Rubber Process Oil Market Size, Share & Industry Analysis, By Product Type (TDAE, Naphthenic, MES, Paraffinic, RAE & TRAE, and Others), By End Use (Tyres, Industrial Rubber Goods, Automotive Components, Consumer Goods & Footwear, and Others), and Regional Forecast, 2026-2034

Rubber Process Oil Market Size and Future Outlook

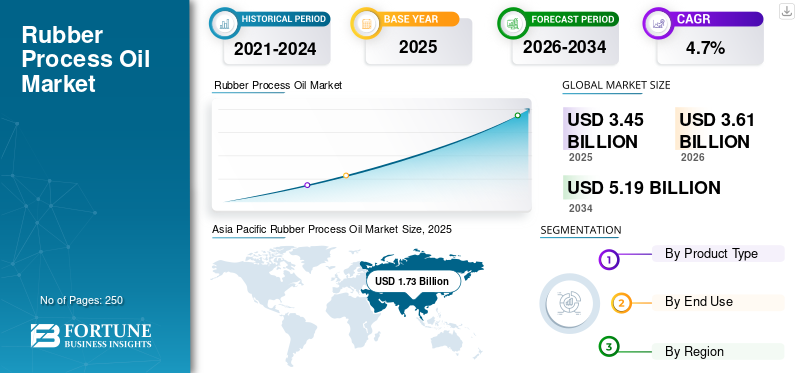

The global rubber process oil market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.61 billion in 2026 to USD 5.19 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the rubber process oil market with a market share of 83.76% in 2025.

Rubber process oils (RPOs) are essential compounding ingredients used in rubber formulations to improve elasticity, softness, filler dispersion, processability, and the overall performance of finished rubber products. They play a critical role in the manufacturing of tires, automotive rubber components, conveyor belts, hoses, footwear, seals, and other industrial rubber goods. These oils help reduce compound viscosity, enhance mixing efficiency, and improve physical properties in both natural and synthetic rubber applications. The growing demand for rubber process oils in the global market is primarily driven by steady tire production, rising consumption of automotive rubber parts, and increasing industrial activity across construction, transportation, and manufacturing sectors.

The market is led by integrated petroleum companies, specialty oil producers, and regional suppliers that maintain strong positions through broad product portfolios and supply capabilities across aromatic, naphthenic, paraffinic, and low-PAH grades. Key players such as Shell plc, TotalEnergies, Nynas AB, TotalEnergies SE, and Apar Industries maintain market presence through refining integration, distribution strength, and product development aligned with regulatory requirements. The competitive landscape is also shaped by the growing shift toward environmentally safer, regulation-compliant process oils, particularly in tire and high-performance rubber applications.

Download Free sample to learn more about this report.

Rubber Process Oil Market Key Takeaways

- 2025 Market Size: USD 3.45 Billion

- 2026 Market Size: USD 3.61 Billion

- 2034 Forecast Market Size: USD 5.19 Billion

- CAGR: 4.70% from 2026–2034

- Asia Pacific dominated the rubber process oil market with an 83.76% share in 2025.

- The naphthenic segment is projected to grow at a CAGR of 4.50% during 2026–2034.

- The consumer goods & footwear segment is projected to grow at a CAGR of 5.30% during 2026–2034.

Asia Pacific

Asia Pacific generated USD 1.73 billion in 2025 and is projected to reach USD 1.82 billion in 2026.

North America

North America reached USD 0.65 billion in 2025 and is projected to grow to USD 0.67 billion in 2026.

Europe

Europe reached USD 0.74 billion in 2025.

U.S.

The rubber process oil market is projected to reach USD 0.61 billion in 2026.

Japan

Strong automotive production and advanced rubber processing capabilities continue to support steady demand for rubber process oils.

Read More

RUBBER PROCESS OIL MARKET TRENDS

Growing Preference for High-Performance Process Oils to Favor Product Adoption

The global rubber process oil market is witnessing a clear transition toward low-polycyclic aromatic hydrocarbon (PAH) and environmentally compliant oils, driven by stringent regulatory frameworks, particularly in Europe and North America. Conventional distillate aromatic extracts (DAE) are increasingly being replaced by safer alternatives such as treated distillate aromatic extract (TDAE), mild extract solvates (MES), and naphthenic oils. This shift is further supported by evolving tire manufacturing requirements, where performance attributes such as low rolling resistance, improved wet grip, and enhanced durability are critical. High-performance process oils play a vital role in achieving these specifications by enabling better filler dispersion and compound uniformity. Additionally, sustainability initiatives by tire manufacturers and OEMs are accelerating the adoption of cleaner, higher-quality process oils. Therefore, the combined impact of regulatory compliance and performance-driven formulation is expected to favor the global adoption of advanced rubber process oils.

- Companies such as Nynas AB, Apar Industries, and TotalEnergies have already included low-PAH, hydrotreated, and high-performance rubber process oil grades in their product portfolios to address evolving regulatory and tire compounding requirements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Tire Manufacturing and Replacement Demand Supporting Market Growth

The global rubber process oil market growth is strongly supported by expanding tire manufacturing capacity and steady replacement demand across both developed and emerging economies. Increasing vehicle production, rising mobility needs, and improved road infrastructure are driving higher tire consumption worldwide. Additionally, the replacement tire segment continues to generate consistent demand due to wear and tear, particularly in commercial vehicles and high-usage transportation fleets. Rubber process oils are essential in tire compounding, where they enhance processability, flexibility, and durability of rubber compounds. Asia Pacific, led by China and India, remains a key market for tire production, driven by cost advantages and strong domestic demand. Therefore, continuous growth in tire production and aftermarket consumption is expected to drive sustained demand for rubber process oils over the forecast period.

- The shift toward specialized EV tires has a direct ripple effect on the market, increasing both the volume and the complexity of oil required in tire manufacturing, with RPO expected to experience significant growth in the foreseen period.

MARKET RESTRAINTS

Volatility in Feedstock Prices and Stringent Environmental Regulations May Affect Margin Stability

The rubber process oil market faces challenges due to fluctuations in feedstock prices and increasingly stringent environmental regulations governing product composition. As rubber process oils are derived from petroleum refining streams, their pricing is closely linked to crude oil price volatility, which directly impacts production costs and profit margins for manufacturers. Sudden price fluctuations can create uncertainty in procurement and pricing strategies, especially for small and mid-scale players. In addition, regulatory restrictions on the use of high-PAH aromatic oils, particularly in Europe under REACH regulations, are limiting the use of conventional products and requiring investment in cleaner alternatives. Compliance with such regulations often involves higher production costs and technological upgrades. Therefore, the combined pressure of raw material price instability and regulatory compliance is expected to challenge margin stability and operational efficiency across the market.

MARKET OPPORTUNITIES

Rising Demand for Non-Tire Automotive and Industrial Rubber Goods to Create Growth Opportunities in the Market

The global market is expected to offer promising opportunities driven by the rising use of non-tire automotive rubber goods and the expanding demand for industrial rubber products. In the automotive sector, rubber process oils are widely used in the production of seals, gaskets, hoses, weatherstrips, bushings, mats, and vibration-control components, where they improve flexibility, softness, and processing efficiency. As vehicle production increases and automotive systems become more component-intensive, demand for such rubber parts is also rising steadily. Beyond automotive applications, industrial rubber goods such as conveyor belts, molded goods, hoses, roofing membranes, and protective rubber components are gaining traction across construction, mining, manufacturing, and material handling sectors. These applications broaden the consumption base of rubber process oils beyond tires alone. Therefore, growing penetration in non-tire automotive and industrial rubber goods is expected to create new and diversified growth opportunities for the market.

Segmentation Analysis

By Product Type

TDAE Segment Dominates Due to Regulatory Compliance and Balanced Performance

Based on the product type, the market is segmented into TDAE, Naphthenic, MES, Paraffinic, RAE & TRAE, and others.

The TDAE segment accounted for the largest global market share in 2025, supported by its strong alignment with regulatory requirements and balanced performance characteristics in tire compounding. TDAE oils have lower PAH content than conventional aromatic oils while maintaining compatibility with elastomers, making them widely preferred in modern tire manufacturing. Their ability to provide good filler dispersion, processability, and durability has reinforced their adoption across high-volume tire applications, particularly in regions with strict environmental regulations.

The naphthenic segment is expected to grow at a CAGR of 4.5% from 2026 to 2034, driven by its excellent solvency, low-temperature flexibility, and compatibility with a wide range of rubber polymers. These oils are particularly suitable for industrial rubber goods and specialty applications where performance under varying environmental conditions is essential. Increasing use in adhesives, sealants, and non-tire rubber applications is supporting demand. Additionally, their relatively lower environmental impact compared to conventional aromatic oils is encouraging adoption.

The paraffinic segment is expected to grow at a CAGR of 4.2% from 2026 to 2034, driven by its high stability, low volatility, and excellent oxidation resistance. These oils are commonly used in applications requiring high purity and long-term performance stability, including certain industrial rubber goods and specialty formulations. However, their relatively lower compatibility with some rubber types compared to aromatic and naphthenic oils limits broader adoption in tire applications.

By End Use

Tyres Segment Leads Owing to High Volume Consumption in Rubber Compounding

Based on the end use, the market is segmented into tyres, industrial rubber goods, automotive components, consumer goods & footwear, and others.

To know how our report can help streamline your business, Speak to Analyst

The tyres segment accounted for the largest global rubber process oil market share in 2025, supported by its dominant consumption of rubber process oils in tire manufacturing. These oils play a critical role in enhancing processability, flexibility, and key performance properties, including rolling resistance, durability, and wear resistance. The large-scale production of passenger, commercial, and off-the-road tires across global markets continues to drive substantial demand. Additionally, the replacement tire segment provides consistent consumption due to regular wear and tear. Strong automotive production and expanding transportation needs further reinforce demand.

The industrial rubber goods segment is expected to grow at a CAGR of 4.9% from 2026 to 2034, driven by rising demand for conveyor belts, hoses, seals, and molded rubber components across industries such as mining, construction, and manufacturing. Increasing industrialization and infrastructure development are driving demand for durable, flexible rubber products. Rubber process oils enhance processing efficiency and performance characteristics in these applications. As industrial activities expand globally, particularly in emerging economies, demand for industrial rubber goods is expected to remain strong, supporting steady growth in this segment.

The consumer goods & footwear segment is expected to grow at a CAGR of 5.3% from 2026 to 2034, driven by rising demand for rubber-based footwear, mats, and household products, particularly in developing regions. Increasing urbanization, improving living standards, and growth in retail markets are supporting consumption. Rubber process oils contribute to product flexibility, comfort, and ease of manufacturing. Additionally, the expansion of the footwear industry and the increasing preference for durable, cost-effective materials are driving demand.

Rubber Process Oil Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa.

Asia Pacific

Asia Pacific Rubber Process Oil Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 1.73 billion, and is projected to grow to USD 1.82 billion by 2026. The region benefits from its position as a global hub for tire manufacturing and rubber goods production, driven by cost advantages, expanding automotive production, and rising industrial activity. Increasing infrastructure development, rising transportation demand, and the strong presence of rubber processing industries continue to sustain consumption. Additionally, rising demand for both tire and non-tire rubber applications, including industrial goods and automotive components, further reinforces the region’s leadership in the market.

China Rubber Process Oil Market

The Chinese market is estimated to value at USD 0.97 billion in 2026, accounting for approximately 27% of global revenues. Demand is supported by extensive tire production capacity, strong domestic automotive demand, and widespread use of rubber in industrial applications such as conveyor belts, hoses, and molded goods. Additionally, increased focus on high-performance, environmentally compliant rubber formulations is further driving demand.

To know how our report can help streamline your business, Speak to Analyst

India Rubber Process Oil Market

The India market is set to reach USD 0.19 billion in 2026, representing roughly 5% of global revenues. Demand is driven by expanding tire manufacturing capacity and growing automotive production. Increasing infrastructure development and industrialization are driving demand for industrial rubber goods such as hoses and belts. Additionally, rising consumption of two-wheelers and passenger vehicles is contributing to steady demand for rubber process oils in the country.

North America

North America remains a significant regional market, reaching USD 0.65 billion in 2025 and expected to rise to USD 0.67 billion in 2026. The region’s demand is primarily driven by replacement tire consumption and steady automotive production. Additionally, strong regulatory frameworks have accelerated the shift toward low-PAH and environmentally compliant process oils. Demand from industrial rubber goods and automotive components also contributes to market stability. The presence of established manufacturers and focus on high-performance materials further support regional growth.

U.S. Rubber Process Oil Market

The U.S. market is projected to hit USD 0.61 billion by 2026, accounting for approximately 17% of global revenues. Demand is supported by strong replacement tire consumption, steady automotive production, and significant use of rubber in industrial applications. Additionally, the growing preference for high-performance, compliant rubber process oils is shaping market demand.

Europe

Europe is expected to hit USD 0.74 billion in 2025, supported by strong regulatory-driven demand and advanced rubber processing industries. The region has been at the forefront of adopting low-PAH and environmentally compliant rubber process oils, particularly in tire manufacturing. Demand is sustained by automotive production, replacement tire consumption, and industrial rubber applications. Additionally, the presence of established automotive OEMs and strict environmental norms continues to influence product selection and innovation.

Germany Rubber Process Oil Market

The Germany market is projected to hit USD 0.19 billion in 2026, accounting for approximately 5% of global revenues. Demand is supported by the country’s strong automotive manufacturing industry and high use of rubber components such as seals, gaskets, hoses, and engineered parts. Germany also maintains steady consumption in tire-related and industrial rubber applications, where product quality and compliance remain important.

U.K. Rubber Process Oil Market

The U.K market is set to reach USD 0.09 billion in 2026, accounting for approximately 3% of global revenues. Demand is supported by steady consumption across automotive components, replacement tires, and industrial rubber applications. The market also benefits from ongoing demand for rubber-based products used in transportation, manufacturing, and infrastructure-related activities.

Latin America

Latin America accounted for a market size of USD 0.19 billion in 2025, supported by growing automotive production and increasing industrial activities. The region is witnessing rising demand for rubber process oils in tire manufacturing and industrial rubber goods. Infrastructure development and expansion of transportation networks are further contributing to market growth.

Brazil Rubber Process Oil Market

The Brazil market is expected to reach USD 0.08 billion in 2026, accounting for approximately 2% of global revenues. Demand is supported by the country’s automotive production base, replacement tire requirements, and growing use of industrial rubber goods across construction, mining, and manufacturing sectors.

Middle East & Africa

The Middle East & Africa accounted for a market value of USD 0.14 billion in 2025, supported by gradual industrialization and infrastructure development. Demand is primarily driven by increasing use of rubber in construction, transportation, and industrial applications. Growing automotive demand and the expansion of logistics and mining sectors are also contributing to market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Focus on Portfolio Upgradation and Geographic Expansion Shaping Competitive Dynamics

Competitive dynamics in the global industry are increasingly shaped by sustainability-led portfolio expansion, geographic footprint strengthening, and closer alignment with tire and industrial rubber manufacturers. Leading suppliers such as Nynas AB, TotalEnergies, Shell plc, Apar Industries, Panama Petrochem, and PSP Specialties are reinforcing their positions through product innovation, export expansion, and investment in specialty oil capabilities. Nynas’ development of its EVO range of tyre and rubber oils highlights the growing importance of lower-carbon, performance-oriented solutions worldwide. PSP Specialties has advanced its strategic positioning by developing bio-based process oils and expanding exports into new international markets. Panama Petrochem continues to strengthen its presence through investments in technology and regional infrastructure to enhance supply reach. Therefore, competitive advantage in the global market is increasingly defined by portfolio compliance, sustainability integration, and global supply capabilities rather than by conventional oil commodity supply alone.

LIST OF KEY RUBBER PROCESS OIL COMPANIES PROFILED

- Shell plc (U.K.)

- Repsol (Spain)

- Nynas AB (Sweden)

- TotalEnergies SE (France)

- Calumet, Inc. (U.S.)

- Cross Oil Refining & Marketing, Inc. (U.S.)

- ORGKHIM Biochemical Holding (Russia)

- APAR Industries Ltd. (India)

- Panama Petrochem Ltd. (India)

- Gandhar Oil Refinery Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025: PSP Specialties announced the development of a bio-based process oil for the rubber industry, designed to reduce reliance on fossil-derived oils while maintaining compatibility, processing efficiency, and user safety. The product was described as being in its final evaluation phase and targeted for commercial launch in 2026, signaling growing innovation in sustainable rubber process oils.

- February 2025: Nynas introduced its EVO concept across specialty oils, including products used in tyres and rubber, positioning it as a drop-in lower-carbon alternative. The company stated that most EVO products can deliver around 25% lower product carbon footprint without reformulation or re-approval, reflecting the market’s push toward lower-footprint rubber process oils.

REPORT COVERAGE

The global rubber process oil market analysis provides an in-depth study of market size & market forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.45 billion in 2025 and is projected to reach USD 5.19 billion by 2034.

In 2025, the market value stood at USD 1.73 billion.

Recording a CAGR of 4.7%, the market is slated to exhibit steady growth during the forecast period.

The tyres segment led in 2025.

Expanding tire manufacturing and replacement demand are expected to drive market growth.

Shell plc, TotalEnergies, Nynas AB, TotalEnergies SE, and Apar Industries are some of the prominent players in the market.

Rising shift toward low-PAH and growing preference for high-performance process oils in modern tire compounding to favor product adoption

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us