Seeds Market Size, Share & Industry Analysis, By Seed Type (Conventional Seeds, Genetically Modified Seeds, and Hybrid Seeds), By Crop Type (Cereals, {Corn, Wheat, Rice, and Others}, Oilseeds & Pulses {Soybean, Cotton, Canola, and Others}, Fruits & Vegetables {Solanaceae, Cucurbits, Leafy Vegetables, Citrus Fruits, Root & Bulb, Rosacea and Others}, and Others), By Cultivation Method (Protected and Open Field), and Regional Forecast, 2026–2034

(Offer valid till 15th Jul 2026)

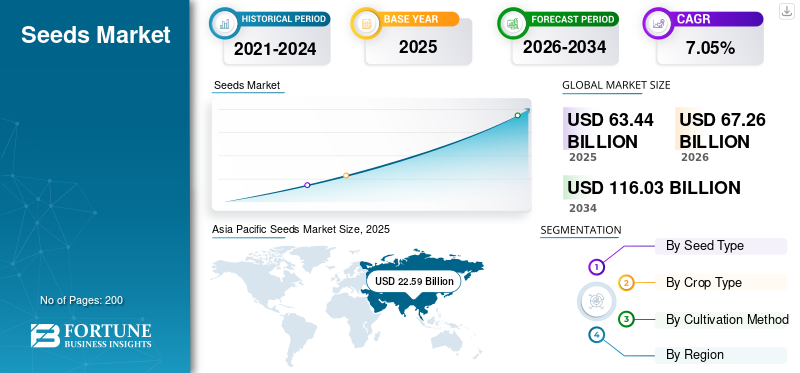

Seeds Market Size

The global seeds market size was valued at USD 63.44 billion in 2025. The market is projected to grow from USD 67.26 billion in 2026 to USD 116.03 billion by 2034, exhibiting a CAGR of 7.05% during the forecast period. Asia Pacific dominated the seeds market with a market share of 35.61% in 2025.

Seeds are fundamental agricultural inputs used for crop cultivation, serving as the primary carriers of genetic traits that determine yield potential, resistance to pests and diseases, and adaptability to varying climatic conditions. They are widely used across cereals, oilseeds, fruits, vegetables, pulses, and other crops, forming the backbone of global food production systems. The market includes conventional, hybrid, and genetically modified (GM) seeds, along with treated and coated variants that enhance germination, crop uniformity, and overall farm productivity.

The market is being driven by rising global food demand, increasing pressure on agricultural productivity, and the growing adoption of high-performance seeds such as hybrids and biotech varieties. Expanding commercial farming practices, supportive government initiatives for quality seed distribution, and advancements in seed treatment and breeding technologies are further strengthening market growth. However, factors such as stringent regulatory frameworks for GM seeds, high R&D costs, intellectual property concerns, and the prevalence of counterfeit seeds continue to influence market dynamics and innovation.

The industry is led by major players such as Bayer AG, Corteva Agriscience, Syngenta Group, BASF SE, Groupe Limagrain, KWS SAAT SE & Co. KGaA, and other regional seed manufacturers.

Download Free sample to learn more about this report.

Seeds Market Key Takeaways

- 2025 Market Size: USD 63.44 billion

- 2026 Market Size: USD 67.26 billion

- 2034 Forecast Market Size: USD 116.03 billion

- CAGR: 7.05% from 2026-2034

- Asia Pacific dominated the seeds market with a 35.61% share in 2025.

- Genetically modified seeds segment is projected to grow at a CAGR of 7.92% during 2026–2034.

- Fruits & vegetables segment is expected to grow at the fastest CAGR of 8.48% during the forecast period.

Asia Pacific

Asia Pacific led the market with USD 22.59 billion in 2025 and is the fastest-growing region globally.

North America

North America accounted for USD 16.63 billion in 2025, driven by large-scale commercial farming.

Europe

Europe reached USD 14.56 billion in 2025, supported by steady agricultural development.

U.S.

The market stood at USD 12.96 billion in 2025, driven by adoption of advanced seed technologies.

South America

The market reached USD 5.95 billion in 2025, supported by strong agricultural exports and expanding cultivation activities.

Read More

Seeds Market Trends

Growing Demand for Organic and Non-GMO Seeds to Change the Industry Outlook

The global seeds market is witnessing a structural shift toward organic and non-GMO seed adoption, driven by regulatory push, consumer awareness, and sustainable agriculture initiatives. Farmers are increasingly aligning seed choices with organic certification standards and export requirements, particularly in Europe and North America. This transition is reshaping seed production systems, encouraging the development of untreated, non-genetically modified, and region-specific seed varieties. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM (2025), global organic farmland exceeded 96 million hectares in 2024, growing steadily due to policy incentives and premium pricing for organic produce. This expansion directly increases demand for certified organic seeds, especially in cereals, oilseeds, and vegetables.

In the European Union, the European Commission’s Farm to Fork Strategy aims to convert 25% of agricultural land to organic farming by 2030, significantly accelerating demand for organic seed systems. Similarly, India’s National Programme for Organic Production (NPOP) and initiatives such as Paramparagat Krishi Vikas Yojana (PKVY) are supporting domestic organic seed usage.

On the industry side, Bayer AG, Syngenta Group, and Limagrain are expanding their organic and non-GMO seed portfolios, focusing on untreated seeds and biological resistance traits. This trend is gradually shifting the market from yield-maximization alone toward sustainability, traceability, and premium crop value.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rise of Seed Treatment Technologies to Enhance Crop Yield and Drive Market Growth

Seed treatment technologies are emerging as a critical driver in the seeds market growth, improving germination rates, pest resistance, and early-stage crop protection. These technologies include chemical treatments, biological coatings, and advanced polymer-based seed coatings that enhance nutrient uptake and stress tolerance. According to the Food and Agriculture Organization (FAO), global crop losses from pests and diseases account for up to 40% of agricultural production annually, underscoring the need for preventive measures such as treated seeds. Seed treatment enables targeted protection at the seed level, reducing the need for excessive pesticide application and improving cost efficiency for farmers.

The International Seed Federation (ISF) highlights that treated seeds can improve crop establishment rates by 10–20%, particularly in cereals and oilseeds. Governments are also promoting seed treatment as part of integrated pest management strategies. For instance, the Government of India’s Seed Mission programs emphasize the use of certified and treated seeds to improve productivity in staple crops such as rice and wheat.

Market Restraints

Rising Counterfeit Seeds May Hamper Market Growth

The proliferation of counterfeit and uncertified seeds remains a major restraint, particularly in developing markets where regulatory enforcement is inconsistent. Fake seeds not only reduce crop yields but also damage farmer trust and disrupt formal seed supply chains. According to reports from the Organization for Economic Co-operation and Development (OECD) and the EU Intellectual Property Office (EUIPO), counterfeit agricultural inputs, including seeds, account for a significant share of illicit trade in emerging economies.

In India and parts of Africa, local authorities frequently report cases of spurious seed distribution during peak sowing seasons. The Government of India’s Ministry of Agriculture has repeatedly flagged counterfeit seeds as a major issue affecting farmer income. Several state-level enforcement drives in 2024–2025 led to the seizure of large quantities of counterfeit hybrid seeds, particularly in the cotton and maize segments.

- Farmers using non-certified seeds often face yield losses of 15–30%, along with higher vulnerability to pests and climatic stress.

Market Opportunities

Adoption of Hybrid and GM Seeds to Change Industry Landscape

The adoption of hybrid and genetically modified seeds is creating a major opportunity in the global seeds market, as growers increasingly seek higher productivity, stronger resilience, and better profitability from limited arable land. Hybrid seeds are widely preferred for their high yield potential, crop uniformity, and stronger commercial performance, while genetically modified seeds offer additional traits such as herbicide tolerance, insect resistance, and stress tolerance. The rising adoption of these advanced seed varieties is especially visible in major crop type segments such as corn, soybean, cotton, and canola, where performance gains are more measurable and commercially valuable.

In parallel, improvements in biotechnology, trait stacking, and breeding science are supporting the development of GM seeds and hybrid products with better drought tolerance and climate adaptability. This is helping the industry move beyond traditional seeds toward more specialized, value-added solutions. According to the International Service for the Acquisition of Agri-biotech Applications (ISAAA, 2024 update), the global biotech crop area remains above 190 million hectares, with major adoption in soybean, maize, cotton, and canola. The U.S., Brazil, and Argentina continue to dominate GM seed adoption, while Asia is gradually expanding its footprint.

Hybrid seed penetration is also increasing in emerging markets, in India, hybrid maize, and vegetable seeds are witnessing strong adoption under government-supported productivity programs.

- The Indian Council of Agricultural Research (ICAR) reports that hybrid seeds can improve yields by 15–25% compared to conventional varieties.

SEGMENTATION ANALYSIS

By Seed Type

High-Yielding and Commercial Farming Practices Help Hybrid Seeds to Hold the Highest Share

On the basis of seed type, the market is segmented into conventional seeds, genetically modified seeds, and hybrid seeds.

The hybrid seeds segment dominated the market in 2025, valued at USD 27.54 billion. Hybrid seeds demand is driven by its superior yield potential, uniform crop quality, and greater resistance to biotic and abiotic stresses. They are extensively used in cereals, oilseeds, and vegetables, particularly in countries with intensive commercial farming such as the U.S., China, India, and Brazil. These seeds offer yield advantages of 15–30% compared to open-pollinated varieties, making them highly attractive for maximizing farm output and profitability.

Additionally, government-supported seed replacement programs and increasing farmer awareness regarding certified seeds are accelerating hybrid seed adoption. Major companies such as Corteva Agriscience, Bayer, and Syngenta are heavily investing in hybrid breeding programs, further strengthening product availability and innovation. The scalability of hybrid seeds across diverse agro-climatic conditions and their compatibility with modern farming practices are key factors supporting the leading market share.

Genetically modified seeds segment is projected to grow at the fastest CAGR of 7.92% during 2026–2034. This growth is supported by increasing demand for crop protection traits such as herbicide tolerance and insect resistance, especially in corn, soybean, and cotton. The commercial value of GM seed is also improving as farmers seek more reliable performance under climate stress, labor shortages, and weed pressure.

To know how our report can help streamline your business, Speak to Analyst

By Crop Type

Large Cultivation Base and Staple Crop Importance Help Cereals to be the Dominant Type of Crop

Based on crop type, the market is categorized into cereals, oilseeds & pulses, fruits & vegetables, and others.

The cereals segment led the global market in 2025, reaching USD 27.32 billion, supported by its vast cultivation area, strong food security relevance, and large-scale seed demand across both developed and emerging countries. Corn, wheat, and rice remain the most important cereal seed varieties in the global market, as they are grown extensively for food, feed, and industrial use. This broad production base creates strong and recurring demand for certified seeds, hybrids, and improved planting materials.

In addition, cereal-focused seed production receives strong policy support in many countries due to the strategic importance of staple crops in national agricultural systems. The segment also benefits from continuous breeding efforts aimed at improving high yield, drought tolerance, disease resistance, and regional adaptability. Since cereals form the foundation of large-scale open-field agriculture, major players continue to prioritize these crops in research, product development, and commercial expansion.

The fruits & vegetables segment is expected to grow at the fastest CAGR of 8.48% during the forecast period.

By Cultivation Method

Open Field Cultivation’s Higher Preference is Due to Extensive Use of Seeds in Large-Scale Farming Systems

Based on cultivation method, the market is classified into protected and open field.

The open field segment held the largest seeds market share in 2025, valued at USD 56.61 billion. Most conventional, hybrid, and genetically modified seeds are widely used in open-field farming, where scale, mechanization, and volume production are critical. Open-field agriculture remains especially important for staple crop type categories that require broad-acre planting and standardized seed production systems. The segment is also supported by continuous improvements in farm mechanization, irrigation access, and agronomic management, which enhance the value of improved seed varieties in large farming operations.

In the U.S., Brazil, India, and China, open-field farming remains central to grain and oilseed production, reinforcing long-term seed demand. Since major players allocate a large share of their commercial seed portfolios to broad-acre agriculture, open-field continues to hold the highest market share globally.

The protected cultivation segment is projected to grow at the fastest CAGR of 9.09% during the forecast period supported by increasing use of greenhouses, polyhouses, and controlled-environment systems for vegetables, fruits, and specialty crops. Protected farming encourages the use of premium seed varieties with better disease resistance, uniformity, and output potential. The rising adoption of high-value cultivation models is expected to make this segment an important future growth area for the market.

Seeds Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Seeds Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 16.63 billion in 2025 and is projected to grow at a CAGR of 5.27% (2026–2034). North America remains one of the key markets globally, supported by highly commercialized farming systems, strong private-sector breeding activity, and rapid technology penetration across major crop type categories. The region benefits from the rising adoption of premium seed varieties, especially in corn, soybean, cotton, and canola, where farmers prioritize high yield, crop uniformity, and operational efficiency. Demand is particularly strong for genetically modified seeds and hybrid materials that offer herbicide tolerance, insect resistance, and better stress management under broad-acre farming conditions.

In addition, the region has a well-developed ecosystem for trait innovation, testing, certification, and large-scale seed production, which supports continuous product commercialization. The presence of major players with strong R&D capabilities also strengthens product availability and farmer outreach. These factors continue to reinforce the region’s leadership in the global seed market size landscape. According to the USDA Economic Research Service (ERS, 2025), over 90% of corn, soybean, and cotton acreage in the U.S. is planted with genetically modified seeds, reflecting deep market penetration of GM seed technology.

U.S. Seeds Market

The U.S. market was valued at approximately USD 12.96 billion in 2025 and is expected to expand at a CAGR of 5.06% during the forecast period. The U.S. dominated North America, supported by its scale in commercial agriculture, deep integration of biotechnology, and broad farmer acceptance of advanced seeds across multiple crop type segments. The market is driven by the widespread use of hybrid corn, soybean, and cotton seeds designed for high yield, efficient weed control, and stable field performance. The country also leads in the use of genetically modified seeds, especially in row crops, where herbicide tolerance and pest resistance traits are now standard across much of the market. In parallel, the U.S. has one of the world’s strongest systems for breeding innovation, certified seed distribution, and large-scale seed production, which supports fast commercialization of new seed varieties. The strong presence of major players and data-driven farming practices further strengthens market demand. These dynamics are expected to keep the U.S. central to growth in the regional market. According to USDA data (2025), corn production exceeded 380 million metric tons, supported largely by hybrid and genetically modified seeds.

Europe

Europe is expected to grow steadily at a CAGR of 6.03% over the forecast period and achieved USD 14.56 billion in 2025. The region represents a technologically strong but regulation-shaped market, where demand is increasingly influenced by sustainability, varietal specialization, and climate adaptation. It remains more focused on hybrids and conventional seeds over the broad commercial penetration of genetically modified seeds. This has encouraged companies to invest in advanced breeding for disease resistance, quality traits, and drought tolerance within non-GM frameworks. Europe also benefits from strong seed certification systems, structured breeding programs, and diversified demand across cereals, oilseeds, vegetables, and forage crops.

Increasing organic farming to achieve greater sustainability in the agricultural sector drives industry growth. The European Commission (2025) reports that organic farming accounts for over 10% of EU agricultural land, increasing demand for conventional seeds. In addition, the region is home to several major players, including Groupe Limagrain, BASF SE, and KWS, which continue to strengthen innovation in hybrid and specialty seed varieties. These factors support Europe’s stable role in the global market.

Germany Seeds Market

Germany accounted for approximately USD 3.03 billion in 2025 and is one of the major markets in Europe due to its strong breeding infrastructure, high standards for certified planting material, and focus on performance-led farming systems. The country’s seed demand is supported by the widespread cultivation of cereals, rapeseed, and other major crops, with growers seeking stable yields, disease resistance, and adaptability to local agronomic conditions. Germany’s market is less about large-scale GM seed penetration and more about the deployment of advanced conventional seeds, hybrids, and specialized seed varieties developed through structured breeding programs. The country also benefits from a strong research environment and the presence of leading developers that invest in yield stability and drought tolerance. This makes Germany a strategically important market for premium seeds within Europe.

Asia Pacific

Asia Pacific reached USD 22.59 billion in 2025 and is the leading and fastest-growing region, with a projected 8.56% CAGR during the forecast period. It is one of the most dynamic regions in the global market, supported by rising food demand, a large farming base, and increasing modernization of agriculture. According to the Food and Agriculture Organization, Asia accounts for over 50% of global agricultural production annually, driving strong demand for seeds. The region is witnessing the rising adoption of improved seeds across major crop type segments, including rice, corn, vegetables, cotton, and oilseeds. Demand is being driven by the need for high yield, greater disease resistance, and stronger climate resilience under increasingly variable weather conditions. Compared with mature markets, Asia Pacific still has significant room for seed replacement and yield improvement, creating long-term growth potential for both hybrids and advanced conventional seeds. Several countries are also strengthening domestic seed production to improve food security and reduce dependence on imports. As a result, Asia Pacific continues to gain strategic importance in the global market.

China Seeds Market

China was valued at USD 6.99 billion in 2025 driven by strong government support for agricultural modernization and the increasing adoption of hybrid and genetically modified seeds across key crop categories. The country is focusing on improving domestic seed production capabilities to reduce reliance on imports and strengthen food security. Large-scale cultivation of corn and rice is driving demand for high-performance seed varieties with higher yields and greater resilience.

India Seeds Market

The Indian market reached USD 5.70 billion in 2025 and is expanding due to the rising adoption of hybrid seeds in cereals, oilseeds, and vegetables, supported by government-backed agricultural programs. The country has a large and diverse crop type base, creating demand for region-specific seed varieties. Increasing focus on improving farm productivity and farmer income is accelerating the shift from conventional seeds to hybrids.

South America and the Middle East & Africa

South America accounted for USD 5.95 billion in 2025, growing at a CAGR of 7.31% over the forecast period. South America is one of the most commercially important markets globally due to its scale in export-oriented agriculture and extensive use of biotechnology in broad-acre crops. The region’s growth is strongly driven by soybean, corn, and cotton cultivation, where genetically modified seeds have become central to field productivity and farm management. Demand is particularly high for GM seed products with herbicide tolerance, insect resistance, and improved stress performance, as these traits support large-scale cultivation and operational efficiency. The region also benefits from strong farm mechanization, large landholdings, and a commercial mindset that favors adopting premium seed when performance gains are visible. In addition, continued expansion in row-crop acreage supports recurring demand for improved seed varieties and higher-value trait packages.

The Middle East & Africa was valued at USD 3.71 billion in 2025 and is expected to expand at a CAGR of 8.07% over the projected timeframe. The market is evolving steadily, supported by growing efforts to improve agricultural productivity amid water stress, land constraints, and a changing climate. Unlike heavily industrial row-crop regions, growth in this region is increasingly linked to the need for resilient seed varieties that can support output under difficult agronomic conditions. Demand is strengthening for seeds with drought tolerance, heat resilience, and better establishment rates in both field crops and horticulture. Governments and agricultural agencies across the region are also encouraging more efficient use of inputs, including certified planting material, to reduce dependence on imports and improve food security.

South Africa Seeds Market

The South African market was valued at approximately USD 1.12 billion in 2025 and is projected to grow at a CAGR of 9.74% from 2026 to 2034. South Africa is the leading market in the region due to its more developed commercial farming base and broader use of improved crop genetics. The country’s demand is supported by the maize, sunflower, soybean, and horticultural crop segments, where farmers increasingly seek high yields, consistent quality, and field resilience. South Africa is also one of the more established adopters of genetically modified seeds in Africa, particularly in maize and soybean, where GM seed use supports better weed and pest management. At the same time, demand for drought-tolerant seeds is increasing as weather volatility and water stress affect production planning. These factors support the country’s position as the regional leader in formal seed demand and commercial seed production.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focused on Innovation, Portfolio Expansion, and Strategic Partnerships to Gain Competitive Edge

The global seeds market is fragmented, characterized by a few dominant multinational corporations and a large number of regional and local seed producers. Leading companies such as Bayer AG, Corteva Agriscience, Syngenta Group, BASF SE, Groupe Limagrain, KWS SAAT SE & Co. KGaA, and Sakata Seed Corporation hold a significant share of the global market, supported by their strong portfolios in hybrid and genetically modified seeds across multiple crop type segments. These major players benefit from extensive research and development capabilities, advanced breeding technologies, and well-established seed production and distribution networks.

Key Players in the Seeds Market

|

Rank |

Company Name |

|

1 |

Bayer AG |

|

2 |

Corteva Agriscience |

|

3 |

Syngenta Group |

|

4 |

BASF SE |

|

5 |

Groupe Limagrain |

List of Key Seeds Companies Profiled

- BASF SE (Germany)

- Bayer AG (Germany)

- Corteva Agriscience (U.S.)

- Syngenta Group (Switzerland)

- Groupe Limagrain (France)

- KWS SAAT SE & Co. KGaA (Germany)

- Sakata Seed Corporation (Japan)

- DLF Seeds A/S (Denmark)

- Advanta Seeds (India)

- Royal Barenbrug Group (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- April 2026: BASF SE, one of the leading crop seed manufacturers, invested nearly USD 43.29 million through its vegetable seeds business to modernize and expand its seeds processing facility in Nunhem, the Netherlands.

- February 2026: Syngenta Group, one of the global leading manufacturers of agricultural products, launched X-Terra® hybrid wheat seeds across Europe, including the U.K, France, and Germany. SY Sphynx and SY Xanthis will be the first X-Terra® hybrid wheat products to be available in France.

- December 2025: BASF SE acquired one of the key players in the Indian vegetable seeds sector, Nunhems India Pvt. Ltd. The acquisition assists the company in expanding its presence in the regional market.

- November 2025: Bayer AG, a global agriculture company, introduced genetically modified soybean varieties Intacta 5+, which offer tolerance to five herbicides and protection against the main caterpillar species that damage soybean crops in Brazil.

- January 2025: Corteva Agriscience, an American multinational agriculture company, launched 27 new grain, corn, and silage corn hybrids, including PowerCore® Ultra Enlist® corn products. These products feature improved corn rootworm (CRW) resistance and flexible weed control.

REPORT COVERAGE

The report analyzes the market in depth and highlights key aspects, including market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. In addition, the research report provides insights into the global market and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.05% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Seed Type

|

|

By Crop Type

|

|

|

By Cultivation Method

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 63.44 billion in 2025 and is anticipated to reach USD 116.03 billion by 2034.

At a CAGR of 7.05%, the global market will exhibit steady growth over the forecast period.

By seed type, the hybrid seeds segment led the market in 2025.

Asia Pacific held the largest market share in 2025.

Rise of seed treatment technologies to enhance crop yield to drive market growth.

Bayer AG, Corteva Agriscience, Syngenta Group, BASF SE, Groupe Limagrain, KWS SAAT SE & Co. KGaA, and Sakata Seed Corporation are the leading companies.

Growing demand for organic and non-GMO seeds is the current market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us