Cell Therapy Market Size, Share & Industry Analysis by Therapy Type (CAR-T Cell Therapy, TCR-T Cell Therapy, Natural Killer (NK) Cells, and Others), By Product (Kymriah, Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, and Others), By Indication (Oncology and Others), By End User (Hospitals & Clinics, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Cell Therapy Market Size and Future Outlook

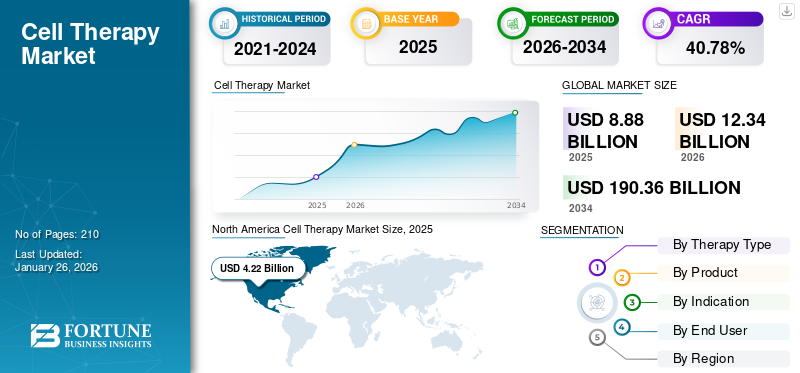

The global cell therapy market size was valued at USD 8.64 billion in 2025. The market is projected to grow from USD 12.22 billion in 2026 to USD 122.87 billion by 2034, exhibiting a CAGR of 33.14% during the forecast period. North America dominated the cell therapy market with a market share of 47.10% in 2025.

Cell therapy or cell-based therapy is a medical treatment that involves the administration of transplanted live cells into a patient to treat or prevent a disease. These therapeutic cells can be collected from the patient themselves (autologous) or from a donor (allogeneic) and then modified in a lab to enhance their ability to destroy diseased cells, regenerate tissue, or restore normal cellular function. The global market is growing rapidly, supported by the rising demand to treat various non-curable diseases, expanding regulatory approvals and accelerated pathways, and increasing investment and strategic collaborations.

The market is dominated by major biopharmaceutical players with Novartis AG, Gilead Sciences, Inc., and Bristol Myers Squibb at the forefront. Factors such as wide product availability, high R&D investments, and advancing pipeline have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

CELL THERAPY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 8.64 Billion

- 2026 Market Size: USD 12.22 Billion

- 2034 Forecast Market Size: USD 122.87 Billion

- CAGR: 33.14% from 2026–2034

- North America dominated the cell therapy market with a 47.10% share in 2025.

- The CAR-T cell therapy segment accounted for 99.8% of the market share in 2025.

- The hospitals & clinics segment held 55.8% of the market share in 2025.

North America

North America reached USD 4.07 billion in 2025, accounting for 47.10% of global market revenue.

Europe

Europe was valued at USD 2.28 billion in 2025 and is projected to grow at a CAGR of 30.80%.

Asia Pacific

Asia Pacific reached USD 1.39 billion in 2025, securing the position of the third-largest regional market.

U.S.

The market was valued at USD 3.79 billion in 2025.

Japan

Cell therapy adoption is expanding alongside the broader growth of the Asia Pacific market.

Read More

MARKET DYNAMICS

MARKET DRIVERS

High Unmet Medical Needs in Oncology and Rare Diseases to Propel Market Growth

High unmet medical needs in oncology and rare diseases play an important role in driving the adoption of cell therapies. The potential for curative, one-time treatments in both oncology (especially for relapsed/refractory cancers) and rare genetic diseases makes cell therapy a high-priority field. Currently, there are around 95% of rare diseases which do not have the U.S. FDA approved treatment. In such cases, these therapies can address rare genetic diseases, many of which are fatal in infancy. Moreover, the personalized nature of cell therapies aligns well with the precision medicine required to treat the unique genetic underpinnings of many rare diseases. Owing to these factors, the demand for cell therapies in rapidly increasing, impelling the global market growth. Additionally, rapid clinical progress in CAR-T and other engineered T-cell therapies, along with increasing approvals and label expansions further propels the market growth.

- According to the World Health Organization Report published in August 2025, around 7.74 million individuals were living with sickle cell diseases in 2021 across the globe. Such a large patient population increases the demand for targeted therapies and is expected to propel the global cell therapy market growth.

MARKET RESTRAINTS

Safety Concerns and Clinical Risks to Restrict Market Expansion

Safety concerns and clinical risks associated with cell therapies limit the market growth to a certain extent. These concerns include tumorigenesis from the cells' growth potential, immune responses such as rejection or graft-versus-host disease (GVHD), and misdirected cell migration to unwanted areas. Additionally, severe side effects such as cytokine release syndrome (CRS) and neurotoxicity can be life-threatening, necessitating specialized care. This limits treatment to certified hospitals with ICU support, restricting widespread adoption.

- For example, according to Gilead Sciences, Inc., Yescarta (axicabtagene ciloleucel), Grade ≥3 neurotoxicity occurred in ~32% of patients with large B-cell lymphoma (LBCL).

MARKET OPPORTUNITIES

Emergence of Allogenic Cell Therapies to Create Lucrative Growth Opportunities

Allogeneic cell therapies are emerging as a transformative medical approach, leveraging healthy donor cells for an "off-the-shelf" solution. These therapies offer enhanced scalability, lower costs, and faster treatment initiation compared to patient-specific autologous therapies. This expanding sector is driven by technological advancements in genetic engineering and manufacturing, with increasing investment and clinical studies focusing on oncology, autoimmune diseases, and neurological conditions.

- For instance, in June 2025, Allogene Therapeutics announced the phase 1 data for ALLO-316. The candidate is an AlloCAR T investigational product targeting CD70 and showed potential in providing clinical benefit in individuals with CD70 TPS ≥ 50% advanced or metastatic renal cell carcinoma (RCC).

CELL THERAPY MARKET TRENDS

Expanding Applications beyond Hematology is one of the Significant Market Trends

Currently, the marketspace is dominated by hematologic cancers. However, in recent years, the operating players are shifting their focus on the development of cell therapies for solid tumors. Due to the huge untapped market, the companies are now designing CAR T cells to recognize multiple antigens simultaneously (dual or tri-CARs) to overcome antigen escape. With growing efforts, the regulatory bodies are also supportive toward approving innovative products for solid tumors.

- For instance, in February 2024, the U.S. FDA approved AMTAGVI (lifileucel) developed by Iovance Biotherapeutics, Inc. It is a T cell immunotherapy indicated for advanced melanoma.

MARKET CHALLENGES

High Treatment Cost to Limit Market Growth

One of the major factors posing challenge to the market growth is the high cost of treatment. These therapies are often high priced owing to their extensive research & development and associated costs. This results in limited accessibility especially in emerging economies with constrained healthcare budgets. Additionally, associated support costs such as hospitalization, monitoring, and follow up care further create a financial burden for the patient.

- For instance, according to Drugs.com data updated in July 2025, the price of Yescarta is around USD 537,592 per treatment regimen.

Download Free sample to learn more about this report.

Segmentation Analysis

By Therapy Type

High Adoption and Investment Support to Propel CAR-T Cell Therapy Segment Growth

On the basis of the therapy type, the market is classified into CAR-T cell therapy, TCR-T cell therapy, natural killer (NK) cells, and others.

To know how our report can help streamline your business, Speak to Analyst

The CAR-T cell therapy accounted for a dominant market share in 2025, representing 99.8% of the total market share. This can be attributed to various factors such as increasing regulatory approvals, strong market adoption, robust clinical pipeline, and broad investment support for the development of innovative products. Additionally, several operating players are actively investing to advance clinical candidates with an aim to get regulatory approval. The confluence of all the above-mentioned factors is anticipated to drive the segment growth.

- According to a study published in the National Center for Biotechnology Information (NCBI) in May 2025, the number of CAR-T clinical trials registered at ClinicalTrials.gov was 1,580 as of April 2024.

By Product

Wide Patient Base Contributed to the Growth of the Yescarta Segment

On the basis of product, the market is classified into Kymriah, Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, and others.

The Yescarta segment accounted for a dominating share of the market in 2025. The dominance of this therapy is majorly driven by its large target patient base, favorable reimbursement landscape, and broad range of approved indications. Moreover, extensive distribution network across the globe also aided the segmental growth.

- For instance, Kite Pharma, the manufacturer of Yescarta, has over 570 authorized treatment centers (ATCs) worldwide, including more than 160 in the U.S. where patients can receive CAR T-cell therapy.

The Abecma segment is likely to witness a growth rate of 13.76% throughout the study period.

By Indication

High Number of Approved Products Fuels Growth of the Oncology Segment

In terms of indication, the market is categorized into oncology and others.

The oncology segment captured the largest cell therapy market share in 2025. In 2025, the segment is anticipated to dominate with 100% share. Key factors responsible for the dominance of the segment include a high number of approved products, rapidly expanding clinical pipeline, expansion of indications to solid tumors, and strong investment flow. Additionally, increasing strategic collaborations between market entities further supplements the segment growth.

- For instance, according to a study published in the journal Nature in May 2024, there are 5,639 interventional cancer cell therapy clinical trials registered, with many ongoing trials still in cancer/oncology indications.

The others segment is projected to reach a market valuation of USD 1.54 billion in 2034.

By End User

Increasing Availability of Cell Therapies in Hospitals & Clinics Propelled Segment Growth

Based on end-user, the market is segmented into hospitals & clinics, specialty clinics, and others.

In 2025, the hospitals & clinics segment dominated the market with the largest share in terms of end-user. Hospitals & clinics are the primary settings where cell therapies can be easily administered. This is due to the presence of specialized infrastructure in large hospitals, availability of multidisciplinary care, and alignment with reimbursement framework. Additionally, an increasing number of hospitals offering cell therapies also supports the segment growth. The segment is set to hold 55.8% share in 2025.

- For instance, in May 2025, Kauvery Hospital in Chennai, India, launched Chimeric Antigen Receptor T cell (CAR-T) therapy for cancer treatment.

The specialty clinics segment is projected to grow at a CAGR of 35.26% over the study period.

Cell Therapy Market Regional Outlook

By geography, the market is divided into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cell Therapy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market, valued at USD 3.02 billion in 2024, and also accounted for the leading share in 2025 with USD 4.07 billion. The dominance of the region in primarily driven by a high number of commercialized products, advanced reimbursement frameworks, and a broad clinical pipeline by operating players. In 2025, the U.S. market is estimated to have reached a value of USD 3.79 billion. The high influx of investment coupled with growing awareness and acceptance among physicians and patients has supported the market growth in the U.S.

- For instance, in July 2025, AstraZeneca announced an investment of USD 50 million across R&D and manufacturing footprint in the U.S. This includes the development of advanced, next-generation manufacturing facilities for cell therapy in California and Maryland.

Asia Pacific and Europe

The Asia Pacific and Europe markets are likely to grow at a noteworthy rate in the coming years. During the forecast period, the European market is anticipated to grow at a CAGR of 30.80%, which is the second largest region amongst all the regions and touch the valuation of USD 2.28 billion in 2025. The regional growth is augmented by strong R&D and clinical adoption, supported by the growing role of regulatory authorities in approving new indications. Backed by these factors, countries including the U.K., Germany, and France are anticipated to have recorded a valuation of USD 0.37 billion, USD 0.55 billion, and USD 0.38 billion respectively in 2025.

After Europe, the market in the Asia Pacific is poised to reach USD 1.39 billion in 2025 and secure the position of the third-largest region in the global market. In the region, the India and China markets are estimated to reach USD 0.08 billion and USD 0.50 billion respectively in 2025.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa markets are anticipated to grow at a slower rate over the study period. The Latin America market, in 2025, is estimated to have recorded a value of USD 0.47 billion. The cell therapy adoption in these regions remains limited due to infrastructure and cost constraints. In the Middle East & Africa, the GCC is set to attain the value of USD 0.24 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on R&D Activities and Expansion of Product Offerings Support the Dominating Position of Leading Companies

The global cell therapy market is characterized by a semi-fragmented structure with the presence of few large biopharmaceutical companies holding significant market share, alongside a growing number of emerging players and specialized startups focusing on innovative platforms. Companies such as Novartis AG, Gilead Sciences, Inc. (Kite Pharma), Bristol-Myers Squibb Company, and Johnson & Johnson (Janssen Biotech) are among the dominant players in this market. These companies offer approved CAR-T therapies, which represent the most widely adopted products in the current market.

The other prominent players include Iovance Biotherapeutics, Fate Therapeutics, and Adaptimmune, and others. These companies are focusing on strategic collaborations, clinical partnerships, and licensing agreements to strengthen their market presence.

- For instance, in April 2025, Fate Therapeutics gained Regenerative Medicine Advanced Therapy (RMAT) Designation for its investigational, off-the-shelf, induced pluripotent stem cells iPSC derived CAR T-cell therapy.

LIST OF KEY CELL THERAPY COMPANIES PROFILED

- Vertex Pharmaceuticals Incorporated (U.S.)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Gilead Sciences, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bristol Myers Squibb Company (U.S.)

- Adaptimmune (U.S.)

- IOVANCE Biotherapeutics, Inc. (U.S.)

- Fate Therapeutics

- Johnson & Johnson (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: The European Medicine Agency (EMA) provided recommendation to grant a conditional marketing authorization for Zemcelpro – a new stem cell therapy in the European Union (EU). It is indicated for the treatment of adults with hematological malignancies.

- June 2025: Bristol Myers Squibb Company announced the U.S. FDA approval for both of its CAR T cell therapies, Abecma to treat multiple myeloma and Breyanzi to treat large B cell lymphoma (LBCL) and other lymphomas.

- April 2025: Thermo Fischer Scientific Inc. introduced the U.S. Advanced Therapies Collaboration Center (ATxCC), a new facility in California, to boost end-to-end cell therapy development from research to commercialization.

- August 2024: The U.S. FDA approved the first T-cell receptor (TCR) therapy, afamitresgene autoleucel or afami-cel (Tecelra), for the treatment of individuals with Advanced Synovial Sarcoma.

- April 2024: The President of India launched NexCAR19, India’s first homegrown anti-Cancer CAR-T cell therapy. It was developed by Tata Memorial Centre, IIT Bombay, and ImmunoACT.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 33.44% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Therapy Type · CAR-T Cell Therapy · TCR-T Cell Therapy · Natural Killer (NK) Cells · Others |

|

By Product · Kymriah · Yescarta · Tecartus · Breyanzi · Abecma · Carvykti · Others |

|

|

By Indication · Oncology · Others |

|

|

By End User · Hospitals & Clinics · Specialty Clinics · Others |

|

|

By Geography · North America (By Therapy Type, Product, Indication, End User, and Country) o U.S. o Canada · Europe (By Therapy Type, Product, Indication, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Therapy Type, Product, Indication, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Therapy Type, Product, Indication, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Therapy Type, Product, Indication, End User, and Country/Sub-region) o GCC o South Africa · Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.64 billion in 2025 and is projected to reach USD 122.87 billion by 2034.

In 2025, the market value stood at USD 4.07 billion.

The market is expected to exhibit a CAGR of 33.14% during the forecast period of 2026-2034.

In 2025, the CAR-T cell therapy segment led the market by therapy type.

The key factors driving the market include high unmet medical needs in oncology and rare diseases, expanding regulatory approvals and accelerated pathways, and increasing investment and strategic collaborations.

Novartis AG, Gilead Sciences, Inc., and Bristol Myers Squibb are some of the prominent players in the market.

North America dominated the cell therapy market with a market share of 47.10% in 2025.

Shift toward personalized medicine and supportive regulatory scenario are some of the factors that are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us