Operating Room Scheduling Software Market Size, Share & Industry Analysis, By Type (Standalone and Integrated), By Deployment (Cloud-Based, On Premise and Hybrid), By Workflow (Preoperative, Intraoperative and Post-Operative), By End User (Hospitals & ASCs, Specialty Clinics and Others) and Regional Forecast, 2026-2034

Operating Room Scheduling Software Market Size and Future Outlook

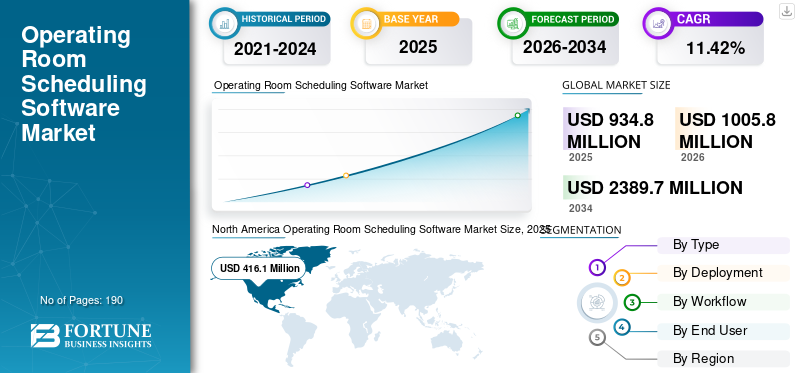

The operating room scheduling software market size was valued at USD 934.8 million in 2025. The market is projected to grow from USD 1,005.8 million in 2026 to USD 2,389.7 million by 2034, exhibiting a CAGR of 11.42% during the forecast period. North America dominated the operating room scheduling software market with a market share of 44.51% in 2025.

The market is anticipated to grow in the upcoming years. Operating room scheduling software is extensively used to plan, allocate, and optimize surgical time, rooms, staff, and equipment across urgent cases. These software solutions ensure higher utilization, providing higher surgical throughput. The increasing adoption of digitalization in healthcare systems is expected to drive growth in the global operating room scheduling software market. Furthermore, innovative product launches in operating room scheduling software that optimize workflows drive market growth.

- For instance, in August 2025, Apella launched Apella Horizon, which included proactive scheduling and capacity optimization for surgical teams. The solution brought together real-time OR management, scheduling optimization and workflow efficiency insights within a single platform powered by computer vision and predictive AI. Such developments are anticipated to boost the overall market growth.

Furthermore, leading players in the operating room scheduling software industry, such as Surgical Information Systems, Picis Clinical Solutions, Inc., Max Systems and TAGNOS, are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

Operating Room Scheduling Software Market Key Takeaways

- 2025 Market Size: USD 934.8 million

- 2026 Market Size: USD 1,005.8 million

- 2034 Forecast Market Size: USD 2,389.7 million

- CAGR: 11.42% from 2026–2034

- North America dominated the market with a 44.51% share in 2025.

- Integrated software segment accounted for the largest market share in 2025.

- Cloud-based deployment segment held the largest revenue share in 2025.

North America

The market reached USD 416.1 million in 2025 and is projected to grow significantly with rising surgical procedures.

Asia Pacific

The market is projected to reach USD 224.7 million by 2026, driven by healthcare digitization and technology adoption.

Europe

The market is projected to reach USD 266.3 million by 2026, supported by digital healthcare initiatives.

U.S.

The market is projected to reach USD 410.6 million by 2026, driven by increasing adoption of digital OR management.

Japan

The market is projected to reach USD 54.5 million by 2026, supported by rising healthcare digitalization.

Read More

OPERATING ROOM SCHEDULING SOFTWARE MARKET TRENDS

Shift Towards Real-Time Operating Room Orchestration is a Prominent Market Trend

The most prominent trend in the market is shift from static scheduling to real-time, data-driven OR adaptation. This shift enables hospitals to use live operational data and continuously balance block time, add-on cases, staffing constraints and room availability. Surgical backlogs and staffing shortages are major hindrances to workflow optimization, and these solutions offer ways to overcome them by prioritizing tools that predict delays, prevent day-of disruptions and improve utilization. As cloud connectivity and analytics develop, vendors are increasingly focusing on optimizing throughput and financial performance, not just on administrative coordination. Emphasizing the growing demand for safety analytics, numerous solution providers are launching updates to these applications to strengthen their market position.

- For instance, in January 2025, LiveData, Inc., launched LiveData PeriOp Manager in 88 VA hospitals. This widespread implementation marked a significant step forward in optimizing OR utilization across the VA health care system. Such developments are expected to boost market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Surgical Case Load Is Pushing Hospitals to Digitize OR Scheduling to Drive Market Growth

As surgical demand increases, hospitals and ASCs face tighter capacity constraints because operating room time is a critical bottleneck in perioperative care. Higher case volumes typically amplify challenges such as block underutilization, day-of delays and cancellations, which directly reduce throughput and revenue. This creates a strong need for efficient operating room scheduling software to standardize booking, improve visibility and reduce avoidable idle time. As a result, rising procedural load and recovery programs push providers to invest in scheduling and OR management tools to protect margins and reduce waiting lists.

- For instance, in 2024, the VHA annual report, the U.S. Department of Veterans Affairs reported that VA delivered more than 130 million health care appointments, representing more than a 7% increase over last year. Such an increase in surgical volumes is expected to drive market growth.

MARKET RESTRAINTS

Integration of OR Scheduling Software Challenges to Hamper Market Growth

Operating room scheduling software faces adoption challenges as hospitals typically operate in complex, multi-vendor perioperative environments, which can extend integration timelines and inflate implementation costs. Buyers are increasingly risk-averse as downtime or workflow errors can disrupt theatre operations, so cybersecurity, resilience and auditability requirements lengthen procurement cycles. As a result, vendors often face longer sales cycles and higher delivery complexity, which can slow market expansion even when demand is strong.

MARKET OPPORTUNITIES

AI-driven capacity optimization and instrumentation to Unlock New Growth Opportunities

Hospitals are under sustained pressure to increase surgical throughput without adding new theatres, so they are prioritizing solutions that convert operational data into actionable scheduling decisions. As staffing constraints and case complexity rise, static block schedules lead to underutilization and cancellations, directly hurting revenue and patient access. This drives demand for AI-enabled OR management tools that continuously rebalance block time, predict overruns and release unused capacity faster. The stronger the backlog and competitive pressure for high-margin surgical cases, the more attractive “optimization overlays” become, especially when they integrate with existing HIS/EHR environments. As a result, vendors that package end-to-end surgical coordination with OR scheduling are well-positioned to expand wallet share.

- For instance, in June 2025, LeanTaaS, Inc., launched iQueue for Surgical Clinics, a surgical coordination platform from the clinics to the hospital's operating rooms (ORs). Such developments are transforming operational efficiency in the hospitals.

MARKET CHALLENGES

High Cost Associated with OR Scheduling Software to Slow Adoption and Pose a Challenge to Market Growth

One of the critical challenges faced by the market is the high implementation cost, as these solutions typically require interfaces with the EHR/HIS, anesthesia, billing, inventory, and other critical systems. Configuration of block rules, data clean-up, and staff training add to the total project cost. Additionally, the cost to develop these solutions is also high, resulting in slower adoption by mid-size hospitals and specialty providers. These factors result in longer procurement cycles and operational change management plans before approving spend. As a result, high upfront and implementation-related costs slow adoption and pose a challenge to market growth.

- For instance, in August 2025, Appinventiv estimated that the cost to build medical scheduling software ranges from USD 30,000 to 300,000, depending on complexity and required features.

Segmentation Analysis

By Type

New Product Launches in Integrated Software Type Leads to Segmental Growth

Based on type, the market is categorized into standalone and integrated.

Among these, the integrated segment accounted for the largest share of the global operating room scheduling software market in 2025. Integrated operating room scheduling software dominated due to increasing preference by hospitals and ASCs. These solutions connect with the EHR and perioperative workflows, reducing duplicate data entry and improving coordination. Additionally, they account for revenue share, encouraging key players to invest in the development of integrated solutions and their subsequent product launches.

- For instance, in January 2026, Haro Gharbigi launched AxiaASC, an AI-powered operating room scheduling platform for ambulatory surgery centers to maximize OR utilization, reduce cancellations, and recover lost revenue. Such developments are expected to drive the segment's growth.

The standalone segment is expected to grow at a CAGR of 9.46% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Real-Time Operations and Scheduling Features of Cloud-Based Deployment to Lead Segmental Growth

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

In 2025, Cloud-based deployment accounted for the largest revenue share. It offers various advantages over other alternatives, such as lower infrastructure burden, rapid multi-site rollouts, and easier upgrades and analytics. Cloud-based deployments also support real-time access for distributed surgical teams, centralized scheduling offices, and multi-site standardization. Overall, these operational benefits translate into higher renewal rates and broader module adoption, which concentrates revenue in cloud deployments. The various advantages of cloud-based deployment encourage key players to participate in strategic partnerships and accelerate adoption.

- For instance, in July 2021, Picis Clinical Solutions, Inc. (Picis) collaborated with North Mississippi Health Services (NMHS) to implement and integrate Picis' cloud-based Picis Total Perioperative Automation (TPA) Solution with the Electronic Medical Records (EMR) system across 5 locations and all 44 operating rooms in two states.

The hybrid segment is projected to grow at a CAGR of 7.98% during the forecast period.

By Workflow

Critical Role of Scheduling in the Preoperative Segment to Drive the Segmental Growth

Based on workflow, the market is segmented into preoperative, intraoperative, and postoperative.

Among these, preoperative workflow dominated the market in 2025. Scheduling is a critical aspect of the preoperative workflow and thus accounts for a significant share of the revenue stream. Minor upstream improvements, such as better-predicted case times, fewer last-minute changes and fewer idle gaps, have a compounding effect on utilization and staffing. This makes pre-operative scheduling intelligence the most heavily used layer of OR scheduling software. Key players operating in the market recognize its critical applications and benefits and are bringing innovative solutions to maximize output.

- For instance, in July 2021, Picis Clinical Solutions, Inc. launched the first Minor Release of Picis 10 (MR1). The release focused on enhancements to the scheduling area of Picis 10, including the display of utilization metrics for a selected OR and surgeon block time. These metrics help improve Operating Room utilization efficiency by minimizing idle time and identifying overtime scenarios.

In addition, the intraoperative segment is projected to grow at a CAGR of 14.83% during the study period.

By End User

Increasing Demand in Hospitals & ASCs Due to Large Surgical Volumes to Lead Growth in the Segment

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics and others.

Hospitals & ASCs held the dominant share of the market by end user in 2025. They account for the bulk of scheduled surgical capacity and are highly affected by the underutilization of existing infrastructure. They also operate complex resource constraints, multiple rooms, surgeon blocks, equipment, pre-op bays, and PACU, which increases the ROI of dedicated scheduling and perioperative operating room management software. They impact a large share of revenue, underscoring their importance, and key players are investing in research and development and expanding their solutions offerings for hospitals and ASCs. Such developments are expected to drive the growth in the segment.

- For instance, in July 2025, LiveData, Inc., a leader in surgical workflow solutions, expanded its flagship PeriOp Manager platform to include full support for hospital procedure suites.

The specialty clinics segment is projected to grow at a CAGR of 15.24% over the study period.

Operating Room Scheduling Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Operating Room Scheduling Software Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 388.8 million, and maintained its leading position in 2025, at USD 416.1 million. The market in North America is expected to grow significantly over the forecast period, driven by increasing surgical procedures and driving demand in the region. Also, the well-established healthcare infrastructure is driving market demand.

U.S. Operating Room Scheduling Software Market

Given North America’s substantial contribution the U.S. market can be estimated at around USD 410.6 million in 2026, accounting for roughly 40.82% of the global operating room scheduling software market.

Europe

Europe is projected to grow at 10.90% over the coming years, the second-highest among all regions, and reach a valuation of USD 266.3 million by 2026. The area is expected to experience robust growth driven by strict government regulations mandating transparency, along with rising national/regional digitization programs that will further accelerate the replacement of manual scheduling processes.

U.K Operating Room Scheduling Software Market

The U.K. market in 2026 is estimated at around USD 41.3 million, representing roughly 4.11% of the global market.

Germany Operating Room Scheduling Software Market

Germany’s market is projected to reach approximately USD 69.0 million in 2026, equivalent to around 6.86% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 224.7 million in 2026 and secure the position of the third-largest region in the market. The region's growth is driven by rising healthcare expenditure and rapid technology adoption.

Japan Operating Room Scheduling Software Market

The Japanese market in 2026 is estimated to be around USD 54.5 million, accounting for approximately 5.42% of the global market.

China Operating Room Scheduling Software Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 75.5 million, representing approximately 7.51% of global sales.

India Operating Room Scheduling Software Market

The Indian market in 2026 is estimated at around USD 18.4 million, accounting for roughly 1.83% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 45.1 million in 2026. The region is experiencing market growth driven by cost-effective cloud deployments and phased implementations. In the Middle East & Africa, the GCC is set to reach USD 10.7 million in 2026.

South Africa Operating Room Scheduling Software Market

The South African market is projected to reach approximately USD 3.3 million by 2026, accounting for roughly 0.33% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Mergers and Acquisitions by Key Players to Propel Market Progress

The global operating room scheduling software market is highly consolidated, with companies such as Surgical Information Systems, Picis Clinical Solutions, Inc., Max Systems, and TAGNOS, Banyan Software holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in December 2025, Banyan Software acquired OR Trax, a provider of surgical scheduling solutions. Such developments are aimed at driving market growth.

Other notable players in the global market include Epic Systems Corporation, Oracle, and LeanTaaS. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their position during the forecast period for the global operating room scheduling software market.

LIST OF KEY OPERATING ROOM SCHEDULING SOFTWARE COMPANIES PROFILED

- Surgical Information Systems (U.S.)

- Picis Clinical Solutions, Inc. (U.S.)

- Max Systems (India)

- TAGNOS (U.S.)

- LeanTaaS (U.S.)

- Epic Systems Corporation. (U.S.)

- Oracle (U.S.)

- LiveData, Inc. (U.S.)

- HST, Healthcare Systems & Technologies, LLC (U.S.)

- SurgiCalendar, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Moon Surgical, the leader in Physical AI for the operating room, launched its Maestro Platform in the U.S.

- January 2025: Qventus launches its Perioperative Care Coordination (PCC) solution that alleviates the administrative burden and enhances productivity for pre-admission testing staff, reduces surgery cancellations, and optimizes more patients pre- and post-surgery.

- November 2024: North American Partners in Anesthesia (NAPA) launched NAPA Managed Services. This comprehensive client solution addressed critical operating room (OR) operational needs for health systems and Academic Medical Centers (AMCs).

- September 2023: Fujitsu and Baptist Health South Florida collaborated to transform operating room scheduling with the launch of a new solution, Fujitsu’s Surgical Capacity Optimization, to boost utilization rates and the financial health of the surgical discipline

- June 2023: Caresyntax collaborated with ProAssurance Corporation to provide innovative Caresyntax surgical intelligence tools to ProAssurance’s insured surgeons.

REPORT COVERAGE

The global operating room scheduling software market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global operating room scheduling software market over the forecast period. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.42% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Type, Deployment, Workflow, End User, and Region |

| By Type |

|

| By Deployment |

|

| By Workflow |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 934.8 million in 2025 and is projected to reach USD 2,389.7 million by 2034.

In 2025, the North America market value stood at USD 416.1 million.

The market is expected to grow at a CAGR of 11.42% over the forecast period of 2026-2034.

The integrated type is expected to lead the market.

Increasing surgical volumes to boost demand for global operating room scheduling software and drive market growth.

Surgical Information Systems, Picis Clinical Solutions, Inc., Max Systems, TAGNOS, and LeanTaaS are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us