Railcar Leasing Market Size, Share & Industry Analysis, By Railcar Type (Tank Cars, Hopper Cars, Boxcars, and Flatcars & Well Cars), By Lease Type (Full-Service Leases, Net (Operating) Leases, and Finance / Long-Term Capital Leases), By Lease Duration (Short-Term Leases (≤3 years), Medium-Term Leases (3–7 years), and Long-Term Leases (>7 years)), By End-Use Industry (Chemicals & Petrochemicals, Energy, Petroleum & Bulk Minerals, Agriculture & Food Commodities, Construction & Industrial Materials, and Automotive, Intermodal & Logistics), and Regional Forecast, 2026-2034

Railcar Leasing Market Size and Future Outlook

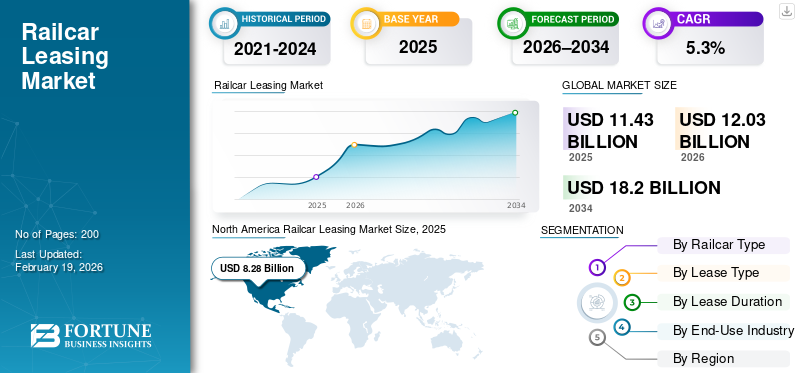

The global railcar leasing market size was valued at USD 11.43 billion in 2025. The market is projected to grow from USD 12.03 billion in 2026 to USD 18.20 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. North America dominated the railcar leasing market with a market share of 72.44% in 2025.

Railcar leasing is a transportation asset model in which specialized freight railcars are owned by leasing companies and rented to shippers, rail operators, or logistics firms, enabling flexible fleet access without a large upfront capital investment. The global market growth is driven by rising freight volumes, increasing preference for asset-light logistics models, high railcar acquisition costs, and stricter safety regulations. The expansion of intermodal transport, long asset life cycles, and the need for fleet flexibility during commodity and trade cycles further support leasing demand.

Players such as GATX, TrinityRail, Wells Fargo Rail, SMBC Rail Services, VTG, and Ermewa dominate the market. Key trends include fleet modernization, growth in full-service leasing, digital fleet monitoring, and long-term contracts for specialized railcars.

Download Free sample to learn more about this report.

Railcar Leasing Market Key Takeways

- 2025 Market Size: USD 11.43 billion

- 2026 Market Size: USD 12.03 billion

- 2034 Forecast Market Size: USD 18.20 billion

- CAGR: 5.3% from 2026–2034

- North America dominated the railcar leasing market with a 72.44% share in 2025.

- The hopper cars segment held the largest market share due to strong demand for bulk commodity transportation.

- The net (operating) leases segment dominated the market owing to its cost efficiency and operational flexibility.

North America

North America led the market, supported by its extensive freight rail network and mature leasing ecosystem.

Europe

Europe maintained steady growth through cross-border freight operations, fleet modernization, and strong leasing adoption.

Asia Pacific

Asia Pacific emerged as the fastest-growing region, driven by industrialization, freight corridor expansion, and rising intermodal logistics.

U.S.

U.S. The market reached USD 7.29 billion in 2025, driven by strong demand from chemicals, agriculture, energy, and intermodal freight.

Japan

Japan The market was valued at USD 0.06 billion in 2025, supported by stable demand from manufactured goods, automotive logistics, and domestic containerized freight.

Read More

RAILCAR LEASING MARKET TRENDS

Fleet Modernization and Intermodal Shift to Reshape Leasing Demand

The global market is increasingly shaped by fleet modernization and the structural shift toward intermodal and specialized freight transportation. Aging railcar fleets in North America and Europe are being replaced with newer, regulation-compliant assets, while the growth of intermodal trade is increasing the demand for flatcars and well cars. Leasing enables faster fleet renewal without long capital cycles, allowing operators to align with evolving cargo patterns, such as containerized cargo, automotive logistics, and temperature-controlled goods. This trend favors professional lessors with diversified fleets, long asset lives, and the ability to redeploy railcars across commodities and corridors as freight demand shifts.

MARKET DYNAMICS

MARKET DRIVERS

Asset-Light Logistics Strategies to Accelerate Leasing Adoption

Shippers and rail operators increasingly prefer asset-light logistics models to preserve capital, improve return on assets, and reduce balance-sheet risk. Railcars are high-value, long-life assets with significant maintenance and compliance obligations, making ownership capital-intensive. Leasing transfers these risks to specialized lessors while providing flexible fleet access. This driver is especially strong among chemical producers, energy companies, and intermodal logistics providers that require reliable capacity but want to avoid cyclical ownership exposure. As supply chains prioritize financial flexibility and scalability, leasing becomes a strategic tool rather than a short-term substitute for ownership.

MARKET RESTRAINTS

High Capital Intensity and Long Payback Cycles May Limit Market Expansion

The railcar leasing market growth is constrained by the high capital intensity of railcar manufacturing and long payback periods for lessors. New railcars require substantial upfront investment, while returns are realized gradually over extended lease terms. This limits rapid fleet expansion, particularly during periods of rising interest rates or economic uncertainty. In emerging regions, limited access to long-term financing further restricts leasing penetration. Additionally, specialized railcars often have narrow secondary markets, increasing residual value risk and discouraging aggressive capacity additions despite rising freight demand.

MARKET OPPORTUNITIES

Emerging Markets and Specialized Cars to Create Long-Term Growth Potential

Opportunities in the market are expanding in emerging economies and in specialized railcar segments. Growing industrialization, mining activity, agricultural exports, and port-linked logistics in Asia Pacific, Latin America, and parts of Africa are creating the demand for modern freight rail solutions. Leasing lowers entry barriers for rail operators and private logistics firms in these regions. At the same time, specialized railcars such as high-specification tank cars and intermodal equipment offer higher yields and longer contract durations, allowing lessors to improve profitability while supporting evolving freight requirements.

MARKET CHALLENGES

Regulatory Complexity and Commodity Cyclicality to Increase Operational Risk

Railcar leasing faces challenges from regulatory complexity and commodity-driven demand volatility. Safety standards, environmental rules, and cross-border compliance requirements differ widely across regions, increasing operational and certification costs for lessors managing global fleets. At the same time, leasing demand is closely tied to commodity cycles in energy, mining, and agriculture, leading to utilization swings. During downturns, excess railcar supply can pressure lease rates and asset values. Managing regulatory compliance while balancing fleet utilization across cycles remains a core challenge for global lessors.

Download Free sample to learn more about this report.

Segmentation Analysis

By Railcar Type

Extensive Use in Bulk Commodity Transportation Efficiency to Propel Hopper Cars Segment Leadership

Based on railcar type, the market is segmented into tank cars, hopper cars, boxcars, and flatcars & well cars.

Among these, the hopper cars segment dominates the market due to their extensive use in transporting bulk commodities such as coal, iron ore, grains, fertilizers, and cement. These commodities form the backbone of rail freight volumes globally and require high-capacity, cost effective transportation over long distances. Leasing hopper cars enables mining companies, agricultural traders, and construction material producers to scale capacity without the risks of asset ownership. Stable bulk demand, long-haul corridors, and predictable utilization patterns continue to reinforce the dominance of hopper cars segment in leasing fleets.

The flatcars & well cars segment is projected to grow at a CAGR of 6.7% over the forecast period.

- In June 2024, China’s National Railway Group reported double-digit growth of the railcar in containerized and automotive rail freight volumes. This highlights the accelerating intermodal logistics demand and supports the faster growth of flatcars and well cars in global leasing fleets.

By Lease Type

Operational Control and Cost Flexibility to Drive Net Lease Segment’s Dominance

Based on lease type, the market is segmented into full-service leases, net (operating) leases, and finance/long-term capital leases.

The net (operating) leases segment dominates the global railcar leasing market share as large rail operators and experienced shippers prefer retaining control over maintenance, routing, and operational scheduling. This structure offers lower lease rentals compared to full-service contracts and suits customers with in-house technical capabilities. Net leases are widely used for standardized railcars such as hoppers and boxcars, particularly in North America and bulk-heavy regions. The model supports cost optimization and fleet customization while keeping assets off balance sheets.

The finance / long-term capital leases segment is projected to grow at a CAGR of 6.1% over the forecast period.

By Lease Duration

Medium-Term Leases Segment Leads Owing to Balance between Cost Efficiency and Flexibility

Based on lease duration, the market is segmented into short-term leases (≤3 years), medium-term leases (3–7 years), and long-term leases (>7 years).

The medium-term leases (3–7 years) segment dominates the market as they strike a balance between flexibility and cost efficiency. These contracts align well with commodity cycles, industrial supply agreements, and infrastructure project timelines, making them suitable across chemicals, construction materials, and agriculture. Medium-term leases allow lessees to adjust fleet size without long-term ownership exposure while providing lessors with reasonable visibility on utilization and returns. This equilibrium makes medium-term contracts the preferred choice across most railcar categories and regions.

The long-term leases segment is projected to grow at a CAGR of 6.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-use Industry

Bulk Energy and Mineral Flows to Push Energy, Petroleum & Bulk Minerals Segment’s Dominance

Based on end-use industry, the market is segmented into chemicals & petrochemicals, energy, petroleum & bulk minerals, agriculture & food commodities, construction & industrial materials, and automotive, intermodal & logistics.

The energy, petroleum & bulk minerals segment dominates the market due to the sheer volume and consistency of bulk freight movements, including coal, ores, oil gas, refined fuels, and industrial minerals. These commodities rely heavily on rail for long-distance inland transportation, creating sustained demand for leased hopper and tank cars. Leasing supports large-scale, repetitive flows without locking capital into owned fleets, particularly in mining and energy-intensive economies.

The automotive, intermodal & logistics segment is projected to grow at a CAGR of 7.5% over the forecast period.

RAILCAR LEASING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Railcar Leasing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America continues to dominate the global market, supported by the world’s largest revenue-earning freight railcar fleet and a highly mature private leasing ecosystem. The region benefits from extensive bulk commodity flows, strong intermodal networks, and widespread adoption of asset-light logistics strategies. The U.S. drives product demand through chemicals, agriculture, and intermodal logistics, while Canada contributes steady bulk and agricultural rail movements. Mexico shows faster relative growth due to cross-border manufacturing and the integration of automotive logistics with the U.S. supply chain.

U.S. Railcar Leasing Market

The U.S. led the global railcar leasing with a value of USD 7.29 billion in 2025 due to its vast intermodal rail network, high leasing penetration, and strong demand from the chemicals, energy, agriculture, and intermodal freight sectors. Long-term and net leases dominate, supported by large private lessors and stable utilization across multiple commodity corridors.

Europe

Europe represents a structurally strong railcar leasing market driven by professional wagon lessors, cross-border freight corridors, and strict regulatory standards that favor leasing over ownership. The region shows the high penetration of full-service leases, particularly for tank and bulk railcars. Germany anchors regional demand through industrial and export-led freight, while the U.K. emphasizes intermodal and construction materials. Ongoing modal-shift policies and fleet modernization support stable, long-term growth across Europe.

U.K. Railcar Leasing Market

Construction materials, intermodal containers, and infrastructure-linked freight drive the U.K. market. Leasing supports flexible capacity for aggregates and consumer goods, with growing emphasis on intermodal logistics and full-service leasing to meet reliability and compliance requirements. The U.K. market was valued at USD 0.25 billion in 2025.

Germany Railcar Leasing Market

Germany dominated the Europe market with a share of 33.2% in 2025 due to its position as the EU's largest rail freight operator. Strong industrial output, cross-border logistics, and bulk commodity movements sustain demand for hopper and tank cars, while intermodal growth supports rising flatcar and well car leasing.

Asia Pacific

Asia Pacific is the fastest-growing railcar leasing market, driven by expanding freight capacity, industrialization, and rising intermodal logistics. China leads through scale and rapid growth in containerized and automotive rail freight. India contributes strong momentum from freight corridor development and wagon capacity expansion, while Japan supports stable leasing demand focused on manufactured goods and intermodal transport. Leasing penetration remains lower in this region than in Western markets but is rising steadily.

China Railcar Leasing Market

China dominated the Asia Pacific market with a share of 62.4% in 2025 due to massive freight volumes across bulk, chemicals, and intermodal logistics. Rapid growth in containerized, automotive, and cold-chain rail transport is accelerating the demand for railcar leasing, flatcars, and specialized equipment to support flexible, large-scale logistics networks.

Japan Railcar Leasing Market

The Japan market is smaller but stable, driven by manufactured goods, automotive logistics, and containerized domestic freight. It was valued at USD 0.06 billion in 2025. Leasing supports efficient asset utilization in a high-cost operating environment, with emphasis on reliability, safety, and long-term fleet planning rather than rapid capacity expansion.

India Railcar Leasing Market

The India market is the fastest-growing market in the Asia Pacific and is poised to expand at a CAGR of 11.5% over the forecast period. The growth is supported by rising freight demand, infrastructure investment, and expanding wagon production. Bulk commodities dominate but intermodal and industrial logistics are gradually increasing, creating long-term opportunities for leased railcar fleets.

Rest of the World

The market in the rest of the world includes Latin America and the Middle East and Africa, where mining, agriculture, and export-oriented bulk logistics drive growth. Leasing penetration remains limited but is increasing as rail infrastructure improves and private logistics participation expands. Demand is concentrated in hopper and tank cars, with intermodal leasing emerging slowly from a low base.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Deploy Long-term Contracts and Fleet Modernization to Secure a Competitive Edge

The global railcar leasing market trends are characterized by competition centered on fleet scale, asset diversification, service capabilities, and access to long-term capital. Leading players such as GATX, TrinityRail, Wells Fargo Rail, SMBC Rail Services, Union Tank Car Company (UTLX), VTG, Ermewa, and Touax compete by offering large, modern fleets covering tank cars, hoppers, and intermodal equipment. Competitive advantage increasingly depends on full-service leasing, regulatory compliance expertise, and the ability to redeploy railcars across regions and commodities. Companies strengthen positioning through fleet modernization, long-term contracts, digital fleet monitoring, and partnerships with financial institutions to optimize funding costs. Strategic portfolio rebalancing and asset sales are also used to focus on higher-yield segments and improve returns.

- In May 2025, Wells Fargo announced the sale of its rail leasing asset portfolio, highlighting ongoing consolidation and strategic realignment within the global railcar leasing industry.

LIST OF KEY RAILCAR LEASING COMPANIES PROFILED

- GATX Corporation (U.S.)

- TrinityRail (U.S.)

- Wells Fargo Rail (U.S.)

- SMBC Rail Services (U.S.)

- Union Tank Car Company (UTLX) (U.S.)

- Greenbrier Leasing (U.S.)

- North American Railcar Leasing (NARL) (U.S.)

- Progress Rail Leasing (U.S.)

- VTG AG (Germany)

- Ermewa Group (France)

- Touax Rail (France)

- Wascosa AG (Switzerland)

- AAE Rail Leasing (Austria)

- Railpool GmbH (Germany)

- Mitsui Rail Capital (MRC) (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: GATX and Brookfield Infrastructure completed the acquisition of Wells Fargo’s rail leasing operation via their joint venture, closing on January 1 and publicly confirming completion on January 5. This marks one of the largest portfolio shifts in railcar leasing, expanding scale and reshaping competitive positioning.

- January 2026: Trinity Industries completed the strategic restructuring of its railcar investment partnerships with Napier Park, finalizing transactions on December 30, 2025. The move highlights how leasing platforms use structured partnerships and balance-sheet actions to optimize capital, returns, and fleet strategy through market cycles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Railcar Type, By Lease Type, By Lease Duration, By End-Use Industry, and By Region |

|

By Railcar Type |

· Tank Cars · Hopper Cars · Boxcars · Flatcars & Well Cars |

|

By Lease Type |

· Full-Service Leases · Net (Operating) Leases · Finance / Long-Term Capital Leases |

|

By Lease Duration |

· Short-Term Leases (≤3 years) · Medium-Term Leases (3–7 years) · Long-Term Leases (>7 years) |

|

By End-Use Industry |

· Chemicals & Petrochemicals · Energy, Petroleum & Bulk Minerals · Agriculture & Food Commodities · Construction & Industrial Materials · Automotive, Intermodal & Logistics |

|

By Geography |

· North America (By Railcar Type, By Lease Type, By Lease Duration, By End-Use Industry, and By Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) o Mexico (By End-Use Industry) · Europe (By Service Type, By Dealership Function, By End-Use Industry, By Deployment Model, and By Country) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Service Type, By Dealership Function, By End-Use Industry, By Deployment Model, and By Country) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Rest of the World (By Service Type, By Dealership Function, By End-Use Industry, and By Deployment Model) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.43 billion in 2025 and is projected to reach USD 18.20 billion by 2034.

In 2025, the market value stood at USD 8.28 billion.

The market is expected to grow at a CAGR of 5.3% during the forecast period from 2026 to 2034.

The medium-term leases segment leads the market share in terms of lease duration.

Asset-light logistics strategies is a key factor driving the market.

Top players in the market include GATX, TrinityRail, Wells Fargo Rail, and SMBC Rail Services.

North America accounts for the largest share in the market.

North America, Europe, Asia Pacific, and the rest of the world are the regional markets considered.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us