Robotic Radiotherapy Market Size, Share & Industry Analysis, By Product (Radiotherapy Systems, Software, 3D Cameras (Surface-Guided), & Others), By Technology (Linear Accelerators {Conventional Linear Accelerators & MRI - Linear Accelerators}, Stereotactic Radiation Therapy Systems {CyberKnife & Gamma Knife}, & Particle Therapy {Proton Beam Therapy & Heavy Ion Beam Therapy}), By Application (Prostate Cancer, Breast Cancer, Lung Cancer, Head & Neck Cancer, Colorectal Cancer, & Other Cancers), By End-user (Hospitals, Independent Radiotherapy Centers, & Others), and Regional Forecast, 2026-2034

Robotic Radiotherapy Market Size and Future Outlook

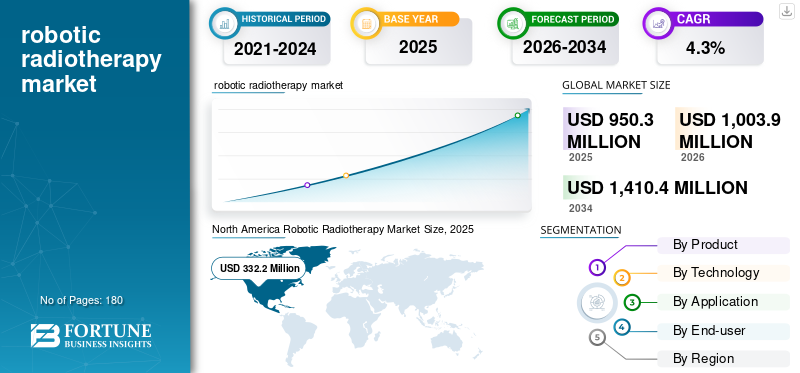

The global robotic radiotherapy market size was valued at USD 950.3 million in 2025. The market is projected to grow from USD 1,003.9 million in 2026 to USD 1,410.4 million by 2034, exhibiting a CAGR of 4.3% during the forecast period. North America dominated the robotic radiotherapy market with a market share of 34.96% in 2025.

Robotic radiotherapy refers to advanced radiation treatment systems that use robotic positioning, real-time imaging, and automated delivery to target tumors with high precision while protecting healthy tissue. These platforms combine high-accuracy beam delivery with motion management, adaptive planning, and software-driven workflows, making them especially valuable for complex cases and tumors that move with breathing. The market is growing as cancer incidence rises, hospitals prioritize shorter, more efficient treatment regimens, and clinicians expand the use of stereotactic procedures that require sub-millimeter accuracy. At the same time, the radiotherapy industry is shifting toward digitalization, AI-assisted planning, automated quality assurance, and integrated data platforms, which increases the value of software and workflow upgrades around robotic systems. In emerging markets, capacity expansion and private oncology networks are also driving demand for modern equipment that improves throughput, reduces rework, and supports consistent clinical outcomes across sites.

Furthermore, Accuray Incorporated, Siemens Healthineers, Elekta AB, and Ion Beam Applications (IBA) held the largest market share, driven by increased investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

ROBOTIC RADIOTHERAPY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 950.3 Million

- 2026 Market Size: USD 1,003.9 Million

- 2034 Forecast Market Size: USD 1,410.4 Million

- CAGR: 4.3% from 2026–2034

- North America dominated the robotic radiotherapy market with a 34.96% share in 2025.

- Linear accelerators are projected to account for 62.2% of the market in 2026.

- Hospitals are expected to hold a dominant 73.8% market share in 2026.

North America

North America generated USD 332.2 million in 2025.

Europe

Europe is expected to reach USD 285.1 million in 2026, supported by radiotherapy modernization and capacity expansion initiatives.

Asia Pacific

Asia Pacific is projected to reach USD 240.0 million in 2026, driven by rising cancer incidence and expanding treatment infrastructure.

U.S.

The robotic radiotherapy market is forecast to reach USD 316.2 million by 2026, accounting for 31.5% of global revenue.

Japan

The robotic radiotherapy market is projected to reach USD 37.2 million by 2026, representing 3.7% of global revenue.

Read More

ROBOTIC RADIOTHERAPY MARKET TRENDS

Convergence of Robotics, Imaging, and AI-driven Planning Mostly to Boost Overall Market

The market is trending toward tighter integration between robotic delivery, high-quality imaging, and AI-enabled planning. In practical terms, buyers increasingly evaluate systems as complete ecosystems, hardware plus software plus service, rather than as standalone machines. AI tools are moving from “nice to have” to daily clinical use: auto-contouring, plan-optimization assistants, and anomaly detection in QA can reduce planning time and standardize outputs across clinicians. Imaging is also becoming more central, with wider adoption of image-guided workflows and more frequent adaptive adjustments for tumors that shrink or shift over the course of treatment.

Another clear trend is motion management becoming mainstream. For thoracic and abdominal treatments, centers are increasingly adopting respiratory gating, breath-hold, and real-time tracking capabilities that align naturally with robotic automation. On the business side, subscription models and managed service agreements are gaining traction, especially for software and analytics layers. Finally, providers want interoperability and data visibility: tools that integrate with oncology IT systems and provide dashboards for utilization, protocol adherence, and treatment quality are influencing purchasing decisions as health systems push for measurable performance improvements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for High-Precision, Motion-Managed Radiotherapy Expected to Fuel Market Growth

A major driver for the growth is the rising clinical preference for high-precision radiotherapy techniques that can safely deliver higher doses per fraction to the tumor while limiting collateral damage. Robotic platforms are designed for accuracy and repeatability: they help clinicians track patient and tumor motion, correct positioning errors, and deliver beams from multiple angles with minimal manual intervention. This matters most in indications where organs move or where critical structures sit close to the tumor, such as the lung, liver, pancreas, and spine, and in select head & neck cases. As Stereotactic Radiosurgery (SRS) and Stereotactic Body Radiotherapy (SBRT) become more routine in cancer centers, demand for robotic radiotherapy systems that support image guidance, motion tracking, gating, and faster plan-to-treatment workflows increases.

In parallel, providers are under pressure to improve utilization of expensive treatment rooms; automation and better workflow integration can reduce set-up time, limit repeat imaging, and improve daily throughput. Finally, payers and providers increasingly value measurable quality and safety features such as automated QA, treatment log analytics, and standardized protocols, which improve confidence and support adoption across multi-site oncology networks.

MARKET RESTRAINTS

High Capital Cost and Complex Adoption Pathway Can Limit Market Growth

The biggest constraints are the total cost of ownership and the operational complexity of adopting robotic radiotherapy. Beyond the initial system purchase, buyers must factor in room shielding and construction, imaging upgrades, software licensing, service contracts, and periodic replacement of key components. Even well-funded centers may delay purchases if budgets are constrained or if reimbursement and utilization assumptions are uncertain. Implementation can also be demanding: robotic workflows often require additional commissioning, physics validation, and staff training, especially when introducing motion management, adaptive planning, or stereotactic protocols. Smaller facilities may struggle to justify investment without sufficient patient volumes or referral pipelines.

Integration is another hurdle; new systems must connect smoothly with oncology information systems, imaging archives, and planning tools while meeting cybersecurity and data governance requirements. In some settings, procurement cycles are lengthy and influenced by public tender rules, which can delay deployments. Finally, outcomes depend on consistent execution; if staffing is limited or turnover is high, centers may underuse advanced features, reducing the perceived return on investment and slowing broader market expansion.

MARKET OPPORTUNITIES

Software-led Upgrades and Expansion of Outpatient Oncology Networks to Create Significant Growth Opportunities

A strong opportunity for the robotic radiotherapy market growth lies in modernizing software and workflows across existing installed bases. Many providers are not replacing entire treatment platforms every cycle. Still, they will invest in add-on software modules such as adaptive planning, AI-assisted contouring, automated QA, and analytics to improve throughput and protocol consistency. Vendors that make upgrades easier to deploy, validate, and integrate can capture recurring revenue while helping hospitals raise performance without major capital projects.

Another opportunity is the steady growth of private oncology groups and outpatient radiotherapy networks, particularly in markets where centralized cancer centers are overburdened. These networks prioritize standardized workflows and predictable quality across sites, areas where automation, guided planning templates, and centralized oversight tools can add real value. There is also room for growth in motion management and surface-guided radiotherapy, which can improve setup accuracy, reduce imaging dose, and support techniques such as breath-hold for thoracic and breast cases. In emerging regions, new capacity additions create a window for “leapfrogging” older technologies. Providers may opt for more automated systems to reduce dependence on highly specialized staffing and to accelerate ramp-up to full clinical utilization.

MARKET CHALLENGES

Workflow Standardization, Staffing Constraints, and Quality Governance are Challenges to Market Growth

Even when budgets are available, operational challenges can slow adoption. Robotic radiotherapy demands disciplined workflows: simulation, contouring, planning, QA, and delivery must be aligned, and stereotactic treatments often require stricter tolerances than conventional fractionation. Many centers face staffing constraints, particularly shortages of experienced medical physicists and dosimetrists, which can lengthen commissioning timelines and limit the ability to scale advanced protocols. Training is not a one-time event; centers must maintain competency as software updates roll out and new clinical indications are added.

Another challenge is balancing speed with safety: automation can reduce manual steps, but providers need clear governance, audit trails, and well-defined exception handling to ensure quality. Interoperability issues can also create friction, especially when mixing vendor ecosystems or integrating third-party imaging, SGRT, and oncology information systems. Cybersecurity and data privacy requirements add further complexity as more functions move to networked software platforms. Finally, access and equity remain difficult: high-end robotic systems tend to cluster in major centers, and referral patterns may limit patient reach, particularly in rural areas or low-resource settings.

Segmentation Analysis

By Product

Rising Technological Advancements in Radiotherapy Systems to Drive Segment Growth

Based on product, the market is segmented into radiotherapy systems, software, 3D cameras (surface-guided), and others.

Radiotherapy systems hold the largest share as they represent the core capital purchase and the largest portion of project cost, including equipment, installation, shielding, and commissioning. Providers typically anchor procurement around a system’s clinical capabilities, image guidance, motion management, stereotactic precision, and room productivity, then add software and accessories afterward. Replacement cycles further support system dominance: even in mature markets, companies continue to invest in new platforms to improve throughput, reduce downtime, and expand advanced cancer treatment offerings.

Additionally, the software segment is projected to grow at a CAGR of 8.7% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Wide Utilization of Electrochemical Lactate Detection to Propel Segment Growth

By technology, the market is classified into linear accelerators, stereotactic radiation therapy systems, and particle therapy. Linear accelerators are further segmented into conventional linear accelerators and MRI-linear accelerators. Additionally, stereotactic radiation therapy systems are classified into CyberKnife and Gamma Knife systems. Furthermore, particle therapy is divided into proton beam therapy and heavy-ion beam therapy.

Linear accelerators lead as they are the workhorse technology of radiotherapy and are used across a broad set of tumor sites, from routine fractionated treatments to increasingly sophisticated stereotactic and image-guided workflows. Modern linacs support a wide clinical menu, including IMRT/VMAT, IGRT, gating, and, in some settings, adaptive capabilities, making them versatile for hospitals that want one platform to cover many indications. Moreover, the segment is projected to hold a 62.2% share in 2026.

Additionally, the particle therapy segment is estimated to grow at a CAGR of 9.6% during the forecast period.

By Application

Rising Lung Cancer Prevalence to Propel Segment Growth

By application, the market is classified into prostate cancer, breast cancer, lung cancer, head & neck cancer, colorectal cancer, and other cancers.

Lung cancer commands a high robotic radiotherapy market share as thoracic tumors frequently benefit from the precision and motion management that robotic radiotherapy enables. Respiratory motion can shift targets during treatment, and surrounding organs are sensitive, so techniques such as SBRT with real-time tracking, gating, or breath-hold are widely used to improve accuracy and reduce toxicity. In addition, lung cancer burden remains substantial globally, and many centers expand SBRT programs as they improve imaging, planning, and workflow efficiency. Moreover, the segment is projected to hold a 20.7% share in 2026.

Additionally, the colorectal cancer segment is estimated to grow at a CAGR of 4.6% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals to Propel Segment Growth

On the basis of end-user, the market is classified into hospitals, independent radiotherapy centers, and others.

Hospitals dominate as they carry the heaviest oncology caseloads, manage complex referrals, and are more likely to invest in high-cost infrastructure such as shielded vaults, imaging integration, and multidisciplinary staffing. Large hospital networks and academic medical centers also serve as regional hubs for stereotactic and motion-managed radiotherapy, where advanced robotics and software workflows are most valuable. Hospitals typically have stronger access to capital budgets, service contracts, and trained physics teams needed for commissioning and ongoing quality governance. Furthermore, the segment is set to hold 73.8% share in 2026.

In addition, the independent radiotherapy centers segment is projected to grow at a CAGR of 6.8% during the forecast period.

Robotic Radiotherapy Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Robotic Radiotherapy Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024 at USD 326.3 million, and further reported to have reached USD 332.2 million in 2025. Growth in North America is supported by a large installed base of radiotherapy equipment, steady replacement and upgrade cycles, and broad clinical adoption of high-precision techniques such as SBRT/SRS that benefit from automation and motion management. Cancer centers continue to invest in workflow efficiency such as, AI-assisted planning, adaptive modules, image guidance, and surface guidance, to improve throughput and standardize quality across multi-site networks. The region also benefits from strong reimbursement pathways for advanced radiotherapy in many settings, high penetration of outpatient oncology networks, and robust clinical evidence generation. It further encourages expansion of stereotactic programs for lung, prostate, spine, and oligometastatic disease.

U.S. Robotic Radiotherapy Market

In 2026, the U.S. market is forecasted to represent USD 316.2 million, capturing 31.5% of total global revenue.

Europe

Europe is expected to achieve a 2.4% growth rate in the coming years, the second-highest globally, reaching USD 285.1 million by 2026. Europe’s growth is driven by public and private investments aimed at modernizing radiotherapy capacity, replacing aging linacs, and expanding access to image-guided and stereotactic treatments. Many countries are prioritizing shorter, more efficient treatment regimens to manage waiting lists and optimize utilization of constrained radiotherapy resources, which increases demand for automation, motion management, and advanced planning software. The region also sees continued rollout of surface-guided workflows and adaptive planning in major centers, while regional cancer networks push for standardized protocols and centralized quality governance.

U.K. Robotic Radiotherapy Market

The U.K. market is projected to reach USD 42.4 million by 2026, accounting for 4.2% of the global market revenue.

Germany Robotic Radiotherapy Market

Germany's market is forecasted to reach about USD 50.6 million by 2026, representing roughly 5.0% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 240.0 million, ranking as the third-largest globally. Asia Pacific shows the fastest growth as expanding cancer burden, improving diagnosis rates, and rising healthcare spending drive rapid radiotherapy capacity additions alongside modernization in established markets. China and India are adding new treatment centers and upgrading technology, while Japan, Australia, and advanced Asia Pacific markets continue to invest in high-precision platforms, motion management, and software-driven workflows to improve consistency and reduce planning time. Private hospital chains and oncology networks are expanding in urban hubs, accelerating adoption of advanced systems that can deliver more patients per day and support premium service lines.

Japan Robotic Radiotherapy Market

Japan is projected to generate approximately USD 37.2 million in revenue by 2026, contributing nearly 3.7% to the global market.

China Robotic Radiotherapy Market

China’s market is forecast to reach approximately USD 87.2 million by 2026, contributing about 8.7% to global revenues.

India Robotic Radiotherapy Market

India is forecast to contribute approximately USD 29.5 million to the market by 2026, corresponding to about 2.9% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate market growth, with Latin America expected to reach around USD 67.2 million by 2026. Growth in Latin America is fueled by the gradual expansion of radiotherapy infrastructure, increasing cancer incidence, and efforts to reduce treatment gaps, particularly in large markets such as Brazil and Mexico. The Middle East & Africa region grows from a low base, driven by rising cancer burden, healthcare infrastructure development, and national initiatives to build or expand oncology services, especially in wealthier Gulf countries.

GCC Robotic Radiotherapy Market

By 2026, the GCC is expected to generate approximately USD 30.3 million in the market, accounting for nearly 3.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce Market Position of Prominent Players

The global robotic radiotherapy market is moderately consolidated at the top and fragmented in the long tail. A small group of large radiation oncology platforms dominates as they sell integrated ecosystems, treatment delivery hardware plus imaging, planning software, oncology IT, and multi-year service contracts, creating high switching costs once a hospital standardizes on a vendor. Key players such as Accuray Incorporated, Siemens Healthineers, Elekta AB, and Ion Beam Applications (IBA) held the largest market share.

Moreover, other key players, such as C-RAD AB, RaySearch Laboratories, Brainlab, and Vision RT, compete on installed-base monetization. Vendors push upgrades such as software modules, motion tracking, surface guidance integration, automation/AI that expand recurring revenue and deepen customer lock-in without requiring full system replacement.

LIST OF KEY ROBOTIC RADIOTHERAPY COMPANIES PROFILED

- Accuray Incorporated (U.S.)

- Siemens Healthineers (Germany)

- Elekta AB (Sweden)

- Ion Beam Applications (IBA) (Belgium)

- C-RAD AB (Sweden)

- RaySearch Laboratories (Sweden)

- Brainlab (Germany)

- Vision RT (U.K.)

- LAP GmbH (Germany)

- CQ Medical (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Elekta announced that its Elekta Evo CT-Linac has received 510(k) clearance from the U.S. Food and Drug Administration (FDA).

- August 2024: Accuray Incorporated and Halifax Health, in Volusia County, Florida, announced that the Charles L. and Miki N. Grant Cancer Center for Hope medical team is the first in the U.S. to treat cancer patients using the Accuray Radixact System with VitalHold technology.

- May 2024: Elekta announced the launch of its latest linear accelerator (linac), Evo, a CT-Linac with new high-definition AI-enhanced imaging, capable of delivering both offline and online adaptive radiation therapy, as well as improved standard image-guided radiation therapy.

- February 2024: Siemens Healthineers company, announced that it has received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for TrueBeam and Edge radiotherapy systems featuring HyperSight imaging solution.

- February 2023: RefleXion Medical, a therapeutic oncology company, announced that the U.S. Food and Drug Administration (FDA) has granted the first marketing clearance for its SCINTIX biology-guided radiotherapy, a cutting-edge treatment applicable for early and late-stage cancers.

- December 2022: Ion Beam Applications (IBA), the world leader in particle accelerator technology, confirms that it has signed a contract with the Spanish Ministry of Health to install ten proton therapy systems across Spain as part of a significant public tender.

- October 2022: Elekta announced that Elekta Esprit, a new Leksell Gamma Knife radiosurgery platform, received 510(k) clearance from the FDA. This milestone makes the system available to clinicians and people with brain disease in the U.S.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.3% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product, Technology, Application, End-user, and Region |

| By Product |

|

| By Technology |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 950.3 million in 2025 and is projected to reach USD 1,410.4 million by 2034.

In 2025, the market value stood at USD 332.2 million.

The market is expected to exhibit a CAGR of 4.3% during the forecast period.

The radiotherapy systems segment led the market by product.

The key factors driving the market are the rising cancer burden and technological advancements in the market.

Accuray Incorporated, Siemens Healthineers, Elekta AB, and Ion Beam Applications (IBA) are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us