Rosacea Drugs Market Size, Share & Industry Analysis, By Drug Class (Anti-inflammatory Agents, Anti-inflammatory Antibiotics, Anti-infective Agents, Anti-parasitic Agents, Vasoactive Agents, and Others), By Disease Type (Erythematotelangiectatic Rosacea, Papulopustular Rosacea, Phymatous Rosacea, Ocular Rosacea, and Others), By Route of Administration (Topical, Oral, and Others), By Age Group (Pediatric and Adults), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

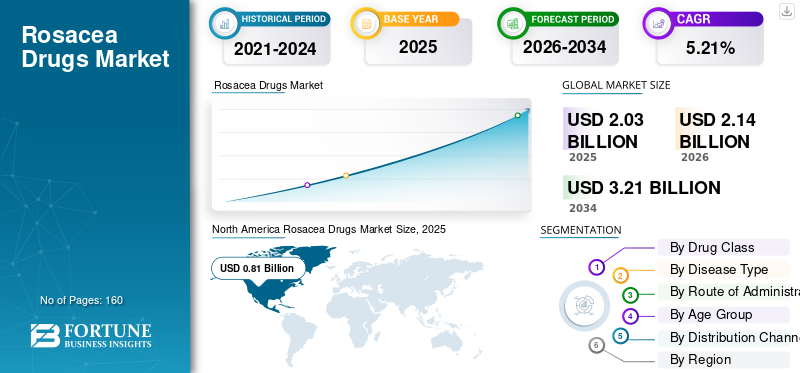

The global rosacea drugs market size was valued at USD 2.03 billion in 2025 and is projected to grow from USD 2.14 billion in 2026 to USD 3.21 billion by 2034, exhibiting a CAGR of 5.21% during the forecast period. North America dominated the global market with a share of 39.9% in 2025.

Rosacea refers to a chronic inflammatory condition which commonly impacts the central part of the face such as the nose, chin, cheeks and the forehead. Some of the characteristic features of the disease includes persistent redness, visible blood vessels, flushing, and other symptoms. In some patients, the symptoms may include acne-like bumps and pustules. Rosacea mainly affects the adults and may progressively worsen, if not effectively managed through the administration of therapies. The global market is estimated to grow at a steady growth rate particularly driven by rising awareness in the patient population coupled with refreshment of treatment guidelines with particular emphasis on phenotype precision that is further augmenting the market growth. Another important factor is the increasing prevalence of rosacea globally. Moreover, in recent times there have been several strategic initiatives involving key products that further drives the accessibility of major therapies, again leading to market growth. In spite of generic competition that challenges some growth prospects, development of oral therapeutics with differentiated claims is set to determine the positive growth trajectory across the forecast period. Innovative product launches by key market players such as Journey Medical Corporation, is also expected to further provide impetus to the market growth.

- For instance, in March 2025, Journey Medical Corporation announced that the U.S. FDA had approved the company product of Emrosi (Minocycline Hydrochloride) Extended-Release Capsules, 40mg, that is indicated for the treatment of papulopustular rosacea.

Also, several pharmaceutical companies such as GALDERMA, Journey Medical Corporation, Mayne Pharma Group Limited, and others, are among the major players in the market. These companies are emphasizing on strategic initiatives coupled with innovative product launches to strengthen their presence in the global market.

Download Free sample to learn more about this report.

Rosacea Drugs Market Key Takeaways

- 2025 Market Size: USD 2.03 billion

- 2026 Market Size: USD 2.14 billion

- 2034 Forecast Market Size: USD 3.21 billion

- CAGR: 5.21% from 2026-2034

- North America dominated the rosacea drugs market with a 39.9% share in 2025.

- The anti-inflammatory agents segment is projected to grow at a CAGR of 7.56% during the forecast period.

- The erythematotelangiectatic rosacea segment is expected to expand at a CAGR of 6.03% during the forecast period.

North America

North America reached USD 0.81 billion in 2025, maintaining its position as the largest regional market.

Europe

Europe is projected to reach USD 0.59 billion in 2026, growing at a CAGR of 2.85% during the forecast period.

Asia Pacific

Asia Pacific accounted for USD 0.50 billion in 2025, ranking as the third-largest regional market.

U.S.

The market is estimated to reach USD 0.80 billion in 2026, accounting for approximately 37.4% of global sales.

Japan

The market was valued at approximately USD 0.09 billion in 2025, representing around 4.6% of global revenue.

Read More

ROSACEA DRUGS MARKET TRENDS

Transition Toward Oral Medications from a Topical Heavy Treatment Pattern is a Key Market Trend

One of the most critical trends witnessed in the global market is the increasing advent of innovative oral therapies in the mainstream. Historically, for the treatment of rosacea, utilization of long-term systematic antibiotics faced strong resistance due to its adverse effects. In recent times, in the high growth markets such as the U.S., a new branded oral therapy was approved for the treatment of moderate to severe form of papulopustular disease. If a large number of patients show improved treatment outcomes from these newer alternatives as compared to the older, traditional drugs, an increasing number of prescribers may shift to these oral therapies, further propelling the market growth across the forecast period.

- The new oral therapy that was approved in the U.S. was Journey Medical Corporation’s drug of Emrosi. In November 2025, the company noted that the total number of Emrosi prescriptions increased 146% over the second quarter of 2025.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Broad Regulatory Access to Several Therapies Coupled with Improved Treatment Algorithm to Bolster Market Growth

Some of the drivers that will contribute to the sustained market growth across the forecast period is the fact that several therapies have approvals from key regulatory agencies such as the U.S. FDA. This is important as the presence of diverse therapies for indications such as inflammatory lesions and erythema, leads to the creation of clinician’ confidence and also payer familiarity. For some mature classes of drugs such as metronidazole and azelaic acid, generic equivalents are present which supports high volume prescribing and repeat prescription refills. Also, recent updates to the treatment algorithm for rosacea, supports more consistent treatment decisions, further driving the uptake of major drugs. All these factors collectively drive the rosacea drugs market growth across the forecast period.

- For instance, in March 2025, National Rosacea Society (NRS) announced the introduction of updated rosacea treatment algorithms, that is considerably based on the phenotype model established by the 2017 updated standard classification and pathophysiology of rosacea.

MARKET RESTRAINTS

Pressures from Generic Equivalents Coupled with Concerns Regarding Side Effects to Restrict Wider Market Growth

The most critical factor that restrains the greater growth rate of this market is the fact that presence of generic competition compresses the market value in core lesion therapies, despite demand for effective treatment. Several common therapies that have higher volumes such as metronidazole and azelaic acid often face intense generic competition. Another key drawback in this market is concerns regarding adverse effects attributed to the administration of these drugs. Some of the common side effects of the existing therapies includes irritation, and triggering of rosacea flares. This leads to a less effective real world adherence of key drugs as compared to the efficacy witnessed in the clinical trials. This further dampens the market growth prospects for other innovative drugs.

- For example, in June 2021, Teva Pharmaceuticals announced the U.S. launch of the generic equivalent of SOOLANTRA (ivermectin) Cream, 1%, which is administered once daily.

MARKET OPPORTUNITIES

Development of Therapies for Ocular Rosacea to Provide Avenues for Market Growth

One of the key forms of rosacea is ocular rosacea that is often under treated, has a wide patient population base, and also has no U.S. FDA approved therapy. Hence, there is a growing demand for these drugs. If a drug is specifically developed for ocular rosacea, it can lead to the creation of new category of reimbursed rosacea drugs, significantly driving the market growth as it would be considered among the premium therapies. The market can be further poised for even more growth if this approval can address the concern of Demodex eradication.

- For instance, in January 2025, Tarsus Pharmaceuticals, Inc. announced that it was planning the Phase 2 initiation of its TP-04 ocular rosacea program. Such approvals can potentially create a submarket within the rosacea drugs market.

MARKET CHALLENGES

Treatment Failures and Reimbursement Coverage Concerns to Pose Challenges to Market Growth

Major challenges associated with the rosacea drugs market is the probability of treatment failures due to the various patients having different phenotypes, leading to differing endpoints. This includes differences in lesion counts, erythema scale, and presence of ocular symptoms. Hence, it creates a situation, wherein the innovating company is unable to gain market share without combination with other therapies or the expansion of their phenotypes. Furthermore, healthcare payers often necessitate failures on existing generic therapies, before covering the newer ones. This considerably reduces the market growth as it delays the patient access to key drugs and also eliminates the possibility of early adoption. Such challenges reduce the probability of a greater market growth rate.

- For instance, in November 2025, UnitedHealthcare has imposed a prior authorization criterion of documented rosacea, inflammatory lesions, and a history of failure or contraindication or intolerance after a 30-day trial to other drugs, before it will cover EPSOLAY.

Segmentation Analysis

By Drug Class

Strong Prescribing Trends of Anti-infective Agents to Bolster Segmental Dominance

On the basis of drug class segment, the market is segmented into anti-inflammatory agents, anti-inflammatory antibiotics, anti-infective agents, anti-parasitic agents, vasoactive agents, and others.

As of drug class, the anti-infective agents segment is projected to account for the largest rosacea drugs market share. The segment’s dominating market share is owing to the fact that anti-infective agents such as metronidazole are often at the forefront of routine rosacea treatment prescriptions. Furthermore, a considerable number of physicians are familiar with these therapies and they have widespread approvals for reimbursement from the payers and also have a heavy generic use volume.

- For instance, variants of metronidazole gel, that is the variants of 0.75% and 1%, is commercialized by GALDERMA under the brand name of METROGEL. Metronidazole, is a prominently used anti-infective agent.

The anti-inflammatory agents segment is anticipated to rise with a CAGR of 7.56% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Type

Strong Regulatory Approvals to Lead to Dominance of Papulopustular Rosacea Segment

On the basis of disease type, the market is segmented into erythematotelangiectatic rosacea, papulopustular rosacea, phymatous rosacea, ocular rosacea, and others.

In 2025, the papulopustular rosacea segment accounted for the dominant revenue share of the global market. This segment’s dominance is primarily due to the reason that it is a form of rosacea and is more addressable in terms of treatment and a considerable proportion of U.S. FDA approvals revolve around treatment of inflammatory lesions that is papules or pustules. Hence, this has led to a large number of product approvals for this form of disease, historically and recently, driving the segmental growth.

- For instance, in September 2025, Sol-Gel Technologies, Ltd. announced the Health Canada approval of EPSOLAY for the treatment of inflammatory lesions of rosacea in adults.

The erythematotelangiectatic rosacea segment is projected to grow at a CAGR of 6.03% over the forecast period.

By Route of Administration

Adoption of Topical Formulations as a First Line of Treatment to Enable Segmental Dominance

In terms of route of administration segment, the market is segmented into topical, oral, and others.

The topical segment accounted for the dominant market share over the forecast period. The dominant share is due to increased adoption of these drugs owing to treatment guidelines that allow for the widespread prescriptions of topical drugs for a chronic facial disease. This is due to the drugs having an acceptable safety and tolerability expectations. Also, the large number of drugs approved by the U.S. FDA are topical formulations, which keep it as a first line treatment for rosacea.

- For instance, in September 2023, Mayne Pharma Group, announced that one of its U.S. subsidiaries entered into an asset purchase agreement for the acquiring of the global rights to RHOFADE from Novan, Inc. RHOFADE is a topical treatment.

The others segment is projected to grow at a CAGR of 4.45% over the forecast period.

By Age Group

Strong Treatment Adoption Rates Among Adults to Boost Segment’s Dominance

On the basis of age groups, the market is segmented into pediatric and adults.

The adults segment accounted for the largest market share over the forecast period. The adults segment accounts for the dominating market share as an overwhelming number of drugs are indicated for the adult demographics. Also, many pivotal clinical trials are focused on the adult patients and pediatric rosacea is rarer and often lacks the presence of approved products.

- For instance, major rosacea drugs are approved for adults only, which includes the drug of EMROSI (Minocycline Hydrochloride) Extended-Release Capsules, 40mg, among others.

The pediatric segment is projected to grow at a CAGR of 9.58% over the forecast period.

By Distribution Channel

Repeat Purchases of Prescribed Drugs to Lead to Drug Stores & Retail Pharmacies’ Segment’s Market Dominance

In terms of distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

The drug stores & retail pharmacies accounted for the largest global market share. The drug stores & retail pharmacies held a significant proportion of the market value as rosacea is a condition that is majorly managed in outpatient settings and requires prescription refills over a long term duration. Furthermore, the segment is set to hold 73.78% share in 2026.

- For instance, in November 2025, one of India’s largest pharmacy chains, Apollo Pharmacy outlined its plans to open two stores per day in its network of pharmacies, over the next five years. These demonstrates the footprint of this segment in one of the key markets globally.

Furthermore, the online pharmacies segment is projected to grow at a CAGR of 9.67% across the forecast period.

Rosacea Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Rosacea Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 0.77 billion, and also maintained the leading share in 2025, with USD 0.81 billion. The market in North America is projected to grow significantly across the forecast period owing to adoption of innovative therapies, launches of advanced therapeutics such as Emrosi, strong payer approval trends and robust retail dispensing volumes. These factors, coupled with advancements in treatment guidelines and diagnostics, is to drive the market growth in the region.

U.S. Rosacea Drugs Market

Based on North America’s regional dominance and the U.S.’ largest share within the region, the U.S. market can be analytically approximated at around USD 0.80 billion in 2026, accounting for roughly 37.4% of global rosacea drugs sales.

Europe

Europe is on track to record a growth rate of 2.85% in the coming years and reach a valuation of USD 0.59 billion by 2026. Some of the parameters to the region’s strong market share includes the presence of strong clinical guidelines, strong local reimbursement pathways, and robust treatment adoption rates.

U.K Rosacea Drugs Market

The U.K. market in 2025 reached the valuation of around USD 0.12 billion, representing roughly 5.8% of global revenues.

Germany Rosacea Drugs Market

Germany’s market reached approximately USD 0.14 billion in 2025, equivalent to around 6.9% of global sales.

Asia Pacific

Asia Pacific market reached the valuation of USD 0.50 billion in 2025 and secured the position of the third-largest region in the market. In the region, India and China was valued at USD 0.06 billion and USD 0.15 billion, respectively in 2025.

Japan Rosacea Drugs Market

The Japan’s market in 2025 was approximately valued around USD 0.09 billion, accounting for roughly 4.6% of global revenues. Japan has a large share in the global market owing to the country’s strong approvals for domestic drugs for this disease coupled with established treatment guidelines.

China Rosacea Drugs Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued around USD 0.15 billion, representing roughly 7.5% of global sales.

India Rosacea Drugs Market

The India’s market in 2025 was valued at USD 0.06 billion, accounting for roughly 2.7% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness steady positive growth rates in this market space during the forecast period. The Latin America market reached a valuation of USD 0.09 billion in 2025. Increasing access toward newer drugs owing to a competitive private sector, coupled with considerable patient population drives the market growth in these regions.

GCC Rosacea Drugs Market

The GCC is set to reach a value of USD 0.03 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Product Portfolio Breadth Coupled with Diverse Geographical Reach to Enable Dominance of Key Players

The global rosacea drugs market comprises of a semi-fragmented competitive structure, including key companies such as GALDERMA, Journey Medical Corporation, Mayne Pharma Group Limited. The significant company revenue share accounted by these companies is owing to presence of established product portfolio, strong payer access, and a robust global footprint. Furthermore, these players are also engaged in several clinical trial initiatives for the approvals of innovative drugs.

- For instance, in September 2025, GALDERMA provided updates from its portfolio at the 34th European Academy of Dermatology and Venereology (EADV) Congress, which included dermatological diseases such as sensitive skin, prurigo nodularis, and atopic dermatitis. The company also presented data on the evaluation of the key differences between sensitive skin and rosacea.

Other major companies present in the global market includes Sol-Gel Technologies Ltd., Bayer AG, Sanofi and others. These companies have major branded rosacea drugs in their product portfolio and strong regulatory approvals which support their strong market share across the forecast period.

LIST OF KEY ROSACEA DRUGS MARKET COMPANIES PROFILED IN REPORT:

- GALDERMA (Switzerland)

- Journey Medical Corporation (U.S.)

- Mayne Pharma Group Limited (Australia)

- Sol-Gel Technologies Ltd. (Israel)

- Bayer AG (Germany)

- Sanofi (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- GLENMARK PHARMACEUTICALS LTD. (India)

- Padagis (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Aurobindo Pharma Limited announced that it had received the final approval for it’s Abbreviated New Drug Application (ANDA) for metronidazole topical cream, 0.75%.

- April 2024: Lupin Limited announced the launch of the first generic version of Oracea (Doxycycline Capsules, 40 mg) in the U.S., after receiving approval from the U.S. FDA.

- May 2023: Reddy’s Laboratories Ltd., announced the launch of Doxycycline Capsules, 40 mg in the U.S. market, post gaining an approval from the U.S. FDA.

- April 2023: Zydus Lifesciences Limited announced receiving the final approval from the U.S. FDA to manufacture and market metronidazole topical cream, 0.75%.

- February 2023: Cosette Pharmaceuticals announced the U.S. FDA approval and launch of Metronidazole USP 1%.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 5.21% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Region |

|

By Drug Class |

· Anti-inflammatory Agents · Anti-inflammatory Antibiotics · Anti-infective Agents · Anti-parasitic Agents · Vasoactive Agents · Others |

|

By Disease Type |

· Erythematotelangiectatic Rosacea · Papulopustular Rosacea · Phymatous Rosacea · Ocular Rosacea · Others |

|

By Route of Administration |

· Topical · Oral · Others |

|

By Age Group |

· Pediatric · Adults |

|

By Distribution Channel |

· Hospital Pharmacies · Drug Stores & Retail Pharmacies · Online Pharmacies |

|

By Region |

· North America (By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Country) o U.S. o Canada · Europe (By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Country/Sub-Region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Country/Sub-Region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Country/Sub-Region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Drug Class, Disease Type, Route of Administration, Age Group, Distribution Channel, and Country/Sub-Region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.03 billion in 2025 and is projected to reach USD 3.21 billion by 2034.

In 2025, the market value stood at USD 0.81 billion.

The market is expected to exhibit a CAGR of 5.21% during the forecast period of 2026-2034.

By drug class, the anti-infective agents segment is expected to lead the market.

Innovative product launches, expanding patient base coupled with improved awareness of rosacea is driving the market expansion.

GALDERMA, Journey Medical Corporation, Mayne Pharma Group Limited are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us