Renewable Energy Certificate Market Size, Share & Industry Analysis by Type (Compliance and Voluntary), By Form (Unbundled Certificates and Bundled Certificates), By End-User (Corporates, Utilities, Household/Retail, and Others), Regional Forecast, 2026-2034

Renewable Energy Certificate Market Size and Future Outlook

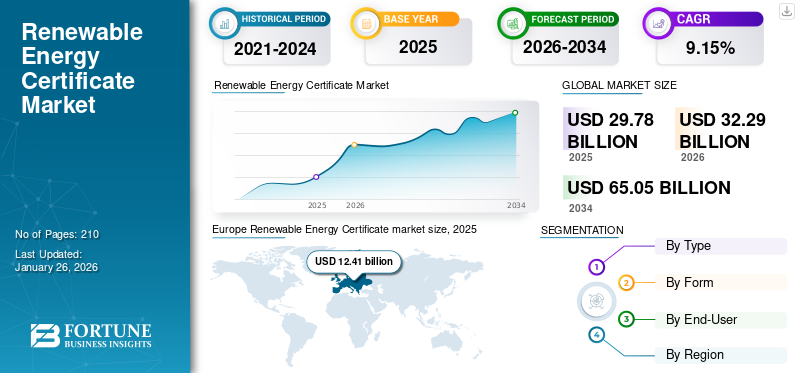

The global renewable energy certificate market size was valued at USD 29.78 billion in 2025 and is projected to grow from USD 32.29 billion in 2026 to USD 65.05 billion by 2034, exhibiting a CAGR of 9.15% during the forecast period.Europe dominated the global market with a share of 41.67% in 2025.

The renewable energy certificate (REC) demand is increasing globally owing to various regulatory, corporate compliances, and sustainability initiatives. Organizations around the globe are making commitments to sustainability initiatives such as RE100 and achieving net-zero emissions. Since RECs offer a flexible and cost-effective means to prove renewable energy consumption without having to invest directly in projects, these certificates are gaining popularity globally. In addition, governments and states require the adoption of renewable energy through Renewable Portfolio Standards (RPS), as RECs play a crucial role in meeting the compliance mechanism.

Moreover, frameworks such as the GHG Protocol acknowledge RECs for reporting Scope 2 emissions, making them vital for ESG reporting. Increasing pressure from consumers and investors is also driving companies to demonstrate sustainable energy practices, while international standards such as International Renewable Energy Certificates (I-RECs) enhance the accessibility of REC utilization in global markets. Consequently, RECs are becoming a more popular, scalable, and credible option for achieving clean energy objectives in both compliance and voluntary markets.

For instance, in 2023, the I-REC(E) program issued 283 million certificates, representing 283 TWh of renewable electricity generation, a ~42% increase over 2022. During the same year, redemptions reached 176 million certificates (176 TWh), growing ~81% compared to 2022. Each Solar Renewable Energy Certificates (SRECs) equals 1 MWh of solar electricity, with U.S. markets trading millions annually to help states meet renewable portfolio standards.

Major players in the renewable energy certificate (REC) market include South Pole, 3Degrees, Shell Energy, Statkraft, Engie, Ørsted, and Tata Power. These companies lead in renewable energy sourcing, certificate trading, and carbon offset solutions facilitating global compliance and voluntary REC programs that drive corporate sustainability and decarbonization goals.

Download Free sample to learn more about this report.

Renewable Energy Certificate Market Key Takeaways

- 2025 Market Size: USD 29.78 billion

- 2026 Market Size: USD 32.29 billion

- 2034 Forecast Market Size: USD 65.05 billion

- CAGR: 9.15% from 2026–2034

- Europe dominated the renewable energy certificate market with a 41.67% share in 2025.

- The compliance segment is projected to account for a 61.88% market share in 2026.

- The unbundled certificates segment is projected to hold a 62.06% market share in 2026.

Europe

Europe generated USD 12.41 billion in 2025 and maintained its leadership position due to strong renewable energy regulations and sustainability commitments.

North America

North America accounted for 30.85% of the global market in 2025 and is projected to reach USD 10.01 billion in 2026.

Asia Pacific

Asia Pacific captured 16.86% of global revenue in 2025 and is projected to grow at a CAGR of 12.38% during the forecast period.

U.S.

The renewable energy certificate market is projected to reach USD 9.57 billion by 2026.

Japan

The renewable energy certificate market is projected to reach USD 0.47 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growing Adoption of Renewable Energy Certificates in the Utility & Energy Sector to Propel the Market Growth

The utility & energy sector is among the fastest-growing areas for RECs as power companies use these certificates to comply with Renewable Portfolio Standards (RPS) and similar regulations. Utilities often purchase RECs to meet state or national renewable obligations when direct renewable generation is not sufficient. Under RPS requirements, utilities or load-serving entities must procure or generate a set minimum share of their electricity from eligible renewable sources; RECs act as a compliance tool to satisfy that requirement.

When utilities are unable to completely fulfil their renewable energy requirements through their own generation, they frequently acquire RECs from outside sources, such as renewable generators or REC brokers, to bridge the deficit. Certain states permit the use of unbundled RECs for compliance, although utilities might encounter restrictions, such as some investor-owned utilities (IOUs) facing limitations on the extent to which they can rely on unbundled RECs, while public utilities might enjoy greater leeway.

For instance, according to Lawrence Berkeley National Laboratory, in numerous U.S. states with Renewable Portfolio Standards (RPS), the expenses associated with compliance are significant. These costs have typically constituted about 4% of retail electricity prices in states enforcing RPS, although the impact varies greatly across states based on REC pricing and the specific design of the policy. Thus, RECs help reduce greenhouse gas emissions by certifying that electricity was generated from renewable, zero- or low-carbon sources.

MARKET RESTRAINTS:

Price Volatility to Restrict Market Expansion

A significant challenge hindering the renewable energy certificate market growth is price volatility. Since REC markets are closely linked to regulatory shifts, fluctuations in supply and demand, and inconsistent renewable generation, prices can experience sharp variations. For instance, according to Oil Price Information Service, LLC, the PJM Tri-Qualified REC forward price surged from approximately USD 24.75/MWh in June 2022 to USD 37.24/MWh in June 2023, which is a 50% increase over the year. Such extreme price changes complicate cost forecasting, long-term procurement planning, and budget stability for utilities, project developers, and corporations.

In regions with high levels of renewable energy adoption (such as Texas and California), oversupply or abrupt policy changes have resulted in significant REC price volatility, eroding confidence in long-term agreements.

MARKET OPPORTUNITIES:

Evolving Sustainability Initiatives and Corporate Climate Commitments to Create Growth Opportunities

The renewable energy certificate (REC) market presents numerous growth possibilities fueled by changing policies, corporate climate pledges, and improved tracking systems. A significant opportunity exists in the voluntary corporate sector, where numerous large companies are setting more ambitious sustainability goals and increasingly depending on RECs as a versatile means to showcase renewable energy consumption, particularly in areas where direct purchasing or onsite generation may be difficult. For instance, according to OSTI.gov, in the U.S., in 2022, approximately 9.6 million retail electricity customers acquired around 272 million MWh of voluntary renewable energy, which accounted for about 38% of non-hydro renewable energy sales.

Another potential area of growth is in emerging markets and regions lacking established certification systems. Global REC frameworks such as I-REC(E) are extending their presence in Asia, Africa, Latin America, and other areas, allowing businesses in these regions to engage in worldwide sustainability initiatives. This indicates significant growth potential in markets that are still building their renewable energy infrastructure and regulatory environments.

RENEWABLE ENERGY CERTIFICATE MARKET TRENDS:

Rapid Rise in the Issuance and Redemptions of I-RECs (International Renewable Energy Certificates) is a Key Market Trend

A notable trend in the REC industry is the swift increase in the issuance and redemption of International Renewable Energy Certificates (I-RECs). According to Renewable Energy Certificate [REC] Registry of India, by mid-2025, approximately 227 million I-REC(E) certificates had been issued worldwide during the initial seven months, representing a rise of about 12% compared to the same period in 2024. Concurrently, close to 187 million certificates were redeemed (or retired), reflecting an annual increase of roughly 8%. In February 2025 alone, global redemptions reached 45.1 TWh, a significant jump from 32.8 TWh in February 2024. This marks one of the highest monthly demands in recent history. These trends suggest a growing adoption and use of RECs across various markets. Additionally, there is regional expansion, with emerging markets gaining traction. As per data from the Ministry of Communications, Brazil is at the forefront of issuance volumes in 2025, having issued around 54 million I-RECs already this year, thereby exceeding its total for 2024.

Other countries such as Guatemala, Peru, Saudi Arabia, Kenya, Bangladesh, India, and Kazakhstan have experienced a notable increase in certificate issuance, indicating a broader geographic presence. According to the International Monetary Fund, Saudi Arabia, in particular, witnessed an increase from roughly 5.3 million certificates in 2024 to over 11 million in 2025. In the voluntary green power market in the U.S., changing procurement models are altering demand patterns. According to National Renewable Energy Laboratory (NREL), in 2022, approximately 9.6 million retail customers bought around 272 million MWh of voluntary green power, accounting for about 38% of non-hydropower renewable energy sales. By 2023, nearly 46% of voluntary renewable energy was acquired through long-term agreements, and bundled models overtook unbundled REC sales for the first time.

MARKET CHALLENGES:

Credibility Issues Due to Overcounting to Hamper the Market Growth

One of the major challenges faced by the renewable energy certificate market is the issue of double-counting or overlapping claims regarding the same environmental attribute. This situation arises when a single megawatt-hour of renewable energy generation is claimed by multiple entities, such as a utility (for regulatory compliance) and a corporate purchaser (for voluntary claims), or due to inconsistencies between different registries. The U.S. EPA cautions that double-counting “can lead to credible accusations of greenwashing” and significantly undermine the integrity of REC markets.

In addition, there is a lack of standardization and harmonization among registries and jurisdictions. Different regions have varying definitions of eligibility criteria, distinct verification and retirement processes, and utilize separate registry platforms. The presence of regional, national, and global REC systems that lack alignment complicates both cross-border trading and corporate procurement.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Use of Compliance RECs to Meet Renewable Energy Targets to Drive Segment Growth

On the basis of segmentation by type, the market is classified into compliance and voluntary.

In 2026, the compliance segment is projected to dominates with a 61.88% share. Compliance Renewable Energy Certificates (RECs) have emerged as a fundamental element in renewable energy markets, acting as the primary mechanism for utilities and energy suppliers to fulfil legally mandated renewable energy obligations. Currently, 31 states, along with the District of Columbia, in the U.S. enforce Renewable Portfolio Standards (RPS) or equivalent clean energy mandates, which stipulate that a certain percentage of electricity sold to consumers must originate from renewable sources. RECs are issued from renewable energy projects such as solar farms, wind turbines, biomass plants, and hydropower facilities that generate clean electricity.

Compliance RECs serve as the official proof that renewable electricity has been produced and integrated into the grid, allowing utilities to demonstrate their compliance with state regulations. In the absence of RECs, tracking renewable attributes across various power markets would lack a standardized approach. One key factor contributing to their widespread use is the flexibility and cost-effectiveness they offer. Many utilities are unable to directly own or procure enough renewable generation due to geographic, financial, or regulatory limitations. By acquiring compliance RECs, they can reconcile the difference between their generation capacity and their procurement obligations.

The voluntary segment is experiencing the fastest growth and is expected to grow at a CAGR of 11.51% over the forecast period. Voluntary RECs have become increasingly popular as organizations, institutions, and individuals seek to lessen their carbon footprints beyond what is required by regulations. In contrast to compliance RECs, which are enforced by renewable portfolio standards at the state or national level, voluntary RECs enable electricity consumers to select renewable energy regardless of their geographical location or local energy resources. This adaptability has transformed them into a vital tool for companies aiming for net-zero emissions, meeting RE100 commitments, or adhering to science-based targets, particularly when direct procurement of renewable energy or on-site generation is not an option.

By Form

Affordability, Scalability, and Flexibility to Drive the Unbundled Certificates Segment Growth

In terms of form, the market is categorized into unbundled certificates and bundled certificates.

The unbundled certificates segment is projected to dominant a segment in the market with a share of 62.06% in 2026. Unbundled certificates are popular as they offer a flexible, cost-effective, and easily accessible means for both organizations and individuals to claim the use of renewable energy without needing to directly purchase or produce renewable electricity. Another key factor contributing to their appeal is their affordability. Typically, unbundled RECs are the most economical choice for providing renewable energy consumption compared to entering into long-term Power Purchase Agreements (PPAs) or funding on-site renewable initiatives. For instance, in voluntary markets, unbundled RECs have historically been priced at just a few dollars per megawatt-hour, making them attainable for small businesses, universities, and even individual homeowners.

The bundled certificates segment is anticipated to grow at the highest CAGR of 11.31% during the forecast period. Bundled Renewable Energy Certificates (RECs) are favored as they merge the actual delivery of renewable energy with the associated environmental benefits into a single transaction, allowing buyers a more straightforward and trustworthy method to assert their use of renewable energy. A major factor that makes bundled certificates appealing is that they are frequently linked to new or recently developed renewable initiatives, meaning that the buyer’s investment contributes to increasing the capacity on the grid. This is especially critical for organizations aiming to fulfil ambitious objectives under initiatives such as RE100 or the Science-Based Targets initiative, where stakeholders require proof of authentic climate impact.

By End-User

Corporations Widely Use RECs to Meet Their Carbon Neutrality & Sustainability Goals

In terms of end-user, the market is categorized into corporates, utilities, household/retail, and others.

The corporates segment is projected to dominates the global renewable energy certificate market share of 58.83% in 2026. This segment holds the largest market share of 58.38% in 2025. Companies from various sectors are some of the biggest purchasers of Renewable Energy Certificates (RECs) as they offer a viable, trustworthy, and adaptable method for fulfilling sustainability and climate goals. Numerous organizations have set bold objectives such as RE100 (100% renewable electricity), achieving net-zero emissions by 2050, or adopting science-based targets, and RECs serve as one of the most attainable means to showcase their use of renewable energy.

For instance, the corporates depend on RECs as they are established and standardized tools monitored through registries such as PJM Generation Attribute Tracking System (PJM GATS), New England Power Pool Generation Information System (NEPOOL GIS), Western Renewable Energy Generation Information System (WREGIS), and I-REC(E). This level of transparency minimizes reputational risks and offers reassurance to investors, customers, and regulators regarding the credibility of their renewable energy claims. The corporates segment is anticipated to grow at a CAGR of 10.89% during the study period.

To know how our report can help streamline your business, Speak to Analyst

Renewable Energy Certificate Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Renewable Energy Certificate market size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

Europe accounted for USD 12.41 billion in 2025, representing 41.67% of the global market share, and is projected to reach USD 13.32 billion in 2026. The demand for Renewable Energy Certificates (RECs) in Europe is increasing due to a mix of regulatory requirements, corporate sustainability pledges, and changing consumer expectations. A significant factor is the European Union's Renewable Energy Directive (RED II), which establishes a mandatory target of at least 42.5% renewable energy in final energy consumption by 2030, aiming for a target of 45%. Member states are required to implement policies to achieve these objectives, and Guarantees of Origin (GOs), which serve as the European equivalent of RECs, function as the standard mechanism for tracking and verifying renewable energy claims. This regulatory framework guarantees consistent demand from utilities, energy providers, and corporations.

In 2025, the Germany market is projected to estimate and reached USD 3.36 billion. Germany exhibits one of the highest demands for Renewable Energy Certificates, known as Guarantees of Origin (GOs) in Europe, driven by a combination of policy, corporate, and consumer influences. As the largest electricity market within the EU, Germany plays a key role in the region’s transition to clean energy. The country’s Renewable Energy Sources Act (EEG) has established ambitious renewable energy goals, as part of the EU Renewable Energy Directive II (RED II). The Japan market is projected to reach USD 0.47 billion by 2026, the China market is projected to reach USD 2.22 billion by 2026, and the India market is projected to reach USD 0.94 billion by 2026.

- For instance, according to European Commission, Germany is required to help achieve the EU-wide objective of at least a 42.5% share of renewable energy by 2030. GOs serve as the standardized method for tracking and certifying renewable electricity, making them essential for both utilities and businesses.

North America and Asia Pacific

North America contributed 30.85% to the global market in 2025, with a valuation of USD 9.19 billion, and is projected to reach USD 10.01 billion in 2026. Other regions, such as North America and the Asia Pacific, are anticipated to witness notable growth in the coming years. During the forecast period, the Asia Pacific is projected to record a growth rate of 12.38%, with a valuation of USD 5.02 billion in 2025. Asia Pacific is home to some of the largest and rapidly expanding electricity markets, such as China, India, Japan, South Korea, and the Southeast Asian region, which are experiencing a sharp rise in energy demand alongside increasing pressure to reduce carbon emissions. The International Energy Agency (IEA) reports that in 2023.

Asia Pacific

The Asia Pacific market was valued at USD 5.02 billion in 2025, capturing 16.86% of global revenue, and is estimated to reach USD 5.56 billion in 2026. the Asia Pacific region was responsible for nearly 60% of the worldwide additions to renewable energy capacity, with China alone contributing over 216 GW of new renewable installations that year. This significant rise in energy generation is directly enhancing the availability of Renewable Energy Certificates (RECs) and boosting trading activities. Backed by these factors, China is expected to record the valuation of USD 2.22 billion in 2026 and the rest of the Asia Pacific, USD 0.67 billion, in 2025. The Japan market is projected to reach USD 0.47 billion by 2026 and the India market is projected to reach USD 0.94 billion by 2026.

After Asia Pacific, the market in North America is estimated to have reached USD 10.01 billion in 2026 and secure the position of the second-largest region in the market. In the region, the U.S. is estimated to have reached a valuation of USD 9.57 billion in 2026.

Middle East & Africa

The market in Middle East & Africa reached USD 1.1 billion in 2025, representing 3.70% of total market revenue, and is projected to reach USD 1.18 billion in 2026. In the Middle East and Africa, the market growth is driven by the ambitious renewable energy objectives of nations and the demand from global corporations has spurred progress. Countries such as Saudi Arabia, the UAE, South Africa, and Kenya have quickly advanced their renewable energy initiatives. As an illustration, Saudi Arabia released over 11 million I-RECs in 2025, compared to approximately 5.3 million in 2024, demonstrating its rapid expansion of renewable projects in alignment with Vision 2030. In the Middle East & Africa, GCC is set to have recorded a value of USD 0.32 billion in 2025.

Latin American

In 2025, the Latin America market stood at USD 2.06 billion, representing 6.91% of global demand, and is projected to grow to USD 2.22 billion in 2026. Over the forecast period, the Latin America and Middle East & Africa regions are anticipated to show tremendous opportunities for renewable energy certificates as countries such as Brazil, Chile, Colombia, and Mexico are emerging as REC leaders. Brazil is particularly significant as in 2025 alone, it issued more than 54 million I-RECs by mid-year, surpassing its entire 2024 total.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vendors to Enhance Market Presence through Expanded Supply of RECs, Innovation, Digitalization, and Sustainability Partnerships

3Degrees, Inc., STX Group, EDF Trading Limited, and others are acknowledged as major participants in the market as each firm is very experienced, innovative, and has invested heavily in the sector.

In September 2025, PT Mitra Stania Prima (MSP), an Indonesian-based mining & smelting company, strengthened its sustainability efforts by purchasing Renewable Energy Certificates (RECs) from Indonesia’s state utility PLN. Each REC, representing 1 megawatt-hour (MWh) or 1,000 kilowatt-hours (kWh) of renewable electricity, serves as a verified instrument of clean energy use. The initiative enhances MSP’s production efficiency and also provides international recognition for its commitment to renewable energy. In addition, the solar panel projects generate RECs that validate the production of renewable, zero-emission electricity.

LIST OF KEY RENEWABLE ENERGY CERTIFICATE MARKET PROFILED:

- 3Degrees, Inc. (U.S.)

- STX Group (Netherlands)

- EDF Trading Limited (U.K.)

- Sterling Planet (U.S.)

- AFS (Netherlands)

- Engie (France)

- Ecohz (Norway)

- REDEX (Singapore)

- Evolugen (Canada)

- Statkraft (Norway)

- Shell Energy (U.K.)

- Enel Spa (Italy)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, India’s Central Electricity Regulatory Commission (CERC) proposed amendments to its REC Regulations, expanding eligibility to self-consumption projects, introducing a Virtual Power Purchase Agreement (VPPA) framework, and revising certificate multipliers to favor storage and emerging technologies.

- In March 2025, the Astana International Exchange (AIX) began trading International Renewable Energy Certificates (I-RECs), a key step in advancing Kazakhstan’s sustainable finance and carbon market. The first trade saw London-based Valor Carbon purchase 1,000 I-RECs from Samruk-Green Energy. I-RECs, active in over 50 countries, certify renewable electricity generation. Added to AIX’s products in September 2024, these instruments highlight Kazakhstan’s green transition.

- In March 2025, the demand for Renewable Energy Certificates (RECs) in Indonesia recorded a rise, with PT PLN (Persero) recently distributing 592 RECs units, equal to 592 MWh of green electricity, to palm oil producer PT Inecda Plantation in Riau. Through PLN’s REC program, customers are assured their electricity consumption comes from renewable sources, recognized globally via the APX Tradable Instrument for Global Renewables (TIGRs) system from the U.S., ensuring international compliance and credibility in renewable energy use.

- In May 2022, India’s Central Electricity Regulatory Commission (CERC) issued a new notification introducing multipliers for Renewable Energy Certificates (RECs), aimed at supporting the adoption of emerging and high-cost renewable technologies. Under this scheme, projects using specific renewable sources will be awarded more than one REC per unit of electricity generated, depending on the tariff range of the technology. The initiative is expected to encourage investment in innovative solutions and accelerate the diversification of India’s renewable energy sector.

- In January 2022, India’s Central Electricity Regulatory Commission (CERC) issued a new notification introducing multipliers for Renewable Energy Certificates (RECs), aimed at supporting the adoption of emerging and high-cost renewable technologies. Under this scheme, projects using specific renewable sources will be awarded more than one REC per unit of electricity generated, depending on the tariff range of the technology. The initiative is expected to encourage investment in innovative solutions and accelerate the diversification of India’s renewable energy sector.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players. RECs represent the attributes of renewable electricity, such as zero emissions, clean generation source, and sustainability, separated from the physical power.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation:

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Years | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.15% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Type |

|

| By Form |

|

| By End-User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 32.29 billion in 2026 and is projected to reach USD 65.05 billion by 2034.

In 2025, the Europe market value stood at USD 12.41 billion.

The market is expected to exhibit a CAGR of 9.15% during the forecast period of 2026-2034.

The corporates segment leads the market by end-user.

The growing adoption of renewable energy certificates in the utility & energy sector is a key factor set to propel the market expansion.

3Degrees, Inc., STX Group, EDF Trading Limited, and others are some of the prominent players in the market.

Europe dominated the market in 2025.

Renewable energy certificate adoption is driven by corporate net-zero commitments, regulatory mandates, cost-effective flexibility, investor and consumer pressure, and global standards such as I-REC enabling credible renewable energy claims.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us