Robotics in Shipbuilding Market Size, Share & Industry Analysis, By Solution (Shipbuilding and Inspection, Repair, Maintenance), By Robot Type (Articulated Robots, Collaborative Robots, Cartesian Robots, and Others), By Ship Type (Cargo Ships, Military/Naval Ships, Recreational Boats, and Offshore Vessels), By Application (Welding, Cutting, Assembly, Painting & Coating, Material Handling, Inspection and Maintenance, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

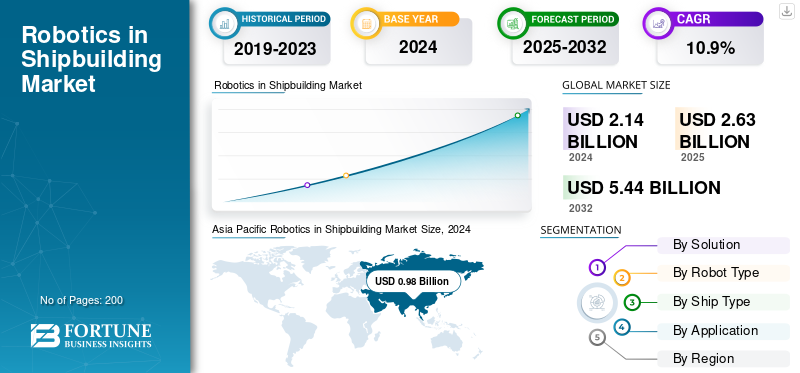

The global robotics in shipbuilding market size was valued at USD 2629.6 million in 2025. The market is projected to grow from USD 3117.1 million in 2026 to USD 5,750.80 million by 2034, exhibiting a CAGR of 8.00% during the forecast period. Asia Pacific dominated the global robotics in shipbuilding market with a market share of 45.50% in 2025.

Robotics technology applied to shipbuilding involves several key applications that are revolutionizing conventional manufacturing methods. Robotic technology offers high consistency and repeatability in operations such as welding, cutting, and painting, resulting in fewer defects and improved structural integrity of ships. Robotic welding eliminates the requirement for post-weld grinding, saving considerable time and labor costs.

Moreover, the shipbuilding sector faces a severe shortage of skilled labor. The Korea Offshore & Shipbuilding Association reported a shortfall of around 14,000 workers by 2023 and highlighted the need for an additional 45,000 workers to fulfill secured orders. Robotics fills this manpower gap by taking over hazardous and repetitive jobs. driving significant market growth throughout the forecast period.

Robotics operate around the clock without time off, greatly increasing shipbuilding processes. Advanced shipyards with completely automated production lines can operate 24/7, manufacturing pre-outfitted sections at twice the past rate with about the same number of people, thereby catalyzing the market growth.

In addition, the market includes various prominent market players with Broad portfolio with new-age products, and extensive regional presence growth have facilitated the market domination of these companies. Prominent shipyards include Samsung Heavy Industries (SHI), HD Hyundai Heavy Industries (HHI), COSCO Shipping Heavy Industry, Mitsubishi Heavy Industries (MHI), Naval Group, and so on.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Growing Concern of Labor Shortage and Skills Gap Mitigation to Drive the Market Growth

The shipbuilding sector is facing a historic workforce crisis that underpins the take-up of robotics across shipyards worldwide. The shortage of labor far exceeds simple headcount, including the loss of specialized skills, especially veteran welders and fabrication professionals who conventionally make up the heart of shipbuilding activities. The older workforce exacerbates the issue, as many experienced individuals are nearing retirement, while fewer young people are entering the maritime manufacturing industry.

Robotics offers the shipbuilding industry an outright solution by automating repetitive and time-consuming procedures, allowing shipyards to maintain production timelines despite manpower shortages. This technology also releases skilled people to focus on higher-value tasks that demand human judgment and decision-making skills.

Industry data indicate that shipyards employing robotic welding systems require far fewer experienced welders, with operations having been known to reduce welding staff needs by as much as 40% while maintaining or enhancing output quality. The technology fills the skills gap by providing less skilled workers with professional-grade capabilities through robot-assisted processes, where collaborative systems assist human operators in carrying out complex procedures.

Market Restraints

High Capital Investment and Implementation Costs of Robotics to Hamper the Market Growth

The large investment requirements involved in robotics deployment reflect the largest constraint impeding widespread application throughout the shipbuilding sector. It also impacts small yards and developing market operators. Suitable industrial robotic systems for marine applications typically entail capital expenditures of between USD 50,000 and USD 150,000 per unit, and total installation expenses, including integration, programming, and infrastructure updates, which usually run 200-300% higher than the initial equipment purchase costs.

These cost requirements extend beyond hardware purchases to include customized software development, facility upgrades, a commitment to innovation, and the installation of safety systems, as well as comprehensive employee training programs, all of which are necessary for the successful deployment of robotics. The payback period for the return on investment makes financial justification even more challenging, as shipbuilding is a long-cycle operation where gains may not be noticeable until several years after the initial application.

Small and medium-sized shipbuilders experience especially severe financial hardship in terms of considering robotics implementation, with limited volume of production and limited cash flow inhibiting the capability to absorb high initial investments and await longer-term productivity benefits.

Market Opportunities

Growing Implementation of Smart Shipyard Development and Digital Integration Catalyze the Market Growth

The merger of digital technologies with robotics provides evaluative possibilities for creating intelligent manufacturing environments that transform conventional shipbuilding strategies using complete automation and data-driven management. Robotics, IoT sensors, AI platforms, digital twin technology, and big data analytics come together to provide smart shipyard programs that create continuous production environments where physical and virtual systems work in perfect harmony.

These converged platforms enable real-time monitoring of all production processes, predictive maintenance planning, automatic quality control, and dynamic resource allocation, optimizing efficiency while reducing operational waste and costs. The digital connection extends beyond single robotic systems to entire production workflows, supply chain coordination, and customer interaction processes, transforming shipbuilding from classic manufacturing to service-based value creation.

Digital twin technology offers significant advantages, including the development of virtual copies of physical ships, manufacturing workflows, and entire shipyard operations that support simulation, optimization, and predictive analytics throughout vessel lifecycles. Virtual environments enable shipbuilders to test design changes, streamline production steps, and forecast maintenance needs prior to physical realization, thereby saving considerable development expenses and reducing time-to-market for new vessel designs.

Robotics in Shipbuilding Market Trends

Artificial Intelligence, Predictive Analytics Integration, Autonomous Inspection and Maintenance Technologies Drives the Market Trend

The fusion of artificial intelligence with robot systems is a disruptive trend that allows for autonomous decision-making, and ongoing process optimization. This technology provides predictive abilities that fundamentally revolutionize shipbuilding operations above and beyond the benefits of traditional automation. AI-driven robotics systems are capable of processing huge amounts of production data, weather conditions, and performance indicators to optimize welding parameters, material handling sequences. These systems also enhance quality control processes in real time without any human interference.

These smart systems are educated through operational experience, recognizing patterns and correlations that the human operators may overlook, while continually adjusting performance parameters to optimize efficiency and achieve quality results. Predictive functions are applied to maintenance scheduling, supply chain optimization, and production planning activities, generating integrated operational intelligence platforms that enable strategic decision-making across shipyard operations.

Advanced analytics platforms handle data from several robotic systems, production sensors, and environmental monitors to generate end-to-end operational efficiency. They provide predictive insights to support proactive management of intricate shipbuilding projects. The convergence of AI with digital twin technologies generates simulation environments where many different production scenarios can be simulated and optimized prior to physical implementation. This approach minimizes risk and maximizes outcomes for new ship designs and production processes.

The transition toward collaborative robotics is a basic transformation of shipbuilding automation philosophy from individual robot cells to integrated human-machine teams. This approach capitalizes on complementary strengths for maximum production effectiveness. Collaborative robots, or "cobots," are specifically engineered to coexist safely with human operators. They combine robotic precision, consistency, and relentless operation with human adaptability, problem-solving ability, and complex decision-making capabilities. This drives robotics in shipbuilding market growth.

Market Challenges

Cybersecurity and Digital Infrastructure Vulnerabilities Can Hinder the Market Growth

The expanding connectivity and digital integration of robot systems bring tremendous cybersecurity exposures that introduce substantial risk to shipyard operations and the safeguarding of intellectual property. These vulnerabilities also pose significant national security concerns in defense-linked maritime industry ventures. Advanced robot systems depend on networked communications, cloud-based processing, and remote monitoring. These elements provide possible avenues for attacks by malicious cyber elements to access sensitive design data, production timetables, or operational control systems.

The implications of effective cyber-attacks go beyond the theft of data to include the possible manipulation of manufacturing processes, quality control systems, or safety systems that might be used to jeopardize vessel integrity or worker safety. The global supply chain for robotic materials and software adds further security issues, as systems may contain pieces from several nations with different security practices and possible vulnerabilities.

Contemporary robots are challenging to protect against cyber threats, as they can be embedded in their hardware and software, as well as in their communication structures and connectivity, making it difficult to detect and mitigate these threats using cybersecurity techniques.

The quickness of technological development generates constant security concerns, as new functionalities and capabilities can introduce unexpected vulnerabilities that must be constantly monitored and counteracted. The lack of cybersecurity experts who understand industrial automation and maritime operations constrains the capacity of most shipyards to properly evaluate and defend robotic systems. Opening up potential security vulnerabilities that malicious actors could leveraged, aim to disrupt business operations or pilfer sensitive data.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Solution

Growing Need of Predictive Maintenance Integration and Digital Transformation Drives the Segment Growth

By solution, the market is segmented into shipbuilding and inspection, repair, maintenance.

The inspection, repair, maintenance segment is estimated to be the fastest growing segment in the forecast year of 2026-2034 with the highest CAGR of 11.2%. The growth is driven by increasing adoption of artificial intelligence-based predictive maintenance solutions. These solutions offer exponential opportunities through proactive intervention approaches that avoid equipment failures prior to their occurrence, thereby lowering maintenance expenses and downtime. Sophisticated sensor networks coupled with robotic inspection technologies constantly track ship operating parameters such as engine vibrations, oil condition, temperature gradients, and structural stress patterns. It also alerts predictive algorithms about potential issues weeks or months in advance of when they would be picked up through conventional maintenance cycles.

- For instance, in December 2024, Samsung Electronics significantly raised its holding in Rainbow Robotics to 35% from a USD 181 million investment, making the Korean robotics a leader subsidiary.

The shipbuilding segment will holds the highest market share of 54.49% in robotics applications in 2026, due to the gigantic scale and intricacy of new ship building operations that require extensive automation solutions across various manufacturing processes. Contemporary shipbuilding includes the construction of various types of vessels, ranging from container ships over 400 meters in length to advanced naval ships and offshore platforms. Each of these builds requires thousands of welded joints and accurate material handling operations. Additionally, the intricate assembly processes involved greatly benefit from robotic automation.

By Robot Type

Human-Robot Collaboration, Rapid Deployment and Integration Advantages Catalyze the Collaborative Robots Segmental Growth

By robot type, the market is divided into articulated robots, collaborative robots, cartesian robots, and others.

The collaborative robots is estimated to be the fastest growing segment during the forecast period with the highest CAGR of 12.4%. The growth is driven by revolutionary improvements in human-robot collaboration technologies that facilitate safe collaboration between human workers and automated systems in shared workplaces without conventional safety fencing. Collaborative robots come equipped with sophisticated sensor systems and safety software that sense the presence of humans. These features allow the robots to modify operating parameters or stop operations to avoid collisions, making it possible to deploy in already existing shipyard settings meant for human laborers. The integration of cobots into shipbuilding processes has resulted ins quantifiable improvements in productivity, such as 25% reduction in overall ship production time and a 30% productivity improvement through uninterrupted operation and enhanced capabilities. This is augmented by human intelligence for sophisticated decision-making and quality inspection.

- For instance, in September 2025, Persona AI and American Bureau of Shipping entered into a historic memorandum of understanding to create inspection technologies for humanoid robot platforms that are specifically intended to boost productivity and safety in shipyard settings. The partnership is centered on the installation of Persona AI's humanoid robots with NASA's robotic hand technology. It aims to facilitate sophisticated shipyard applications such as measurement, forming, control, and precision welding operations that conventionally demand skilled human operators.

To know how our report can help streamline your business, Speak to Analyst

The articulated robots segment will holds the largest market share of 56.12% in shipbuilding robotics in 2026, largely due to their superior six-axis flexibility, which allows for full movement capability akin to human arm motion, making them better suited for intricate maritime manufacturing processes. The advanced systems offer higher degrees of freedom in their six individual axes to enable precise positioning and orientation control required for detailed shipbuilding processes such as welding, material handling, assembly, and part installation tasks.

By Ship Type

The Growing Volume Production Requirements and Standardization Benefits Drives the Segmental Growth

The market is by ship type segment is further divided into cargo ships, military/naval ships, recreational boats, and offshore vessels.

The cargo ships segment will holds both the largest market share of 39.77% in 2026 and is estimated to be the fastest growing with highest CAGR of 11.8% among robotics applications, due to the vast volume production needs and standardization possibilities involved in commercial shipbuilding. International shipping demand leads to the ongoing construction of bulk carriers, container ships, and tankers. A given shipyard builds 20-50 cargo vessels per year across several standardized designs to maximize robotics deployment efficiency. The commercial ship sector accounts for the largest market share due to growing international demand for cargo vessels, cruise ships, and bulk carriers, driven by the expansion of international trade and increasing maritime logistics needs. The standardized process of building cargo vessels enables shipyards to develop specialized, robot-based solutions that can be replicated for numerous similar projects, ensuring a high return on investment and continually refining automation capabilities through ongoing refinement processes.

- For instance, in August 2024 Garden Reach Shipbuilders & Engineers Limited adopted wide-ranging technology updates such as six AI applications in several operating functions, robotic welding systems to boost productivity, and automated warehouse management systems that serve defense vessel building.

The military and naval ships sub-segment depicts the second quickest growth rate due to historic defense modernization initiatives across the globe. These initiatives necessitate advanced robotic solutions for building advanced warfare platforms that involve complex weapon systems and stealth technologies. Naval construction poses challenges that demand expert robotic solutions for the manipulation of classified materials, precise welding of high-performance alloys. Moreover, the assembly of advanced electronic warfare systems is greatly enhanced by automated precision and inspection. The creation of unmanned naval vessels such as autonomous underwater vehicles and unmanned surface vessels generates additional need for robot construction skills that are tailored to military use.

By Application

Digital Transformation, Predictive Analytics Integration, Autonomous Underwater Vehicle Revolution and Cost Avoidance Drives the Segmental Growth

The market is segmented by application into welding, cutting, assembly, painting & coating, material handling, inspection and maintenance, and others.

The inspection and maintenance segment exhibits the highest growth rate, mainly as a result of technological breakthroughs in autonomous underwater vehicles and robotics that allow thorough hull inspections and maintenance activities while ships are still in operation, thereby removing expensive dry-docking needs. The quick uptake of artificial intelligence-based predictive maintenance solutions presents exponential growth opportunities within the market, enabling proactive intervention strategies to avoid equipment breakdowns before they occur. It also reduces maintenance expenses and operational downtime while maximizing equipment life.

The welding segment will holds the highest market share of 29.75% in 2026, in shipbuilding robot applications based on the unprecedented number of welding operations involved in ship building, where single vessels demand 15,000 to 40,000 welded joints by size and complexity. New generation cargo ships and naval vessels entail gargantuan steel fabrication demands. Robotic welding systems deliver uniform quality, higher accuracy, and round-the-clock operation possibilities that are not available through manual welding in such vast ship construction processes.

- For instance, in September 2025, Finnish welding automation expert Pemamek Oy secured a second significant order from Spanish shipbuilding company Astilleros Gondán for the turnkey supply of an advanced PEMA VRWP-SH robotic welding station with two welding units for open block welding operations.

Robotics in Shipbuilding Market Regional Analysis

By geographic, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Robotics in Shipbuilding Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 1195.42 Million in 2025, representing 45.46% of the global industry, and is expected to reach USD 1409.88 Million in 2026. The Asia Pacific region holds the highest robotics in shipbuilding market share of 45.69% in robotics in shipbuilding, largely due to its dominance of world shipbuilding capacity, with China, South Korea, and Japan together representing about 90% of global ship manufacturing. The Japan market is projected to reach USD 328.36 million by 2026, the China market is projected to reach USD 641.07 million by 2026, and the India market is projected to reach USD 66.55 million by 2026.

The scale of the region's shipbuilding complex imposes unprecedented requirements for automated solutions. Giant shipbuilders, such as Hyundai Heavy Industries, Samsung Heavy Industries, and China State Shipbuilding Corporation, have facilities that can produce several ships in parallel over standardized production lines. The adoption of robots within shipyards is highest in China, South Korea, and Japan, which are significant drivers of the growth of the Asia Pacific market, aided by their high manufacturing capacity and ambitious automation adoption policies.

China's shipbuilding robotics market growth directly results from China's overall Made in China 2025 industry strategy that targets high-technology manufacturing restructuring and indigenous capability development in the production of core components. The master plan increased local content in high-tech ships to 80% in 2025 as it develops end-to-end industrial chains for design, assembly, and equipment supply services that decrease reliance on overseas providers. The Chinese government offers sizeable fiscal support through specialized subsidy schemes. Approximately 82% of these subsidies provide financial assistance over 10% of robot equipment purchase costs. On average, subsidy rates are around 17.5%, which significantly impacts the manufacturing sector’s uptake of robotics.

Europe

In 2025, Europe generated USD 739.97 Million, contributing 28.14% to global market revenue, and is projected to grow to USD 886.82 Million in 2026. Europe has the highest growth rate in robotics in shipbuilding essentially due to the holistic digital transformation programs and a position of leadership in Industry 4.0 technologies that are transforming maritime manufacturing on the continent. European shipbuilders are utilizing advanced digital platforms that consolidate robotics with all-embracing data analytics and predictive maintenance systems. This integration along with artificial intelligence, helps design intelligent manufacturing environments that maximize productivity while ensuring higher quality outputs. European shipyards are expert in intricate, high-value vessel fabrication such as cruise ships, naval frigates, and customized offshore platforms requiring advanced robotic solutions for precise assembly and quality control. Fincantieri and Meyer Werft are world leaders in cruise shipbuilding, establishing benchmarks for future-generation green vessels through the wide-ranging automation incorporation, integrating high-tech robotics with green compliance technology. The Germany market is projected to reach USD 162.29 million by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 563.79 Million in 2025, accounting for 21.44% share, and is expected to reach USD 672.05 Million in 2026. North America play a significant role in the robotics in shipbuilding industry, driven by high defense spending and advanced robot technology integration programs from premier military contractors. General Dynamics and Huntington Ingalls Industries are the U.S. biggest military shipbuilders with extensive robotics programs for nuclear submarine and aircraft carrier production. They demand complex automation to handle classified materials and advanced propulsion systems. The U.S. market is projected to reach USD 562.37 million by 2026.

Rest of the World

The rest of the world, which includes Latin America, the Middle East, Africa, and other emerging maritime economies, reflects an increased uptake of shipbuilding robotics due to the widening of offshore exploration activities and rising commercial vessel demand. Rest of the World accounted for USD 130.43 Million in 2025, representing 4.96% of the global market share, and is projected to reach USD 148.38 Million in 2026. The Middle East nations, especially the UAE and Saudi Arabia, invest significantly in maritime infrastructure that comprises enhanced shipyard facilities with enhanced robotics for commercial vessels and naval shipbuilding.

Competitive Landscape

Key industry Players

Key Players’ Focus on the Quality and Precision Advantages Strengthen Their Market Position

The competitive context increasingly supports companies that can provide advanced collaborative robotics solutions facilitating seamless human-robot collaboration in intricate shipbuilding environments. These solutions offer differentiated value propositions that extend beyond conventional industrial automation.

Universal Robots (Denmark) gained market dominance in the application of collaborative robots. They made flexible systems easily deployed and reconfigured for various shipyard operations without the need for significant technical knowledge or safety infrastructure redesign. The competitive edge of the Danish firm lies in intuitive programming interfaces, sophisticated safety systems. Their modular design methodologies allow shipyards to adopt automation step by step while preserving flexibility of operations and worker involvement.

The competitive market is vulnerable to disruption by advanced startups creating specialized robotics solutions tailored to specific shipbuilding challenges using innovative technological solutions and nimble development practices.

Neptune Robotics (China) became a major competitive challenge in hull cleaning and underwater inspection uses, creating autonomous systems that encompass above-water and underwater capabilities in one system and integrating high-end filtration systems that tackle environmental compliance needs. The Chinese startup's strength is in its targeted strategy for particular maritime use cases coupled with the use of artificial intelligence and big data analysis to deliver end-to-end fleet management solutions beyond standard robotics capabilities.

List of Key Global Robotics in Shipbuilding Companies Profiled (Robotics Technology Provider

- ABB (Switzerland)

- FANUC (Japan)

- KUKA AG (Germany)

- Yaskawa Electric (Japan)

- Kawasaki Robotics (Japan)

- Mitsubishi Electric (Japan)

- Nachi-Fujikoshi (Japan)

- Staübli (Switzerland)

- Epson (Japan)

- Universal Robots (Denmark)

- Comau (Italy)

- Denso Robotics (Japan)

- Inrotech (Denmark)

List of Key Global Robotics in Shipbuilding Companies Profiled: (Shipyards Who Use Robotics for Shipbuilding

- Samsung Heavy Industries (SHI) (South Korea)

- HD Hyundai Heavy Industries (HHI) (South Korea)

- Hanwha Ocean (South Korea)

- Shanghai Waigaoqiao Shipbuilding (SWS) (China)

- China Shipbuilding (China)

- Mitsubishi Heavy Industries (MHI) (Japan)

- Japan Marine United (JMU) (Japan)

- Oshima Shipbuilding (Japan)

- Fincantieri (Italy)

- Naval Group (France)

- Navantia (Spain)

- ThyssenKrupp Marine Systems (TKMS) (Germany)

- General Dynamics NASSCO (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Nippon Yusen Kabushiki Kaisha (NYK Line), a global leader in shipping companies, extended its collaboration with Neptune Robotics to increase robotic hull cleaning across its international fleet, supporting maritime decarbonization projects. Neptune's AI robots can clean full-draft Capesize vessels 3-5 times faster than traditional systems, working autonomously above and below water within currents of up to 4 knots - three times the ability of human divers.

- September 2025: Startup DIDEN Robotics, based at KAIST, successfully showcased its feature model, the DIDEN 30 quadruped robot, at prominent Korean shipyards such as Samsung Heavy Industries, HD Hyundai Samho, Hanwha Ocean, and HD Korea Shipbuilding & Offshore Engineering. The cutting-edge robot successfully tested navigating tightly installed steel supports (longitudinals) at a shipyard, indicating it can excel in challenging sea-construction sites.

- July 2025: Hanwha Robotics signed a wide-ranging memorandum of understanding with Royal IHC, a leading Dutch shipyard that generates around USD 509.5 million in annual sales, to jointly develop collaborative robot-based welding automation technology. The agreement includes joint development and marketing of welding automation solutions, technology and human exchanges, and extensive information sharing programs across various specialty vessel construction applications.

- July 2025: Russia's Baltic Shipyard adopted sophisticated collaborative welding robots featuring machine vision systems to speed up the construction of nuclear-powered icebreakers and other specialized ships. These groundbreaking robots automatically scan workpieces, generate three-dimensional models, calculate the best welding lines and paths, inspect metal thickness, and set up required weld parameters without the need for manual programming or graphic modeling.

- February 2025: Damen Shiprepair Dunkerque received five AMBPR Autonomous Mobile Blast & Paint Robots after rigorous successful trials, the world's first shipyard to order these groundbreaking hull restoration systems. The advanced robots perform entire cycles of hull restoration such as cleaning at 400 bars pressure, ultra-high pressure water jetting at 2,500 bars, and effective painting of 100 square meters per hour, greatly minimizing vessel downtime while delivering quality consistency.

REPORT COVERAGE

The market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market trends and dynamics expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.0% from 2026-2034 |

|

Unit |

USD Million |

|

Segmentation |

By Solution · Shipbuilding · Inspection, Repair, Maintenance By Robot Type · Articulated Robots · Collaborative Robots · Cartesian Robots · Others By Ship Type · Cargo Ships · Military/Naval Ships · Recreational Boats · Offshore Vessels By Application · Welding · Cutting · Assembly · Painting & Coating · Material Handling · Inspection and Maintenance · Others North America (By Solution, By Robot Type, By Ship Type, By Application, By Country) · U.S. (By Ship Type) · Canada (By Ship Type) Europe (By Solution, By Robot Type, By Ship Type, By Application, By Country) · Italy (By Ship Type) · Germany (By Ship Type) · France (By Ship Type) · Nordic Countries (By Ship Type) · Russia (By Ship Type) · Rest of Europe (By Ship Type) Asia Pacific (By Solution, By Robot Type, By Ship Type, By Application, By Country) · China (By Ship Type) · Japan (By Ship Type) · South Korea (By Ship Type) · India (By Ship Type) · Southeast Asia (By Ship Type) · Rest of Asia Pacific (By Ship Type) Rest of World (By Solution, By Robot Type, By Ship Type, By Application, By Country) · Middle East & Africa (By Ship Type) · Latin America (By Ship Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2629.6 million in 2025 and is projected to reach USD 5,750.80 billion by 2034.

2025年の市場規模は7億4,000万米ドルであった

The market is expected to exhibit a CAGR of 8.00% during the forecast period of 2026-2034.

The inspection, repair, maintenance segment is expected to hold the highest CAGR over the forecast period.

Growing concern of labor shortage and skills gap mitigation are the key factors driving the market.

Raytheon Technologies, Lockheed Martin, ThyssenKrupp Marine Systems, Thales Group, General Atomics, and among others are top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us