Research Antibodies Market Size, Share & Industry Analysis, By Product (Primary Antibodies, Secondary Antibodies, and Others), By Source (Rabbit, Mouse, Goat, and Others), By Type (Monoclonal Antibodies, Polyclonal Antibodies, and Others), By Technique (Western Blotting, Immunohistochemistry (IHC), Immunofluorescence, Flow Cytometry, ELISA, and Others), By Application (Infectious Diseases, Immunology, Oncology, Stem Cells, Neurobiology, and Others), By End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, CROs/CDMOs, and Others), and Regional Forecast, 2026-2034

Research Antibodies Market Size and Future Outlook

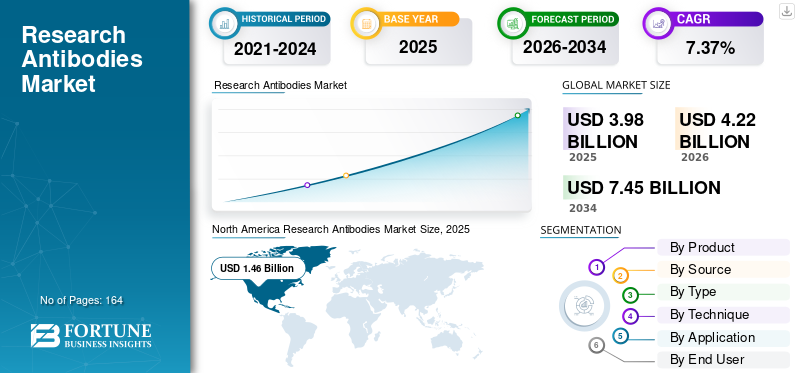

The global research antibodies market size was valued at USD 3.98 billion in 2025. The market is projected to grow from USD 4.22 billion in 2026 to USD 7.45 billion by 2034, exhibiting a CAGR of 7.37% during the forecast period. North America dominated the research antibodies market with a market share of 36.68% in 2025.

The global research antibodies market comprises antibodies used in laboratories to assist scientists in detecting, quantifying, localizing, and characterizing biological targets across various workflows. The market is driven by the ongoing expansion of the global research base, rising demand for well-validated, reproducible antibodies, and the broader adoption of antibody-based tools in oncology, immunology, neurobiology, stem cell research, and studies of infectious diseases. The market for research antibodies is also influenced by increasing demand for high-quality monoclonal and recombinant formats, broader adoption of specialty products such as tag antibodies, controls, and panels, and the rising significance of high-content imaging and cell analysis.

Prominent firms in the worldwide market include Thermo Fisher Scientific Inc., Danaher Corporation, Bio-Techne, Cell Signaling Technology, Merck KGaA, among others. These companies are strengthening their positions through large antibody catalogs, workflow-specific offerings, recombinant and multiplex-ready products, and solutions targeted toward advanced applications in cancer biology, immune profiling, spatial biology, and translational research.

Download Free sample to learn more about this report.

Research Antibodies Market Key Takeaways

- 2025 Market Size: USD 3.98 billion

- 2026 Market Size: USD 4.22 billion

- 2034 Forecast Market Size: USD 7.45 billion

- CAGR: 7.37% from 2026–2034

- North America dominated the research antibodies market with a 36.68% share in 2025.

- The secondary antibodies segment is anticipated to grow at a CAGR of 6.87% during the forecast period.

- The polyclonal antibodies segment is anticipated to expand at a CAGR of 5.68% during the forecast period.

North America

North America led the global market, reaching USD 1.46 billion in 2025.

Asia Pacific

Asia Pacific is projected to reach a market value of USD 1.02 billion by 2026.

Europe

Europe is expected to expand at a CAGR of 6.43% during the forecast period.

U.S.

The market is projected to reach approximately USD 1.39 billion by 2026, accounting for around 33.0% of global revenue.

Japan

The market is expected to reach USD 0.15 billion by 2026, representing roughly 3.6% of global revenue.

Read More

RESEARCH ANTIBODIES MARKET TRENDS

Increasing use in Precision Medicine and Diagnostics is a Remarkable Market Trend

The rising application of precision medicine and diagnostics is a significant trend in the global market, as antibodies are increasingly used to identify, validate, and quantify disease-specific biomarkers that facilitate patient stratification and informed treatment choices. With the growth of precision oncology, spatial biology, and translational pathology, scientists require highly specific and consistent antibodies for protein identification in tissue and cell samples. This is increasing the need for high-quality monoclonal, recombinant, IHC, immunofluorescence, and multiplex-compatible antibody products. The trend is further enhancing the significance of research antibodies for identifying biomarkers, developing assays, and advancing translational discoveries into clinical testing. Consequently, suppliers that possess robust antibody validation, imaging, and biomarker-centered portfolios are becoming increasingly significant in the market. These factors are supporting the overall global research antibodies market growth.

- For instance, in September 2025, Bio-Techne announced that its new spatial biology advancements help researchers and pathologists bridge translational research and clinical applications by enabling the detection of RNA and protein biomarkers on the same tissue section.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand in Drug Discovery and Development is Propelling Market Growth

Rising demand in drug discovery and development significantly influences the market, as antibodies play a crucial role in target identification, target validation, biomarker analysis, pathway mapping, mechanism-of-action studies, and candidate screening. With the expansion of pharmaceutical and biotechnology companies in oncology, immunology, cell therapy, and biologics, there is a growing demand for highly specific, reproducible antibodies to generate reliable preclinical data. Research antibodies play a crucial role in western blotting, flow cytometry, immunohistochemistry, immunofluorescence, and ELISA processes employed in both discovery and translational research. There is a growing need for validated monoclonal antibodies, specialized antibodies, and reagents tailored for specific workflows. The transition to more advanced biologics and precision-targeted treatments is increasing demand for improved antibody tools that can minimize experimental variability and enhance decision-making during early development. Consequently, suppliers with robust validation abilities and extensive portfolios centered on drug discovery are experiencing heightened market demand. All these factors cumulatively drive the overall market growth.

- For instance, in June 2025, Bio-Techne announced a collaboration with the U.S. Pharmacopeia (USP) to distribute USP monoclonal antibody and AAV reference standards with its analytical solutions to support monoclonal antibody and gene therapy product development worldwide.

MARKET RESTRAINTS

High Cost of Premium, Validated, and Recombinant Antibodies to Hamper Market Expansion

The significant expense of premium, validated, and recombinant antibodies is a major market limitation, as these products require more rigorous development, precise sequence definition, lot-to-lot consistency, and broader application validation than conventional formats. Suppliers offer recombinant antibodies with enhanced specificity, consistency, and reliable long-term supply, which improve research quality but also increase the cost per experiment. In budget-conscious academic laboratories and smaller biotech environments, this may postpone the acquisition of high-end antibodies and promote selective over broad portfolio adoption. It may also impede use in standard workflows, as researchers might opt for cheaper traditional reagents unless the demand for reproducibility is extremely high. This limits market growth to a certain extent.

- For example, in February 2025, Abcam published an article in which it explained that only recombinant antibodies meeting stringent quality standards are allowed into its catalog, highlighting the heavy validation burden behind premium products.

MARKET OPPORTUNITIES

Growing Adoption of Recombinant Antibodies for Reproducibility to Offer Growth Opportunities

The rising use of recombinant antibodies for reproducibility represents a significant market opportunity, as research laboratories face growing demands to produce results that are reliable, verified, and consistent across different batches and extended research periods. Recombinant antibodies have defined sequences, which minimizes lot-to-lot variability and decreases the likelihood of performance inconsistencies observed with certain conventional antibody formats. This renders them particularly important in drug development, biomarker research, translational studies, and impactful publication efforts where data dependability is essential. Consequently, an increasing number of researchers are moving towards recombinant monoclonal antibodies for western blotting, IHC, immunofluorescence, and additional sensitive protocols. This trend is allowing suppliers to expand premium recombinant offerings, strengthen validation criteria, and gain market share in research initiatives that prioritize quality. All these factors would drive the market growth in the coming years.

- For instance, in January 2025, Cell Signaling Technology announced that it was named “2025 Recombinant Antibody Supplier of the Year” by CiteAb. Further, the company highlighted that researchers increasingly choose highly validated and reliable recombinant antibodies for publication-quality work, which directly supports the opportunity for suppliers focused on reproducibility-led product adoption.

MARKET CHALLENGES

Antibody Validation and Reproducibility Issues Are a Prominent Challenge to Market Growth

Antibody validation and reproducibility issues remain a major market challenge because research antibodies do not always perform consistently across batches, sample types, and applications. When an antibody shows poor specificity or weak validation data, researchers may generate misleading results, repeat experiments, and spend more time optimizing protocols. This raises the total cost of use and reduces buyer confidence, especially in academic labs and early-stage drug discovery programs. The challenge is even more important in western blotting, IHC, immunofluorescence, and flow cytometry, where application-specific performance is critical. As a result, end users increasingly prefer highly validated antibodies, but this also makes vendor selection stricter and slows the purchasing of poorly characterized products. Overall, reproducibility concerns act as a barrier to wider market expansion because they increase experimental risk and make customers more cautious about reagent spending. All the factors cumulatively affect the market growth.

- For instance, in December 2024, Nature Protocols published an article on the YCharOS protocol for antibody validation, highlighting that poorly performing antibodies contribute to the reproducibility crisis in biomedical research and that validating antibodies remains cumbersome despite millions of antibodies available on the market.

Research Antibodies Market Segmentation Analysis

By Product

Broad Utility Across Core Research Workflows Supported the Primary Antibodies Segment’s Dominance

In terms of product, the market is divided into primary antibodies, secondary antibodies, and others.

The primary antibodies segment captured the largest global research antibodies market share in 2025. The segment’s dominance is due to its direct function in attaching to the target antigen, establishing it as the essential reagent in key procedures like western blotting, immunohistochemistry, and others. Primary antibodies possess the widest catalog range since researchers require target-specific antibodies for oncology, immunology, neurobiology, stem cell, and infectious disease research. The segment’s leadership has been further reinforced by its increased product variety, frequent use in experiments, and rising demand for validated monoclonal and recombinant formats. Moreover, leading suppliers are broadening their application-specific primary antibody portfolios, which is anticipated to maintain the segment's dominance throughout the forecast period.

- For instance, in November 2025, Molecular Instruments and Abcam announced broad compatibility of the HCR HiFi encoder with Abcam’s RabMAb and mouse antibody portfolio for advanced biological research.

The secondary antibodies segment is anticipated to rise with a CAGR of 6.87% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Source

Higher Affinity, Better Sensitivity, and Wider Target Recognition Supported the Rabbit Segment’s Dominance

On the basis of source, the market is divided into mouse, rabbit, goat, and others.

The rabbit segment accounted for the largest market share in 2025. The segment’s dominance can be attributed to the strong binding affinity and broad epitope recognition of rabbit-derived antibodies, which make them highly effective in various workflows. Rabbit antibodies are also widely preferred for difficult targets because they often provide stronger signal intensity and better sensitivity than many conventional alternatives. In addition, the rising adoption of recombinant rabbit monoclonal antibodies has further strengthened this segment by improving batch-to-batch consistency and reproducibility. Their broad use across oncology, immunology, neurobiology, and translational research has also contributed to sustained demand. Furthermore, suppliers continue to expand rabbit antibody portfolios for high-performance research applications, which is expected to support the segment’s leadership over the forecast. Furthermore, the segment is set to hold 46.1% share in 2026.

- For instance, in April 2026, Cell Signaling Technology listed its Annexin A1 (D5V2T) Rabbit Monoclonal Antibody as a newly available product validated for flow cytometry, immunofluorescence, IHC, IP, and western blot.

The goat segment is growing at a CAGR of 6.24% over the forecast period.

By Type

High Specificity, Better Consistency, and Stronger Validation Supported the Monoclonal Antibodies Segment’s Dominance

Based on type, the market is classified into polyclonal antibodies, monoclonal antibodies, and others.

The monoclonal antibodies segment dominated the global market in 2025. The segment’s growth is driven by its high specificity, as monoclonal antibodies bind to a single epitope and therefore provide more targeted and consistent results across research workflows. This makes them highly suitable for various workflows. Additionally, their growing use in biomarker research, oncology, immunology, and translational studies has further strengthened demand. Furthermore, the segment is set to hold 59.4% share in 2026.

- For instance, in October 2025, Bio-Techne launched its ProximityScope assay for the BOND RX platform to support advanced spatial biology workflows.

The polyclonal antibodies segment is anticipated to rise with a CAGR of 5.68% over the forecast period.

By Technique

Wide Routine Use and High Workflow Familiarity Supported the Western Blotting Segment’s Leadership

In terms of technique, the market is divided into western blotting, immunohistochemistry (IHC), immunofluorescence, flow cytometry, ELISA, and others.

The western blotting segment captured the highest share of the global market in 2025. The segment’s dominance can be attributed to its wide use as a standard protein detection method across academic research, drug discovery, cell biology, oncology, and immunology studies. Western blotting remains one of the most common antibody-based workflows because it helps researchers confirm protein expression, compare target levels across samples, and validate findings from other assays. It also uses both primary and secondary antibodies in routine laboratory practice, which supports recurring product demand. In addition, the method is well established, relatively familiar to researchers, and supported by broad catalogs of validated antibodies, loading controls, and detection reagents. Furthermore, the segment is set to hold 25.7% share in 2026.

- For instance, in July 2025, Bio-Techne announced that its Simple Western Technology was used in supporting the U.S. FDA approval of ZEVASKYN, a cell-based gene therapy.

The flow cytometry segment is anticipated to rise with a CAGR of 8.49% over the forecast period.

By Application

High Cancer Research Activity and Broad Use in Translational Studies Supported the Oncology Segmental Growth

On the basis of application, the market is divided into infectious diseases, immunology, oncology, stem cells, neurobiology, and others.

The oncology segment captured the highest share of the global market in 2025. The segment’s growth is driven by the very high use of antibodies in cancer biomarker discovery, tumor profiling, pathway analysis, drug target validation, and tissue-based research. Oncology studies also rely heavily on western blotting, immunohistochemistry, immunofluorescence, and flow cytometry, which increases routine demand for primary and secondary antibodies. In addition, cancer remains one of the most funded and active areas of biomedical research, which supports repeated antibody use across academic, translational, and pharmaceutical settings. Furthermore, the segment is set to hold 28.8% share in 2026.

- For instance, in May 2025, Merck announced that it would present new oncology data across more than 12 tumor types at ASCO 2025.

The stem cells segment is anticipated to rise with a CAGR of 8.72% over the forecast period.

By End User

Large Research Base and Broad Use Across Life Science Studies Supported the Academic & Research Institutes Segment’s Dominance

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs/CDMOs, academic & research institutes, and others.

In 2025, the academic & research institutes segment held the leading position in the global market. The segment’s dominance can be attributed to the large number of universities, public research centers, and nonprofit laboratories that use antibodies regularly in basic and translational research. In addition, academic labs conduct a high volume of exploratory and validation experiments, which creates repeated demand for primary antibodies, secondary antibodies, and specialty antibody products. Furthermore, the segment is set to hold 48.1% share in 2026.

- For instance, in January 2025, Proteintech announced a collaboration with the Abdullah Gül University (AGU) Research and Innovation Center to support advanced imaging and life sciences research.

In addition, CROs/CDMOs are projected to witness 9.66% growth rate during the forecast period.

Research Antibodies Market Regional Outlook

By region, the market is divided into North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

North America

North America Research Antibodies Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 1.39 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 1.46 billion. The region has the strongest biomedical research ecosystem, a large installed base of university and translational labs, and high use of premium validated antibodies across oncology, immunology, and neuroscience research, which is driving the regional market growth.

U.S. Research Antibodies Market

The U.S. market dominated the North American market and will be analytically approximated at around USD 1.39 billion in 2026, accounting for roughly 33.0% of the global market.

Europe

The European market size is anticipated to grow at 6.43% CAGR during the forecast period. Europe’s market growth is supported by a strong public research base, broad academic collaboration, and sustained regional research funding.

U.K. Research Antibodies Market

The U.K. market in 2026 is estimated to be around USD 0.24 billion, representing roughly 5.7% of global revenues.

Germany Research Antibodies Market

Germany's market size is projected to reach approximately USD 0.27 billion in 2026, equivalent to around 6.3% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 1.02 billion by 2026, making it the third-largest region in the global industry. Rising R&D investment, expanding university and biotech research capacity, and increasing adoption of advanced life-science tools are some of the prominent factors driving this market growth.

Japan Research Antibodies Market

The Japanese market in 2026 is set to reach USD 0.15 billion, accounting for roughly 3.6% of global revenues.

China Research Antibodies Market

China’s market is projected to reach revenues of around USD 0.34 million in 2026, representing roughly 8.0% of global sales.

India Research Antibodies Market

The Indian market in 2026 is estimated to reach USD 0.15 billion, accounting for roughly 3.7% of global revenues.

Latin America and the Middle East & Africa

The Middle East & Africa and Latin America regions are likely to witness a slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.28 billion by 2026. Prominent factors such as the gradual strengthening of laboratory systems, better access to diagnostics and public-health lab services, and improving research capability in countries are boosting the market growth in these regions.

In the Middle East and Africa region, the GCC market is projected to reach approximately USD 0.10 billion by 2026, representing about 2.4% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Validation Quality and Application-specific Performance Supported the Market Position of Leading Companies

The global research antibodies market features a moderately fragmented structure with the presence of well-established as well as emerging players in the market. Key companies include Thermo Fisher Scientific Inc., Danaher Corporation, Cell Signaling Technology, Inc., Merck KGaA, Bio-Rad Laboratories, Inc., and Bio-Techne. These companies are increasingly focusing on highly validated antibodies, recombinant formats, workflow-specific products, and broader catalog depth to strengthen their market position.

- For instance, in April 2025, Cell Signaling Technology announced that it was named CiteAb’s 2025 Recombinant Antibody Supplier of the Year.

Additional key contributors include Santa Cruz Biotechnology Inc., Proteintech Group, Inc., GeneTex, Inc., Rockland Immunochemicals Inc., and others. Emphasis on new product expansion, enterprise partnerships, and collaborations is a key strategy undertaken by these players.

LIST OF KEY RESEARCH ANTIBODIES COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- Cell Signaling Technology, Inc. (U.S.)

- Merck KGaA (Germany)

- Bio-Rad Laboratories, Inc. (U.S.)

- Bio-Techne (U.S.)

- Santa Cruz Biotechnology Inc. (U.S.)

- Proteintech Group, Inc. (U.S.)

- GeneTex, Inc. (U.S.)

- Rockland Immunochemicals, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Rockland Immunochemicals introduced Feimin antibodies for metabolic and myokine research. It reflects new antibody product development for emerging biological targets and expands antibody use in metabolic disease and neuroinflammation research.

- September 2025: Proteintech launched Able AI, an AI tool designed to help scientists design experiments and identify relevant products more efficiently.

- October 2024: Proteintech Genomics launched the MultiPro Human Discovery Panel, an antibody-based single-cell multiomics panel that enables profiling of hundreds of proteins alongside whole-transcriptome analysis.

- September 2024: Bio-Techne (Lunaphore) partnered with Discovery Life Sciences to bring COMET spatial biology solutions into clinical research services.

- January 2024: Bio-Techne (Lunaphore) and Advanced Cell Diagnostics (ACD) launched the first fully automated same-section hyperplex multiomics application for spatial biology.

REPORT COVERAGE

The global research antibodies market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.37% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Source, Type, Technique, Application, End User, and Region |

| By Product |

|

| By Source |

|

| By Type |

|

| By Technique |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.98 billion in 2025 and is projected to reach USD 7.45 billion by 2034.

In 2025, the market value stood at USD 1.46 billion.

The market is expected to exhibit a CAGR of 7.37% during the forecast period.

By product, the primary antibodies segment is expected to lead the market.

Increasing usage in drug discovery and development, and increasing demand in oncology and immunology research, are primarily driving market expansion.

Thermo Fisher Scientific Inc., Danaher Corporation, Cell Signaling Technology, Inc., and Merck KGaA are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us