Pumps Market Size, Share & Industry Analysis, By Pump Type (Centrifugal Pumps and Positive Displacement Pumps {Reciprocating Pumps, Rotary Pumps, and Dosing Pumps}), By Operation Type (Electric Motor-Driven Pumps and Engine-Driven Pumps (Diesel/Gas)), By End-User (Water & Wastewater, Oil and Gas {Upstream, Midstream, and Downstream}, Power Generation, Chemical & Petrochemicals, Mining and Minerals, HVAC & Building Services, Food & Beverage, Pulp & Paper, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

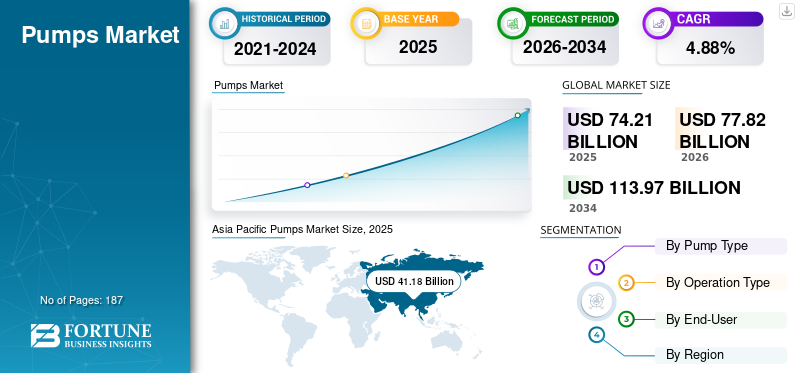

The global pumps market size was valued at USD 74.21 billion in 2025. The market is projected to grow from USD 77.82 billion in 2026 and is expected to reach USD 113.97 billion by 2034, exhibiting a CAGR of 4.88% during the forecast period. Asia Pacific dominated the global pumps market with a market share of 55.49% in 2025.

Pumps are essential mechanical devices used to move fluids by converting mechanical energy into hydraulic energy, enabling fluid transfer, circulation, and pressure boosting across a wide range of applications. They play a critical role in infrastructure and industrial systems, including water and wastewater management, oil & gas operations, power generation, chemical processing, HVAC systems, mining, food & beverage processing, and building services. The global market is a mature yet steadily evolving segment of the industrial equipment landscape, driven by continuous demand from both essential utilities and process industries.

Demand for pumps is expected to grow steadily due to expanding urbanization, rising investments in water and wastewater infrastructure, increasing industrial activity in emerging economies, and the need for energy-efficient solutions for fluid handling. Stricter energy efficiency regulations, growing adoption of smart and automated pumping systems, and rising replacement demand for aging installed bases are further supporting market growth. Additionally, climate resilience initiatives, desalination projects, and increased focus on process optimization across industries are contributing to sustained pump demand globally.

Leading companies, such as Grundfos, Flowserve, Sulzer, KSB, Xylem, and others, are shaping the market through continuous innovation, global manufacturing scale, and robust service networks. Major players are investing in high-efficiency motor technologies, digital monitoring and predictive maintenance solutions, advanced materials, and application-specific pump designs to improve reliability, reduce lifecycle costs, and enhance operational efficiency. Expansion into emerging markets, growth in aftermarket services, and the integration of IoT-enabled pumping solutions remain key strategic priorities across the competitive landscape.

Download Free sample to learn more about this report.

Pumps Market Key Takeaways

- 2025 Market Size: USD 74.21 billion

- 2026 Market Size: USD 77.82 billion

- 2034 Forecast Market Size: USD 113.97 billion

- CAGR: 4.88% from 2026–2034

- Asia Pacific dominated the global pumps market with a market share of 55.49% in 2025.

- Positive displacement pump is projected to grow at a CAGR of 5.31% during the forecast period.

- Engine-driven pump is projected to grow at a CAGR of 3.36% during the forecast period.

Asia Pacific

Asia Pacific generated USD 41.18 billion in 2025, driven by large-scale water infrastructure projects, industrial expansion, and growing construction activity.

Europe

Europe accounted for USD 13.56 billion in 2025, supported by energy-efficiency upgrades, water infrastructure modernization, and demand from process industries.

North America

North America reached USD 11.06 billion in 2025, benefiting from replacement demand, industrial automation, and investments in cooling infrastructure.

U.S.

The market was valued at USD 9.74 billion in 2025 and is supported by extensive water & wastewater assets, industrial processing operations, and demand for high-reliability pumping systems.

Japan

Demand is driven by replacement cycles, reliability enhancements, and the adoption of energy-efficient pumping solutions across industrial and commercial applications.

Read More

Pumps Market Trends

Shift Toward Smart Monitoring and Predictive Maintenance is a Major Trend in Market

The market is seeing a clear shift toward high-efficiency and digitally enabled pumping systems as end-users prioritize lower energy consumption, reduced lifecycle costs, and improved reliability. Since pumps account for a significant share of electricity use in water networks, HVAC systems, and many industrial processes, operators are increasingly replacing legacy fixed-speed units with high-efficiency motors, variable frequency drives (VFDs), and system-optimized pump designs that better match actual demand, rather than running at a constant load.

Overall, this trend reflects the transition of pumps from purely mechanical assets into “connected” efficiency equipment, where sensors, remote monitoring, and predictive maintenance help minimize unplanned downtime, reduce energy waste, and extend asset life. As efficiency regulations tighten and industrial facilities push for automation and decarbonization, smart and energy-efficient pumping solutions are becoming a standard specification across water & wastewater, building services, and process industries, strengthening long-term replacement and upgrade demand.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Expansion of Cooling Demand in Buildings and Data Centers is Supporting HVAC Pump Growth

Cooling and circulation requirements are expanding as commercial building stock grows and as data centers scale globally. HVAC circulation pumps are critical for chilled water, condenser water, and district energy systems, making them a consistent demand driver in both new construction and retrofit projects.

Importantly, many HVAC systems are being redesigned around variable flow and intelligent controls, which increases demand for VFD-compatible, high-efficiency pumps and integrated control packages. For instance, in November 2025, Vertiv announced the acquisition of PurgeRite specifically to strengthen its liquid-cooling services for data centers—an investment tied to surging AI-driven thermal loads and the need for more efficient, lower-emission cooling infrastructure, which ultimately depends on pumped liquid loops and upgraded HVAC systems.

Market Restraints

High Installation Complexity and System Integration Challenges in Pumping Systems

Pump systems are often perceived as more complex to design and integrate compared to simpler mechanical or passive alternatives, particularly in environments with extensive retrofit requirements. Unlike standalone equipment, pumps must be carefully matched with piping networks, valves, controls, motors, and process conditions to achieve reliable and efficient operation. Improper sizing, hydraulic imbalance, or poor integration with existing infrastructure can lead to cavitation, excessive energy consumption, vibration, and premature failures—making system-level engineering critical rather than optional.

These challenges are most pronounced in retrofit projects, where legacy piping layouts, space constraints, outdated controls, and non-standard operating conditions increase installation effort and cost. In large industrial, water, and district energy applications, complexity further rises due to requirements for redundancy, safety interlocks, pressure management, variable flow operation, and integration with SCADA or building management systems. As a result, longer design cycles and higher engineering costs can delay decision-making and, in some cases, limit the adoption of advanced or higher-efficiency pumping solutions.

Market Opportunities

District Energy, Cooling Networks, and Large-Scale Water Infrastructure are Creating Scalable Growth Opportunities for Pumps

Expansion of district heating and cooling networks, centralized cooling plants, and large-scale water infrastructure represents a high-impact growth opportunity for the global market. These systems rely heavily on high-capacity circulation pumps, booster pumps, and redundancy-driven designs to move large volumes of water or thermal fluids efficiently across urban networks. As cities pursue decarbonization, resilience, and energy efficiency, investments in district energy and centralized utility systems are accelerating.

In particular, district cooling and integrated heating and cooling systems are gaining traction in dense urban areas, commercial hubs, and data center clusters. These projects favor long-life, high-efficiency pumps paired with variable-speed operation and advanced control strategies. For pump suppliers, this creates opportunities not only in equipment sales but also in engineered packages, system optimization, and lifecycle services, as utilities prioritize reliability, performance guarantees, and long-term operating cost reduction.

Market Challenges

Skilled Labor and Engineering Capability Gaps Are Emerging as a Key Execution Challenge in Market

A rising constraint in the global pumps market growth is not the availability of equipment, but rather the shortage of skilled personnel who can correctly specify, integrate, commission, and maintain modern pumping systems. Pumps are increasingly operated as part of a system, featuring VFDs, sensors, automation logic, energy-optimization controls, and tighter reliability requirements. That shift widens the gap between “basic installation” (getting a pump running) and “best-practice system performance” (running it efficiently, reliably, and within design envelopes). When the right skills are missing, buyers may delay upgrades, avoid advanced solutions, or accept underperforming installations that fail to deliver expected savings and uptime.

This challenge is especially visible in regions and end-users facing workforce constraints—utilities with aging staff, contractors dealing with turnover, and multi-site industrial operators operating with lean maintenance teams. It is also amplified by decentralization trends (distributed booster stations, remote mining sites, municipal pumping stations, packaged skids), where fewer specialists are available on-site and troubleshooting must happen quickly.

Segmentation Analysis

By Pump Type

Centrifugal Pumps Dominate Market Due to Broad Applicability and Strong Replacement Demand

Based on pump type, the global market is segmented into centrifugal pumps and positive displacement pumps (sub-segmented into reciprocating, rotary, and dosing pumps).

Centrifugal pumps represent the largest global pumps market share as they are the default technology for high-volume fluid movement in various applications, including water & wastewater, HVAC circulation, power generation, and general industrial services. Their scalability across a wide range of flow rates, broad availability, and relatively lower upfront cost make them the preferred choice for both greenfield projects and the vast installed base replacement cycle. Additionally, demand is reinforced by system upgrades such as VFD adoption and energy-efficiency retrofits, which are typically implemented first in centrifugal pump-heavy applications (water networks, building circulation, and industrial utilities).

Positive displacement pumps represent a structurally important and steadily expanding segment, supported by applications where flow accuracy, pressure stability, and the handling of viscous or shear-sensitive fluids are critical. While PD pumps are smaller in total value compared with centrifugal pumps, they often command higher specification intensity in process industries. Growth is driven by tighter dosing requirements in water treatment, chemicals, food & beverage, and by expanding process automation where precise metering and controlled injection are needed. The positive displacement pump is projected to grow at a CAGR of 5.31% during the forecast period.

By Operation Type

Electric Motor-Driven Pumps Dominate Market Due to Their Efficiency, Lower Operating Cost, and Broad Grid Availability

Based on operation type, the market is segmented into electric motor-driven pumps and engine-driven pumps (diesel/gas).

Electric motor-driven pumps dominate the global market and are expected to remain the primary operating mode, as they deliver the best combination of energy efficiency, controllability, and lower lifecycle costs for continuous-duty applications. Electric pumps are the standard choice across water & wastewater, HVAC/building services, chemical processing, power generation, and most industrial utilities, where infrastructure is fixed, and power supply is available. This dominance is reinforced by the accelerating adoption of variable frequency drives (VFDs) and automation, which are far easier to implement and optimize on electric pump systems.

Engine-driven pumps (diesel/gas) represent a smaller but strategically important segment, primarily serving applications where grid power is unavailable, unreliable, or where mobility is required. These pumps are widely used for construction dewatering, mining dewatering in remote sites, emergency flood control, temporary bypass pumping in municipal networks, irrigation in off-grid areas, and certain oil & gas field operations. In these scenarios, the value proposition is not energy efficiency but deployment speed, independence from grid infrastructure, and operational resilience. The engine-driven pump is projected to grow at a CAGR of 3.36% during the forecast period.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Water & Wastewater Dominates Market Due to Large Installed Base and Non-Discretionary Infrastructure Spending

Based on end-user, the global market is segmented into water & wastewater, oil & gas (upstream/midstream/downstream), power generation, chemical & petrochemicals, mining & minerals, HVAC & building services, food & beverage, pulp & paper, and others.

Water & wastewater is the leading end-user segment globally. It remains the most structurally resilient source of demand as pumping is fundamental to intake, transmission, distribution, booster stations, sewage lift stations, and treatment operations. Utilities operate one of the world’s largest installed bases of pumps, and replacement cycles are continuous due to wear, corrosion, and reliability requirements. Demand is further supported by urbanization, network expansion, regulatory compliance for wastewater treatment, and growing focus on leakage reduction and energy optimization. Since water infrastructure spending is typically non-discretionary, this segment tends to provide stable, long-duration demand in both developed and emerging markets.

Oil & gas is a major value-driving segment, particularly in midstream and downstream operations where pumps are critical for pipelines, terminals, refining, and petrochemical integration. Although project cycles can be more volatile than those of municipal infrastructure, pumps in the oil & gas industry frequently require higher specifications (in terms of materials, seals, and pressure capability), which increases the value per unit. Upstream applications also contribute through injection, transfer, and field services; however, the segment is overall influenced by capital expenditure (capex) cycles, energy price conditions, and regional investment priorities. The oil and gas segment is expected to grow at a CAGR of 4.95% during the forecast period.

Pumps Market Regional Outlook

By geography, the market has been studied geographically across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Pumps Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific was the largest region in 2025, valued at USD 41.18 billion, accounting for roughly 55.5% of global market revenues. The demand is supported by the region’s scale of municipal water infrastructure development, industrial capacity expansion (including chemicals and manufacturing), and high levels of construction-related pumping needs. Asia Pacific also benefits from strong momentum in energy efficiency upgrades and the rising need for reliable cooling and circulation systems across commercial buildings and expanding data center ecosystems.

China Pumps Market

China remained the dominant contributor within the Asia Pacific region, with a valuation of USD 18.88 billion in 2025, and is expected to reach USD 19.85 billion in 2026. The scale of industrial process pumping, municipal water investments, and broad installed base replacement—making it the primary contributor to regional volumes and upgrades.

India Pumps Market

India is among the fastest-growing country markets in the Asia Pacific region, supported by infrastructure expansion (water & wastewater), industrialization, and the increasing penetration of efficient motor-driven/VFD-enabled systems in municipal and building applications.

Japan Pumps Market

Japan is a mature but high-value market where replacement cycles, reliability upgrades, and energy-efficient circulation systems in industrial and building services strongly drive demand.

North America

North America reached USD 11.06 billion in 2025, contributing approximately 14.9% of the global market revenues. The region is supported by a large installed base across municipal water systems, oil & gas value chain assets, chemicals, and building services—resulting in steady replacement demand and upgrades for energy efficiency and reliability. Demand is also strengthened by industrial automation, the adoption of predictive maintenance, and continued investments in cooling infrastructure for large facilities.

U.S. Pumps Market

The U.S. market was valued at USD 9.74 billion in 2025 and is set to reach USD 10.19 billion in 2026, accounting for roughly 13% of the global market size. The market is growing due to the scale of water & wastewater assets, industrial processing footprint, and high demand for engineered and high-reliability pump systems across multiple end-users

Europe

Europe was valued at USD 13.56 billion in 2025, accounting for approximately 18.3% of global revenues. Growth in Europe is largely driven by replacement and retrofit, with energy-efficiency upgrades (such as VFD adoption and optimized systems), the modernization of water infrastructure, and continued demand from the chemicals, process industries, and district energy/cooling systems. A strong focus on lifecycle costs and high specification requirements in regulated and safety-sensitive industrial applications also shapes Europe’s market.

Germany Pumps Market

Germany's market was valued at USD 2.67 billion in 2025 and is projected to reach USD 2.77 billion in 2026. Germany is the dominant market in Europe, supported by the depth of its industrial base (chemicals, manufacturing), high installed base, and strong retrofit orientation toward energy-efficient pumping systems.

U.K. Pumps Market

The U.K. was valued at USD 2.01 billion in 2025, accounting for approximately 3% of the global market. The U.K. market is driven by building retrofit activity (HVAC circulation upgrades), investments in water network resilience, and modernization across municipal and industrial utilities.

Latin America

Latin America was valued at USD 3.42 billion in 2025, accounting for approximately 4.6% of global revenues. The growth is supported by municipal water and wastewater expansion, industrial activity in select hubs, and project-driven demand from mining and oil & gas in specific countries. However, adoption of higher-efficiency and digitally enabled pumping solutions can be constrained by budget cycles and execution capacity, making demand relatively more cyclical than in developed regions.

Middle East & Africa

The Middle East & Africa market was valued at USD 4.98 billion by 2025, accounting for approximately 6.7% of global pump revenues. The demand is supported by investments in water security (including desalination-related systems, where applicable), municipal infrastructure expansion, and industrial activity. In the Middle East, pumping demand is also closely tied to oil & gas, petrochemical complexes, and large-scale utilities, while water access projects, mining activity, and infrastructure development drive parts of Africa.

GCC Pumps market

The GCC was valued at USD 2.45 billion by 2025, accounting for around 3.3% of the global market.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Energy Efficiency and VFD Integration are Becoming Default Specification in Market

The global pumps market is moderately fragmented, with a combination of large multinational OEMs and strong regional manufacturers supplying pumps, motors, drives, controls, and packaged pumping solutions tailored to local infrastructure conditions, end-user requirements, and regulatory environments. Major pump manufacturers are actively investing in hydraulic design optimization, VFD-ready pump architectures, and integrated control platforms to ensure pumps operate closer to real demand rather than constant-speed conditions. For instance, in October 2023, Xylem introduced hydrovar X as part of its push toward fully integrated, digitally enabled pumping solutions, combining an ultra-premium efficiency motor, an embedded variable frequency drive, and native connectivity to allow pumps to dynamically match real system demand rather than operate at a constant speed. This launch clearly illustrates how leading pump manufacturers are investing in hydraulic optimization, VFD-ready architectures, and integrated control platforms to deliver measurable energy savings and simplified commissioning.

List of Key Pump Companies Profiled

- Grundfos (Denmark)

- Xylem Corporation (U.S.)

- Flowserve (U.S.)

- KSB (Germany)

- Sulzer (Switzerland)

- Wilo Corporation (Germany)

- Ebara Corp. (Japan)

- The Weir Group (U.K.)

- Pentair (Ireland)

- ITT Inc. (U.S.)

- Kirloskar Brothers Limited (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Sulzer expanded its BlueLinQ™ digital ecosystem with new energy-optimization and condition-monitoring modules specifically tuned for water transport and industrial process pumps, enabling real-time efficiency tracking, variable-speed optimization, and predictive maintenance insights. The update highlights how major pump OEMs are enhancing integrated digital and VFD-enabled platforms to enable customers to operate pumps closer to system demand, reduce energy losses, and extend asset life, rather than relying on constant-speed operation.

- August 2025: Wilo launched the Wilo-Stratos GIGA2.0-I, positioning it as a smart, high-efficiency vertical in-line pump for HVAC and industrial duties, built around an IE5 electronically commutated motor and “system optimization” intelligence, reinforcing the industry shift toward high-efficiency, digitally enabled, variable-speed circulation platforms rather than fixed-speed designs.

- July 2025: Grundfos announced the rollout of a new generation of TPE3 in-line pumps, highlighting IE5-class MGE motors, improved hydraulics, and intelligent functions aimed at lowering energy consumption and lifecycle costs, directly aligning with the trend of hydraulic optimization and VFD-ready architectures becoming standard in HVAC/district energy circulation.

- March 2025: Xylem introduced the e-1531X Smart Pump, emphasizing an integrated motor and control package, as well as scalable system controls (including multi-pump control), designed to improve system performance and reduce energy use. This is a clear example of OEMs pushing integrated, “out-of-the-box” smart pumping solutions.

- February 2025: KSB announced the launch of the MultiTec Plus high-pressure pump series, developed with a focus on optimized hydraulic efficiency for drinking water transport and designed to pair with variable-speed operation. This illustrates how major players are engineering efficiency-first platform renewals for core municipal applications.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects, including leading companies, product processes, and Porter’s Five Forces analysis. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.88% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Pump Type o Centrifugal Pumps o Positive Displacement Pumps · Reciprocating Pumps · Rotary Pumps · Dosing Pumps |

|

By Operation Type · Electric Motor-Driven Pumps · Engine-Driven Pumps (Diesel/Gas) |

|

|

By End-User o Water & Wastewater o Oil and Gas · Upstream · Midstream · Downstream o Power Generation o Chemical & Petrochemicals o Mining and Minerals o HVAC & Building Services o Food & Beverage o Pulp & Paper o Others |

|

|

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 74.21 billion in 2025.

The market is likely to grow at a CAGR of 4.88% over the forecast period (2026-2034).

By end-user, the water & wastewater segment leads the market.

The market size of the Asia Pacific stood at USD 41.18 billion in 2025.

Expansion of cooling demand in buildings and data centers is supporting HVAC pump growth.

Some of the top players in the market include Grundfos, Xylem Corporation, Flowserve, and KSB, among others, who are leading players.

The global market size is expected to reach USD 113.97 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us