Robotic Palletizers and De-Palletizers Market Size, Share & Industry Analysis, By Type (Palletizing and De-palletizing), By Payload Capacity (Low Payload (<50 kg), Medium Payload (50–200 kg), and High Payload (>200 kg)), By Robot Type (Articulated Robots, Cartesian Robots, and Collaborative Robots (Cobots)), By End-Use Industry (Food & Beverage, Pharmaceuticals, Consumer Goods (FMCG), Chemicals, E-commerce & Logistics, Automotive, and Others (Paper, Construction Materials, etc.)), and Regional Forecast, 2026 – 2034

Robotic Palletizers and De-Palletizers Market Size and Future Outlook

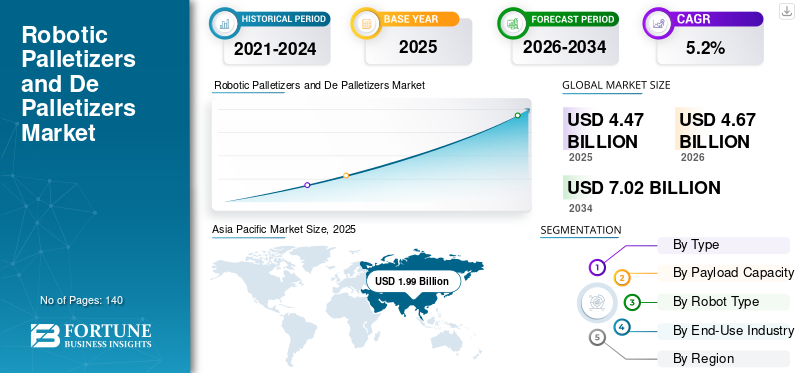

The global robotic palletizers and de-palletizers market size was valued at USD 4.47 billion in 2025. The market is projected to grow from USD 4.67 billion in 2026 to USD 7.02 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period. Asia Pacific dominated the robotic palletizers and de palletizers market with a market share of 44.51% in 2025.

Robotic palletizers and de-palletizers solutions help organizations automate end-of-line material handling processes, enabling efficient stacking, sorting, and movement of goods across manufacturing and logistics operations. These automated systems combine advanced industrial robots, end-of-arm tooling, vision systems, and intelligent control software to improve throughput, reduce manual labor dependency, and enhance operational accuracy in palletizing and de-palletizing applications. The industry is witnessing strong growth, as companies accelerate automation initiatives, driven by labor shortages, rising operational costs, and increasing demand for automation. The need to handle high volumes in packaging and warehouse operations is further supporting adoption. Growing implementation of robotic automation in food & beverage, consumer goods, e-commerce, and logistics sectors is further driving demand across North America, Europe, and Asia Pacific. This trend is particularly evident in fulfillment centers, where organizations are focused on improving productivity, workplace safety, and supply chain efficiency, contributing to the overall market growth.

- For instance, in January 2026, FANUC Corporation expanded its robotic palletizing portfolio with enhanced high-payload palletizing robots and integrated vision-guided systems designed to support mixed-case palletizing and high-throughput warehouse automation in global logistics and manufacturing environments.

ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, and Daifuku Co., Ltd. are among the key players holding a significant share of the market. Their competitive positioning is supported by advanced robotic platforms, integrated automation solutions, strong global distribution networks, and the ability to deliver scalable palletizing and de-palletizing systems tailored for diverse industrial applications, including food processing, logistics, and heavy industries.

Download Free sample to learn more about this report.

ROBOTIC PALLETIZERS and DE-PALLETIZERS MARKET TRENDS

Growing Adoption of Warehouse Automation and E-Commerce Fulfillment Operations to Boost Product Demand

Demand for robotic palletizers and de-palletizers is increasingly influenced by the rapid expansion of warehouse automation and e-commerce fulfillment operations across global supply chains. Companies are prioritizing the automation of end-of-line material handling processes to improve throughput, reduce manual labor dependency, and enhance accuracy in palletizing and de-palletizing applications. These evolving priorities are driving the adoption of advanced robotic systems integrated with vision technologies, intelligent software, and flexible grippers capable of handling mixed-SKU and high-variability packaging environments. Organizations are also expanding automation investments beyond traditional manufacturing toward distribution centers and omnichannel fulfillment networks, where speed, scalability, and operational efficiency are critical. These developments are influencing market dynamics as companies adopt data-driven automation frameworks, real-time monitoring systems, and modular robotic solutions to improve supply chain responsiveness. Solution providers are responding by introducing flexible and scalable palletizing systems that support seamless integration with warehouse management and manufacturing execution systems, enabling improved operational visibility and productivity across complex logistics environments.

- For instance, in March 2025, ABB announced the expansion of its robotic solutions portfolio for logistics and e-commerce applications, highlighting advanced palletizing and material handling capabilities designed to improve warehouse automation efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Higher Operational Efficiency to Drive Market Growth

The robotic palletizers and de-palletizers market is experiencing accelerated growth as industries increasingly adopt automation to address labor shortages, rising wage pressures, and the need for higher operational efficiency. Companies across the manufacturing, food & beverage, and logistics sectors are prioritizing the automation of end-of-line material handling processes to improve throughput, reduce manual intervention, and enhance workplace safety. The expansion of e-commerce and omnichannel distribution is further driving demand for high-speed and flexible palletizing solutions capable of handling diverse product formats and mixed-SKU environments. As operational complexity increases, organizations are investing in advanced robotic systems integrated with vision technologies, intelligent software, and modular automation platforms to improve accuracy and scalability. Solution providers are responding by expanding their portfolios with flexible and high-performance palletizing systems that support seamless integration with warehouse management and production systems, enabling enterprises to optimize supply chain efficiency and maintain consistent operational performance across global facilities.

- For instance, in 2025, FANUC Corporation continued to expand its palletizing robot portfolio, including high-payload models such as the M-410 series, designed to support high-throughput industrial palletizing applications across manufacturing and logistics environments.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity to Constrain Market Expansion

Unlike conventional material handling systems, robotic palletizers and de-palletizers require significant upfront investment in robotic hardware, end-of-arm tooling, software integration, and system configuration. The deployment of these systems often involves complex integration with existing production lines, warehouse management systems, and enterprise resource planning platforms, which can increase implementation timelines and costs. Small and medium-sized enterprises, in particular, may face challenges in adopting robotic automation due to budget constraints and limited technical expertise. Variability in product types, packaging formats, and operational requirements further complicates system design and customization, requiring tailored solutions rather than standardized deployments. Additionally, the need for skilled personnel to operate, program, and maintain robotic systems can create operational challenges in regions with limited technical workforce availability. These factors can slow adoption rates, particularly in emerging markets, and may limit the rapid deployment of robotic palletizing solutions across diverse industrial environments.

MARKET OPPORTUNITIES

Rising Demand for Compact and Modular Palletizing Systems among SMEs Creating New Growth Avenues

An emerging opportunity in the robotic palletizers and de-palletizers market is the increasing adoption of compact and modular automation solutions among small and medium-sized enterprises (SMEs). Traditionally, robotic palletizing systems were deployed primarily by large-scale manufacturers due to high capital requirements and complex integration processes. However, advancements in collaborative robots, plug-and-play systems, and pre-engineered palletizing cells are enabling SMEs to adopt automation with lower investment and faster deployment timelines. Manufacturers are developing scalable palletizing solutions with reduced footprint, simplified programming, and flexible configurations to address the needs of smaller production facilities and decentralized operations. These systems allow organizations to gradually expand automation capabilities without major infrastructure changes. As SMEs continue to modernize operations and address labor shortages, demand for cost-effective and easy-to-deploy robotic palletizing solutions is expected to increase across emerging and developed markets.

- For instance, in 2025, Universal Robots continued expanding its application-focused palletizing solutions designed for SMEs, enabling faster deployment and flexible automation in small-scale production environments.

MARKET CHALLENGES

Limited Standardization in End-of-Arm Tooling and Gripping Technologies to Hinder Market Growth

A critical challenge in the robotic palletizers and de-palletizers market growth is the lack of standardization in end-of-arm tooling and gripping technologies required to handle diverse product types. Different industries require specialized grippers such as vacuum-based systems, clamp grippers, fork-type tools, and hybrid solutions to manage varying packaging formats, including boxes, bags, bottles, and irregular items. This diversity increases system design complexity and often requires customized engineering for each application. The absence of standardized gripping solutions can lead to longer deployment cycles, increased integration costs, and higher maintenance requirements. Additionally, selecting the appropriate end-of-arm tooling becomes critical to ensure stability, speed, and accuracy in palletizing operations, particularly in high-throughput environments. These challenges can limit scalability and create operational inefficiencies, especially for companies managing multiple product lines with varying packaging characteristics.

Segmentation Analysis

By Type

Palletizing Segment Led the Market due to Streamlined End-of-Line Processes

By type, the market is segmented into palletizing and de-palletizing.

Palletizing held the largest robotic palletizers and de-palletizers market share as it represents the primary and most widely adopted application across manufacturing, packaging, and logistics operations. Organizations prioritize palletizing automation to streamline end-of-line processes, improve stacking accuracy, and enhance throughput in high-volume production environments. The demand is particularly strong in industries such as food & beverage, consumer goods, and chemicals, where consistent and high-speed pallet formation is critical for downstream distribution and supply chain efficiency. As companies continue to scale production and optimize packaging operations, there is increasing investment in robotic palletizing systems integrated with advanced grippers, vision technologies, and programmable software to handle diverse product formats and packaging configurations. These systems enable improved operational efficiency, reduced labor dependency, and enhanced workplace safety, making palletizing the foundational use case for robotic automation in material handling.

- For instance, in 2025, KUKA AG continued to promote its KR QUANTEC series for high-payload palletizing applications, supporting automated end-of-line operations across global manufacturing and logistics facilities.

De-palletizing is emerging as the fastest-growing segment and is projected to expand at a CAGR of 5.9%. The growth of this segment is driven by increasing automation in inbound logistics, warehouse operations, and distribution centers, where efficient unloading and sorting of goods are becoming critical for maintaining supply chain speed and accuracy. As e-commerce and omnichannel distribution models expand, organizations are adopting robotic de-palletizing systems equipped with vision-guided technologies and intelligent software to handle mixed loads and variable packaging formats.

To know how our report can help streamline your business, Speak to Analyst

By Payload Capacity

Medium Payload Segment Led due to Its Widespread Applicability Across Diverse Industries

By payload capacity, the market is segmented into low payload (<50 kg), medium payload (50–200 kg), and high payload (>200 kg).

Medium payload (50–200 kg) held the largest share of the robotic palletizers and de-palletizers market, driven by its widespread applicability across diverse industries such as food & beverage, consumer goods, pharmaceuticals, and general manufacturing. These systems offer an optimal balance between payload capacity, speed, and flexibility, making them suitable for handling cartons, cases, and packaged goods in high-throughput production and packaging environments.

- For instance, in 2025, Yaskawa Electric Corporation continued deployment of its MOTOMAN palletizing robots in the medium payload range, widely used for case handling and packaging line automation across the food and consumer goods industries.

Low Payload (<50 kg) is expected to register the highest growth rate in the market, expanding at a CAGR of 6.2%. The growth of this segment is driven by increasing adoption of collaborative robots and lightweight automation solutions in e-commerce, retail distribution, and small-scale manufacturing environments. These systems are designed to handle lighter loads, enabling flexible palletizing and de-palletizing operations in space-constrained facilities and dynamic production settings.

By Robot Type

Articulated Robots Segment Led due to their High Flexibility

By robot type, the market is segmented into Articulated Robots, Cartesian Robots, and Collaborative Robots (Cobots).

Articulated Robots held the largest robotic palletizers and de-palletizers market share, driven by their high flexibility, wide range of motion, and ability to handle complex palletizing patterns in high-throughput industrial environments. These robots are extensively deployed across industries such as food & beverage, chemicals, consumer goods, and logistics, where speed, precision, and payload versatility are critical.

Collaborative Robots (Cobots) are expected to register the highest growth rate in the market, expanding at a CAGR of 7.3%. The growth of this segment is driven by increasing demand for flexible, space-efficient, and easy-to-deploy automation solutions, particularly among small and medium-sized enterprises and logistics operators. Cobots are designed to work safely alongside human operators, reducing the need for complex safety infrastructure while enabling faster implementation in dynamic work environments.

By End-Use Industry

Food & Beverage Segment Lead the Market due to Rising Need for Hygienic Material Handling

Based on end-use industry, the market is segmented into food & beverage, pharmaceuticals, Consumer Goods (FMCG), chemicals, e-commerce & logistics, automotive, and others (paper, construction materials, etc.).

Food & Beverage accounts for the highest share of the robotic palletizers and de-palletizers market, driven by the need for high-speed, continuous, and hygienic material handling across production and packaging operations. The industry operates high-volume manufacturing environments with standardized packaging formats such as cartons, bottles, and cases, making it highly suitable for palletizing automation.

E-commerce & logistics is expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 7.0%, supported by the rapid expansion of online retail, warehouse automation, and omnichannel distribution networks. Logistics operators are increasingly adopting robotic de-palletizing and palletizing systems to manage high order volumes, mixed-SKU handling, and fast-paced fulfillment requirements.

Robotic Palletizers and De-Palletizers Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market accounted for over USD 1.10 billion in revenue in 2025, supported by high adoption of industrial automation, advanced logistics infrastructure, and strong demand for end-of-line material handling solutions across the U.S., Canada, and Mexico. Regional demand is closely linked to labor shortages, rising labor costs, and the increasing need for operational efficiency in manufacturing and warehouse environments. Companies across food & beverage, consumer goods, e-commerce, and logistics sectors are increasingly investing in robotic palletizing and de-palletizing systems to improve throughput, reduce manual handling, and enhance workplace safety. The region also exhibits strong adoption of advanced technologies such as vision-guided robotics, AI-enabled automation, and collaborative robots to support flexible and high-speed operations.

U.S. Robotic Palletizers and De-Palletizers Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 0.90 billion in 2026, driven by the country’s large industrial base, advanced automation adoption, and strong presence of leading robotics manufacturers and system integrators. Unlike many regions, U.S. organizations are rapidly integrating robotic palletizing systems into both manufacturing lines and warehouse operations to address labor shortages and improve operational scalability. Industries such as food processing, e-commerce, and consumer goods are leading adopters, deploying robotic systems to manage high product volumes, mixed-SKU handling, and fast-paced distribution requirements. The growing use of collaborative robots and flexible automation solutions is further enabling companies to implement palletizing systems with lower complexity and faster deployment timelines.

Europe

The European market is supported by a highly developed industrial base, advanced automation adoption, and a strong focus on operational efficiency across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for robotic palletizers and de-palletizers is closely tied to the region’s mature manufacturing sector, well-established packaging industry, and increasing investments in smart factories and Industry 4.0 initiatives. Companies across the food & beverage, pharmaceuticals, automotive, and consumer goods industries are increasingly adopting robotic palletizing solutions to improve production efficiency, ensure consistent product handling, and reduce dependency on manual labor. Unlike emerging regions, the region benefits from a high level of automation maturity, enabling widespread integration of robotic systems with digital production environments, warehouse management systems, and advanced control technologies.

U.K. Robotic Palletizers and De-Palletizers Market

The U.K. market is estimated at around USD 0.12 billion by 2026, representing roughly 2.6% of global sales.

Germany Robotic Palletizers and De-Palletizers Market

Germany’s market is projected to reach approximately USD 0.22 billion in 2026, equivalent to around 4.8% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing region and holds the highest market share, generating revenue of USD 1.99 billion in 2025 globally. The region is also driven by rapid industrialization, expanding manufacturing capacity, and increasing adoption of automation across key economies such as China, Japan, India, and South Korea. The region’s growth is also supported by large-scale production in industries such as food & beverage, consumer goods, chemicals, and electronics, where high-volume material handling and packaging operations require efficient palletizing solutions.

China Robotic Palletizers and De-Palletizers Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with 2026 revenues estimated at around USD 1.02 billion, representing roughly 21.7% of global sales.

Japan Robotic Palletizers and De-Palletizers Market

The Japanese market in 2026 is estimated at around USD 0.24 billion, accounting for roughly 5.1% of the global sales.

India Robotic Palletizers and De-Palletizers Market

The Indian market in 2026 is estimated at around USD 0.20 billion, accounting for roughly 4.4% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in logistics infrastructure, warehouse automation, and expanding manufacturing activity, particularly across the GCC and select North African economies. Government-backed initiatives in industrial diversification, food security, and supply chain modernization are supporting demand for robotic palletizers and de-palletizers used in end-of-line material handling and packaging operations. The GCC benefits from high-capex, large-scale logistics and distribution projects requiring advanced automated pallet handling systems, while North Africa is witnessing a gradual expansion of manufacturing and packaging industries aligned with European trade networks. Across parts of Sub-Saharan Africa, limited but growing industrial capability is encouraging incremental adoption of semi-automated and robotic palletizing solutions in food processing, consumer goods, and basic manufacturing operations.

GCC Robotic Palletizers and De-Palletizers Market

The GCC market is projected to reach around USD 0.09 billion by 2026, representing roughly 2.0% of the global sales.

South America

The South American market is supported by the region’s developing manufacturing and food processing footprint, particularly in Brazil and Argentina, which serve as key hubs for consumer goods production, packaging operations, and export-oriented industries. Brazil’s large-scale food & beverage and agricultural processing sectors represent the primary driver of demand for robotic palletizers and de-palletizers, supported by high-volume packaging and distribution requirements. While overall automation adoption remains lower compared to North America and Europe, growing industrial activity and supply chain modernization are encouraging investment in automated pallet handling systems. Argentina and select regional facilities are gradually modernizing production infrastructure to improve operational efficiency, reduce manual dependency, and align with international manufacturing and logistics standards.

Brazil Robotic Palletizers and De-Palletizers Market

The Brazilian market is projected to reach around USD 0.16 billion by 2026, representing roughly 3.3% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Participants Focus on Advanced Robotics Platforms to Support End-to-end Automation Across Production Lines

The robotic palletizers and de-palletizers market is moderately consolidated, with competitive positioning primarily driven by technological capabilities, system integration expertise, and long-term relationships with industrial customers. Leading players such as ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, and Daifuku Co., Ltd. maintain strong market positions by delivering high-performance robotic systems, integrated automation solutions, and scalable palletizing technologies tailored to complex manufacturing and logistics environments. Their competitive strength is reinforced by advanced robotics platforms, global service networks, and the ability to support end-to-end automation across production lines and distribution centers.

Competitive differentiation is increasingly driven by a company’s ability to integrate robotics with vision systems, AI-enabled control software, and flexible end-of-arm tooling rather than by product range alone. As organizations prioritize efficiency, flexibility, and rapid deployment, market leaders are strengthening investments in intelligent automation, modular system design, and collaborative robotics to address evolving industry requirements. Additionally, the ability to deliver customized solutions for mixed-SKU handling, high-speed operations, and space-constrained environments is becoming a key factor in maintaining competitive advantage and expanding global customer relationships.

- For instance, in Jan 2025, KUKA AG highlighted advancements in its palletizing automation solutions through its KR QUANTEC and KR FORTEC robot platforms, supporting high-payload palletizing and logistics automation applications across industrial environments.

LIST OF KEY ROBOTIC PALLETIZERS and DE-PALLETIZERS COMPANIES

- Mitsubishi Electric Corporation (Japan)

- ABB Ltd. (Switzerland)

- Omron Corporation (Japan)

- FANUC Corporation (Japan)

- Daifuku Co., Ltd. (Japan)

- Yaskawa Electric Corporation (Japan)

- Murata Machinery, Ltd. (Muratec) (Japan)

- KUKA AG (Germany)

- Teradyne, Inc. (U.S.)

- Premier Tech (Canada)

KEY INDUSTRY DEVELOPMENTS

- October 2025: ABB Ltd. published a customer case showing Solema integrating ABB’s GoFa™ collaborative robot into its Omega 693 palletizing system, with ABB RobotStudio used to simulate the application and the system delivering over 20% productivity gains in palletizing operations.

- September 2025: FANUC Corporation highlighted expanded applications of its R-50iA controller with advanced motion control and energy efficiency features, improving the performance of robotic palletizing and material handling operations across industrial environments.

- June 2025: FANUC Corporation announced the new M-410/800F-32C heavy-payload palletizing robot, with 800 kg payload capacity, higher stacking reach, and support from the new R-50A controller for palletizing and loading/unloading applications.

- May 2025: KUKA AG published an official 2025 feature focused on modular robotic palletizing systems, highlighting faster integration, reduced downtime, and the use of solutions such as the KR QUANTEC PA in palletizing cells for manufacturing environments.

- March 2025: KUKA AG continued industrial deployment of its KR FORTEC PA palletizing robots, supporting heavy payload handling and high stacking performance in end-of-line automation processes.

REPORT COVERAGE

The global robotic palletizers and de-palletizers market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Payload Capacity, Robot Type, End-Use Industry, and Region |

| By Type |

|

| By Payload Capacity |

|

| By Robot Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.47 billion in 2025 and is projected to reach USD 7.02 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.99 billion.

The market is expected to exhibit a CAGR of 5.2% during the forecast period (2026-2034).

By end-use industry, the food & beverage segment leads the market.

Growing demand for higher operational efficiency is a key factor driving market growth.

ABB Ltd., FANUC Corporation, Daifuku Co., Ltd., Yaskawa Electric, and KUKA AG are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us