Racing Tires Market Size, Share & Industry Analysis, By Tire Type (Slick Tires (Dry Track), Intermediate Tires, Wet/Rain Tires, and Grooved/Semi-Slick Tires), By Vehicle Type (Passenger Car Racing, Two-Wheeler Racing, and Off-Road & Specialty Racing), By Sales Channel (OEM and Aftermarket), By Construction Type (Radial and Bias), and Regional Forecast, 2026-2034

Racing Tires Market Size and Future Outlook

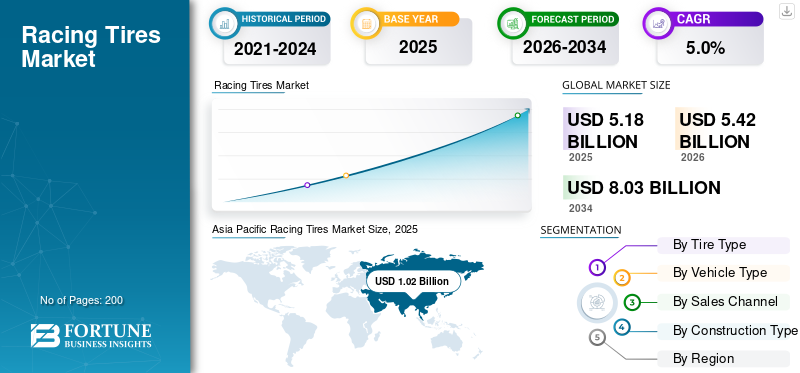

The global racing tires market size was valued at USD 5.18 billion in 2025. The market is projected to grow from USD 5.42 billion in 2026 to USD 8.03 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the racing tires market with a market share of 19.69% in 2025.

Racing tires are high-performance tires engineered for competitive motorsports, designed to deliver superior grip, handling precision, heat resistance, and stability under extreme speeds, cornering forces, and varying track conditions. Market drivers include technological advancements, rising consumer interest, regulatory support, economic expansion, competitive innovation, and increasing investments across the value chain.

Major players in the market include Michelin, Bridgestone, Goodyear, Pirelli, Continental, and Yokohama, competing through advanced rubber compounds, lightweight construction, enhanced grip technologies, motorsport partnerships, and continuous performance-focused innovation.

Download Free sample to learn more about this report.

RACING TIRES MARKET TRENDS

Technological Advancements in Tire Compounds Enhancing Competitive Performance

Continuous innovation in rubber compounds, tread patterns, and lightweight materials is shaping key racing tires market trends. Manufacturers are focusing on improved thermal stability, enhanced cornering grip, and reduced rolling resistance to optimize lap times. Integration of simulation tools and data analytics in tire design is accelerating product development cycles. These advancements strengthen competitive differentiation and influence market share, as teams increasingly prioritize performance consistency and durability across diverse track conditions.

- In January 2026, Nokian Tyres unveiled its Betula concept tire, incorporating a renewable birch bark-derived material, boosting the tread compound's recycled and renewable content to 93%. This innovation aims to enhance performance and advance sustainability goals in tire manufacturing.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Motorsport Participation to Accelerate Market Growth

The increasing popularity of professional and amateur motorsports globally is a major driver for the market. Expanding racing leagues, grassroots track events, and growing fan engagement are stimulating market demand for high performance tire. Automotive manufacturers are also leveraging motorsports for brand positioning and technology testing, further supporting racing tires market growth. Emerging economies are witnessing new racetrack developments and sponsorship investments, contributing to sustained demand across multiple racing categories during the market forecast period.

In November 2025, Ford Racing officially launched its 2026 global motorsports season, marking an ambitious return to Formula 1 competition and expanded racing programs across premier series. The kickoff event highlighted Ford’s commitment to speed, innovation, and a renewed competitive presence on iconic international circuits.

MARKET RESTRAINTS

High Replacement Costs and Limited Road Applicability Restricting Wider Adoption

Racing tires are engineered for specialized track use and have significantly shorter lifespans compared to conventional tires, leading to high recurring replacement costs. Their limited usability outside professional or organized racing environments restricts broader consumer adoption. Additionally, stringent safety standards and homologation requirements can increase production costs. These factors collectively constrain market expansion, particularly in cost-sensitive regions, and may moderate overall market growth despite rising enthusiasm for motorsports activities.

MARKET OPPORTUNITIES

Expansion of Electric and Hybrid Racing Series Creating New Growth Avenues

The rapid development of electric and hybrid racing championships presents a significant opportunity for the market. Electric race cars demand specialized tires capable of handling instant torque delivery and heavier battery loads. This shift is encouraging manufacturers to develop innovative tire solutions tailored for next-generation propulsion technologies. As sustainability becomes central to motorsports strategies, companies invest in research and development, eco-friendly materials and low-emission manufacturing processes can capture emerging market demand and strengthen long-term market positioning.

- In February 2026, the Nissan Formula E Team prepared to battle under the lights at the Jeddah Corniche Circuit as Rounds 4 and 5 of the 2025/26 ABB FIA Formula E World Championship highlighted its efforts to bounce back and score key points on the double-header weekend. The team aims to capitalize on past podiums and improve its qualifying performance to enhance its standing in the global electric vehicles racing series.

MARKET CHALLENGES

Volatility in Raw Material Prices Impacting Production and Profit Margins

Fluctuations in the prices of natural rubber, synthetic rubber, carbon black, and other petrochemical derivatives pose a key challenge for racing tire manufacturers. Geopolitical tensions, trade tariffs, and supply chain disruptions can intensify cost pressures and affect procurement strategies. Since racing tires require high-quality, specialized materials, manufacturers face limited substitution flexibility. Managing pricing strategies while maintaining product performance and protecting racing tires market share remains a critical challenge throughout the market forecast period.

Segmentation Analysis

By Tire Type

Superior Dry-Track Grip and Professional Racing Adoption to Propel Slick Tires Segmental Dominance

Based on tire type, the market is segmented into slick tires (dry track), intermediate tires, wet/rain tires, and grooved/semi-slick tires.

The slick tires (dry track) segment dominates the market due to its extensive use in professional circuit racing and elite motorsport championships. These tires provide maximum surface contact, superior traction, and optimal heat management under controlled dry conditions, making them the preferred choice for competitive racing teams. Strong adoption across Formula racing, touring cars, and track events sustains consistent replacement cycles, reinforcing their leading market share during the forecast period.

- In May 2025, Pirelli launched the P Zero Trofeo Track, a DOT-approved competition tire that combines slick-like high-grip performance with regulatory compliance for club racers, SCCA, NASA events, and serious track-day drivers seeking consistent dry-surface lap times.

The grooved/semi-slick tires segment is projected to expand at a CAGR of 6.1% over the forecast period. Rising participation in amateur racing, track-day events, and performance driving schools is increasing market demand for versatile tires that offer balanced grip in mixed surface conditions.

By Vehicle Type

Strong Global Motorsport Infrastructure and Sponsorship Ecosystem to Strengthen Passenger Car Racing Segment Dominance

Based on vehicle type, the market is segmented into passenger car racing, two-wheeler racing, and off-road & specialty racing.

The passenger car racing segment holds the largest market share, driven by its extensive presence across Formula racing, touring car championships, endurance racing, and regional circuit competitions. Established motorsport infrastructure, strong OEM participation, and significant sponsorship funding sustain consistent replacement tires cycles. Additionally, continuous technological innovation and regulatory frameworks in professional car racing support steady market growth and reinforce long-term demand across major racing hubs globally.

- In February 2026, Hankook’s iON Race tires delivered dependable grip and thermal control during Formula E’s double-header at the Jeddah Corniche Circuit, supporting strategic racing under lights and reinforcing performance credibility in high-intensity electric motorsport competition.

The two-wheeler racing segment is projected to grow at a CAGR of 5.9% during the market forecast period. Expanding motorcycle racing leagues, rising youth participation, and increasing popularity of superbike championships are accelerating market demand for high-performance racing tires globally.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Frequent Tire Replacement Cycles and Team-Level Procurement to Drive Aftermarket Segment Dominance

By sales channel, the market is divided into OEM and aftermarket.

The aftermarket segment dominates the market and is also the fastest growing, supported by frequent tire replacements during racing seasons and performance testing sessions. Professional teams, independent racers, and track-day participants typically procure tires directly from specialized distributors and performance retailers. Short tire lifespans, evolving compound preferences, and event-specific requirements consistently generate repeat purchases. This dynamic ensures sustained market demand and strengthens the aftermarket’s leading market share throughout the forecast period.

The OEM segment is projected to grow at a CAGR of 4.9% o

By Construction Type

ver the forecast period. Growth is supported by supply agreements between tire manufacturers and racing series organizers, along with standardized tire regulations in select championships.

- In December 2024, the Kawasaki Ninja 1100SX was announced to roll on Bridgestone Battlax S23 tires, enhancing sport-touring grip and stability for riders, blending high-performance dynamics with all-weather confidence for street and track use.

Enhanced Stability and High-Speed Performance to Strengthen Radial Segment Leadership

By construction type, the market is categorized into radial and bias.

The radial segment holds the largest market share in the market due to its superior heat dissipation, structural stability, and enhanced cornering precision at high speeds. Radial construction allows better tread contact and consistent performance under extreme racing conditions, making it the preferred choice across professional car and motorcycle racing formats. Continuous technological refinement and broad adoption in premier championships sustain steady market demand and reinforce its dominant position throughout the forecast period.

-

In February 2026, Vee Tire Co. announced the release of three new RAD-Core radial tires for gravity bikes, offering larger contact patches, increased grip, impact absorption, and reduced rolling resistance across Attack FSX, Attack HPL, and WCE MK2 tread patterns.

The bias segment is projected to grow at a CAGR of 5.8% during the forecast period. Rising participation in vintage racing events, entry-level competitions, and select motorcycle racing categories is supporting renewed demand for bias-constructed racing tires globally.

Racing Tires Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Racing Tires Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is projected to grow at a CAGR of 6.2% during the forecast period, making it the fastest-growing regional market. Increasing investments in motorsport infrastructure, rising disposable incomes, and growing interest in professional and amateur racing are boosting market demand. China, Japan, India, South Korea, and Southeast Asian nations are witnessing new circuit developments and regional championships. Expanding automotive performance culture and manufacturer-led promotional racing events are further accelerating market growth across the region.

- In July 2025, Mitsubishi Motors announced its participation in the 2025 All-Japan Rally Championship, reinforcing its commitment to competitive motorsports and product development through performance testing under extreme conditions to enhance vehicle durability and handling.

China Racing Tires Market

The China market is estimated at around USD 0.25 billion in 2026, accounting for roughly 4.6% of global revenues. Strong domestic motorsport expansion, circuit investments, and OEM-backed racing programs support steady market growth and rising regional market demand.

Japan Racing Tires Market

The Japan market is estimated at around USD 0.22 billion in 2026, accounting for roughly 4.0% of global revenues. Established motorsport heritage, advanced tire technology development, and manufacturer-led championships sustain consistent market share and innovation-driven growth.

India Racing Tires Market

The India market is estimated at around USD 0.16 billion in 2026, accounting for roughly 2.9% of global revenues. Rapid expansion of motorcycle racing leagues and rising youth participation accelerate market growth, making it the fastest-growing country in the region.

Europe

Europe holds the largest market share in the market, supported by its deep-rooted motorsport culture and concentration of premier racing championships such as Formula racing, endurance series, and touring car competitions. The presence of leading tire manufacturers, advanced testing facilities, and established racetrack infrastructure sustains consistent market demand. Stringent technical regulations and continuous innovation in performance compounds further strengthen regional competitiveness. Stable sponsorship ecosystems and cross-border racing events contribute significantly to sustained market growth during the forecast period.

-

In October 2025, Pirelli clinched the FIA European Rally Championship for Tyre Suppliers title, finishing the 2025 season ahead of Michelin with strong performances across multiple rounds and demonstrating product reliability and competitive edge on varied rally surfaces.

Germany Racing Tires Market

The Germany market is estimated at around USD 0.65 billion in 2026, accounting for roughly 12.0% of global revenues. Strong automotive engineering capabilities, premium racing events, and leading manufacturer presence reinforce dominant European market share and sustained demand.

U.K. Racing Tires Market

The U.K. market is estimated at around USD 0.56 billion in 2026, accounting for roughly 10.4% of global revenues. Home to major Formula and endurance racing teams, the country benefits from advanced R&D ecosystems and stable championship calendars.

North America

North America represents the third-largest market in the racing tires industry, driven by well-established racing formats such as NASCAR, IndyCar, drag racing, and sports car championships. Strong fan engagement, sponsorship backing, and structured racing calendars ensure consistent tire consumption across professional and semi-professional categories. The region also benefits from advanced R&D capabilities and collaboration between racing teams and tire manufacturers. Stable economic conditions and performance-driven automotive culture sustain steady market growth throughout the forecast period.

- In November 2025, American Racer was confirmed to continue as the official tire of Must See Racing, reinforcing its presence in sprint car competition and supporting performance consistency, durability, and racer confidence across the series’ national events.

U.S. Racing Tires Market

The U.S. market is estimated at around USD 0.73 billion in 2026, accounting for roughly 13.5% of global revenues. Strong NASCAR, IndyCar, and drag racing participation ensures consistent aftermarket demand and technological advancements in high-performance tire solutions.

Rest of the World

The rest of the world region, including South America, the Middle East & Africa, is witnessing gradual growth in the market. Expanding regional championships, improving racetrack infrastructure, and increasing government support for international sporting events are contributing to rising market demand. Although smaller in overall market share, growing youth participation and automotive enthusiast communities are supporting long-term opportunities. Strategic partnerships and event hosting are expected to enhance regional market analysis outcomes over the forecast period.

- In February 2026, Continental introduced the Archetype 30mm road bike racing tire designed to optimize rolling efficiency and grip for competitive road cyclists while balancing low weight and durability for race conditions.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation, Motorsport Partnerships, and Compound Development Define Competitive Intensity

The market is moderately consolidated, with a few global tire manufacturers controlling a significant market share. Leading players such as Michelin, Bridgestone, Goodyear, Pirelli, and Yokohama compete through advanced compound engineering, exclusive championship supply agreements, and continuous track-tested innovation. Companies focus on high-grip formulations, lightweight construction, and rapid customization for different racing formats. Strategic motorsport partnerships, regional distribution channel, and investments in sustainable materials strengthen competitive positioning. Limited supplier approvals in the premier racing series further intensify competitive rivalry.

- In February 2026, Goodyear unveiled a new tire specification for the EchoPark Automotive Race at Atlanta, enhancing grip and wear performance to support high-speed NASCAR Cup competition and improve overall race consistency for teams and drivers.

LIST OF KEY RACING TIRES COMPANIES PROFILED IN REPORT

- Michelin (France)

- Bridgestone Corporation (Japan)

- The Goodyear Tire & Rubber Company (U.S.)

- Pirelli & C. S.p.A. (Italy)

- Continental AG (Germany)

- Yokohama Rubber Co., Ltd. (Japan)

- Sumitomo Rubber Industries Ltd. (Dunlop) (Japan)

- Hankook Tire & Technology Co., Ltd. (South Korea)

- Toyo Tire Corporation (Japan)

- Kumho Tire Co., Inc. (South Korea)

- Maxxis International (Cheng Shin Rubber Industry Co., Ltd.) (Taiwan)

- Hoosier Racing Tire Corp. (U.S.)

- Nexen Tire Corporation (South Korea)

- Apollo Tyres Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Hankook’s iON Race tires demonstrated reliable grip and thermal efficiency during Formula E competition, supporting high-intensity electric racing and strengthening the company’s position in global motorsport supply programs.

- February 2026: Hankook strengthened its global motorsport portfolio by expanding high-performance tire supply programs and reinforcing partnerships across electric and circuit racing championships, highlighting advanced compound durability and thermal management capabilities.

- February 2026: NASCAR introduced competition changes at Atlanta, including tire and race format adjustments aimed at improving on-track action, durability balance, and overall event competitiveness.

- February 2026: Michelin Motorsport showcased ongoing innovations in racing tire compounds, emphasizing enhanced grip consistency, sustainability initiatives, and collaborative development with premier endurance and rally championships globally.

- February 2026: IndyCar announced a mandate requiring teams to complete two stints on alternate tires during street races, increasing strategic variability and intensifying tire performance management throughout race weekends.

- February 2026: Dunlop unveiled its 2026 Team Dunlop Road Race Elite roster, supporting emerging motorcycle racing talent and reinforcing brand visibility across national-level two-wheel racing championships.

- September 2025: Goodyear launched a new Global Racing Organization to streamline its global motorsport strategy, improving coordination across NASCAR, endurance, and international series while accelerating innovation and competitive responsiveness.

- March 2025: IndyCar highlighted ongoing technical developments and competition updates ahead of the racing season, emphasizing tire performance optimization and strategic race regulations.

REPORT COVERAGE

The global racing tires market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Tire Type |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Construction Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.18 billion in 2025 and is projected to reach USD 8.03 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.02 billion.

The market is expected to exhibit a CAGR of 5.0% during the forecast period of 2026-2034.

The passenger car racing segment leads the market in terms of vehicle type.

Technological advancements in tire compounds are enhancing competitive performance.

Major players in the market include Michelin, Bridgestone, Goodyear, Pirelli, and Yokohama, among others.

Europe holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us