Returnable Glass Bottle Market Size, Share & Industry Analysis, By Grade (Type I, Type II, and Type III), By Capacity (Below 50 ml, 50 - 200 ml, 201 - 500 ml, 501 - 1000 ml, and Above 1000 ml), By End Use (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Household, and Others), and Regional Forecast, 2026-2034

Returnable Glass Bottle Market Size and Future Outlook

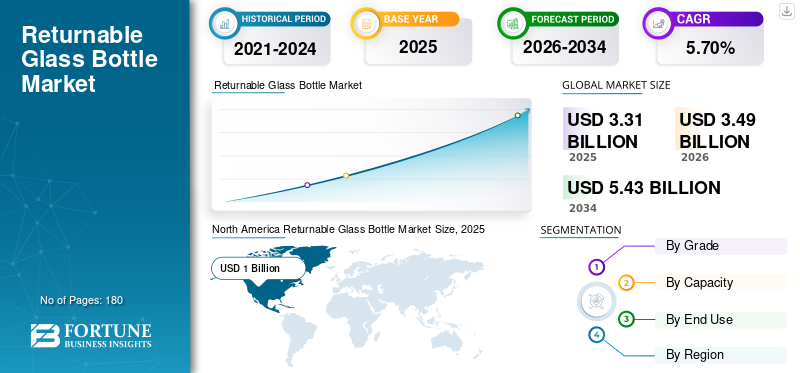

The global returnable glass bottle market size was valued at USD 3.31 billion in 2025. The market is projected to grow from USD 3.49 billion in 2026 to USD 5.43 billion by 2034, exhibiting a CAGR of 5.70% during the forecast period. North America dominated the global returnable glass bottle market with a market share of 30.21% in 2025.

The global returnable glass bottle industry refers to the sector engaged in the design, production, distribution, and management of reusable glass bottles. These bottles are intended to be collected, cleaned, sanitized, and refilled numerous times for ongoing utilization across a range of end-use industries.

Sustainability goals, regulatory push for waste reduction, lower environmental footprint compared to single-use packaging, and cost efficiencies achieved through repeated bottle reuse are key factors propelling the global market growth. The product aligns with circular economy principles by reducing packaging waste, lowering carbon footprint, and minimizing raw packaging material consumption.

Furthermore, the market is dominated by several major players, including Ardagh Group S.A., Vetropack Group, and Vidrala at the forefront. A broad portfolio, innovative product launches, and initiatives aimed at the expansion of geographical presence have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Growing Sustainability Mandates to Drive Market Expansion

The growing global focus on sustainability, the adoption of circular economy practices, and the implementation of stricter regulations regarding single-use plastics are significant factors driving the returnable glass bottle market growth. Governments and regulatory agencies in Europe, North America, and the Asia Pacific regions are promoting refillable packaging solutions that minimize waste and lower carbon emissions. Glass, which can be recycled indefinitely without losing its quality, is increasingly favored by beverage brands aiming to achieve their Environmental, Social, and Governance (ESG) objectives. This transition, along with consumer demand for returnable glass, environmentally friendly and non-toxic packaging, greatly enhances market expansion.

MARKET RESTRAINTS:

High Initial Infrastructure Costs May Hamper the Market Growth

Although the returnable glass bottle system offers several benefits, it necessitates a considerable upfront investment in areas such as washing, sanitization, sorting, reverse logistics, and tracking infrastructure. Small and medium-sized beverage manufacturers frequently face challenges related to the capital expenditure needed to implement large-scale returnable systems. Furthermore, issues such as bottle breakage, inefficiencies in transport, and the upkeep of cleaning facilities contribute to increased operational costs, hindering adoption in regions that are sensitive to costs.

MARKET OPPORTUNITIES:

Premiumization and Brand Differentiation to Create New Opportunities

The increasing popularity of premium craft beer, kombucha, cold-pressed juices, and artisanal spirits presents significant opportunities for returnable glass bottles. Brands are progressively adopting high-quality reusable glass packaging to improve product perception, maintain flavor integrity, and establish brand identity. In markets where consumers link glass with purity, high quality, and luxury, companies are utilizing returnable bottles to enhance customer loyalty and prolong product life cycles. Additionally, the incorporation of technologies such as RFID/NFC-enabled tracking can further optimize operations and unlock data-driven efficiencies.

RETURNABLE GLASS BOTTLE MARKET TRENDS:

Rising Popularity of Refill and Deposit-Return Systems Emerges as a Key Trend

Deposit-return schemes (DRS), refill-on-the-go models, and retailer-led collection initiatives are swiftly gaining popularity across the globe, particularly in Europe and certain regions of the Asia Pacific. Governments and major beverage corporations are advocating for circular packaging systems, motivating consumers to return bottles in exchange for financial rewards. This is generating a significant structural momentum toward returnability frameworks. Furthermore, advancements in digital technology, such as intelligent tracking, automated washing systems, and standardized reusable bottle pools, are transforming the sector, rendering returnable glass more efficient and scalable than it has ever been.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Complex Reverse Logistics Poses as a Major Challenge for Industry Expansion

The effectiveness of returnable bottle systems depends on a well-organized network for return, collection, and redistribution, creating challenges in numerous markets. Overseeing bottle circulation, guaranteeing prompt returns, addressing breakage, and sustaining a uniform bottle pool necessitate strong collaboration among manufacturers, retailers, and consumers. In areas with underdeveloped infrastructure, inefficiencies in reverse logistics greatly hinder scalability, complicating the ability of companies to run returnable systems profitably. Hence, concerns associated with complex reverse logistics pose as a key challenge for the development of the market.

Segmentation Analysis

By Grade

Benefits of Cost-Efficiency and Durability Drove Type III Grade Leadership in 2025

In terms of grade, the market is categorized as type I, type II, and type III.

The type III segment captured the largest returnable glass bottle market share in 2025 with a 45.42% share. The dominance is mainly due to its durability, chemical stability, and cost-effectiveness necessary for mass-market beverage applications. Type III glass is commonly favored in returnable systems due to its outstanding resistance to mechanical stress experienced during repeated washing, filling, transportation, and handling processes. In contrast to higher grades that are more expensive and generally designated for pharmaceuticals or specialty items, Type III offers sufficient strength and functional performance at a considerably lower production cost, rendering it economically viable for high-volume beverage producers.

The type II grade segment is expected to grow at a CAGR of 5.55% over the forecast period.

By Capacity

501 - 1000 ml Segment Led the Market with Optimal Volume for Value and Convenience

In terms of capacity, the market is categorized into below 50 ml, 50 - 200 ml, 201 - 500 ml, 501 - 1000 ml, and above 1000 ml.

The 501 -1000 ml segment captured the largest share of the market in 2025 with a 38.19% share. The segmental dominance is due to its optimal combination of consumer convenience, product value, and operational efficiency for manufacturers. This size range is especially popular for beverages such as beer, dairy products, carbonated soft drinks, juices, and household liquids, as consumers tend to favor mid-sized packaging that offers greater value per fill than smaller bottles, while remaining easy to handle and store.

The 201 - 500 ml capacity segment is expected to grow at a CAGR of 5.77% over the forecast period.

By End Use

Food & Beverages Segment Depicts Leadership with High Demand for Glass Bottles due to Superior Flavor Preservation Attributes

Based on end use, the market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals, household, and others.

To know how our report can help streamline your business, Speak to Analyst

In 2025, the global market was dominated by food and beverages in terms of end use. The segment held a 42.87% share in 2025. The segment leads as products such as beer, carbonated drinks, milk, juices, and functional beverages produce the highest global packaging turnover, rendering returnable systems both cost-effective and scalable. Beverage manufacturers particularly favor glass bottles for their superior flavor preservation, chemical inertness, and capacity to endure numerous washing and refilling cycles, attributes that are crucial for both mass-market and premium beverage brands.

The personal care and cosmetics segment is projected to grow at a CAGR of 6.56% during the study period.

Returnable Glass Bottle Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Returnable Glass Bottle Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific held the dominant share in 2024, valued at USD 0.94 billion, and maintained its leading position in 2025, with a value of USD 1.00 billion. The region is dominating the market due to swift urbanization, increasing disposable incomes, and a surge in the consumption of packaged beverages. Additionally, the rising awareness of environmental issues and initiatives that advocate for sustainable packaging solutions also contribute to this trend. Major beverage corporations are persistently enhancing refill and return programs in emerging markets, thereby reinforcing the growth momentum.

In the region, China and India reached USD 0.32 billion and USD 0.27 billion, respectively, in 2025.

North America and Europe

North America and Europe are anticipated to experience notable growth in the coming years. During the forecast period, the North America region is projected to record a growth rate of 5.90%, which is the second highest among all regions, and reach a valuation of USD 0.85 billion by 2025. In North America, the increasing awareness of environmental issues and the significant commitments made by leading beverage companies to minimize plastic waste are crucial factors driving the adoption of returnable glass bottles. The region's growing premium beverage industry, comprising craft beer, specialty sodas, kombucha, and organic juices, prefers glass for its upscale appearance, resilience, and capacity to maintain flavors. Major retailers and breweries are progressively implementing closed-loop return initiatives to improve their brand sustainability profiles. Together, these elements bolster market demand throughout the U.S. and Canada. In 2025, the U.S. market reached a value of USD 0.67 billion.

After North America, the Europe market secured the position of the third-largest region in the global market and reached USD 0.73 billion in 2025. This is attributed to stringent sustainability regulations, well-established deposit-return schemes (DRS), and a broad consumer acceptance of reusable packaging. European consumers favor glass due to its recyclability, safety, and reduced environmental impact, which contributes to high adoption rates in sectors such as beer, milk, carbonated beverages, and household products. Backed by these factors, Germany, the U.K., and France touched valuation of USD 0.16 billion, USD 0.14 billion, and USD 0.10 billion in 2025.

Latin America and the Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market, in 2025, reached a valuation of USD 0.40 billion. The region stands as a prominent supporter of returnable glass bottle systems, attributed to their economic efficiency and established market tradition. The region's commitment to lowering packaging costs and reducing waste persistently fuels the adoption of returnable glass bottles in both alcoholic and non-alcoholic beverage sectors.

In the Middle East & Africa, South Africa reached a value of USD 0.09 billion by 2025. In the region, the growth of the carbonated beverage, water, and beer sectors, fueled by population increase and urban development, is contributing to the advancement of the returnable glass bottle market. Although still in progress, sustainability efforts and anti-plastic campaigns are motivating brands to embrace refillable packaging options.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Companies’ Wide Range of Product Offerings and Strong Distribution Networks Supported their Leading Position

The global market exhibits a semi-concentrated structure, with numerous small to mid-size companies actively operating worldwide. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Ardagh Group S.A., Vetropack Group, and Vidrala are among the leading players in the market. A comprehensive range of returnable glass bottle products, a global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include Verallia, O-I, Toyo Glass Co., Ltd., and others. These companies are undertaking various strategic initiatives, including investments in R&D and partnerships with pharmaceutical companies, to enhance their market presence.

LIST OF KEY RETURNABLE GLASS BOTTLE COMPANIES PROFILED:

- Ardagh Group S.A. (Luxembourg)

- Vetropack Group (Switzerland)

- Vidrala (Spain)

- Verallia (France)

- O-I (U.S.)

- Toyo Glass Co., Ltd. (Japan)

- Frigoglass (Greece )

- Nihon Yamamura Glass Co., Ltd. (Japan)

- Egger Getränke (Austria)

- AGI Glaspac (India)

- Solenis (U.S.)

- The Coca‑Cola Company (U.S.)

- Ajanta Bottle (India)

- Vical (Guatemala)

- KHS (Germany)

KEY INDUSTRY DEVELOPMENTS:

- August 2025: In Lüneburg, Coca-Cola Europacific Partners Deutschland (CCEP DE) implemented one of the group’s most advanced returnable-glass lines, achieving this during active production with remarkable technical accuracy. This new filling line is efficient but also establishes new benchmarks in automation, sustainability, and quality. The Lüneburg facility is among the 13 production sites managed by CCEP DE, and with the introduction of its new glass line, it serves as a significant driver for beverage filling in the Northern region.

- July 2025: Sidel assisted Grupo GEPP, the exclusive bottler for PepsiCo in Mexico, in the installation of expanded returnable PET and glass bottling lines to address the increasing consumer demand and sustainability objectives. Grupo GEPP manages 44 production facilities focused on the manufacturing and distribution of well-known international brands such as Gatorade, Lipton, Pepsi, and 7Up, and also owns the brands Epura and Garci-Crespo.

- April 2024: O-I and Revino completed the cycle with returnable glass wine bottles, utilizing a regional infrastructure that aligns with a shared goal of global sustainability. O-I Glass will manufacture over 2.4 million returnable, reusable glass wine bottles locally as a component of this comprehensive refillable glass bottles reuse system. Each of these bottles is capable of being reused a minimum of 25 times on average prior to being retired and recycled into new glass packaging.

- February 2024: In collaboration with Brau Union Österreich, Vetropack Group, a prominent manufacturer of glass packaging in Europe, introduced a new 0.33-litre returnable bottle to be launched in February 2024 as a standard solution for the brewing sector. This bottle is one-third times lighter than its traditional reusable equivalent owing to the innovative Echovai production process created by Vetropack. Consequently, it is expected to aid in meeting the new Austrian requirements for returnable packaging.

- June 2022: Otsuka Pharmaceutical Co., Ltd. (Otsuka) launched POCARI SWEAT in 250ml returnable bottles. These new returnable bottles will be made available at Aeon and Aeon Style outlets that are part of the circular shopping platform Loop. One of the initiatives includes the creation of a robust glass bottle designed for reuse, which also emphasizes the intrinsic quality of POCARI SWEAT.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.70% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Grade

By Capacity

By End Use

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.31 billion in 2025 and is projected to reach USD 5.43 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.00 billion.

The market is expected to exhibit a CAGR of 5.70% during the forecast period of 2026-2034.

The 501 - 1000 ml segment led the market by capacity in 2025.

The key factors driving the market growth are the increasing sustainability mandates.

Ardagh Group S.A., Vetropack Group, Vidrala, Verallia, O-I, and Toyo Glass Co., Ltd. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

The rising sustainability and anti-plastic regulations are the factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us