Retro Reflective Materials Market Size, Share & Industry Analysis, By Type (Paints, Inks & Coatings, Films & Tapes, and Others), By Application (Traffic Control & Work Zone, Safety Apparel, Automotive, Industrial, and Others), and Regional Forecast, 2026-2034

Retro Reflective Materials Market Size and Future Outlook

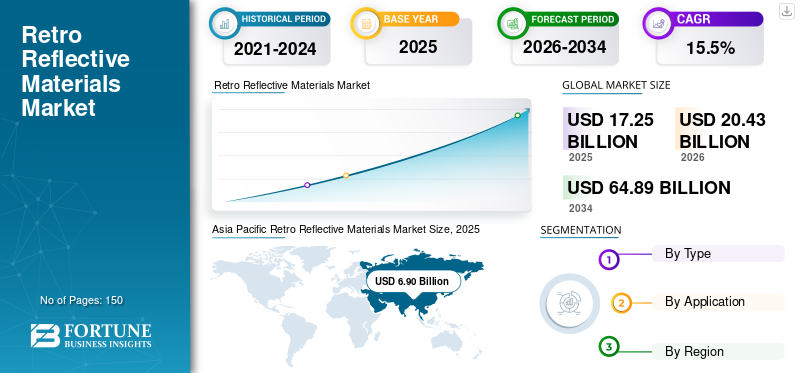

The global retro reflective materials market size was valued at USD 17.25 billion in 2025. The market is projected to grow from USD 20.43 billion in 2026 to USD 64.89 billion by 2034, exhibiting a CAGR of 15.5% during the forecast period. Asia Pacific dominated the retro reflective materials market with a market share of 40% in 2025.

Retro reflective materials are engineered surfaces that return light back toward its source, improving visibility at night and in low-light conditions. They are used mainly in traffic and road signs, pavement markings, safety apparel, and vehicle conspicuity tapes, where fast recognition and safety are critical. Demand is closely tied to road-safety regulations, infrastructure maintenance budgets, and replacement cycles, since outdoor exposure, abrasion, and UV weathering gradually reduce brightness and performance. Globally, the market tends to grow steadily, driven more by compliance-led upgrades and routine replacements than by rapid new demand growth.

The market is dominated by a small group of established manufacturers with large-scale coating and converting assets and proven optical technologies. Major players 3M, ORAFOL Europe GmbH, Avery Dennison Corporation, NIPPON CARBIDE INDUSTRIES CO., INC., and SH Reflective, and regional producers focus on certified product performance, durable outdoor life, and consistent technical support, resulting in a moderately consolidated market characterized by steady replacement demand, high qualification costs, and controlled capacity.

Download Free sample to learn more about this report.

RETRO REFLECTIVE MATERIALS MARKET Key Takeaways

- 2025 Market Size: USD 17.25 billion

- 2026 Market Size: USD 20.43 billion

- 2034 Forecast Market Size: USD 64.89 billion

- CAGR: 15.5% from 2026–2034

- Asia Pacific dominated the retro reflective materials market with a market share of 40% in 2025.

- The films & tapes segment is projected to expand at a CAGR of 15.3% during the forecast period.

- The safety apparel segment is anticipated to grow at a CAGR of 15.7% over the forecast period.

Asia Pacific

Asia Pacific led the market with a value of USD 6.90 billion in 2025 and is expected to reach USD 8.29 billion in 2026, supported by strong road infrastructure development and traffic safety investments.

North America

North America reached USD 3.10 billion in 2025, driven by established roadway safety programs, vehicle conspicuity requirements, and demand for high-visibility safety products.

Europe

Europe accounted for USD 3.62 billion in 2025, supported by stringent road safety regulations, mature transportation infrastructure, and ongoing replacement demand.

U.S.

The U.S. market in 2025 is estimated at USD 2.67 billion. Consumption is driven by traffic control and roadway safety needs, including retroreflective sheeting for signs, reflective elements for pavement markings, and work-zone visibility devices.

Japan

Demand is supported by transportation infrastructure, road safety standards, and the continued use of retro reflective materials in traffic management and industrial safety applications.

Read More

RETRO REFLECTIVE MATERIALS MARKET TRENDS

Shift Toward Higher-Spec, Performance-Verified Reflective Products Is Changing Buying Behavior

A key trend in the market is the move from basic procurement to performance-based visibility, where buyers increasingly focus on how long a sign, tape, or marking can maintain brightness in real-world conditions. This is supporting faster adoption of micro-prismatic reflective films, improved topcoats, and more durable marking optics designed to perform better under UV exposure, abrasion, and wet-night conditions. From a business perspective, customers are placing greater emphasis on certification, consistency, and service life, which is shifting the product mix toward higher-grade materials and favoring suppliers that can support testing, qualification, and compliance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Focus on Road Safety and Nighttime Visibility Sustains Demand

Retro reflective materials demand is primarily driven by increasing requirements for road safety and nighttime visibility across transportation infrastructure, work zones, and personal safety applications. Traffic signs, pavement markings, and vehicle conspicuity tapes rely on retro reflection to improve early driver recognition, especially in low-light, rain, or fog conditions. At the same time, high-visibility apparel for construction, logistics, and emergency services continues to be specified to reduce accident risk and meet safety standards. This broad, regulation- and safety-led adoption creates a clear demand-side pull for retroreflective materials, as higher installation and routine replacement of visibility products directly increase consumption of reflective films, beads, and tapes.

- According to the U.S. Federal Highway Administration (FHWA), work zone crashes in 2022 resulted in an estimated 37,000 injuries in the U.S., reinforcing the ongoing need for high-visibility measures such as retroreflective signs, vehicle markings, and safety apparel.

MARKET RESTRAINTS

Reliance on Government Budgets and Project Timing Can Slow Demand

Retro reflective materials demand is limited by its strong dependence on public road maintenance spending and scheduled procurement for traffic signs, pavement markings, and safety products. When government budgets tighten, tenders get delayed, or maintenance programs are postponed, purchases of reflective sheeting, beads, and conspicuity tapes can drop in the short term. Demand also depends on project timing and seasonal installation windows, since many road works are planned around weather and traffic constraints. As a result, the market can see uneven ordering patterns, even though safety rules still provide a steady baseline level of need.

MARKET OPPORTUNITIES

Upgrades to Higher-Performance Visibility Solutions Are Creating Growth Opportunities

Retro reflective materials are seeing growth opportunities from a shift toward better, longer-lasting visibility products rather than routine replacement. Road agencies are increasingly upgrading to higher-grade reflective sheeting and more durable marking systems to improve nighttime guidance and reduce rework and maintenance. Demand is also expanding beyond roads into commercial vehicle conspicuity, warehouse and industrial safety marking, and micromobility visibility, where operators want clearer identification and lower accident risk. As specifications move from basic compliance to higher performance and longer service life, suppliers of premium films, beads, and conspicuity tapes can capture additional value and incremental volume.

- According to the U.S. National Highway Traffic Safety Administration (NHTSA), 42,514 people were killed in motor vehicle traffic crashes in 2022 in the U.S., reinforcing why agencies continue to prioritize better nighttime visibility measures such as retroreflective signs, markings, and conspicuity tapes.

MARKET CHALLENGES

Balancing Long-Term Visibility Performance with Cost Targets Is a Core Challenge

Retro reflective materials must maintain high brightness for long periods while facing harsh outdoor conditions such as UV exposure, rain, dust, abrasion, and temperature changes. Delivering consistent retro reflectivity over the full service life is challenging because even minor issues in film construction, bead optics, coatings, or lamination can reduce performance and lead to early replacement. At the same time, customers often push for longer warranties and lower total lifecycle cost, limiting how much suppliers can increase pricing to fund higher durability. This trade-off between long-term performance, quality consistency, and cost control remains a key challenge for the retro reflective materials market growth.

Segmentation Analysis

By Type

Road Marking and Surface-Applied Visibility Needs Drive Dominance of Paints, Inks & Coatings Segment

Based on type, the market is segmented into paints, inks & coatings, films & tapes, and others.

The paints, inks & coatings segment accounted for the largest retro reflective materials market share in 2025. This segment drives consumption because retroreflective road markings and surface coatings are applied across high-volume roadway areas, including lane lines, edge lines, pedestrian crossings, symbols, and work-zone guidance, creating a large, recurring material requirement. These systems typically use reflective elements (such as glass beads) to provide nighttime visibility and require regular reapplication due to traffic wear, abrasion, and weathering. As road agencies continue prioritizing clearer lane guidance and safer nighttime driving conditions, paints, inks, and coatings remain the most structurally anchored and volume-heavy outlet within the market.

The films & tapes segment is expected to grow at a steady CAGR of 15.3% over the forecast period, supported by fleet conspicuity requirements, ongoing traffic sign upgrades, and a gradual shift toward higher-grade micro-prismatic films with longer service life.

To know how our report can help streamline your business, Speak to Analyst

By Application

Road Safety and Visibility Compliance Position Traffic Control & Work Zone as the Primary Demand Anchor

By application, the market is segmented into traffic control & work zone, safety apparel, automotive, industrial, and others.

The traffic control & work zone segment accounted for the largest share in 2025. Traffic control and work zones lead product demand because traffic signs, temporary work-zone devices, cones, delineators, barricades, and pavement guidance require reliable nighttime visibility to reduce accident risk and improve driver reaction time. These applications consume large volumes of reflective films, beads, and tapes and also follow planned replacement cycles, since outdoor exposure, dirt, and abrasion gradually reduce brightness and performance. As road agencies continue focusing on safer highways and clearer lane guidance, traffic control and work-zone needs remain a compliance- and maintenance-driven demand base that supports steady consumption beyond one-time infrastructure builds.

The safety apparel segment is expected to grow at a CAGR of 15.7% over the forecast period.

Retro Reflective Materials Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Retro Reflective Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in 2025, valued at USD 6.90 billion, and is expected to retain its leading role in 2026, reaching USD 8.29 billion. The region’s leadership is driven by its extensive road infrastructure, high urbanization, and strong manufacturing of traffic-safety and visibility products. Robust demand from traffic signs and road markings, expanding highway networks, commercial vehicle conspicuity needs, and industrial safety applications support sustained consumption of retro reflective films, beads, and coatings, particularly in high-volume and cost-sensitive deployment programs.

China Retro Reflective Materials Market

Based on Asia Pacific’s strong contribution and China’s large-scale manufacturing footprint, the China market was valued at USD 3.41 billion in 2025, accounting for approximately xx% of global revenues. Demand is supported by extensive road infrastructure expansion and maintenance, high volumes of traffic signs and pavement markings, and strong domestic production of reflective films, glass beads, and safety products. Continued growth in highway networks, urban traffic management, and commercial vehicle conspicuity needs, along with broad industrial safety adoption, further reinforces China’s role as a major consumption and manufacturing hub.

India Retro Reflective Materials Market

India’s market in 2025 accounted for USD 1.03 billion. The growth is supported by expanding road infrastructure and the adoption of pavement markings and upgraded signage. Rising demand for work-zone safety, vehicle conspicuity compliance, and domestic film-and-bead conversion reinforces steady consumption.

North America

North America remains a significant regional market, expected to reach USD 3.10 billion in 2025. Demand is anchored by mature roadway safety programs for traffic signs, pavement markings, and work-zone guidance devices, along with steady use of high-visibility apparel and vehicle conspicuity tapes. The region benefits from established standards, strong product qualification, and regular replacement cycles, though growth stays moderate due to market maturity.

U.S. Retro Reflective Materials Market

The U.S. market in 2025 is estimated at USD 2.67 billion, representing approximately 86.0% of global revenues. Consumption is driven by traffic control and roadway safety needs, including retroreflective sheeting for signs, reflective elements for pavement markings, and work-zone visibility devices, as well as steady demand for high-visibility safety apparel and vehicle conspicuity tapes in commercial fleets and industrial operations.

Europe

Europe is projected to record modest growth, and reached USD 3.62 billion in 2025. The region is characterized by strict road safety standards, mature transport infrastructure, and strong performance requirements for traffic signs, pavement markings, and vehicle conspicuity. Despite slower expansion in mature markets, steady replacement demand, routine road maintenance, and continued use of high-visibility safety apparel support ongoing consumption of retroreflective materials.

Germany Retro Reflective Materials Market

Germany’s market was accounted for USD 0.87 billion in 2025, accounting for about 24.1% of global revenues. Demand is supported by well-maintained road networks, strict traffic safety standards, and automotive and industrial activity using reflective films, tapes, and markings.

U.K. Retro Reflective Materials Market

The U.K. market in 2025 reached USD 0.62 billion, accounting for roughly 17.1% of global revenues. Consumption is concentrated in roadway safety applications, such as traffic signs, pavement markings, and work-zone visibility products, as well as a steady demand for high-visibility safety apparel and vehicle conspicuity tapes used across construction, logistics, and public services.

Latin America, the Middle East, and Africa

Latin America and the Middle East & Africa are expected to see moderate market growth during the forecast period. Latin American market was valued for USD 2.07 billion in 2025, supported by expanding road networks, higher spending on pavement markings and traffic signage, and rising work-zone safety needs in major cities. In the Middle East & Africa, the demand is driven by highway development, routine maintenance programs, and increased use of reflective films, beads, and conspicuity tapes for traffic control and industrial safety. The Middle East & Africa market was valued at USD 1.55 billion in 2025, with growth improving as procurement systems mature.

GCC Retro Reflective Materials Market

The GCC market accounted for around USD 0.78 billion in 2025, about 50.0% of regional revenues. The demand is supported by highway and urban infrastructure projects, upgraded signage and pavement markings, vehicle conspicuity needs, and industrial safety requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in the Market

The market is relatively consolidated and technology-intensive, as complex optical technologies, high investment requirements, and strict performance and regulatory compliance create significant barriers to entry. These factors limit new participation and concentrate supply among a small group of global producers with integrated operations and established manufacturing expertise.

Key players such as 3M, ORAFOL Europe GmbH, Avery Dennison Corporation, NIPPON CARBIDE INDUSTRIES CO., INC., and SH Reflective, and regional producers, focus primarily on optimizing existing assets and strengthening product quality and technical support rather than pursuing aggressive capacity expansion. Recent activities across these companies highlight a strategic emphasis on operational efficiency, cost competitiveness, and gradual adoption of higher-performance reflective technologies to support long-term market positioning.

LIST OF KEY RETRO REFLECTIVE MATERIALS COMPANIES PROFILED

- 3M (U.S.)

- Paiho Group (Taiwan)

- ORAFOL Europe GmbH. (Germany)

- Avery Dennison Corporation (U.S.)

- DM Reflective India (India)

- NIPPON CARBIDE INDUSTRIES CO., INC. (Japan)

- Coats Group plc (U.K)

- SH Reflective (China)

- Aura Optical Systems, L.P. (U.S.)

- Unitika Sparklite Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- September, 2025: ORAFOL acquired Reflomax Co., Ltd. (Korea), and stated the deal enables implementation of innovative reflective technologies within the ORAFOL Group.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 17.25 billion in 2025 and is projected to reach USD 64.89 billion by 2034.

Recording a CAGR of 15.5%, the market is slated to exhibit steady growth during the forecast period.

The traffic control & work zone application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Rising focus on road safety and nighttime visibility standards sustains demand.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us