Radiation Hardened Electronics Market Size, Share & Industry Analysis, By Component (Integrated Circuits, Memory, Microcontrollers and Microprocessors, Power Management, and Others), By Technique (Rad-Hard by Design (RHBD), Rad-Hard by Process (RHBP), and Others), By Application (Space, Avionics & Defense, Nuclear Power Plants, Medical, and Others), and Regional Forecast, 2026-2034

Radiation Hardened Electronics Market Current & Forecast Market Size

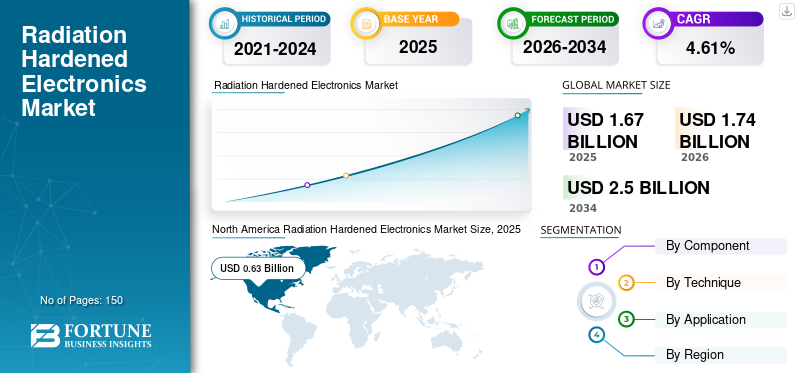

The global radiation hardened electronics market size was valued at USD 1.67 billion in 2025 and is projected to grow from USD 1.74 billion in 2026 to USD 2.50 billion by 2032, exhibiting a CAGR of 4.61% during the forecast period. North America dominated the global market with market share of 37.48% in 2025.

Radiation hardened electronics (Rad-Hard Electronics) are specialized components and systems designed to operate in environments with high levels of ionizing radiation, such as space, nuclear reactors, and military applications. These electronics are engineered to resist radiation-induced malfunctions and degradation, ensuring reliability in critical missions. Applications of such electronics include satellite systems, space exploration, nuclear power plants, and defense systems, where failure due to radiation exposure could lead to catastrophic outcomes.

The global market is poised for steady growth driven by increased space exploration, defense spending, and advancements in nuclear technology. Key players in the market include Honeywell International (U.S.), BAE Systems (U.K.), and Microchip Technology (U.S.), with products such as Honeywell's Radiation Hardened Processors and BAE Systems' RAD750. The market's future will likely see technological innovations focused on enhancing durability and efficiency in extreme conditions. For instance,

- June 2024: BAE Systems and GlobalFoundries collaborated to enhance the supply chain of essential semiconductors crucial for U.S. national security programs. BAE Systems utilized GlobalFoundries' 12LP and 12S0 technology platforms to develop custom-made radiation hardened electronics specifically designed for critical space applications.

Download Free sample to learn more about this report.

RADIATION HARDENED ELECTRONICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.67 Billion

- 2026 Market Size: USD 1.74 Billion

- 2034 Forecast Market Size: USD 2.50 Billion

- CAGR: 4.61% from 2026–2034

- North America dominated the radiation hardened electronics market with a 37.48% share in 2025.

- The integrated circuits (ICs) segment is projected to account for 34.29% of the market in 2026.

- The space segment is expected to hold a 58.35% market share in 2026.

North America

The North America market was valued at USD 0.63 billion in 2025, capturing 37.48% of global revenue, and is estimated to reach USD 0.65 billion in 2026.

Europe

Europe held 15.08% of the global market, reaching a valuation of USD 0.25 billion, and is projected to grow to USD 0.26 billion in 2026.

Asia Pacific

Asia Pacific reached USD 0.53 billion in 2025, representing 31.76% of total market revenue, and is projected to reach USD 0.56 billion in 2026.

U.S.

The U.S. radiation hardened electronics market is estimated to reach USD 0.50 billion in 2026, supported by ongoing defense modernization programs, NASA initiatives, and leadership in nuclear technology.

Japan

Japan’s radiation hardened electronics market is projected to reach USD 0.10 billion in 2026, driven by growing investments in space technologies and advanced aerospace programs.

Read More

MARKET DYNAMICS

Market Drivers

Growing Need for Reliable Components in LEO Space and Other Critical Applications to Increase Demand for Rad Hard Electronics

The growing demand for satellite-based services, including communication, navigation, Earth observation, and other LEO space applications, drives the market growth. As more countries and private companies invest in satellite constellations, the need for reliable rad-hard electronic systems that can withstand space radiation increases is driving the radiation hardened electronics market growth. For instance,

- May 2023: Teledyne e2v HiRel introduced a radiation tolerant integer for LEO space applications. It is a space-grade COTS phase-locked loop (PLL) designed to provide high performance and reliability for space applications. This device meets NASA's EEE-INST-002 specifications to withstand the rigorous demands of radiation-hardened environments in space.

- May 2022: Micross and Apogee Semiconductor partnered to provide radiation-tolerant and radiation-hardened integrated circuits designed for space, defense, and extreme environments. This collaboration enhanced the availability of electronics to withstand harsh radiation conditions, meeting the growing demand for reliable components in critical applications.

Market Restraints/Challenges

High Cost of Production to Limit Rad-Hard Adoption in Cost-Sensitive Projects

The high cost of development and production of rad hard electronics is a significant restraint in the market. The specialized materials, testing, and manufacturing processes required to ensure radiation resistance make these components more expensive than standard electronics, limiting their adoption in cost-sensitive projects or emerging markets.

Market Opportunities

Expansion of Nuclear Power Generation to Boost Demand for Rad Hard Components

One of the opportunities in the global market is the expansion of nuclear power generation, particularly in emerging economies. As these countries build new nuclear power plants, the demand for reliable, radiation-resistant electronics will grow, creating new market opportunities for rad-hard component manufacturers. For instance,

- April 2024: Micross Components introduced a new Nuclear Event Detector (NED) with 4x greater sensitivity, optimized for applications such as missiles and satellites. The NED's enhanced radiation-hardened design offers improved size, weight, and power (SWaP) performance, faster detection, and heightened protection for critical electronics during nuclear events, making it ideal for aerospace and defense systems.

RADIATION HARDENED ELECTRONICS MARKET TRENDS

Increasing Demands for Small Satellites to Set Trend for Miniaturization of Rad-Hard Components

A key trend in the global radiation hardened electronics market is the miniaturization of rad-hard components, driven by the need for lightweight and efficient systems in space and defense applications. The trend toward small satellites, or CubeSats, requires compact and highly reliable rad-hard electronics. The availability of radiation-hardened plastic-packaged devices is designed to support high-reliability spacecraft and satellite missions. This trend reflects the broader shift toward more versatile and adaptable technology that can perform in increasingly challenging environments. For instance,

- July 2021: Renesas Electronics introduced a portfolio of high-reliability radiation-hardened plastic-packaged devices designed for satellite power management in medium and geosynchronous Earth orbits. These ICs provided space-grade solutions with enhanced durability and reduced size, weight, and power (SWaP) costs, meeting the stringent requirements of radiation environments and supporting longer mission lifespans.

SEGMENTATION ANALYSIS

By Component Analysis

Rising Need for Efficient and Continuous Control in Space Applications to Drive Demand for Rad Hard ICs

Based on component, the market is divided into integrated circuits, memory, microcontrollers and microprocessors, power management, and others.

Integrated Circuits (ICs) is expected to hold the global radiation hardened electronics market share by 34.29% in 2026 due to their widespread use in various critical applications, including space and defense. They provide assistance in essential functions in processing, communication, and control. For instance,

- January 2024: Japan’s first Moon lander, SLIM, touched down on January 20, 2024, with Renesas' radiation-hardened (rad-hard) ICs onboard, marking an achievement for Japan's space exploration. These rad-hard ICs are critical for ensuring reliable performance in the harsh space environment, supporting data transmission, telemetry, and power regulation in the spacecraft.

However, memory components are expected to have the highest CAGR, driven by the increasing demand for robust data storage solutions that can withstand high radiation environments, particularly in space missions.

By Technique Analysis

Effective Integration of Radiation Resistance Directly into Component Design to Boast RHBD Adoption

Based on technique, the market is divided into Rad-Hard by Design (RHBD), Rad-Hard by Process (RHBP), and others.

Rad-Hard by Design (RHBD) segment accounted for the largest market globally due to its effectiveness in integrating radiation resistance directly into the design of the components. This approach is preferred over post-manufacturing hardening because it offers better performance, cost-efficiency, and reliability, making it ideal for mission-critical applications. The segment is projected to hold 51.84% of the market share in 2026.

However, Rad-Hard by Process (RHBP) is expected to experience the highest CAGR of 6.76% during the forecast period due to its cost-effectiveness and improved reliability compared to traditional radiation-hardening methods. RHBP involves incorporating radiation-hardened features directly into the semiconductor manufacturing technique, which results in better performance and efficiency for electronics used in high-radiation environments such as space and nuclear applications. As demand for advanced and reliable electronics in these sectors grows, RHBP technology is likely to see accelerated adoption of radiation hardened electronics and market growth.

By Application Analysis

Growing Number of Space Missions and Satellite Launches to Boost Development of Rad Hard Electronics in Space Segment

To know how our report can help streamline your business, Speak to Analyst

By application, the market is categorized into space, avionics & defense, nuclear power plants, medical, and others.

Space segment dominated the global market share and is projected to have the highest CAGR of 5.65% during the forecast period due to the critical need for reliable electronics that can withstand the extreme radiation levels encountered in space. The growing number of space missions, satellite launches, and exploration activities are key drivers of this trend, making the space sector the largest and fastest-growing segment in the market. The segment is expected to hold 58.35% of the market share in 2026. For instance,

- March 2023: Coherent Logix launched the HyperX Midnight, a radiation-hardened System-on-Chip (SoC) designed for space applications, with quadruple computing power at half the energy consumption of leading rad-hard FPGAs. The SoC, designed for the Space 2.0 market, enhances satellite capabilities while reducing costs and launch complexities, supporting both space and terrestrial sectors with advanced, software-defined solutions.

RADIATION HARDENED ELECTRONICS MARKET REGIONAL OUTLOOK

North America

North America Radiation Hardened Electronics Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America leads the global radiation hardened electronics market in terms of size and share, driven by significant investments in defense, space exploration, and advanced nuclear technologies. The North America market was valued at USD 0.63 billion in 2025, capturing 37.48% of global revenue, and is estimated to reach USD 0.65 billion in 2026. The U.S., in particular, with its extensive space programs and military spending, will continue to lead the market, with key companies, such as Honeywell International and BAE Systems, driving innovation.

Download Free sample to learn more about this report.

The U.S. radiation ongoing defense modernization programs support hardened electronics market growth, NASA's ambitious space exploration initiatives and the country's leadership in nuclear technology boosts the regional market growth. The U.S. government's focus on maintaining technological superiority in these areas will ensure sustained demand for advanced rad-hard components. The U.S. market size is estimated to be USD 0.5 billion in 2026.

Asia Pacific

Meanwhile, the Asia Pacific region is experiencing the highest CAGR in the market, driven by the region's increasing focus on space exploration, defense modernization, and nuclear energy development. The market in Asia Pacific reached USD 0.53 billion in 2025, representing 31.76% of total market revenue, and is projected to reach USD 0.56 billion in 2026. Moreover, countries such as China, India, and Japan are key players, investing heavily in rad-hard technologies to support their ambitious space and defense programs. The market size in China is expected to hit USD 0.14 billion in 2026, whereas Indian market is expecting to be USD 0.12 billion and Japan is projected to hit USD 0.1 billion in 2026.

- July 2023: Renesas Electronics introduced a space-grade power management reference design for AMD's Versal XQRVC1902 adaptive SoC, developed in collaboration with AMD. This solution integrates key radiation-hardened components, including four Intersil ICs, which support high-performance power rails for next-gen space avionics, ensuring reliable power delivery in the extreme conditions of space.

Europe

In Europe, the market is set for steady growth, supported by several factors. In 2025, Europe held 15.08% of the global market, reaching a valuation of USD 0.25 billion, and is projected to grow to USD 0.26 billion in 2026. It is driven by strong investments in space exploration, nuclear energy, and defense across the region. The European Space Agency (ESA) and other national space agencies play a vital role in this growth, with a focus on developing advanced rad-hard systems for upcoming space missions. The market size in U.K. is likely to be USD 0.05 billion in 2026. Germany is projecting to be USD 0.05 billion in 2026, and France is anticipating to be USD 35.94 million in 2025.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 0.15 billion in 2025, accounting for 8.75% share, and is expected to reach USD 0.15 billion in 2026.

Middle East & Africa (MEA) and South America

In 2025, the Middle East & Africa market stood at USD 0.12 billion, representing 6.94% of global demand, and is projected to grow to USD 0.12 billion in 2026. The markets in the Middle East & Africa (MEA) and South America are still in the emerging stages but are showing a significant potential. The MEA region is supported by emerging nuclear energy projects and increasing defense expenditures in certain countries. However, political instability and limited technological infrastructure may pose challenges to market expansion in this region. The GCC market size is estimated to be USD 49.10 million in 2025.

Similarly, the market in South America is expected to grow modestly, with key drivers including the development of satellite programs and nuclear energy projects in countries such as Brazil and Argentina. South America is anticipated to be the fourth-largest market with a value of USD 145.95 million in 2025. However, the market's growth may be constrained by economic challenges and limited technological infrastructure in the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Partnerships and Collaborations to Boost Market Presence of Key Players

The key players in the radiation hardened electronics industry are entering into strategic partnerships and collaborating with other significant market leaders to expand their portfolio and provide enhanced products to fulfill their customer's application requirements. Also, through collaboration, the companies are gaining expertise and expanding their business by reaching a mass customer base.

List of Key Radiation Hardened Electronics Companies Profiled

- Honeywell International (U.S.)

- BAE Systems (U.K.)

- Microchip Technology (U.S.)

- Data Device Corporation (U.S.)

- Texas Instruments (U.S.)

- STMicroelectronics (Switzerland)

- Analog Devices (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Cobham Advanced Electronic Solutions (U.S.)

- Teledyne Technologies (U.S.)

- Infineon Technologies (Germany)

- Sandia National Laboratories (New Mexico)

- TTM Technologies Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Renesas Electronics Corporation (Japan)

- VORAGO Technologies (U.S.)

- Mercury Systems (U.S.)

- Alphacore Inc. (U.S.)

- Rakon Limited (New Zealand)

- GSI Technology (U.S.)

- Frontgrade Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- August 2024: Moog introduced a radiation-hardened space computer designed to enhance high-speed computing capabilities for future space missions. This advanced system aims to support the next generation of space technology by ensuring reliable performance in harsh space environments.

- June 2024: Infineon launched the radiation-hardened 1 and 2 Mb parallel interface ferroelectric RAM (F-RAM) devices designed for space applications. These non-volatile memory solutions provide high endurance, fast random access, and exceptional radiation resistance, making them ideal for satellites and space instruments requiring robust data storage and reliability in extreme environments.

- May 2024: Microchip Technology expanded its portfolio of radiation-tolerant microcontrollers, enhancing its offerings for space and harsh-environment applications. These SAMD21RT microcontrollers are designed to provide robust performance and reliability in radiation-intensive environments, including space missions.

- April 2024: EPC Space introduced the EPC7009L16SH, a radiation-hardened Gallium Nitride (GaN) gate driver IC designed for space applications, offering improved power efficiency and size reduction for high-speed circuits. The device is radiation-tolerant to 1000 kRad and is optimized for critical space environments, enabling higher performance in satellite systems, motor drivers, and power conversion compared to traditional silicon-based solutions.

- January 2024: Honeywell and QuickLogic partnered to develop advanced radiation-hardened FPGA solutions aimed at enhancing space and aerospace applications. This collaboration combined QuickLogic's FPGA technology with Honeywell's expertise in radiation-hardened electronics to address the unique challenges of these demanding environments.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The rad hard electronics industry is focused on research & development activities to develop more advanced, efficient, and cost-effective rad-hard solutions. Companies are increasingly collaborating with space agencies and defense organizations to secure long-term contracts, ensuring a steady revenue stream. The sector also attracts venture capital for startups working on innovative rad-hard technologies, reflecting the market's potential for growth amidst rising demand in critical applications such as space and defense.

- June 2023: Zero-Error Systems (ZES), a Singapore-based deep-tech startup, raised USD 7.5 million in an oversubscribed Series A round to expand its global reach and enhance its semiconductor technologies for space and power applications. Their radiation-hardened solutions safeguard commercial semiconductors in extreme environments, ensuring power reliability and data integrity for satellites, rovers, and landers.

REPORT COVERAGE

The report provides a competitive landscape of the market overview and focuses on key aspects such as market players, product/service types, and leading applications of the product. Besides, it offers insights into the market trends and highlights key radiation hardened electronics industry developments. In addition to the factors above, it encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

|

Study Period |

2021-2034 |

|

|

Base Year |

2025 |

|

|

Estimated Year |

2026 |

|

|

Forecast Period |

2026-2034 |

|

|

Historical Period |

2021-2024 |

|

|

Unit |

Value (USD Million) |

|

|

Growth Rate |

CAGR of 4.61% from 2026 to 2034 |

|

|

Segmentation |

By Component, Technique, Application, and Region |

|

|

Segmentation |

By Component

By Technique

By Application

By Region

|

|

|

Companies Profiled in the Report |

BAE Systems, Renesas Electronics Corporation, Infineon Technologies AG, TTM Technologies Inc., Honeywell International Inc., Microchip Technology Inc., STMicroelectronics, Advanced Micro Devices, Inc., Teledyne Technologies Inc., and Texas Instruments Incorporated. |

|

Frequently Asked Questions

The market is projected to record a valuation of USD 2.50 billion by 2034.

In 2025, the market size stood at USD 1.67 billion.

The market is projected to grow at a CAGR of 4.61% during the forecast period.

Integrated Circuits (ICs) are the leading component segment in the market.

The growing need for reliable components in LEO space and other critical applications is expected to increase demand for rad hard electronics.

BAE Systems, Renesas Electronics Corporation, Infineon Technologies AG, TTM Technologies Inc., Honeywell International Inc., Microchip Technology Inc., STMicroelectronics, Advanced Micro Devices, Inc., Teledyne Technologies Inc., and Texas Instruments Incorporated. are the top players in the market.

North America holds the highest market share.

Asia Pacific is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us