Specialty Chemicals Market Size, Share & Industry Analysis, By Type (Agrochemicals, Dyes and Pigments, Construction Chemicals, Specialty Polymers, Textile Chemicals, Base Ingredients, Surfactants, Functional Ingredients, Water Treatment, and Others) and Regional Forecast, 2026-2034

Specialty Chemicals Market Size & Outlook

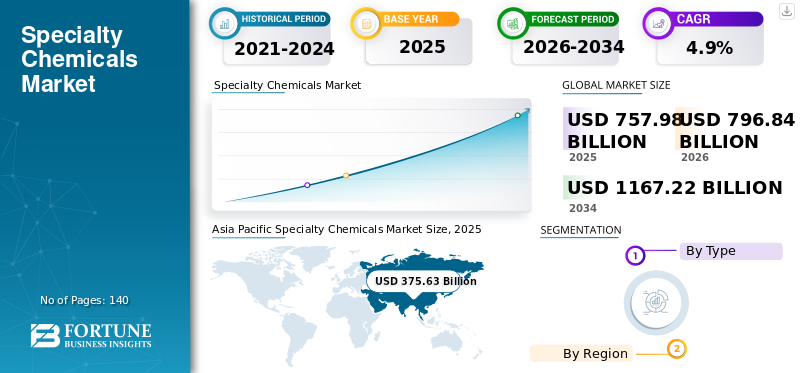

The global specialty chemicals market size was USD 757.98 billion in 2025 and is projected to grow from USD 796.84 billion in 2026 to USD 1,167.22 billion in 2034 at a CAGR of 4.90% during the forecast period 2026-2034. Asia Pacific dominated the specialty chemicals market with a market share of 49.60% in 2025.

The global specialty chemicals market occupies a strategically important position within the broader chemical industry, supported by performance-driven formulations, application-specific functionality, and diversified exposure across industrial value chains. Unlike commodity chemicals, competitive differentiation depends less on production scale and more on technical capabilities, regulatory compliance, intellectual property, and customer qualification processes. Specialty chemicals market growth, therefore, reflects value creation, formulation expertise, and end-market sophistication rather than volume expansion alone.

Demand fundamentals remain closely linked to structural trends across agriculture, infrastructure, healthcare, water management, consumer products, electronics, and advanced manufacturing. Product performance requirements continue to raise the importance of customized solutions capable of improving efficiency, durability, safety, and sustainability outcomes. As downstream industries pursue higher productivity and regulatory compliance, specialty formulations increasingly command stronger pricing power and customer retention characteristics than conventional chemical products.

Portfolio optimization has emerged as a defining strategic theme across the industry. Leading manufacturers are directing investment toward higher-margin businesses, including specialty polymers, electronic chemicals, functional ingredients, water treatment technologies, and bio-based formulations. This migration reflects a broader shift away from undifferentiated chemistry toward solutions supported by technical service, formulation know-how, and long qualification cycles that create meaningful barriers to entry.

Specialty chemicals are used by a plethora of manufacturing industries such as textiles, oil and gas, ink additives, construction, food, and cosmetics. The chemical composition and effectiveness of these compounds determine their use. With the world becoming increasingly concerned about health and safety, the growth in sales of industrial and institutional cleaners (I&I), disinfectants, and sanitizers has expanded at a swifter rate than usual.

According to a report by The Gulf Petrochemicals and Chemicals Association (GPCA), the demand for hand sanitizers and disinfectants in January 2020 increased by 1,400% compared to December 2019. This demand growth has made specialty chemicals manufacturers ramp up their production.

Download Free sample to learn more about this report.

Specialty Chemicals Market Key Takeaways

- 2025 Market Size: USD 757.98 billion

- 2026 Market Size: USD 796.84 billion

- 2034 Forecast Market Size: USD 1,167.22 billion

- CAGR: 4.90% from 2026–2034

- Asia Pacific dominated the specialty chemicals market with a 49.60% share in 2025.

- The agrochemicals segment is projected to account for 27.04% of the market in 2026.

- The dyes and pigments segment is expected to hold a 22.02% market share in 2026.

Asia Pacific

Asia Pacific led the global market with USD 375.63 billion in revenue in 2025 and is expected to maintain its dominance.

North America

North America accounted for 22.40% of global market revenue in 2025 and is expected to reach USD 174.17 billion in 2026.

Europe

Europe represented 18.10% of global demand in 2025 and is projected to grow to USD 140.57 billion in 2026.

U.S.

The specialty chemicals market is projected to reach USD 135.77 billion by 2026.

Japan

The specialty chemicals market is projected to reach USD 49.02 billion by 2026.

Read More

Key Market Dynamics

Market Trends:

Higher Demand for Daily Essential Chemicals to Aid Market Growth

While the market is anticipated to rebound in 2021, the influence and route to recovery will be diverse, given the number of end industries each segment caters to. Market participants are looking to expand their businesses and create a one-of-a-kind blend of novel specialty chemical manufacturing units.

As an example, in January 2021, Huntsman announced that it has agreed to acquire Gabriel Performance Products, a North American manufacturing company dealing with specialty additives and epoxy curing agents, with the goal of expanding its product portfolio. Another such example is LANXESS, which signed an agreement with INTACE SAS, a French biocide company, in January 2021 to expand its business and achieve a competitive advantage as one of the world's leading manufacturers of antimicrobial biocides and fungicides for the packaging sector. Asia Pacific witnessed a specialty chemicals market growth from USD 375.63 billion in 2025 to USD 402.11 billion in 2026.

Download Free sample to learn more about this report.

Many industry players have collaborated to create groundbreaking amenities and innovations by applying advanced resources such as artificial intelligence, which are slated to open new avenues in the market. These chemicals offer a chance to overcome profitability obstacles in the GCC countries, particularly in light of the low crude price environment, while also mitigating China's growing self-sufficiency in commodities.

Portfolio migration toward higher-value chemistries has emerged as one of the defining specialty chemicals market trends. Producers are increasingly allocating resources toward formulations characterized by stronger margins, technical differentiation, and lower exposure to commodity price cycles. Electronic chemicals, specialty polymers, functional ingredients, and advanced water treatment products are attracting significant investment attention.

Circular economy considerations are reshaping innovation priorities across the industry. Manufacturers are developing bio-based formulations, low-carbon ingredients, and recyclable material systems to address customer sustainability targets and regulatory expectations. Product design increasingly incorporates lifecycle considerations and resource efficiency principles.

Digitalization is transforming research, manufacturing, and customer engagement processes. Advanced analytics, process automation, and artificial intelligence tools are improving formulation development and accelerating product optimization. These capabilities support faster innovation cycles and enhance operational efficiency across production networks.

Market Drivers:

Surging Demand for Personal Care Products to Strengthen Growth of the Market

As the effects of the COVID-19 pandemic sweep across the globe, leading manufacturers are observing a considerable increase in the demand for hygiene products such as hand sanitizers, liquid soaps, disinfectant sprays, and germ safeguard wipes. Over the past 12-18 months, chemical companies have noticed an expansion in the consumption of specialty items. They have now assessed their production plans in light of current circumstances and are speedily scaling up and streamlining their production capacities. Therefore, this rising adoption of cleaners and disinfectants has given a quiet boost to the market.

Furthermore, according to a United Nations report, there were 962 million people aged 60 and above in 2017, with the number expected to almost double by 2050. These older folks suffer from advanced age and health conditions such as hair loss and skin deterioration, which will fuel the adoption of cosmetic chemicals, favoring the market. This factor has led to considerable growth in the demand for surfactants and personal care chemicals, driving the growth of the market.

Strong Demand from the Construction Industry to Boost Growth of the Market

The expanding number of development projects around the globe will drive the growth rate in this sector. According to the Global Construction Review Survey, the global construction industry will be valued at USD 8 trillion by 2030, which will be mainly driven by China, India, and the U.S.

This is due to the fact that these chemicals help to improve the structural and decorative properties of a building while also extending its life. They also reduce the need for repairs and help concrete structures retain their strength. Construction chemicals, such as surface treatment chemicals, foaming agents, and coatings, are some of the most critical components of the construction process. As a result, they account for a sizable portion of this market. With the construction industry expected to rejuvenate post-pandemic, it is expected to propel the specialty chemicals market growth.

Industrial performance requirements remain a fundamental growth catalyst for the specialty chemicals market. Manufacturers across agriculture, construction, electronics, healthcare, and consumer industries increasingly prioritize materials capable of improving durability, efficiency, and regulatory compliance. Product differentiation and application-specific performance, therefore, continue supporting demand for value-added chemical solutions rather than undifferentiated formulations.

Infrastructure development represents another important source of specialty chemicals market growth. Rising investment in residential construction, transportation networks, and energy projects supports the consumption of construction chemicals, specialty polymers, coatings, and water treatment solutions. Emerging economies undergoing rapid urbanization are generating additional demand across multiple application categories.

Market Restraints:

Declining Automotive Production to Restraint Market Growth

Chemicals are important in the automotive industry because they are essential for the smooth functioning of a vehicle, besides improving its feel and comfort. Motor oil, for instance, attracts heat away from an engine's combustion chamber and allows its mechanical components to operate smoothly. Rubber blacks are used in wheels and brake pads as performance additives. However, the competition from the availability of less expensive conventional counterparts of specialty chemicals is a major hindrance to this market. In addition to the above, the COVID-19 pandemic has caused unprecedented upheavals in the auto industry in terms of production and demand.

Raw material volatility represents one of the principal challenges affecting the specialty chemicals market. Feedstock costs remain sensitive to fluctuations in crude oil prices, natural gas markets, and supply chain disruptions. Margin pressure frequently emerges when rising input costs cannot be transferred immediately to customers through pricing adjustments, particularly in highly competitive end-use sectors.

Regulatory complexity creates another important constraint. Environmental standards, product safety requirements, and chemical registration frameworks vary significantly across jurisdictions, increasing compliance costs and extending product development timelines. Companies operating globally must manage diverse regulatory regimes while maintaining formulation consistency and customer service levels.

Lengthy qualification cycles may also restrict commercialization speed. Customers in electronics, healthcare, and automotive industries often require extensive testing before approving new materials. Although these barriers support long-term relationships, they can delay revenue generation and increase development expenses for suppliers introducing innovative products.

According to a report published by OICA (Organization Internationale des Constructeurs d'Automobiles), major automotive production globally was around 17.9 billion units, during the first quarter of 2020 and making it to 31.1 billion units in the second quarter, and 52.1 billion units in the third quarter, which was nearly down about 23.1%, 32.4%, and 22.9 % respectively, from the past year.

On a similar note, automobile sales in the markets of Europe, Brazil, Japan, India, China, and the US fell by 27.3%, 15.0%, 24.6%, 30.9%, 10.0%, and 17.0%, respectively. The lowering of automobile production, alterations in raw material costs, and strict government regulations are anticipated to stymie the global market growth.

Market Opportunities:

Water scarcity and environmental protection requirements represent attractive long-term opportunities within the specialty chemicals market. Industrial wastewater treatment, desalination technologies, and resource management initiatives are increasing the demand for advanced treatment chemicals and performance additives. Regulatory pressure surrounding water quality is expected to strengthen investment across both developed and emerging economies.

Healthcare and life sciences applications provide another high-value avenue for expansion. Pharmaceutical ingredients, diagnostic materials, and specialized formulations benefit from stringent qualification requirements and relatively stable demand patterns. Aging populations and increasing healthcare expenditure continue to support long-term consumption visibility.

Energy transition initiatives are creating favorable conditions for specialized materials supporting renewable power systems, battery technologies, and electric mobility applications. Functional chemicals used in energy storage, electronics, and lightweight materials are expected to gain strategic importance as decarbonization efforts accelerate.

Agricultural modernization presents additional growth potential. Precision farming practices and resource optimization requirements are increasing the importance of advanced crop protection technologies and specialty inputs designed to improve productivity. Food security concerns further reinforce investment across agricultural value chains.

Specialty Chemicals Market Segmentation Analysis

By Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Increasing Demand for Food Security to Aid the Dominance of the Agrochemicals Segment

The specialty chemicals market is classified on the basis of type into agrochemicals, dyes and pigments, construction chemicals, specialty polymers, textile chemicals, base ingredients, surfactants, functional ingredients, water treatment, and others.

Agrochemicals:

The agrochemicals segment is projected to account for roughly one-eighth of the market’s share with 27.04% in 2026 and is projected to be the fastest-growing segment during the forecast period. The growing population base, combined with the rising food demand, is increasing the adoption of agrochemicals for improved crop production and protection, fueling the growth of the market.

Food security considerations and agricultural productivity requirements provide the foundation for demand within the agrochemicals segment. Population growth, limited arable land availability, and changing climatic conditions are increasing the need for specialized crop protection products and performance-enhancing formulations. These factors continue to support the segment's strategic importance within the specialty chemicals market.

Yield optimization has become a priority across commercial farming operations. Herbicides, fungicides, insecticides, and advanced adjuvants enable producers to improve output while managing pest pressures and environmental constraints. Precision agriculture practices are also encouraging the adoption of products capable of delivering targeted performance and improved resource utilization.

Furthermore, growing awareness amongst farmers about the use of agrochemicals in agricultural fields also fuels the market’s growth. Moreover, as urbanization and industrial development speed up, agricultural land decreases, leading to a higher demand for agrochemicals to significantly raise crop yield per acre of land, thereby propelling the growth of the market in the upcoming years.

Dyes and Pigments:

The dyes and pigments segment is expected to hold a 22.02% share in 2026. On the flip side, there has been a surging demand for dyes and pigments owing to their manifold end-use applications. The demand for smart paints and coatings that can counter the effects of weather on building construction is expanding, thus boosting the demand for dyes and pigments in recent years.

Color performance and formulation stability remain central considerations within the dyes and pigments segment. Textile manufacturers, packaging producers, coatings companies, and plastics converters depend on specialized colorants capable of delivering durability, consistency, and compliance with increasingly stringent environmental requirements. Product differentiation frequently depends on technical performance rather than cost alone.

Consumer preferences and premiumization trends continue influencing demand patterns. Automotive coatings, digital printing applications, and decorative products increasingly require advanced pigments offering enhanced color intensity, weather resistance, and compatibility with multiple substrates. Specialty formulations support higher-value applications and improve supplier positioning.

Furthermore, the demand for printing inks has also expanded over the previous half a decade on account of the increasing efforts of countries such as India, Brazil, Thailand, Indonesia, and China to increase literacy amongst citizens and improve their taxation system. Owing to this factor, the dyes and pigments segment has gained momentum in the global market.

However, due to the pandemic situation, there has been a drop in the manufacturing process of paints and coatings in 2023 as a result of the global building industry slowdown. Nevertheless, the situation is expected to improve in 2024, regaining the market's growth.

Construction Chemicals:

The construction chemicals segment is set to witness significant market growth during the forecast period. The segment growth is attributed to rapid urbanization and infrastructure development worldwide, and there is a growing demand for high-performance construction chemicals.

Specialty chemicals cater to this need by providing solutions for various construction challenges, including waterproofing, corrosion protection, and structure reinforcement. The construction industry is increasingly focusing on sustainability and green building practices. Specialty construction chemicals offer eco-friendly solutions that contribute to energy efficiency, reduced environmental impact, and prolonged structure lifespan.

Specialty chemicals in construction continually evolve with advancements in materials science and technology. Companies innovate to develop tailored solutions for specific construction applications, addressing unique project requirements and challenges. The increasing demand for residential, commercial, and industrial space across the region boosts the demand for construction chemicals. Emerging markets, particularly in the Asia Pacific and the Middle East & Africa, are experiencing rapid urbanization and infrastructure development, driving significant growth in the market.

Specialty Polymers:

Performance requirements across advanced manufacturing industries are elevating the importance of specialty polymers. Electronics, healthcare, automotive, and aerospace sectors increasingly require materials capable of delivering thermal stability, lightweight characteristics, and superior mechanical properties. These capabilities support premium pricing and strengthen customer retention.

Application diversity distinguishes this segment from commodity polymer markets. Medical devices, battery systems, electrical insulation, and engineered components frequently depend on customized formulations designed to satisfy demanding operating conditions. Product development often involves extensive collaboration between suppliers and end users.

Textile Chemicals:

Shifting consumer preferences and increasing performance requirements are redefining demand patterns within the textile chemicals segment. Apparel manufacturers, technical textile producers, and home furnishing companies increasingly require specialty formulations capable of improving softness, color retention, moisture management, and durability. Product performance has become a more important purchasing criterion than price alone, particularly in premium and industrial textile applications.

Supply chain transformation is also influencing the segment. Brands are placing greater emphasis on traceability, sustainability, and compliance with evolving environmental standards. These priorities are encouraging adoption of low-emission dyes, finishing agents, and processing auxiliaries designed to reduce water consumption and chemical discharge.

Base Ingredients:

Formulation flexibility and broad industrial applicability underpin demand for specialty base ingredients. Personal care products, food applications, pharmaceuticals, and industrial formulations frequently rely on these materials to deliver consistency, stability, and performance enhancement. Their role within the value chain extends beyond simple raw material supply, making technical quality and regulatory compliance increasingly important competitive factors.

Customer expectations regarding safety and traceability continue to influence purchasing decisions. End users increasingly seek ingredients that satisfy evolving regulatory requirements while supporting sustainability objectives. This trend has encouraged manufacturers to expand portfolios incorporating renewable feedstocks and cleaner production processes.

Surfactants:

Cleaning efficiency and formulation versatility make surfactants one of the most widely utilized categories within the specialty chemicals market. Household products, industrial cleaners, agricultural formulations, and personal care applications all depend on surface-active agents capable of improving dispersion, wetting, and emulsification characteristics. Demand patterns are influenced by both industrial activity and consumer spending behavior.

Personal care and hygiene applications remain particularly important. Rising awareness regarding sanitation and health standards has reinforced demand for formulations used in detergents, shampoos, and skincare products. Premium product categories increasingly require specialized surfactants offering mildness, biodegradability, and enhanced sensory performance.

Functional Ingredients:

Performance enhancement rather than bulk material usage defines the commercial importance of functional ingredients. Food processing, cosmetics, pharmaceuticals, and personal care industries increasingly require additives capable of improving stability, texture, preservation, and efficacy. These characteristics support premium pricing structures and create relatively high customer switching barriers.

Consumer preferences are influencing formulation strategies across multiple sectors. Demand for clean-label products, wellness-oriented solutions, and naturally derived ingredients is encouraging manufacturers to reformulate existing portfolios. Regulatory scrutiny regarding ingredient safety further reinforces the need for technical expertise and extensive testing capabilities.

Water Treatment:

Water scarcity and tightening environmental standards are elevating the strategic significance of water treatment chemicals. Industrial users, municipalities, and utilities increasingly require technologies capable of improving water quality, reducing contamination, and enhancing operational efficiency. These requirements are creating sustained demand across both developed and emerging economies.

Industrial wastewater management has become a major investment priority. Mining, energy, food processing, pharmaceuticals, and manufacturing facilities rely on specialty chemicals to maintain compliance with increasingly stringent discharge regulations. Treatment efficiency and process reliability remain central purchasing considerations.

Specialty Chemicals Market Regional Insights:

Asia-Pacific Specialty Chemicals Market Analysis:

Asia Pacific Specialty Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 49.60% of the global market in 2025, generating USD 375.63 billion in revenue, and is projected to reach USD 402.11 billion in 2026. This can be attributable to the large chemical production base concentrated in China and India. China has emerged as the hub for the production of chemicals owing to the easy availability of raw materials and cheap labor. On a similar note, the Indian market is also highly split, with the majority of companies being small to medium-sized.

However, one of the main constraints is the limited feedstock supply, and a large proportion of smaller-scale players are unable to compete with Chinese companies. This is a key reason behind the smaller share being held by the country as compared to China. The Japan market is projected to reach USD 49.02 billion by 2026, the China market is projected to reach USD 189.05 billion by 2026, and the India market is projected to reach USD 57.33 billion by 2026.

Manufacturing concentration and expanding industrial output position the Asia-Pacific as the largest regional contributor to the specialty chemicals market. Electronics production, agriculture, infrastructure development, and consumer goods industries generate broad-based demand. Regional supply chains and cost competitiveness support production growth. Rising income levels and industrial modernization continue to expand opportunities across diverse application categories.

Japan Specialty Chemicals Market:

Precision manufacturing and stringent quality standards distinguish Japan's role within the specialty chemicals market. Electronics, semiconductor materials, healthcare products, and automotive technologies represent important demand centers. Competitive advantages arise from formulation expertise and strong intellectual property capabilities. Premium applications and continuous innovation support Japan's contribution to the specialty chemicals market share globally.

China Specialty Chemicals Market:

Industrial scale and extensive downstream manufacturing ecosystems elevate China's importance within the specialty chemicals market. Electronics, construction, agriculture, and consumer products collectively drive substantial demand. Government support for advanced manufacturing and domestic innovation is reshaping competitive dynamics. Capacity expansion, localization strategies, and technology upgrades are strengthening specialty chemicals market growth prospects.

North America Specialty Chemicals Market Analysis:

North America contributed approximately USD 169.45 billion to the global market in 2025, accounting for 22.40% share, and is expected to reach USD 174.17 billion in 2026. North America is a major consumer of biocides, cosmetic chemicals, corrosion inhibitors, institutional cleaners, lubricating oil additives, and synthetic lubricants, which account for a sizable portion of the market.

Innovation intensity and strong downstream manufacturing capabilities underpin North America's position within the specialty chemicals market. Demand originates from healthcare, electronics, construction, and agricultural applications requiring high-performance formulations. Regional producers benefit from advanced research infrastructure and feedstock availability. Sustainability targets, reshoring initiatives, and customer preference for specialized solutions support long-term specialty chemicals market growth.

The expanding demand for construction chemicals from the U.S. and Canada, on account of an increase in investments in infrastructure projects, has also enabled North America to secure constructive market growth. As a result, this region is regarded as a promising destination for specialty chemical manufacturers owing to the profitable investment opportunities provided to foreign players. The U.S. market is projected to reach USD 135.77 billion by 2026.

United States Specialty Chemicals Market:

The United States represents a major contributor to the specialty chemicals market size due to its diversified industrial base and strong innovation ecosystem. Pharmaceutical manufacturing, electronics, personal care products, and infrastructure investments support consumption across multiple categories. Competitive advantages stem from research capabilities, shale-based feedstock access, and customer proximity. Portfolio specialization continues to strengthen domestic market positioning.

Europe Specialty Chemicals Market Analysis:

In 2025, the European market stood at USD 137.09 billion, representing 18.10% of global demand, and is projected to grow to USD 140.57 billion in 2026. As per our study, Europe is expected to witness moderate growth in the market. Europe accounted for the third-largest share in the market, strongly backed by the chemical industry in the region.

Regulatory sophistication and emphasis on sustainable chemistry characterize the European specialty chemicals market. Demand from automotive, industrial manufacturing, healthcare, and consumer products sustains the region's importance. Producers increasingly prioritize low-carbon formulations and circular economy solutions to address environmental requirements. Technical expertise and long-standing customer relationships contribute to stable specialty chemicals market growth across Europe.

Western Europe is the world's largest consumer of nutraceuticals, fragrances, and flavors. It is also one of the region's most important exporting divisions of electronic chemicals, which has resulted in the magnification of this market. Furthermore, the extraordinary rise in the use of water treatment chemicals has aided the progress of Europe's chemicals industry, thus spurring the demand for specialty chemicals. The UK market is projected to reach USD 27.38 billion by 2026, and the German market is projected to reach USD 29.72 billion by 2026.

Germany Specialty Chemicals Market:

Advanced manufacturing capabilities and engineering expertise make Germany a strategically important market for specialty chemicals. Automotive production, industrial machinery, and high-value manufacturing applications support demand for performance-oriented formulations. Research intensity and process innovation remain competitive strengths. Environmental regulations and sustainability priorities are accelerating investment in resource-efficient chemistries and advanced material technologies.

United Kingdom Specialty Chemicals Market:

Life sciences, personal care products, and specialty manufacturing activities shape the United Kingdom specialty chemicals market. Customer demand increasingly favors differentiated formulations supported by technical service and regulatory compliance capabilities. Innovation ecosystems and collaboration between industry and academia strengthen product development activities. High-value applications provide resilience despite changing trade and supply chain dynamics.

Latin America Specialty Chemicals Market Analysis:

In Latin America, manufacturers may benefit from the increased production activities in emerging economies such as Brazil. The rapid expansion of construction activities in Latin American countries will also benefit the market. Latin America recorded a market size of USD 43.14 billion in 2025, capturing 5.70% of the global market share, and is projected to reach USD 45.36 billion in 2026.

Agricultural production and infrastructure investment provide the foundation for specialty chemicals demand across Latin America. Crop protection products, construction chemicals, and water treatment applications account for significant consumption. Economic modernization and urban development are expanding opportunities for performance-oriented formulations. Increasing industrial diversification supports steady specialty chemicals market growth throughout the region.

Middle East & Africa Specialty Chemicals Market Analysis

The demand for oilfield chemicals in the Middle Eastern countries is expected to drive market growth. In 2025, the Middle East & Africa generated USD 32.66 billion, contributing 4.30% to global market revenue, and is projected to grow to USD 34.63 billion in 2026. In the GCC region, the specialty chemical sector has enormous potential for multi-fold economic expansion.

Infrastructure expansion and industrial diversification are enhancing the importance of the Middle East & Africa specialty chemicals market. Water treatment, construction chemicals, and agricultural applications remain key demand drivers. Resource management challenges and population growth create additional opportunities. Investments in manufacturing capacity and downstream industries support sustained specialty chemicals market growth.

Giant chemical companies in the GCC are well-positioned to use their knowledge in the production process to establish new and better ways to broaden their downstream existence. For instance, according to the report by the GPCA, construction chemicals accounted for 0.8 MMT in 2023 and are projected to reach 0.9-1.0 MMT by 2025. It also asserted that the packaging industry in GCC countries is poised to increase from USD 1 billion in 2023 to USD 1.5 billion in 2025, owing primarily to the expanding packaging needs in the region.

Specialty Chemicals Industry Competitive Landscape

Leading Companies Focus on Acquisition and Expansion Strategies to Garner Market Share

To capture the smallest of whitespace and promote financial adeptness, organizations are working on infrastructure upgrades and technological advancements in their production plants. The demand for food additives, along with paper and plastic additive applications, has led them to further improve the reliability of their offerings and maintain long-term service contracts with raw material suppliers or end-users. Intensive R&D for feasible, cost-effective product development and the adoption of new technologies are some of the market players' prominent operational strategies. Furthermore, R&D for bio-based chemicals has gained significant traction in recent years as a result of shifting end-user perceptions and favorable regulatory mandates.

Competitive dynamics within the specialty chemicals market are defined by formulation expertise, application-specific knowledge, regulatory capabilities, and customer intimacy rather than production scale alone. Unlike commodity chemical businesses, competitive advantage frequently depends on technical service, intellectual property, qualification cycles, and the ability to deliver measurable performance improvements. Portfolio quality and exposure to high-value end markets increasingly influence profitability and long-term strategic positioning.

Global leaders, including BASF, Evonik Industries, Clariant, Solvay, Croda International, Arkema, LANXESS, Nouryon, Ashland, and Huntsman, maintain significant specialty chemicals market share through diversified product portfolios and extensive research capabilities. Their competitive strength derives from strong customer relationships, broad geographic presence, and the ability to provide customized formulations across multiple industries. Technical collaboration with end users has become an increasingly important differentiator, particularly in healthcare, electronics, and advanced manufacturing applications.

Margin optimization has emerged as a central strategic priority across the industry. Leading companies are actively migrating toward higher-value businesses characterized by stronger pricing power and lower cyclicality. Functional ingredients, electronic chemicals, specialty polymers, and water treatment technologies are attracting greater investment because these categories benefit from long qualification cycles and relatively high switching costs.

Companies have already started taking initiatives and started their own campaigns catering to the need for chemicals in different sectors and fueling the growth of the market. One such example is Novozymes, an industrial enzymes giant, which took an initiative by collaborating with the cleaning start-up Aks2tal and the Danish municipality of Gladsaxe to test the former’s probiotic cleaning product, named Microvia Pro. Microvia Pro is a solution for the post-COVID struggle with the excessive need for deep cleaning. All this new revolution by the key players remarkably boosts the market. From May 3, 2024, it will be available in multiple Gladsaxe offices and canteen areas.

LIST OF KEY COMPANIES PROFILED

- Solvay AG (Belgium)

- Evonik Industries AG (Germany)

- Clariant AG (Switzerland)

- Akzo Nobel N.V. (Netherlands)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- LANXESS AG (Germany)

- Croda International Plc (U.K.)

- Huntsman International LLC (U.S.)

- The Lubrizol Corporation(U.S.)

- Albemarle Corporation (U.S.)

Latest Specialty Chemicals Industry Developments:

- January 2025: Arkema S.A. completed the acquisition of Dow’s flexible packaging laminating adhesives business. The transaction strengthened Arkema’s Adhesive Solutions segment and expanded its portfolio serving packaging applications. Technologies and capabilities involved included solvent-based laminating adhesives, solventless laminating adhesives, and heat-seal coating technologies.

- April 2025: Solvay S.A. inaugurated a new rare earths production line for permanent magnets at its La Rochelle site in France. The project marked the start of commercial production of rare earth materials for permanent magnets and expanded the company’s rare earth processing activities. Technologies and capabilities involved included rare earth separation, purification, and oxide production processes for magnet applications.

- November 2025: Clariant AG completed its CHF 80 million Care Chemicals expansion project at Daya Bay, China. The investment increased manufacturing capabilities and strengthened the company’s position in the Chinese market. Technologies and capabilities involved included alkoxylation technologies and specialty chemical production capabilities serving pharmaceutical, personal care, and industrial applications.

- May 2025: Clariant AG announced the expansion of its Catofin catalyst production facility in Louisville, Kentucky, United States. The action was undertaken to support growing global demand and enhance supply capabilities. Technologies and capabilities involved included Catofin catalyst technology and catalyst manufacturing capabilities.

- December 2024: Arkema S.A. finalized the acquisition of Dow’s flexible packaging laminating adhesives business. The acquisition broadened Arkema’s specialty materials offering and reinforced its position in packaging adhesives. Technologies and capabilities involved included flexible packaging adhesive technologies, heat-seal coatings, and formulation expertise for packaging applications.

REPORT COVERAGE

The global specialty chemicals market research report provides a detailed analysis of the market and focuses on crucial aspects such as production technologies, leading companies, and application segments. Also, it offers insights into specialty chemicals market trends, price trends, and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the market’s growth in recent years. The competitive landscape section covers detailed profiles of leading key players operating in the global market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.90% during 2026-2034 |

|

Unit |

Volume (Million Tons); Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 757.98 billion in 2025 and is projected to reach USD 1,167.22 billion by 2034.

Growing at a CAGR of 4.90%, the market will exhibit significant growth during the forecast period (2026-2034).

The agrochemicals segment is the leading type in the market.

The rising adoption of cleaners and disinfectants, coupled with strong demand from the personal care industry, is likely to drive the market.

Solvay AG, Evonik Industries AG, BASF SE, and Clariant AG are the prominent players in the global market.

Asia Pacific dominated the market share in 2025.

Growing R&D activities and the strategic initiatives by market players are opening up new areas of growth to surge the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us