Radiology Scheduling Software Market Size, Share & Industry Analysis, By Type (Standalone and Integrated{ RIS-integrated, RIS + PACS integrated, EHR/EMR-integrated, and Others}), By Deployment (On-premise, Cloud-based, and Hybrid), By Workflow (Appointment Booking & Slot Management, Order/Referral Intake, Patient Preparation & Communication, Rescheduling, Cancellation & Waitlist Management, Resource Allocation & Modality Scheduling, and Others), By Application (CT, MRI, Ultrasound, X-ray, Mammography/Breast Imaging, and Others), By End User, and Regional Forecast, 2026-2034

Radiology Scheduling Software Market Size and Future Outlook

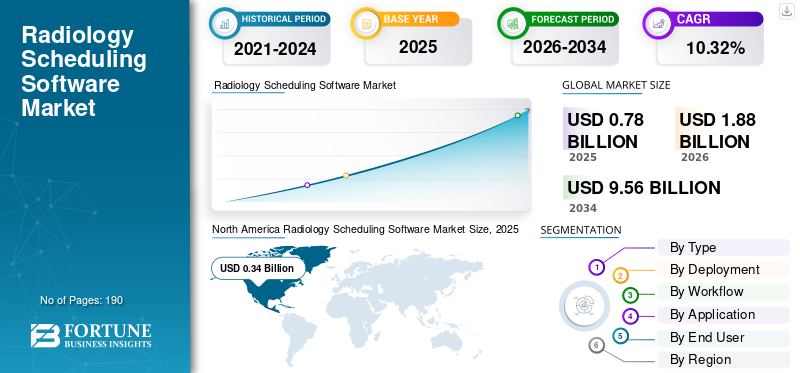

The global radiology scheduling software market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 1.88 billion in 2026 to USD 9.56 billion by 2034, exhibiting a CAGR of 10.32% during the forecast period. North America dominated the radiology scheduling software market with a market share of 43.59% in 2025.

The global market is contemplated to witness a steady growth in the forthcoming years. The growth of the market is driven by the rising volume of diagnostic imaging procedures and the increasing need to manage patient appointments more efficiently across settings. As radiology departments handle higher patient loads, with significant staff shortages, healthcare providers are adopting scheduling software to optimize their workflows and reduce delays. These solutions help to improve scanner utilization and simplify coordination from booking to exam completion. The market is also benefiting from the shift toward integrated radiology information systems, which help providers improve patient outcomes.

Additionally, key companies operating in the market are increasingly focusing on new product launches to capitalize on the market's growth potential and on incorporating AI capabilities into their scheduling solutions.

- In February 2025, Koninklijke Philips N.V. launched a new AI-enabled system, intelligent software, and imaging cloud services designed to streamline radiology workflows and improve operational efficiency. Such developments indicate that vendors are increasingly investing in workflow-focused radiology platforms, which are expected to support broader adoption of advanced scheduling and workflow management solutions in the market.

Furthermore, there are a few players leading in the radiology scheduling software industry, such as eRAD, Ltd, MedInformatix, Inc., Koninklijke Philips N.V., Inc., and FUJIFILM Holdings Corporation. However, these companies are focusing on expanding their offerings and strengthening their positions in the marketspace.

Download Free sample to learn more about this report.

RADIOLOGY SCHEDULING SOFTWARE MARKET TRENDS

Increasing Demand for Real-Time Scheduling Analytics and Capacity Management is Observed as a Market Trend

The global market trend predominantly observed is the increasing demand for real-time scheduling analytics and capacity management. As imaging providers are under pressure to handle rising scan volumes, radiology departments use real-time analytics to monitor appointment utilization, identify underused slots, reduce scheduling bottlenecks, and balance workloads more effectively across modalities. These critical applications improve patient flow, support faster exam turnaround, and help providers make better operational decisions on a routine basis. As a result, healthcare organizations are showing stronger interest in scheduling platforms with innovative product launches and technology advancements.

- For instance, in November 2025, GE HealthCare launched Imaging 360 powered by AI to help improve operational efficiency by providing a unified view to streamline radiology fleet management, optimize staff allocation, and drive productivity. Such developments are expected to strengthen global radiology scheduling software market demand.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Diagnostic Imaging Volumes Driving Need for Efficient Scheduling to Facilitate Market Growth

A key factor driving the global radiology scheduling software market growth is the increasing diagnostic imaging volumes across hospitals, diagnostic centers, and outpatient facilities. As more patients demand for MRI, CT, X-ray, ultrasound, and other imaging exams, radiology departments are under greater pressure to manage more appointments without creating delays, or workflow confusion. This is increasing the need for scheduling software that can organize appointment flow, reduce patient wait times, and support better coordination across staff. As a result, healthcare service providers are adopting more advanced scheduling solutions to handle higher imaging volumes in a more efficient and patient-centric way. This trend is also encouraging vendors to strengthen workflow-focused imaging platforms and focus on innovative product launches that help providers manage growing operational complexity more effectively.

- In November 2025, FUJIFILM Healthcare Americas Corporation announced the launch of Synapse One, a comprehensive enterprise imaging and informatics solution tailored for outpatient imaging centers in North America. The solution is designed to improve operational efficiency by providing a single system for managing information systems and imaging workflows. Such development reflects the importance of streamlined scheduling and workflow management solutions in the market.

MARKET RESTRAINTS

Integration Complexity with RIS, PACS, EHR, and Billing Systems to Limit Market Growth

The global market faces a key restraint in the form of integration complexity with RIS, PACS, EHR, and billing systems. Most radiology scheduling software does not work in isolation and must exchange patient, order, imaging, reporting, and payment data across multiple hospital platforms. When these systems are not well-connected, providers face delays in implementation, workflow disruption, and a higher risk of scheduling errors. This increases deployment time and cost, and slows down adoption by hospitals and imaging centers. Such integration challenges can reduce buyer confidence and further restrain growth in the market.

- In June 2025, the Radiology Society of North America published an article titled 'Integrating Imaging Tools Helps Radiology AI Deliver Real Value' that highlighted interoperability remains a critical but often overlooked requirement for imaging tools to deliver value, showing that poor system connectivity continues to be a practical barrier in radiology workflow software adoption.

MARKET OPPORTUNITIES

Workflow Automation in Radiology Front-End Operations is Supporting Market Expansion

Workflow automation across front-end operations is creating a strong growth opportunity for the market. Varied applications such as patient intake, appointment booking, order management, insurance verification, and pre-exam coordination can be automated, reducing delays, duplicate work, and higher administrative burden. This is creating new growth opportunities for vendors that can connect front-end scheduling with broader radiology workflow systems. As providers increasingly want a smoother process from patient access to exam completion. Underscoring the growth potential, key operating players in the market are focusing on technological advancements and new product launches to capitalize on growth.

- In January 2026, medQ announced AI- and automation-powered enhancements across the radiology patient journey, from patient access and intake to radiologist reporting, follow-up, and analytics. These enhancements were designed to reduce administrative burden, improve turnaround times, and improve patient and provider experiences.

MARKET CHALLENGES

Radiology Workforce Shortages and Burnout Limiting Operational Efficiency Pose a Challenge for Market Growth

The global market faces a notable challenge of workforce shortages and burnout across radiology departments. Many hospitals and diagnostic centers are struggling to manage appointments with a limited number of radiologists, technologists, and support staff. Such a factor creates heavier workloads, longer scheduling backlogs, and increasing pressure on existing teams, leading to rapid burnout. These factors can reduce the ability of providers to adopt and optimize new scheduling systems effectively.

- In October 2024, October 2024 RSNA published an article reporting that the radiologic technologist vacancy rate had risen to 18.1%, up from 6.2% three years earlier, and noted that the shortage was affecting patient wait times for scheduling and imaging. Such factors disrupt radiology operations and act as a challenge for effective use of radiology scheduling software.

Segmentation Analysis

By Type

Increasing Preference for Integrated Solutions to Lead Segmental Growth

Based on the type, the market is categorized into standalone and integrated.

Among these, the integrated segment accounted for the largest radiology scheduling software market share. The integrated segment dominated the market due to increasing preference by radiology providers. This software works as part of a broader RIS, PACS, EHR, and workflow environment. When scheduling is integrated with order intake, reporting, imaging data, and patient communication, providers can reduce duplicate work, improve coordination, and manage patient flow more efficiently across the imaging journey. This makes integrated platforms more valuable for hospitals and imaging networks that want one connected system instead of multiple disconnected applications. Also, they account for revenue share, encouraging key players to invest in developing software solutions and new product launches to monetize their growth.

- For instance, in May 2025, GE HealthCare launched an enterprise imaging solution, including True PACS and Centricity PACS integrated with Pace and Balance, and Datalogue, to help improve workflow and productivity. Such developments support the dominance of the integrated segment in the market. Such developments are expected to drive the segment's growth.

The standalone segment is expected to observe a growth at a CAGR of 7.19% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Reduction of Cost and Workflow Delays by On-premise Deployments to Lead Segmental Growth

Based on deployment, the market is segmented into on-premise, cloud-based, and hybrid.

In 2025, the on-premise segment dominated the market. The dominance of the segment is attributed to its potential to reduce workflow delays and cost reduction. Diagnostic imaging providers still rely on locally deployed radiology IT systems to maintain stronger control over data, security, system customization, and integration with existing RIS, PACS, EHR, and billing infrastructure. So, providers often prefer on-premise deployment for lower dependence on external hosting environments and better alignment with hospital IT architecture.

- For instance, in May 2025, Radiology Business published an article that reported the radiology department explored the use of an on premise artificial intelligence solution with the potential to reduce costs and simplify workflows.

The cloud-based segment is projected to grow at a CAGR of 18.96% during the global market forecast period.

By Workflow

Increasing Adoption for Core Application of Appointment Booking & Slot Management to Lead Growth in Segment

Based on workflow, the market is segmented into appointment booking & slot management, order/referral intake, patient preparation & communication, rescheduling, cancellation & waitlist management, resource allocation & modality scheduling, and others.

In 2025, the appointment booking & slot management segment accounted for the dominant share in the market. The share is attributed to the highest-frequency function of the application in radiology scheduling operations. Every imaging exam begins with appointment creation, time-slot allocation, and matching the patient to the right modality, location, and prep requirements. As imaging providers handle rising patient volumes, these tasks become more critical as poor slot management can lead to idle scanners, overbooking, delays, and patient dissatisfaction. This is increasing demand for software that can automate booking, improve slot visibility, and make scheduling faster and more accurate. As a result, appointment booking and slot management remain the core workflow areas where most providers witness immediate operational value, prompting key players to participate in strategic collaborations and partnerships.

- For instance, in February 2025, Intelerad collaborated with Strategic Radiology to expand the private practices it serves and underscored its impact on the radiology community.

In addition, the order/referral intake segment is projected to grow at a CAGR of 10.59% during the study period.

By Application

Increasing Screening Volumes to Drive Demand for CT Segment

Based on application, the market is segmented into CT, MRI, ultrasound, X-ray, mammography/breast imaging, and others.

Based on the application, CT accounted for the largest share of the global market during the forecast period. The segment dominates as it is most widely used in imaging modalities across emergency, inpatient, and outpatient settings, which creates a high volume of appointments that need to be managed efficiently. This makes scheduling especially important in CT workflows, where faster turnaround and higher throughput directly affect operational efficiency and revenue realization. Due to these factors, providers continue to invest in solutions that help manage heavy scan volumes more smoothly.

- For instance, in November 2025, Koninklijke Philips N.V., launched Verida, a detector-based spectral CT fully powered by AI. The system was built for high-demand environments to streamline workflows, reduce repeat scans, and support operational outcomes. Such developments support the dominance of the CT segment in the market by application.

In addition, the mammography/breast imaging segment is projected to grow at a CAGR of 11.02% during the study period.

By End User

Increasing Demand in Hospitals Due to Large Patient Volumes to Lead Growth in Segment

Based on end user, the market is segmented into hospitals, diagnostic imaging centers, ambulatory imaging centers, and others.

By end user, the hospitals segment is estimated to have dominated the market as hospitals handle high imaging volumes across multiple modalities and departments, making scheduling coordination more complex and more critical. Unlike smaller centers, hospitals must manage inpatient, outpatient, emergency, and referral-based imaging demand within one operational environment. This increases the need for scheduling software that can support high throughput, resource visibility, and coordination across radiology teams and locations. Hospitals also tend to invest more in connected imaging workflow platforms as part of broader digital modernization programs.

- For instance, in December 2025, GE HealthCare announced new AI enhancements to Imaging 360, its cloud-based operational solution for radiology departments, to help improve efficiency by automating analysis and surfacing actionable insights. This reflects the strong demand from hospital radiology departments for tools that can improve operational control and workflow performance, supporting the dominance of hospitals as the leading end-user segment.

The diagnostic imaging centers segment is projected to grow at a CAGR of 11.72% over the study period.

Radiology Scheduling Software Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Radiology Scheduling Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.30 billion and maintained its leading position in 2025 at USD 0.34 billion. The market is growing in North America as the region has high imaging volumes, a large outpatient imaging base. The region also witnesses faster adoption of integrated cloud-based imaging workflow platforms.

U.S. Radiology Scheduling Software Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.35 billion in 2026, accounting for roughly 40.65% of global share.

Europe

Europe is projected to grow at 9.19% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.23 billion by 2026. The region is witnessing growth as healthcare facilities are increasingly adopting cloud-based radiology informatics and AI-enabled workflow tools to improve efficiency and manage workforce pressure. These developments are creating a stronger demand for scheduling software that can support smoother patient flow.

U.K. Radiology Scheduling Software Market

The U.K. market is estimated at around USD 0.05 billion in 2026, representing roughly 5.86% of the global market.

Germany Radiology Scheduling Software Market

Germany's market is projected to reach approximately USD 0.06 billion in 2026, equivalent to around 6.71% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.19 billion in 2026 and secure the position of the third-largest region in the market. The diagnostic infrastructure is expanding, digital healthcare adoption is improving, and providers are investing more in imaging workflow modernization in the region. These factors collectively support growth for radiology scheduling solutions.

Japan Radiology Scheduling Software Market

The Japanese market in 2026 is estimated at around USD 0.04 billion, accounting for approximately 4.78% of the global market.

China Radiology Scheduling Software Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.06 billion, representing approximately 7.26% of global sales.

India Radiology Scheduling Software Market

The Indian market size in 2026 is estimated at around USD 0.02 billion, accounting for roughly 1.81% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.03 billion in 2026. The market is growing in Latin America as private hospitals and imaging providers are upgrading imaging infrastructure and adopting cloud-based enterprise imaging platforms to improve workflow efficiency. In the Middle East & Africa, the GCC is set to reach USD 0.01 billion in 2026.

South Africa Radiology Scheduling Software Market

The South African market is projected to reach approximately USD 0.004 billion by 2026, accounting for roughly 0.42% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global market is dominated by a few key players, including eRAD, MedInformatix, Inc., Koninklijke Philips N.V., FUJIFILM Holdings Corporation, RamSoft Inc., and Magentus, all of which hold considerable market presence. Factors such as strategic partnerships, new product launches, continuous technological progress, and growing financial commitments within the industry are contributing to the expansion of their market share.

- For example, in November 2025, FUJIFILM Healthcare Americas Corporation launched Synapse One, a workflow solution designed for unique outpatient imaging needs, in North America. The imaging solution enabled a patient engagement portal, self-scheduling of exams, RIS (Radiology Information System), advanced scheduling capability, RCM options, PACS (Picture Archiving and Communication System), advanced 3D imaging, a physician portal, and more, all within the Synapse platform in the secure Amazon Web Services (AWS) cloud. Such developments are supporting the expansion of the global market.

Additional global participants in the market include AbbaDox, Swearingen Software, and SolumedRis. Such organizations are anticipated to focus on enhancing their technological capabilities, forming strategic alliances, and launching new offerings to reinforce their competitive standing over the forecast period.

LIST OF KEY RADIOLOGY SCHEDULING SOFTWARE COMPANIES PROFILED

- eRAD (U.S.)

- MedInformatix, Inc. (U.S.)

- Koninklijke Philips N.V.,(Netherlands)

- FUJIFILM Holdings Corporation (Japan)

- RamSoft Inc.(Canada)

- Magentus (Australia)

- AbbaDox (U.S.)

- Swearingen Software (U.S.)

- SolumedRis (South Africa)

- Soliton IT Ltd (U.K.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: GE HealthCare announced the latest advancements of Imaging 360 with artificial intelligence (AI) integration designed to help improve efficiency in the radiology department. AI-driven Discoveries help to balance device utilization, optimize slot times, and identify opportunities to standardize protocols, all with the intent of giving back time and energy to healthcare providers so they can deliver optimal care to more patients with existing resources.

- May 2025: Intelerad, a leader in medical imaging software solutions, partnered with RADPAIR, a leader in generative AI-driven radiology solutions, to deliver an enhanced radiology reporting experience. This partnership combined Intelerad's workflow orchestration capabilities with RADPAIR's agentic AI technology, allowing radiologists to work more efficiently by automating entire portions of reporting workflows.

- March 2025: ai partnered with RamSoft, a global provider of cloud-based imaging and RIS/PACS solutions. The partnership integrates and offers NewVue.ai's EmpowerSuite, including the Intelligent Worklist and Radiologist Cockpit, to its PowerServer and OmegaAI RIS/PACS customers, helping them to streamline workflows further, improve efficiencies, and modernize their radiology operations.

- July 2024: AbbaDox partnered with Merge Healthcare Solutions to deliver an enhanced suite of radiology workflow solutions, including Merge RIS and Merge Document Management.

- April 2024: AbbaDox collaborated with Radiology Imaging Associates to transform the operational and patient care landscape across Florida and the US Virgin Islands. The collaboration elevated the standard of care and operational efficiency across 17 locations, processing over 600,000 annual studies.

REPORT COVERAGE

The global radiology scheduling software market report provides a comprehensive analysis of market size and forecast across all the major segments covered in the study. It includes detailed insights into key market dynamics, growth drivers, restraints, challenges, and emerging opportunities expected to influence market expansion over the forecast period. The report also presents information on important industry trends such as cloud-based deployment, workflow automation, integration with RIS, PACS, and EHR systems, and the growing use of digital patient communication tools. In addition, it covers major developments including product launches, partnerships, mergers and acquisitions, and other strategic activities shaping the competitive environment. Further, the report offers a detailed competitive landscape with market share analysis and profiles of major companies operating in the global market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.32% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Deployment, Workflow, Application, End User, and Region |

| By Type |

|

| By Deployment |

|

| By Workflow |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 0.78 billion in 2025 and is projected to reach USD 9.56 billion by 2034.

In 2025, the market value stood at USD 0.34 billion.

The market is expected to grow at a CAGR of 10.32% over the forecast period.

The integrated segment is expected to lead the market by type.

The rising diagnostic imaging volumes are driving the need for efficient scheduling and market growth.

eRAD, Ltd, MedInformatix, Inc., Koninklijke Philips N.V., FUJIFILM Holdings Corporation, and iCAD, Inc are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us