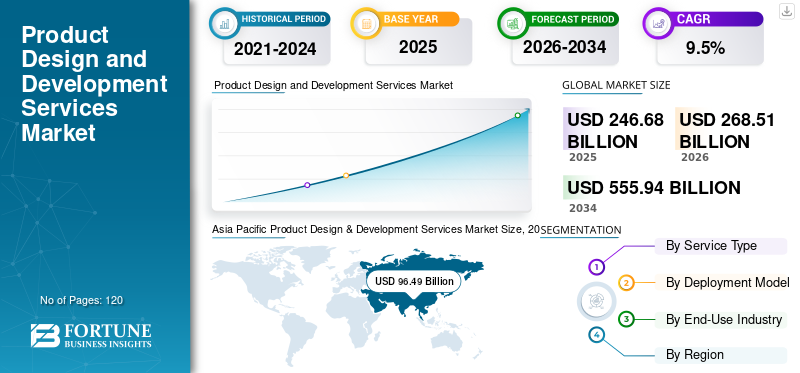

The product design & development services market size was valued at USD 246.68 billion in 2025. The market is projected to grow from USD 268.51 billion in 2026 to USD 555.94 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period. Asia Pacific dominated the product design and development services market with a market share of 39.12% in 2025.

Product design & development services are integrated engineering solutions used to conceptualize, design, validate, and industrialize complex products across automotive, aerospace, healthcare, electronics, and industrial machinery sectors. These services support end-to-end product design and development, including requirements development, system architecture engineering, and structured process validation to ensure performance, safety, and regulatory compliance. These capabilities span from mechanical architecture development, embedded electronics design, firmware engineering, digital simulation, rapid prototyping, and lifecycle data management within collaborative digital engineering environments. Advanced platforms integrate CAD/CAE tools, model-based systems engineering frameworks, digital twins, and cloud-enabled product lifecycle management systems to support commercialization, manufacturing transfer, and scalable deployment across global product programs, including in the U.S., one of the fastest growing regions for engineering innovation.

- For instance, in October 2024, Capgemini Engineering expanded its digital engineering capabilities to support automotive electrification programs across Europe, integrating model-based systems engineering and battery management platform design.

Capgemini Engineering, Tata Consultancy Services, HCLTech, L&T Technology Services (LTTS), and Accenture plc are among the key players holding a significant share of the market. Their competitive positioning is supported by comprehensive product engineering portfolios, cross-industry domain specialization, advanced digital simulation and embedded software capabilities, scalable global delivery models, and the ability to execute certification-aligned, performance-driven engineering programs across diverse high-technology manufacturing and innovation-intensive industries.

Download Free sample to learn more about this report.

PRODUCT DESIGN & DEVELOPMENT SERVICES MARKET TRENDS

Shift toward Digital Engineering Integration and Model-Based Development is Prominent Market Trend

Demand for product design & development services is increasingly shaped by OEM requirements for accelerated innovation cycles, integrated software-hardware architectures, and full digital continuity across multi-site product development programs with stringent regulatory and performance validation obligations. These evolving requirements are significantly influencing overall market dynamics, as enterprises prioritize structured requirements development, model-based systems engineering, simulation-led design, and connected lifecycle data environments to enhance product reliability and long-term maintainability. Rather than focusing solely on cost optimization, leading providers are investing in digital twin frameworks, cloud-enabled collaboration platforms, and advanced technologies such as AI to strengthen process validation, predictive performance modeling, and cybersecurity-integrated embedded development.

- For instance, in May 2024, LTTS deployed model-based systems engineering frameworks for an electric vehicle platform program incorporating digital validation and connected lifecycle analytics.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Acceleration of Electrification and Software-Defined Product Platforms Drives Market Growth

The market is witnessing accelerated expansion as rapid electrification trends, software-defined architectures, and connected device ecosystems compel OEMs and industrial manufacturers to increase investment in advanced engineering capabilities and scalable digital development frameworks. Electric vehicle programs, smart industrial equipment platforms, next-generation medical devices, and semiconductor-enabled consumer electronics are driving sustained demand for integrated mechanical, embedded, and software engineering services. Product development cycles intensified in 2024, prompting leading engineering service providers to expand model-based systems engineering adoption, simulation-driven validation, and digital twin integration to meet compressed timelines and regulatory requirements. Rising complexity across multi-domain systems architecture is reinforcing the need for end-to-end engineering partnerships capable of delivering validated, certification-ready product platforms across global innovation ecosystems.

- For instance, in February 2026, Capgemini Engineering expanded its global digital engineering centers to support software-defined vehicle and electrification programs for European and North American OEMs, integrating model-based systems engineering and AI-enabled validation frameworks to accelerate platform development timelines.

MARKET RESTRAINTS

Integration Complexity and Cross-Domain System Dependencies to Constrain Market Expansion

Unlike traditional product engineering environments, modern product design & development services must address tightly integrated mechanical, electronic, and software subsystems that operate within strict regulatory, cybersecurity, and performance compliance frameworks. Variability in system architectures, legacy platform dependencies, and customer-specific qualification standards limits rapid standardization of reusable engineering modules. Differences in embedded firmware protocols, hardware abstraction layers, safety certification requirements, and lifecycle documentation processes demands customized validation workflows and iterative integration cycles, increasing program complexity and delivery timelines. For service providers supporting automotive, aerospace, healthcare, and industrial OEMs, where performance non-conformance or regulatory misalignment can directly impact commercialization schedules and brand reputation, these technical interdependencies can slow large-scale program scaling, even amid strong underlying market growth.

MARKET OPPORTUNITIES

Rising Adoption of AI-Enabled Engineering and Software-Defined Product Platforms Creates New Market Opportunities

An emerging opportunity in the market is created by rapid adoption of AI-enabled engineering workflows, software-defined product architectures, and connected device ecosystems across automotive, healthcare, electronics, and industrial equipment sectors. OEMs are increasingly prioritizing engineering partners capable of delivering model-based systems development, embedded software integration, cybersecurity-aligned architectures, and cloud-connected lifecycle management frameworks to accelerate innovation and reduce development risk. This shift is expanding demand for product design & development services providers that can support electric vehicle platforms, intelligent medical devices, industrial automation systems, and next-generation consumer electronics programs while ensuring regulatory compliance, digital traceability, and scalable global deployment across distributed engineering environments.

- For instance, in January 2025, LTTS secured a multi-year engagement to deliver embedded systems design and lifecycle integration services for a global industrial automation manufacturer.

MARKET CHALLENGES

Increasing Multi-Domain System Complexity Hampers Market Expansion

Product design & development services providers face significant challenges arising from increasing multi-domain system complexity and evolving regulatory frameworks across automotive, aerospace, healthcare, and industrial sectors. Modern product platforms integrate mechanical components, embedded electronics, firmware layers, cloud connectivity, and cybersecurity controls, each governed by distinct validation and certification requirements. Differences in regional safety standards, industry-specific compliance mandates, and OEM-defined engineering protocols require customized workflows, extended verification cycles, and program-specific documentation controls. For service providers operating across multiple industries and geographies, repeated integration testing, software requalification, and certification reviews can extend project timelines and increase engineering costs, limiting scalability even as product innovation cycles continue to accelerate globally.

Segmentation Analysis

By Service Type

Software & Firmware Development Segment Led as it Forms Core of Software-Defined and Connected Product Architectures

By service type, the market is segmented into product design & concept development, mechanical engineering services, electronics & embedded systems design, software & firmware development, prototyping & testing services, and Product Lifecycle Management (PLM) services.

Software & firmware development held the largest product design & development services market share as it forms the digital backbone of modern software-defined products across automotive, healthcare, consumer electronics, and industrial automation sectors. These services integrate application software development, embedded firmware programming, real-time operating systems, cybersecurity layers, and cloud connectivity frameworks within unified digital engineering environments, enabling intelligent functionality, remote diagnostics, and continuous product updates. As OEMs increasingly prioritize connected ecosystems, over-the-air update capabilities, data-driven performance optimization, and cybersecurity compliance, software-centric engineering programs are becoming a strategic investment focus for enterprises seeking to accelerate innovation cycles while ensuring regulatory alignment and long-term lifecycle adaptability under evolving technology standards.

- In August 2025, L&T Technology Services launched PLxAI, its proprietary GenAI framework to accelerate product development lifecycles, enabling embedded and software product engineering clients to enhance design, validation, and digital twin integration workflows across mobility, sustainability, and tech segments.

Electronics & embedded systems design plays a critical role in enabling intelligent device functionality across automotive electrification platforms, semiconductor-enabled equipment, and connected medical technologies and is growing at a CAGR of 10.2%. Embedded systems engineering is witnessing accelerated growth driven by increasing demand for sensor integration, power electronics control units, edge computing modules, and safety-certified hardware architectures supporting next-generation connected and electrified product ecosystems.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Model

Hybrid Delivery Models Segment Led as Enterprises Prioritize Scalable and Globally Distributed Engineering Execution

By deployment model, the market is segmented into onshore services, offshore services, and hybrid delivery models.

Hybrid delivery models held the largest share of the market, driven by their widespread adoption across automotive, electronics, healthcare, and industrial manufacturing programs where scalability, cost optimization, and domain specialization are critical. These models integrate onshore client-facing engineering teams with offshore development centers, enabling synchronized collaboration across mechanical design, embedded systems engineering, software development, and lifecycle management environments. Their ability to balance proximity-driven innovation with global cost efficiency significantly enhances program flexibility, accelerates time-to-market, and reduces execution risk. As product complexity increases and OEMs seek continuous engineering support across multi-region development cycles, hybrid delivery structures continue to serve as the core operational framework for large-scale, multi-domain product engineering engagements, reinforcing their dominance in overall market consumption.

Offshore services segment is expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 9.7%, supported by rising demand for cost-competitive engineering talent, expanding ER&D centers in Asia Pacific, and increasing digital collaboration maturity. Growing emphasis on cloud-enabled engineering platforms, secure development environments, and standardized validation workflows is driving enterprises to expand offshore engineering footprints while maintaining governance oversight through integrated global delivery networks.

By End-Use Industry

Extensive Deployment in Electrification and Connected Vehicle Programs Led to Automotive Segmental Dominance

Based on end-use industry, the market is segmented into automotive, aerospace & defense, healthcare & medical devices, consumer electronics, industrial machinery, energy & utilities, and others.

Automotive accounts for the highest share of the market, driven by extensive utilization of engineering services across electric vehicle platforms, advanced driver assistance systems, power electronics integration, and connected mobility architectures. Automotive development environments require cross-domain coordination of mechanical systems, embedded electronics, firmware layers, and software-defined control platforms, making integrated product engineering partnerships a strategic investment priority. Vehicle programs are characterized by compressed innovation cycles, global regulatory compliance requirements, and platform-based development strategies, requiring service providers to deliver scalable, digitally enabled, and validation-ready engineering solutions. As electrification accelerates and software-defined vehicle architectures expand across global OEM portfolios, automotive continues to represent the primary consumption base of overall product design & development services demand.

The healthcare & medical devices segment is expected to register highest growth rate during the study period, expanding at a CAGR of 11.3%, supported by increasing investments in connected diagnostics, wearable medical technologies, and minimally invasive device innovation. Development of next-generation medical platforms requires precision mechanical design, embedded firmware validation, regulatory documentation support, and lifecycle traceability under strict compliance standards, driving accelerated adoption of specialized product engineering services across global healthcare ecosystems.

Product Design & Development Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

North America

Asia Pacific Product Design & Development Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 74.05 billion in revenue in 2025, supported by a highly concentrated base of automotive OEMs, semiconductor design centers, medical device manufacturers, and industrial automation companies across the U.S., Canada, and Mexico. Regional demand is structurally tied to electric vehicle platform development, software-defined product architectures, and advanced manufacturing digitization initiatives that rely heavily on integrated mechanical, embedded, and software engineering capabilities. Automotive and industrial enterprises in the region increasingly utilize model-based systems engineering, digital twin validation frameworks, and cloud-connected lifecycle management platforms to accelerate innovation cycles. The region also exhibits a significant installed base of legacy product platforms undergoing modernization through embedded upgrades, cybersecurity enhancements, and connected feature integration. Ongoing electrification programs, semiconductor ecosystem expansion, and industrial digital transformation initiatives continue to sustain consistent engineering expenditure toward scalable, high-complexity product development programs across North America.

U.S. Product Design & Development Services Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 68.97 billion in 2026, driven by its concentration of global automotive headquarters, advanced semiconductor R&D hubs, medical technology innovators, and large-scale industrial equipment manufacturers. Unlike cost-focused engineering sectors, U.S. enterprises emphasize high-value, innovation-led product development requiring synchronized execution across mechanical architecture design, embedded systems integration, firmware validation, and cybersecurity compliance. Large engineering programs increasingly incorporate AI-assisted simulation, over-the-air software frameworks, and digitally integrated lifecycle management systems to ensure regulatory alignment and continuous product improvement. Continuous investments in electrification, autonomous mobility technologies, smart medical platforms, and industrial IoT ecosystems are reinforcing modernization of existing engineering infrastructures.

Europe

The European market is supported by a distributed and innovation-driven industrial ecosystem, particularly across automotive engineering clusters in Germany, embedded systems development hubs in France, advanced manufacturing centers in Italy and Spain, and semiconductor-aligned design activity in the Netherlands and Nordic countries. Demand for product design & development services is closely tied to electric vehicle platform engineering, industrial automation modernization, connected medical device development, and next-generation consumer electronics innovation programs. Unlike centralized engineering structures, Europe’s cross-border product development architecture requires collaborative digital platforms capable of supporting multi-country design validation, regulatory alignment, and lifecycle data synchronization across segmented R&D facilities. Stringent safety certification standards, sustainability-focused product regulations, and digital continuity mandates are accelerating investment in model-based systems engineering, simulation-driven validation frameworks, and cloud-enabled product lifecycle management environments. Countries such as Germany, France, the U.K., Italy, Spain, and the Netherlands lead regional adoption, supported by strong automotive OEM presence, advanced industrial automation capabilities, and export-oriented high-technology manufacturing programs.

U.K. Product Design & Development Services Market

The U.K. market in 2026 is estimated at around USD 9.54 billion, representing roughly 3.6% of global sales.

Germany Product Design & Development Services Market

Germany’s market is projected to reach approximately USD 18.46 billion in 2026, equivalent to around 6.9% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market and generated revenue of USD 96.49 billion in 2025. Market expansion is primarily driven by rapid electrification programs, semiconductor ecosystem expansion, and large-scale industrial digital transformation initiatives across major economies. China’s growth is closely linked to domestic electric vehicle platform engineering, consumer electronics innovation, and expanding semiconductor design capabilities, while Japan’s demand is supported by advanced automotive systems development, robotics engineering, and precision industrial automation programs integrated into global manufacturing supply chains. India, South Korea, and ASEAN countries are emerging contributors as regional governments promote electronics manufacturing, EV ecosystem investments, and engineering R&D center expansion to strengthen product innovation capacity and global technology competitiveness.

China Product Design & Development Services Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 46.31 billion, representing roughly 17.2% of global sales.

Japan Product Design & Development Services Market

The Japan market in 2026 is estimated at around USD 14.23 billion, accounting for roughly 5.3% of the global sales.

India Product Design & Development Services Market

The India market in 2026 is estimated at around USD 20.08 billion, accounting for roughly 7.5% of the global revenue.

Middle East & Africa

The Middle East & Africa market is driven by economic diversification strategies, industrial digitalization programs, and expanding high-technology manufacturing activity, particularly across the GCC, Israel, and select North African economies. Government-backed investments in semiconductor design initiatives, electric mobility programs, smart infrastructure, and advanced healthcare technologies are supporting demand for product design & development services across mechanical, embedded, and software engineering domains. The GCC benefits from high-capex, specification-driven industrial and energy projects requiring digitally integrated engineering solutions, secure development environments, and lifecycle management frameworks, while Israel demonstrates strong demand supported by semiconductor innovation, defense electronics engineering, and medical device R&D ecosystems. North Africa is witnessing gradual expansion of automotive and electronics manufacturing aligned with European supply chains, while parts of Sub-Saharan Africa are observing incremental adoption of engineering services driven by industrial modernization and infrastructure development initiatives.

GCC Product Design & Development Services Market

The GCC market is projected to reach around USD 5.69 billion in 2026, representing roughly 2.1% of the global sales.

South America

The South America market is supported by the region’s expanding automotive production base, industrial machinery manufacturing footprint, and gradually strengthening electronics and healthcare device ecosystems, particularly in Brazil and Argentina, which serve as key hubs for product engineering and advanced manufacturing activity. Brazil’s electric vehicle development initiatives, industrial automation programs, and consumer electronics assembly operations represent the primary drivers of demand for product design & development services, supported by engineering activities requiring integrated mechanical design, embedded systems development, and software validation capabilities. While overall engineering expenditure remains lower compared to North America and Europe, export-oriented automotive production and participation in global supply chains are encouraging investment in digitally integrated product development frameworks and lifecycle management systems. Argentina and few other regional markets are gradually modernizing engineering infrastructure to enhance design efficiency, reduce reliance on imported technology platforms, and align with international safety, compliance, and performance standards across diversified industrial sectors.

Brazil Product Design & Development Services Market

The Brazil market is projected to reach around USD 5.32 billion in 2026, representing roughly 2.0% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Engineering Depth, Domain Expertise, and Long-Term OEM Partnerships Leads to Growing Market Competition

The product design & development services market is moderately consolidated, with competitive positioning shaped less by the breadth of service portfolios and more by depth of domain expertise, cross-industry engineering integration capability, and long-term participation in complex product development programs. Leading players such as Capgemini Engineering, Tata Consultancy Services, HCLTech, L&T Technology Services (LTTS), and Accenture plc maintain strong market positions by delivering integrated mechanical, embedded, and software engineering solutions tailored to automotive, healthcare, industrial, and electronics innovation environments. Their competitive strength is reinforced by advanced digital engineering frameworks, model-based systems integration capabilities, regulatory-aligned validation processes, and the ability to execute multi-year global engineering programs under compressed development timelines.

Competitive differentiation is increasingly driven by a provider’s ability to enable software-defined architectures, integrate cybersecurity and digital twin capabilities into product lifecycles, and manage complex multi-domain system development requirements rather than by service scale alone. As OEMs prioritize execution reliability, digital continuity, and long-term lifecycle optimization, product design & development services leaders are strengthening in-house domain consulting, AI-assisted engineering platforms, and global delivery integration capabilities to protect strategic client relationships and elevate switching barriers for emerging competitors.

- For instance, in January 2026, Capgemini was recognized as a Leader in Connected Product Engineering Services by an independent research firm, reinforcing its competitive positioning in end-to-end digital engineering and lifecycle management services.

LIST OF KEY PRODUCT DESIGN & DEVELOPMENT SERVICES COMPANIES PROFILED

- Capgemini Engineering (France)

- Tata Consultancy Services (TCS) (India)

- Infosys Engineering Services (India)

- HCLTech (India)

- L&T Technology Services (LTTS) (India)

- Wipro Engineering Edge (India)

- Cognizant Engineering Services (U.S.)

- Accenture plc (Ireland)

- Cyient Ltd. (India)

- EPAM Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: TCS and AMD expanded their strategic collaboration to co-develop a rack-scale AI infrastructure (“Helios”) designed to accelerate AI-driven engineering workloads and support sovereign AI factories, strengthening development platforms that underpin advanced engineering services.

- January 2026: HCLTech announced it will showcase cutting-edge Physical AI capabilities at the World Economic Forum 2026, underlining ongoing investment in advanced engineering frameworks broadly applicable to product design, embedded systems, and digital engineering innovation.

- September 2025: Tata Consultancy Services (TCS) launched chiplet-based system engineering services to accelerate semiconductor innovation and support next-generation chip design capabilities, enabling system-level integration and verification for advanced product platforms.

- June 2025: L&T Technology Services inaugurated a new Engineering Design Center in Plano, Texas, creating hundreds of high-skilled jobs and strengthening AI-enabled, digital manufacturing, cybersecurity, and engineering delivery capabilities close to clients in advanced product development markets.

- January 2025: L&T Technology Services secured a multiyear USD 80 million digital engineering transformation deal with a U.S.-based industrial products manufacturer, establishing a Center of Excellence to support connected products, digital thread integration, and product lifecycle management services globally.

REPORT COVERAGE

The global product design & development services market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Deployment Model, End-Use Industry and Region |

| By Service Type |

|

| By Deployment Model |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 268.51 billion in 2026 and is projected to reach USD 555.94 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 96.49 billion.

The market is expected to exhibit a CAGR of 9.5% during the forecast period (2026-2034).

By end-use industry, the automotive segment leads the market.

Electrification growth, software-defined architectures, embedded complexity, and digital lifecycle integration demand drive market expansion.

Capgemini Engineering, Tata Consultancy Services (TCS), Infosys Engineering Services, HCLTech, and L&T Technology Services (LTTS) are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us