Recycled Concrete Market Size, Share & Industry Analysis, By Product Type (Recycled Concrete Aggregate (RCA) and Recycled Concrete Powder (RCP)), By Application (Road Base & Sub-base, Structural Fill & Embankments, Non-Structural Concrete Production, and Others), and Regional Forecast, 2026-2034

Recycled Concrete Market Size and Future Outlook

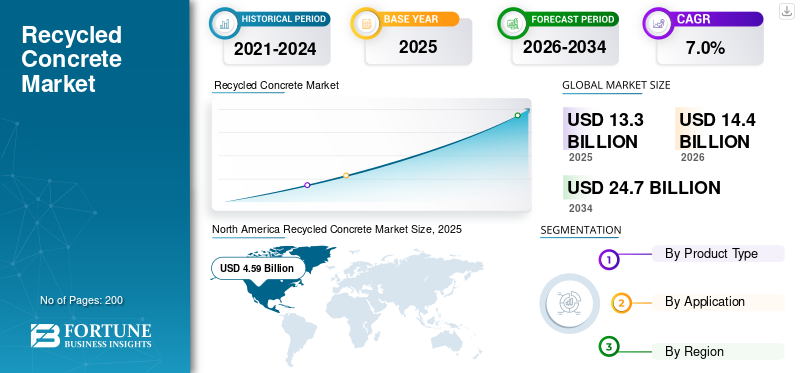

The global recycled concrete market size was valued at USD 13.3 billion in 2025. The market is projected to grow from USD 14.4 billion in 2026 to USD 24.7 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. North America dominated the recycled concrete market with a market share of 33.98% in 2025.

The recycled concrete market is progressing steadily as the construction sector shifts toward more responsible material usage and waste management practices. Expanding urban development and infrastructure upgrades are increasing the need for affordable and resource-efficient building inputs. The product supports this transition by enabling the reuse of demolition materials while delivering dependable performance in civil and structural applications. Strengthening environmental policies and broader adoption of circular construction approaches are driving the recycled concrete market growth.

Key players such as Heidelberg Materials, HOLCIM, CEMEX Group, Vulcan Materials, and Breedon Group plc strengthen their presence in the market through advanced recycling facilities, integrated supply networks, and consistent material quality to meet diverse requirements across infrastructure development, road construction, civil engineering, and sustainable building applications.

Download Free sample to learn more about this report.

RECYCLED CONCRETE MARKET TRENDS

Increasing Focus on Sustainable Construction and Circular Economy Practices Creates New Market Trend

A prominent trend in the market is the rising emphasis on sustainable construction materials and circular economy principles. Governments, developers, and contractors are increasingly prioritizing materials that reduce landfill waste, conserve natural resources, and lower the carbon footprint of infrastructure projects. The product is gaining traction as it enables the reuse of construction and demolition waste while maintaining dependable performance in road base, structural fill, and non-structural applications. This shift toward resource efficiency and responsible material sourcing is encouraging broader adoption across public infrastructure, commercial developments, and urban redevelopment projects.

- According to the European Commission, construction and demolition waste accounts for approximately 35–40% of total waste generated in the European Union, and under the EU Waste Framework Directive, Member States are required to achieve a minimum 70% recovery rate for non-hazardous construction and demolition waste.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Infrastructure Development and Urban Expansion Support Market Growth

The market is significantly driven by rising construction and infrastructure activities across transportation, residential, commercial, and industrial sectors. Increasing investments in roads, highways, bridges, urban redevelopment, and public utilities are creating sustained demand for cost-effective and durable construction materials. This product is widely used in road base, sub-base layers, structural fill, and non-structural concrete applications due to its reliable load-bearing capacity and suitability for large-scale civil works.

- According to a Reuters report, the world needs to invest USD 94 trillion in infrastructure by 2040, with annual spending required at approximately USD 3.7 trillion to meet global demand. This large-scale infrastructure requirement supports sustained demand for construction materials, including cost-efficient and sustainable materials.

MARKET RESTRAINTS

High Transportation Costs and Logistical Constraints Limit Market Expansion

The market faces challenges related to high transportation and handling costs. Since the product is a heavy and low-value material per unit weight, its economic viability is highly dependent on the proximity between recycling facilities and construction sites. Long-distance transportation can significantly increase overall project costs, reducing the price advantage compared to locally sourced natural aggregates. Additionally, the limited availability of well-distributed recycling infrastructure in certain regions can restrict supply consistency and timely delivery.

- According to the U.S. Geological Survey (USGS), construction aggregates such as crushed stone and sand & gravel are low unit-value, high-bulk materials, and their transportation costs can represent a significant portion of the final delivered price, often limiting the economic shipping distance.

MARKET OPPORTUNITIES

Rising Government Support for Sustainable Infrastructure Creates New Market Opportunities

The market presents significant growth opportunities as governments increasingly promote sustainable infrastructure development and waste reduction initiatives. Public authorities are encouraging the reuse of construction and demolition materials through regulations, green procurement policies, and recycling targets. Expanding investments in smart cities, transportation networks, and resilient infrastructure further create avenues for increased adoption.

- According to the U.S. Environmental Protection Agency (EPA), of the 600 million tons of C&D debris generated in 2018, approximately 313 million tons were directed to aggregate reuse applications. This demonstrates the growing institutional support and practical implementation of recycled materials in construction, reinforcing opportunities for secondhand concrete adoption in infrastructure and civil projects.

MARKET CHALLENGES

Material Quality Variability and Standardization Gaps Create Market Challenges

The market faces challenges related to variations in material quality and the absence of uniform standards across regions. Since this product is produced from construction and demolition waste, differences in source material, contamination levels, and processing methods can affect consistency and performance. Contractors and project developers may hesitate to adopt recycled materials where technical specifications or certification frameworks are unclear.

- According to the European Commission’s Joint Research Centre (JRC), variability in composition and contamination levels of construction and demolition waste can impact the quality consistency of recycled aggregates, underscoring the need for standardized quality control and certification frameworks.

Segmentation Analysis

By Product Type

Cost Efficiency, Structural Reliability, and Broad Application Base Support the Dominance of the Recycled Concrete Aggregate Segment

Based on product type, the market is segmented into recycled concrete aggregate (RCA) and recycled concrete powder (RCP).

Recycled Concrete Aggregate (RCA) holds the largest recycled concrete market share due to its wide applicability and strong demand across infrastructure and civil construction projects. RCA is extensively used in road base, sub-base layers, structural fill, embankments, and non-structural concrete applications, making it the most commercially viable and widely accepted recycled product type. The large volume requirements in transportation and urban development projects further reinforce RCA’s leading position within the overall market.

- According to Science Direct, aggregates account for approximately 80–85% of concrete pavement and 60–75% of asphalt pavement by volume, and secondhand concrete aggregate (RCA) is widely evaluated for use in pavement sublayers, rigid layers, and flexible layers due to its structural performance and sustainability benefits. This supports the dominant position of RCA within secondhand concrete applications.

The Recycled Concrete Powder (RCP) segment is expected to grow at a CAGR of 6.2% over the forecast period.

By Application

Extensive Infrastructure Usage and High Volume Requirements Support Road base & Sub-Base Segment Leadership

In terms of application, the market is categorized into road base & sub-base, structural fill & embankments, non-structural concrete production, and others.

To know how our report can help streamline your business, Speak to Analyst

The road base & sub-base segment holds the largest share of the market, driven by its extensive use in transportation infrastructure and civil engineering projects. This product is widely utilized in highways, urban roads, parking areas, and foundation layers due to its dependable load-bearing capacity and cost efficiency. These applications require large material volumes, making road construction one of the most significant consumption channels for secondhand concrete.

- According to the Federal Highway Administration (FHWA), concrete is routinely recycled into the U.S. highway system, and the principal application of secondhand concrete aggregate in the United States has been as a base material. This confirms that road base and sub-base applications represent the leading utilization segment for secondhand concrete.

The structural fill & embankments segment is expected to grow at a CAGR of 6.7% over the forecast period.

Recycled Concrete Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Recycled Concrete Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant position in the market in 2025, valued at USD 4.59 billion, and is expected to maintain its leading position in 2026, reaching USD 4.97 billion. The region’s leadership is supported by established recycling infrastructure, strong highway rehabilitation programs, and well-defined regulatory frameworks promoting construction and demolition waste recovery. Extensive road networks, continuous maintenance of aging infrastructure, and steady public infrastructure funding contribute significantly to material demand.

U.S. Recycled Concrete Market

Based on North America’s strong contribution and the country’s advanced highway recycling practices, the U.S. market was valued at USD 4.33 billion in 2025, accounting for approximately 94.2% of regional revenues. Large-scale roadway reconstruction projects, structured state-level recycling programs, and routine use of secondhand crushed concrete aggregate in base and sub-base layers support domestic demand.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific represents a high-growth regional market for recycled concrete, projected to reach a valuation of USD 3.44 billion in 2025. Rapid urbanization, large-scale transportation infrastructure projects, and continuous expansion of residential and commercial construction support demand. Increasing government focus on sustainable construction practices and resource efficiency is encouraging the reuse of construction and demolition materials across major economies.

China Recycled Concrete Market

The Chinese market in 2025 reached a valuation of USD 0.59 billion, accounting for approximately 17.1% of regional revenues. Extensive highway expansion, urban redevelopment initiatives, and large-scale infrastructure modernization programs drive demand. The country generates substantial volumes of construction and demolition waste, creating strong potential for recycled aggregate utilization.

Europe

Europe is expected to demonstrate stable growth in the market, and the regional market reached a valuation of USD 4.07 billion in 2025. Strict waste management regulations, well-established recycling systems, and a strong emphasis on circular economy principles support the region’s progress. High construction activity in transportation infrastructure, urban redevelopment, and public works projects sustains demand for recycled aggregates. Environmental compliance requirements and landfill diversion targets further encourage the use of recycled concrete in road base and civil engineering applications.

Germany Recycled Concrete Market

Germany’s market reached a valuation of USD 0.27 billion in 2025, accounting for approximately 6.7% of regional demand. The regional growth is driven by infrastructure rehabilitation projects, highway modernization programs, and structured construction waste recovery systems. The country’s strong regulatory oversight and focus on sustainable building practices promote consistent utilization of recycled aggregates.

Italy Recycled Concrete Market

The Italian market in 2025 was valued at USD 0.22 billion, representing roughly 5.4% of regional revenues. The growing demand is supported by residential renovation, transportation upgrades, and the increasing implementation of recycling practices within the construction industry. Public infrastructure improvements and regional redevelopment programs contribute to sustained recycled concrete usage, particularly in base and sub-base applications.

Latin America, the Middle East, and Africa

Latin America and the Middle East & Africa regions are projected to experience steady growth in the market during the forecast period. The Latin America market reached a valuation of USD 0.32 billion in 2025, supported by expanding transportation networks, urban housing projects, and increasing adoption of construction waste recycling practices. Infrastructure rehabilitation programs and gradual improvements in waste management frameworks are encouraging the use of recycled aggregates across civil works. The Middle East & Africa market was valued at USD 0.84 billion in 2025, driven by large-scale infrastructure developments, road expansion projects, and rising emphasis on sustainable building materials in public construction initiatives.

Brazil Recycled Concrete Market

The Brazilian market in 2025 was valued at USD 0.12 billion, accounting for approximately 38.9% of revenues. The demand is supported by roadway development, urban redevelopment programs, and growing attention to resource-efficient construction practices. Investments in transportation corridors, housing expansion, and municipal infrastructure upgrades continue to support recycled concrete utilization, particularly in road base and sub-base applications.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in the Market

The market remains moderately consolidated, as large-scale operations require established recycling infrastructure, efficient material recovery systems, and compliance with environmental and construction standards. Significant investment in crushing facilities, sorting technologies, quality assurance processes, and logistics networks creates entry barriers for new participants. Additionally, project approvals and technical specifications in public infrastructure projects often require proven performance records, further favoring established players.

Leading companies such as Heidelberg Materials, HOLCIM, CEMEX Group, Vulcan Materials, and Breedon Group plc focus on expanding recycling capabilities, optimizing processing efficiency, strengthening regional supply networks, and ensuring consistent material quality to sustain their competitive position, rather than relying solely on aggressive capacity additions.

LIST OF KEY RECYCLED CONCRETE COMPANIES PROFILED

- Heidelberg Materials(Germany)

- HOLCIM (Switzerland)

- CEMEX Group (Mexico)

- Vulcan Materials. (U.S.)

- Breedon Group plc (U.K.)

- GBM Recycled Concrete (U.K.)

- Arcosa, Inc. (U.S.)

- Colorado Aggregate Recycling (U.S.)

- RUBBLE MASTER (Austria)

- Sika AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- December 2025: HOLCIM completed the acquisition of Thames Materials (UK) and a majority stake in A&S Recycling GmbH (Germany), and signed an agreement to acquire a C&D recycler in Northwest France; combined 1.3 million tons/year permitted processing capacity to scale Holcim’s ECOCycle circular construction platform.

- October 2024: Heidelberg Materials commissioned an industrial concrete recycling facility in Poland (near Katowice) designed to recycle 100% of demolition concrete into recycled aggregates, sand, and cement paste for reuse in building materials.

- May 2024: Heidelberg Materials acquired B&A Group, a construction soil and aggregate recycling company, strengthening the regional supply of recycled aggregates and circular services.

- May 2024: Heidelberg Materials completed the acquisition of Mick George Group, the market leader in construction & demolition waste recycling in parts of the UK, expanding its recycled-materials platform.

- January 2024: Arcosa, Inc., announced agreement to acquire Stavola’s Construction Materials business (NY–NJ area), which includes recycled aggregates sites (plus quarries, asphalt plants), strengthening aggregates-led materials footprint.

- April 2023: HOLCIM acquired Sivyer Logistics (UK), a major recycler/handler of construction & demolition waste in London, supporting Holcim’s circular construction ambitions, recycled aggregates, and manufactured soils.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Product Type, Application, and Region |

| By Product Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 13.3 billion in 2025 and is projected to reach USD 24.7 billion by 2034.

Recording a CAGR of 7.0%, the market is slated to exhibit steady growth during the forecast period.

The road base & sub-base application segment led in 2025.

North America held the highest market share in 2025.

Rising infrastructure development and increasing use of recycled construction materials are driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us