Rigid Foam Market Size, Share & Industry Analysis, By Type (Polyurethane, Polystyrene, Polyethylene, Polyvinyl-Chloride and Others), By Application (Building & Construction, Packaging, Automotive, Appliances and Others), and Regional Forecast, 2026-2034

Rigid Foam Market Size & Share

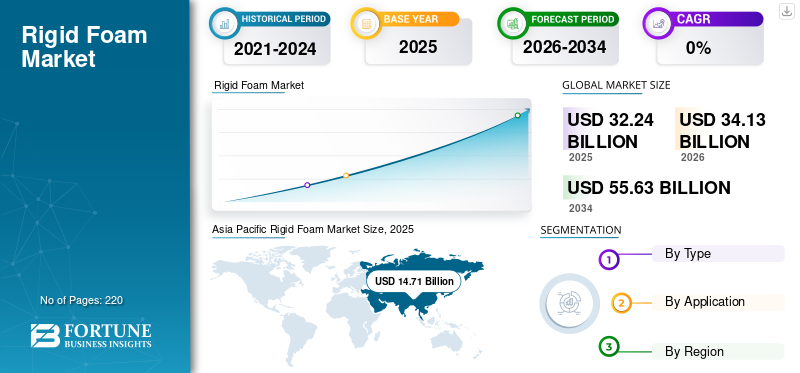

The global rigid foam market size was valued at USD 32.24 billion in 2025. The market is projected to grow from USD 34.13 billion in 2026 to USD 55.63 billion by 2034 at a CAGR of 6.3% during the 2026-2034 forecast period. Asia Pacific dominated the global rigid foam market with a market share of 45.78% in 2025.

The market refers to the sector involving the production and use of solid polyurethane, polyisocyanurate (polyiso), polystyrene, and other polymer-based foam materials that exhibit high strength, low density, and excellent insulation properties. Different factors driving the market include rising demand for energy-efficient and sustainable building materials owing to stringent building energy codes and sustainability mandates. Growing construction activities, urbanization, and expanding industrial sectors also increase demand for advanced insulation solutions that enhance thermal performance, reduce heat loss, and provide moisture barriers. Various innovations such as bio-based raw materials and net-zero emission chemical inputs contribute to market growth by aligning with environmental regulations and consumers’ preference for lower-carbon footprint products. Owens Corning, Kingspan Group, BASF SE, and Covestro are few prominent key players operating in the market.

Download Free sample to learn more about this report.

Rigid Foam Market Key Takeaways

- 2025 Market Size: USD 32.24 billion

- 2026 Market Size: USD 34.13 billion

- 2034 Forecast Market Size: USD 55.63 billion

- CAGR: 6.3% (2026–2034)

- Asia Pacific dominated the market with a 45.78% share in 2025.

- The polyurethane segment held the largest market share in 2025.

- The building & construction segment accounted for the dominant market share in 2025.

Asia Pacific

Asia Pacific accounted for USD 14.71 billion in 2025

North America

North America is expected to witness steady growth during the forecast period.

Europe

Europe is projected to witness steady growth, supported by stringent energy efficiency regulations and green building certifications.

U.S.

U.S. market is expected to remain the largest country-level market, driven by strict building codes and sustainability initiatives.

Japan

Japan market is projected to witness steady growth during the forecast period.

Read More

RIGID FOAM MARKET TRENDS

Expansion in Zero Energy Buildings & Green Construction is an Emerging Market Trend

The expansion of zero-energy buildings and green construction is a significant trend driving demand for high-performance insulation materials such as polyisocyanurate (PIR), phenolic, and other high-R-value market products. Green building certification systems including LEED, BREEAM, and WELL, alongside national net-zero carbon strategies, set stringent necessities for energy efficiency and reduced environmental impact. These initiatives emphasize superior thermal insulation to minimize heating and cooling loads, leading to lower operational carbon emissions and energy costs. The high R-value (thermal resistance) properties of PIR and phenolic foams make them ideal for walls, roofs, industrial facilities, and retrofit projects, where maintaining thermal comfort with minimal energy use is paramount.

MARKET DYNAMICS

MARKET DRIVERS

Rising Construction in Emerging Economies Drives Market Growth

Rising construction activity in emerging economies such as China, India, ASEAN countries, and the Gulf Cooperation Council (GCC) nations is a key driver for the rigid foam market growth. These regions are witnessing rapid urbanization, industrial growth, and infrastructure development, which creates substantial demand for effective insulation in residential housing, commercial buildings, industrial facilities, and public infrastructure projects.

The growing focus on energy efficiency and thermal comfort in these construction sectors makes insulation a critical component. The product insulation materials such as Expanded Polystyrene (EPS), Extruded Polystyrene (XPS), and polyurethane boards are widely preferred for roofing, wall insulation, exterior insulation finish systems (EIFS), and floor systems due to their high thermal resistance, moisture durability, and structural support.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Volatility in Raw Materials Significantly Restraining Market Expansion

Volatility in raw material prices, particularly for key inputs such as methylene diphenyl diisocyanate (MDI), toluene diisocyanate (TDI), polyols, and styrene, poses a significant restraining factor for the market. The resulting cost uncertainties can slow market growth as insulation producers face challenges in passing on increased expenses to end-users, who may be price-sensitive, particularly in construction and industrial sectors. This unpredictability undermines investment in capacity expansions and innovation within the market. Despite efforts including backward integration, inventory buffers, and trials of bio-based or recycled feedstocks, the raw material price volatility remains a persistent challenge that restricts consistent profitability and competitiveness across the industry.

MARKET OPPORTUNITIES

Growing Demand for Hygiene Products Creates an Opportunity For Market

Circular-economy innovations in rigid polyurethane and polystyrene foams are rapidly advancing through chemical recycling technologies developed by leading chemical companies such as BASF, Covestro, and Dow, along with specialized recyclers. These chemical recycling processes break down used PU rigid foams and EPS/XPS waste back into their molecular building blocks, such as polyols, isocyanates, and styrene monomers that can be purified and reused to manufacture new foam products of comparable quality. Such closed-loop recycling systems significantly reduce plastic waste and reliance on fossil-based raw materials, thereby lowering the carbon footprint of insulation materials and aligning with circular economy principles.

Covestro’s Circular Foam project and BASF’s solvent-based recycling initiatives exemplify industry efforts to enable large-scale recovery and reintegration of foam waste into production cycles, with the potential to divert millions of tons from incineration and landfill.

MARKET CHALLENGES

Supply-chain Disruptions in Raw Materials is Challenging Market Growth

Supply-chain disruptions in key raw materials such as methylene diphenyl diisocyanate (MDI), polyols, styrene, and flame-retardant alternatives (e.g., replacements for hexabromocyclododecane - HBCD) presents significant challenges for insulation production. Shortages and supply constraints in these essential feedstocks can delay manufacturing schedules and restrict the volume of insulation products available to original equipment manufacturers (OEMs) and construction companies. These disruptions are often caused by a combination of factors, including geopolitical tensions, logistic bottlenecks, raw material production outages, and increased regulatory scrutiny on hazardous chemicals. The unpredictability in availability complicates procurement planning and can lead to significant delivery delays, hampering project timelines in residential, commercial and industrial sectors.

Regulatory Compliance May Hurdle Market

Regulatory compliance presents a significant hurdle to the market due to increasingly stringent environmental, health, and safety standards governing the production, use, and disposal of foam insulation materials. Regulations aimed at reducing greenhouse gas emissions, limiting the use of high-global-warming-potential blowing agents, and restricting hazardous flame retardants necessitate costly reformulations and technology upgrades. These compliance requirements increase manufacturing complexity and costs, potentially slowing product development and market entry. Additionally, some forms of product insulation face restrictions or market rejection in key regions due to concerns over fire safety, chemical emissions, and end-of-life disposal challenges, limiting its widespread adoption.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade Protectionism and Geopolitical Issues Leads to Disruption in Global Supply Chains and Increasing Production Costs

Trade protectionism and geopolitical tensions significantly impact the market by disrupting global supply chains and increasing production costs. Governments have implemented tariffs, import restrictions, and local content requirements, which affect the international flow of critical raw materials such as polyols, isocyanates, and specialty additives essential for foam production.

Furthermore, geopolitical conflicts and trade disputes can cause market fragmentation, slowing innovation and investment due to heightened uncertainty. For example, U.S. tariffs on petrochemicals have increased prices and limited access to affordable raw materials, squeezing profit margins and delaying capacity expansions.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Research and development (R&D) trends in the market are increasingly focused on enhancing energy efficiency, sustainability, and performance. Key R&D efforts include developing High-R-value insulation boards that provide superior thermal resistance without increasing thickness, which is crucial in space-constrained applications such as retrofits and high-performance buildings. There is growing emphasis on incorporating recyclable, bio-based, and low-global-warming-potential (GWP) materials to reduce environmental impact, alongside innovations such as vacuum-insulated panels and aerogel-infused foams that push thermal performance boundaries. Manufacturers are also prioritizing health and indoor air quality by reducing volatile organic compounds (VOCs) and avoiding harmful chemicals in foam formulations.

SEGMENTATION ANALYSIS

By Type

Polyurethane Segment Leads Due to Its Thermal Insulation Properties

Based on type, the market is segmented into polyurethane, polystyrene, polyethylene, polyvinyl chloride, and others.

The polyurethane segment held the largest rigid foam market share in 2025. The growth is driven by its excellent thermal insulation properties, structural rigidity, and versatility across industries including construction, refrigeration, and automotive.

The polystyrene segment held a notable share of the market. This growth is owing to its use in packaging and insulation due to its lightweight and cost-effectiveness.

However, the polyethylene and PVC foams serve in specialized applications requiring chemical resistance and durability. The other category includes emerging and niche foam types presenting innovation opportunities in thermal and structural performance.

By Application

Building & Construction Segment Dominated Due To Its Energy-Efficient Insulation Capability

Based on application, the market is segmented into building & construction, packaging, automotive, appliances, and other.

Among these, the Building & Construction segment registers a dominating share in 2025. The growth is driven by rising demand for energy-efficient insulation materials in residential, commercial, and industrial buildings. Products including insulation boards, roofing components, and structural panels are extensively used to enhance thermal performance and meet stricter building codes globally.

The packaging segment accounts for significant market growth. The leveraging of rigid foams for protective cushioning and thermal control in shipping sensitive goods, especially in cold-chain logistics, drives segment growth.

The automotive application is growing notably as market products contribute to light weighting vehicles for improved fuel efficiency and emission reduction.

Similarly, appliance manufacturers use product insulation in refrigerators, freezers, and HVAC systems to boost energy efficiency.

Other applications include marine, electronics, and industrial insulation, where customized foam materials deliver specialized performance such as moisture resistance and high compressive strength.

To know how our report can help streamline your business, Speak to Analyst

RIGID FOAM MARKET REGIONAL OUTLOOK

Based on geography, the market is divided into Asia Pacific, North America, Europe, Middle East & Africa, and Latin America.

Asia Pacific Rigid Foam Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific accounted for the leading market share in 2025. The region’s growth is due to rapid urbanization, infrastructure expansion, and increasing demand for energy-efficient building materials in countries such as China, India, and Southeast Asia. The region exhibits strong growth rates driven by investments in residential, commercial, and industrial construction, as well as expanding cold-chain logistics applications.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is registering significant growth, supported by construction modernization and a strong automotive industry emphasizing lightweight materials for improved fuel efficiency. The U.S. is the largest market, where strict building codes and sustainability goals drive demand for market products. There is ongoing investment in high-density and composite foam production lines to meet the growing needs in cold-chain logistics and residential/commercial applications.

Europe

Europe registers positive growth driven by stringent energy efficiency regulations, green building certifications, and a mature appliance manufacturing industry. Countries including Germany, Italy, and the U.K. are major contributors, with steady growth rates fueled by regulatory compliance and replacement demand in both new constructions and retrofits.

Middle East & Africa

The Middle East & Africa market is growing steadily, propelled by large infrastructure projects, commercial buildings, and energy sector applications across GCC countries, South Africa, and Egypt. Investments in modernization and urbanization strengthen demand, while the region is gradually adopting sustainability-oriented foam products.

Latin America

Latin America's market is smaller but developing due to rising investments in industrial facilities, housing, and public infrastructure. Countries including Brazil and Mexico are primary contributors, where increasing awareness of energy efficiency and insulation benefits fosters demand.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Growing Investments by Companies in Innovations Drives Market Competitiveness

Owens Corning, Kingspan Group, BASF SE, and Covestro are the key players in the market. Major investments by companies in developing products that address evolving demands for sustainability and performance.

LIST OF KEY RIGID FOAM COMPANIES PROFILED:

- Owens Corning (U.S.)

- Kingspan Group (Ireland)

- BASF SE (Germany)

- Covestro (Germany)

- DuPont de Nemours (U.S.)

- Huntsman Corporation (U.S.)

- Carlisle Construction Materials (U.S.)

- Saint-Gobain (France)

- Armacell (Luxembourg)

- Recticel (Belgium)

KEY INDUSTRY DEVELOPMENTS:

August 2024: Carlisle Construction Materials announced the launch of a new polyisocyanurate (polyiso) rigid foam insulation board called Polyiso Eco, containing approximately 5% bio-circular content. This product, developed in collaboration with Covestro and Stepan Company, uses renewable raw materials certified under the International Sustainability and Carbon Certification (ISCC) to reduce the carbon footprint compared to traditional fossil-based polyiso insulation.

March 2024: Covestro AG announced the expansion of its Baytherm product line for thermal insulation solutions. The new products are designed to meet the growing demand for energy-efficient materials in the construction and refrigeration sectors. These advanced rigid foams offer superior thermal insulation and are tailored for use in both residential and industrial applications, helping reduce energy consumption globally.

January 2024: BASF and Carlisle Construction Materials announced a partnership to explore the use of "Lupranate ZERO," which is claimed to be the world's first net-zero-emissions isocyanate, in the production of polyisocyanurate (PIR/polyiso) rigid foam insulation boards branded as InsulBase and VersiCore. Lupranate ZERO is a zero carbon footprint methylene diphenyl diisocyanate (MDI) used to manufacture these insulation boards, targeting the reduction of the carbon footprint in rigid foam production.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kilo Ton) |

|

Growth Rate |

CAGR of 6.3% from 2026 to 2034 |

|

Segmentation |

By Type, By Application, By Region |

|

By Type |

· Polyurethane · Polystyrene · Polyethylene · Polyvinyl-Chloride · Others |

|

By Application |

· Building & Construction · Packaging · Automotive · Appliances · Others |

|

By Region |

· North America (By Type, By Application and By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Type, By Application and By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Type, By Application and By Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Type, By Application and By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Type, By Application and By Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 32.24 billion in 2025 and is projected to reach USD 55.63 billion by 2034.

Recording a CAGR of 6.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building & construction application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Expansion in zero-energy buildings & green construction drives market growth

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us