Refractories Market Size, Share & Industry Analysis, By Form (Bricks & Shaped and Monolithics & Unshaped), By Product (Clay and Non-Clay), By Alkalinity (Acidic & Neutral and Basic), By End-Use Industry (Iron & Steel, Non-Ferrous Metals, Glass, Cement, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

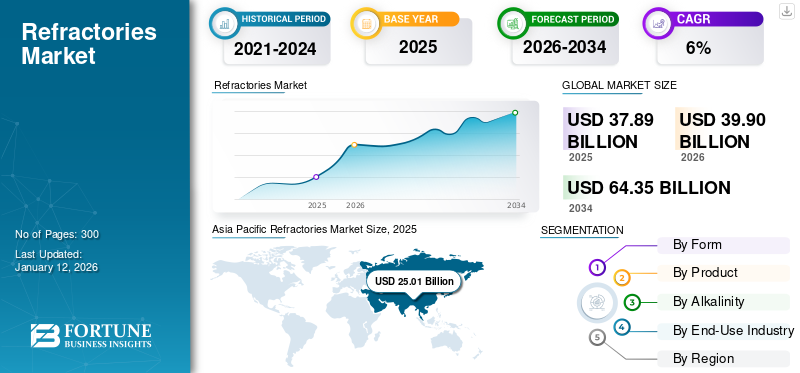

Refractories Market Size and Future Outlook

The global refractories market size was valued at USD 39.18 billion in 2025. The market is projected to grow from USD 41.39 billion in 2026 to USD 64.60 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the refractories market with a market share of 67.20% in 2025.

Refractories are heat-resistant materials used in various industries to withstand high temperatures in processes such as steel and glass production. They are essential for furnaces, kilns, and reactors, providing durability and efficiency in extreme heat conditions. They can be made from different compounds and minerals, such as alumina and silica, chosen based on their ability to endure specific thermal and chemical stresses. Key properties of refractory include heat resistance, ability to resist thermal shock, strength, and low thermal conductivity, ensuring energy efficiency and long-lasting thermal processing equipment.

The market is dominated by several major players, including Saint-Gobain, Imerys, Intocast Group, RHI Magnesita, and Posco Chemical, which are at the forefront of the industry.

Download Free sample to learn more about this report.

REFRACTORIES MARKET TRENDS

Recycling of Refractory Products to Foster Market Development

The need for recycling refractory products is increasing owing to the rising cost of raw materials, while environmental regulations have compelled companies to seek sustainable alternatives for refractory applications. Taxes on emissions and landfill sites are also being imposed, and tax benefits are introduced to boost the waste recycling efforts among companies. Hence, the recycling of refractories helps reduce production costs for manufacturers, thus offering lucrative growth opportunities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Focus on Infrastructure Development by Developing Countries to Provide Growth Opportunities for the Market

The rising population, especially in developing countries such as China, India, and Brazil, has prompted their governments to focus on development in order to provide safer housing, infrastructure, and related facilities. Infrastructure development activities have increased the uptake of products, such as cement, glass, steel, and other non-metallic minerals. These products require refractory materials during the manufacturing process, which is heat-intensive in nature. Thus, as the demand for these products is projected to expand in the future, the growth of the industry is expected to mirror this increasing demand.

Government initiatives to highlight the importance of the product for making steel and cement have significantly changed the mindset of market players. Moreover, incentivizing the market will help develop the local capabilities to manufacture refractories to meet the growing demand. Additionally, China and India are among the fastest-growing economies globally, and the rising demand for travel requires constant development of transportation infrastructure in these countries.

MARKET RESTRAINTS

Carbon-Intensive Manufacturing Processes to Create Environmental Concerns and Increasing Regulatory Implementation

The U.S. has introduced regulations for the disposal of waste generated from refractory and guidelines concerning the use of these materials to encourage the recycling of chrome-based refractory, which are in high demand in the iron & steel industry. Similarly, projects such as the Review and Improvement of Testing Standards for Refractory Products (ReStaR) in Europe are being executed to ensure the accuracy and reliability of current testing standards for refractory products in the region. Such stringent environmental regulations and rules on the use of refractory materials are expected to hinder the refractories market growth.

MARKET OPPORTUNITIES

Industrial Decarbonization and Furnace Modernization to Strengthening Demand for Advanced Refractories

A major opportunity for the market lies in the global shift toward industrial decarbonization, furnace modernization, and higher operating efficiency across the steel, cement, glass, non-ferrous metals, petrochemicals, and waste-to-energy industries. As heavy industries adopt electric arc furnaces, hydrogen-ready steelmaking, alternative fuels in cement kilns, energy-efficient glass furnaces, and cleaner thermal-processing systems, the operating environment for linings is becoming more demanding. This is increasing the need for advanced refractories with better thermal-shock resistance, corrosion resistance, insulation performance, and longer service life.

This trend creates strong value-growth potential, even in regions where volume growth is moderate. End users are increasingly focused on reducing downtime, improving lining life, lowering energy consumption, and reducing CO₂ emissions per production cycle. As a result, suppliers that offer high-performance monolithics, engineered bricks, insulating refractories, precast shapes, and application-specific service support are well positioned to gain market share. The opportunity is especially strong in India, Southeast Asia, the Middle East, and parts of North America, where new capacity additions and modernization projects are occurring alongside stricter efficiency and sustainability targets.

MARKET CHALLENGES

Raw Material Volatility and Energy-Cost Pressure to Challenge Margin Stability

A key challenge for the market is the volatility in raw material and energy costs, particularly for magnesia, alumina, bauxite, graphite, zircon, silicon carbide, and high-grade clay-based inputs. Refractory production is energy-intensive, and many raw materials are geographically concentrated, especially in China and a few mineral-rich regions. Any disruption in mining, export controls, logistics, power costs, or environmental regulation can quickly affect input availability and pricing. This creates uncertainty for refractory manufacturers and makes long-term pricing contracts more difficult to manage.

The impact is especially significant as many refractory end-use industries, such as steel and cement, are highly price-sensitive and often resist rapid cost pass-through. In times of weak steel or construction activity, suppliers may face margin pressure even when input costs remain elevated. Smaller and regional producers are more exposed as they may lack backward integration, global sourcing networks, or pricing power. Therefore, companies will need to focus on raw material security, recycling of spent refractories, localized supply chains, and value-added product differentiation to protect profitability.

Segmentation Analysis

By Form

Bricks & Shaped Segment Holds the Largest Market Share Due to Strong Demand from Key Industries

Based on form, the market is classified into bricks & shaped and monolithic & unshaped.

The bricks & shaped segment accounted for the largest refractories market share in 2025 on account of heavy requirements of such products from the metal and non-metal industries. Refractory bricks and blocks are refractory shapes that are stacked to form insulating furnaces, boilers, or other thermal process vessel walls. Typically, refractory bricks are cemented together with refractory mortar. Refractory shapes also include catalyst supports, which often consist of porous structures with large surface areas, or honeycomb structures that hold a metal catalyst, providing easy exposure to a stream of reactive gases or other reactants.

Monolithic & unshaped refractories are increasingly capturing market share globally owing to their enhanced flexibility, shorter installation durations, diminished risk of joint-related failures, and their appropriateness for maintenance-intensive operations. These categories encompass castables, gunning mixes, ramming masses, plastics, mortars, coatings, and dry vibratables. The segment benefits from the rising preference for abbreviated shutdown periods, expedited repair cycles, and lowered total ownership costs across industries such as steel, cement, aluminum, petrochemical, and foundry. In steel manufacturing, monolithics are progressively employed in ladles, tundishes, runners, and repair areas. Moreover, the segment is expected to grow at a CAGR of 6.0% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Product

Clay Segment Led Market Due to Low-Cost

Based on product, the market is segmented into clay and non-clay.

The clay segment held the largest market share in 2025, due to its lower price compared to the non-clay section. Fireclay bricks and insulation products are made of clay materials and are heavily consumed by iron & metal product manufacturers. Furthermore, raw materials for the production of refractory clay products are easily available, which will strengthen this segment’s market dominance.

Specific production processes are relatively corrosive due to strong acids and bases, which will drive the market for non-clay refractory products. They offer superior resistance to corrosion compared to their regular clay counterparts. Moreover, the segment is expected to grow at a CAGR of 4.2% during the forecast period.

By Alkalinity

Backed by Large Demand the Acidic & Neutral Segment to Gain Substantial Market Share

Based on alkalinity, the market is segmented into acidic & neutral and basic.

The acidic & neutral segment accounted for the largest market share in 2025, as the demand for these materials is expanding at a considerable rate. An acidic refractory is a type of refractory material with silica as its main component. Such refractory material can resist acid slag erosion, but it can easily react to alkaline slag erosion in high-temperature environments. As the properties of acidic refractory are quite different from those of basic refractory, the uses of such material are also different.

Basic refractories are those that are attacked by acid slags but stable to alkaline slags, dusts, and fumes at high temperatures. Since they do not react with alkaline slags, this refractory is quite important for furnace linings where the environment is alkaline, such as during steelmaking operations. Moreover, the segment is expected to grow at a CAGR of 6.0% during the forecast period.

By End-Use Industry

Iron & Steel Segment to Lead Market Due to Wide Applications

In terms of end-use industry, the market is categorized into iron & steel, non-ferrous metals, glass, cement, and others.

The iron & steel industry constitutes the largest end-use sector for refractory materials globally, as refractory products are indispensable at nearly every high-temperature stage of steel production. These stages include blast furnaces, basic oxygen furnaces, electric arc furnaces, ladles, tundishes, reheating furnaces, and continuous casting systems. The demand for refractories is closely correlated with crude steel output, capacity utilization rates, and the intensity of secondary metallurgy processes. Although global steel demand has experienced a period of weakness, Worldsteel anticipates stabilization in global steel demand by 2026, with an expected acceleration in 2027.

Cement constitutes the second principal demand segment for refractories, with consumption predominantly focused on rotary kilns, preheaters, precalciners, coolers, kiln hoods, and lime kilns. Investments in infrastructure, housing development, urbanization, road construction, and industrial expansion primarily drive the demand. In developed economies, this segment is largely replacement-driven. However, in India, Southeast Asia, Africa, and parts of Middle Eastern countries, growth continues to be fueled by new cement capacity and increased kiln utilization. Moreover, the segment is expected to grow at a CAGR of 5.6% during the forecast period.

The non-ferrous metals segment encompasses refractories utilized in the production and processing of aluminum, copper, zinc, nickel, lead, and other metals. Applications include smelting furnaces, holding furnaces, converters, anode baking furnaces, refining vessels, and transfer systems. Demand is driven by aluminum manufacturing in China, the Gulf region, India, Canada, and Australia, as well as copper and battery-related activities across Latin America, China, Africa, and parts of Southeast Asia. Consequently, the segment presents greater potential for value growth than its volume share alone indicates, particularly for high-performance monolithic and shaped products employed in aluminum and copper operations.

Refractories Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Refractories Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the dominant share, valued at USD 24.21 billion, and continued to lead in 2025, with a valuation of USD 26.33 billion. China held a major market share due to higher demand from the iron & steel industry. China and India are the world’s leading manufacturers of cement and cement-based products. The region is experiencing high demand for cement due to the rapid expansion of the building & construction industry. Additionally, both countries are major exporters of cement globally.

China Refractories Market

By 2026, the Chinese market size is projected to reach USD 0.43 billion. China remains the largest market globally as it is still the world’s biggest steel, cement, glass, non-ferrous metals, and industrial furnace base. However, growth is becoming more moderate as the country moves from capacity-led expansion toward replacement, efficiency, and modernization-led demand.

To know how our report can help streamline your business, Speak to Analyst

Japan Refractories Market

The Japanese market value in 2026 is estimated to be around USD 2.75 billion, accounting for roughly 6.6% of the global revenues.

India Refractories Market

The Indian market size in 2026 is estimated at around USD 3.38 billion, accounting for roughly 8.2% of global revenues.

Europe

Europe is expected to experience steady market growth over the forecast period. In Europe, refractory materials play a triple role by providing mechanical strength, protection against corrosion, and thermal insulation. They are adapted to each specific application through fine-tuning and careful choice of raw materials and processing. This, along with the major presence of the automotive industry in the region, is creating significant growth opportunities for the market. During the forecast period, the European region is projected to grow at a 3.8% rate. It is further estimated to reach a valuation of USD 6.04 billion in 2026.

Italy Refractories Market

The Italy market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 1.6% of global revenues.

Germany Refractories Market

Germany’s market in 2026 is estimated at around USD 1.14 billion, accounting for roughly 2.8% of global revenues.

North America

North America is a mature but high-value market led by the U.S., with additional demand from Canada and Mexico. Demand is supported by steel, cement, lime, glass, foundry, aluminum, petrochemicals, and energy applications. The region’s volume growth is moderate, but value growth is stronger due to technical product requirements, higher labor costs, engineered refractory systems, and service-intensive maintenance models.

U.S. Refractories Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 3.78 billion in 2026, accounting for roughly 9.1% of global sales.

Latin America and the Middle East & Africa

Latin America is a mid-sized market led by Brazil and Mexico. Demand is supported by steel, cement, mining, non-ferrous metals, glass, foundry, and industrial furnace applications. Brazil is the region’s largest industrial base, with refractory demand tied to steel, cement, mining, and non-ferrous processing. At the same time, Mexico benefits from automotive, steel, glass, foundry, and nearshoring-linked manufacturing growth. The Latin America market is projected to reach USD 1.22 billion by 2026.

The Middle East & Africa market is smaller than Asia Pacific in absolute volume but has a favorable long-term growth profile due to steel, cement, aluminum, glass, petrochemicals, and infrastructure-led industrialization. GCC countries support demand through aluminum smelting, cement, glass, and petrochemical processing, while Turkey and Iran have large steel and cement bases.

GCC Refractories Market

The GCC market in 2026 is estimated at USD 0.45 billion, accounting for approximately 1.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Market Share through Acquisitions and Capacity Expansions

This market is fragmented, with many global and local players operating in the market. To gain a competitive edge in the market, companies are continuously investing in emerging and developed economies to launch new products, expand their production capacities, collaborate with distributors, and engage in strategic acquisitions. However, increasing the production capacity to reach the maximum number of consumers and cater to diversified applications is the primary strategy being adopted by most players in this industry. Companies such as Imerys, Intocast Group, and Posco Chemical are heavily investing in strengthening their capabilities and enhancing their market positions.

LIST OF KEY REFRACTORIES COMPANIES PROFILED

- Saint-Gobain (France)

- Imerys (France)

- RHI Magnesita (Austria)

- POSCO Future M Co., Ltd. (South Korea)

- KAEFER SE & Co. KG (Germany)

- Beijing Lier High-Temperature Materials Co., Ltd. (China)

- HarbisonWalker International (U.S.)

- Intocast Group (Germany)

- Alsey Refractories Co. (U.S.)

- Magnezit Group (Russia)

- Vesuvius (U.K.)

- Puyang Refractories Group Co., Ltd. (China)

- Refratechnik Holding GmbH (Germany)

- Ruitai Materials Technology Co., Ltd. (China)

- Plibrico Company, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Imerys signed an agreement to acquire Great Lakes Minerals, a U.S.-based processor and distributor of minerals for the refractory and abrasive industry. Further, signaling a strategic move to strengthen its Solutions for Refractory, Abrasives and Construction portfolio with calcined bauxite, mullite, and fused alumina while expanding its North American refractory raw-material footprint.

- March 2026: HWI officially opened its new Fulton lightweight monolithics facility, emphasizing the investment's commercial and supply-chain impact. The company stated that the plant is vertically integrated through direct access to local clay reserves and includes a purpose-built furnace for GREENLITE aggregate production, robotic automation, and upgraded packaging options.

- December 2025: HWI announced the completion of construction of its new lightweight monolithics production facility in Fulton, Missouri, confirming that the expansion had materially increased the company’s production capability in this category.

- July 2025: HWI entered a strategic manufacturing partnership with Electrified Thermal Solutions to develop and produce electrically conductive firebricks for the Joule Hive thermal battery.

- June 2025: INTOCAST commissioned a new high-performance tempering kiln at its Oberhausen plant, strengthening its MgO-C brick manufacturing capabilities and further modernizing one of Europe’s advanced shaped refractories production sites.

- January 2025: RHI Magnesita completed the acquisition of Resco Group, calling it the Group’s most significant investment since the 2017 merger and highlighting stronger North American customer solutions, greater local-for-local production, and improved supply security for refractory users in cement, steel, aluminum, and other industrial sectors.

- March 2024: INTOCAST officially announced construction of a new production plant in Huntingdon, Tennessee, dedicated to MgO-C refractories and related materials for the American market, marking a major manufacturing expansion in North America.

REPORT COVERAGE

The global refractories market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Form, By Product, Alkalinity, End-Use Industry, and Region |

| By Form |

|

| By Product |

|

| By Alkalinity |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 39.18 billion in 2025 and is projected to reach USD 64.60 billion by 2034.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period.

By end-use industry, the iron & steel segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Increase in the demand for metals and glass from various end-use industries is the key factor driving the market’s growth.

- 2021-2034

- 2025

- 2021-2024

- 300

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us