Satellite Docking System Market Size, Share & Industry Analysis, By Product Type (Active Docking System (ADS) (Structural Docking Interface, Grappel Interface, and Others) and Passive Docking System), By Mission (On-orbit Servicing, Refueling, Life Extension, In-Space Assembly, and Others), By Orbit (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Earth Orbit (GEO)), By End User (Commercial, Government, Military, and Research), and Regional Forecast, 2026-2034

Satellite Docking System Market Size and Future Outlook

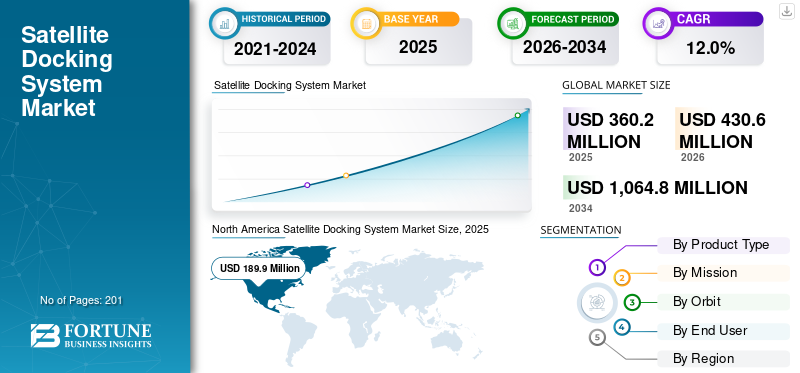

The global satellite docking system market size was valued at USD 360.2 million in 2025. The market is projected to grow from USD 430.6 million in 2026 to USD 1,064.8 million by 2034, exhibiting a CAGR of 12.0% during the forecast period. North America dominated the satellite docking system market with a market share of 52.44% in 2025.

Satellite docking systems enable precise in-orbit alignment, capturing, and rigidization of satellites using advanced sensors, robotics, and actuators to facilitate servicing, assembly, or deorbiting operations. These systems, exemplified by ISRO's SpaDeX mission, integrate laser rangefinders, proximity sensors, and autonomous navigation for reliable low-speed connections in space environments. The global market for satellite docking system is experiencing robust growth, fueled by the proliferation of mega-constellations, rising demand for in-orbit satellite servicing and refueling, and expanding space debris mitigation initiatives requiring precise orbital maneuvers.

- For instance, in December 2025, Redwire Corporation was awarded an eight-figure contract to provide two International Docking System Standard (IDSS)-compliant docking systems for The Exploration Company's Nyx spacecraft, supporting autonomous rendezvous and docking capabilities.

Key players such as Redwire Corporation, Northrop Grumman Corporation, Airbus Defence and Space, Lockheed Martin Corporation, and Starfish Space are prioritizing innovations like Automated Rendezvous and Docking (AR&D) technologies for autonomous operations, magnetic and electrodynamic capture systems for non-contact docking, and modular interfaces compatible with diverse satellite architectures.

Download Free sample to learn more about this report.

Satellite Docking System Market KEY TAKEAWAYS

- 2025 Market Size: USD 360.2 million

- 2026 Market Size: USD 430.6 million

- 2034 Forecast Market Size: USD 1,064.8 million

- CAGR: 12.0% from 2026–2034

- North America dominated the satellite docking system market with a 52.44% share in 2025.

- The passive docking system segment is projected to grow at an 11.1% CAGR during the forecast period.

- The in-space assembly segment is projected to grow at a 15.3% CAGR during the forecast period.

Asia Pacific

Asia Pacific reached USD 69.4 million in 2025, driven by rapid satellite constellation deployments and expanding national space programs.

North America

North America reached USD 189.9 million in 2025, supported by strong NASA and DoD funding and growing commercial space activities.

Europe

Europe is projected to grow at a CAGR of 12.2% from 2026–2034, driven by satellite servicing initiatives and space debris mitigation programs.

U.S.

The U.S. market is driven by leading commercial space companies, advanced on-orbit servicing technologies, and strong government support.

Japan

Japan reached USD 19.6 million in 2025, supported by commercial LEO satellite initiatives and advancements in satellite servicing technologies.

Read More

SATELLITE DOCKING SYSTEM MARKET TRENDS

Shift toward Autonomous Docking System is a Prominent Trend Observed in the Market

Rapid shift toward autonomous docking solutions is reshaping the satellite docking market as space agencies and commercial operators prioritize in-orbit sustainability amid growing orbital congestion and debris risks. Traditional manual docking maneuvers face scalability challenges due to human dependency and precision limitations, driving adoption of fully autonomous systems that enable reliable rendezvous without ground intervention. There is rise in development of autonomous docking to support commercial space stations in low Earth orbit (LEO). Such advancements to enhance mission safety, and reduce operational costs are significant trends in the market during the forecast period.

- For instance, in September 2025, Northrop Grumman successfully demonstrated autonomous rendezvous and docking of its Cygnus spacecraft with Starlab Space Station's port in its specialized lab.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Proliferation of Mega-Constellations and Orbital Sustainability Mandates To Drive Market Growth

The proliferation of mega-constellations drives the market by necessitating scalable on-orbit maintenance solutions. Operators like SpaceX with Starlink and Amazon's Kuiper are launching thousands of satellites into LEO, creating dense orbital environments that amplify collision risks and debris generation. Docking systems enable automated refueling, repairs, and deorbiting, allowing individual satellites to be serviced rather than replaced. This reduces launch cadences and costs, as maintaining satellite fleets becomes economically viable only through life extension. Orbital sustainability mandates further accelerate adoption, with regulations from FCC, ESA, and ITU requiring operators to demonstrate end-of-life disposal plans which drives market growth.

MARKET RESTRAINTS

High Development Costs to Limit Market Expansion

High development and qualification costs for these systems significantly restrain market growth, as designing reliable rendezvous, capture, and berthing mechanisms demands extensive R&D investments exceeding tens of millions per program. These systems must undergo rigorous on-ground simulations, vibration testing, and in-orbit demonstrations to achieve the sub-millimeter precision required for zero-gravity operations, creating substantial financial barriers for smaller operators and new market entrants. Moreover, the lack of standardized docking interfaces across legacy satellites increases customization expenses, limiting scalability for commercial mega-constellations which limit the market expansion.

MARKET OPPORTUNITIES

Increasing Demand for Sustainable Space Operations To Open New Growth Prospects for the Market

The growing demand for sustainable space operations is putting the market on growth trajectory, enabling critical orbit services. Satellite docking systems allow spacecraft to physically connect in orbit, facilitating refueling to extend satellite lifespans beyond their original design limits. This reduces the frequency of costly new launches, conserving resources and launch vehicle capacity. Repair functions, such as component replacement or fixing malfunctions, become feasible through docking, minimizing total mission failure rates. Increased investments from companies such as Northrop Grumman and startups such as Orbit Fab is propelling the market growth. The docking systems are necessary as they provide the precise physical interface and guidance navigation and control mechanisms required for extending spacecraft life and reducing orbital congestion.

- For instance, in October 2025, UARX Space announced launch of its OSSIE orbital transfer vehicle in 2026 equipped with Dawn Aerospace's Docking and Fluidic Transfer (DFT) Port, enabling Europe's first in-orbit refueling capability as part of the scalable Loop Network.

In addition, as mega-constellations such as Starlink expand, docking systems become essential for scalable, eco-friendly maintenance driving the satellite docking system market growth during the forecast period.

MARKET CHALLENGES

Lack of Industry Standardization to Act as a Challenge for the Market Growth

A major market challenge in the market demand is the absence of universal design and interface standards across manufacturers. Without standardized docking mechanisms, service satellites cannot reliably connect to diverse target satellites from different builders, limiting interoperability for on-orbit tasks like refueling or repair. This forces developers to create proprietary systems tailored to specific missions, escalating R&D costs and delaying commercialization.

Segmentation Analysis

By Product Type

ADS’s Autonomous Precision and Adaptability Propels their Leading Share in the Market

Based on product type, the market is divided into Active Docking System (ADS) and passive docking system.

The active docking system segment holds the largest satellite docking system market share due to their autonomous precision and adaptability across diverse orbital missions. The systems are independently having in-built sensors and thrusters to connect satellites precisely in space. They handle varying speeds and positions, making them ideal for different orbits which drives their demand.

- For instance, in March 2024, NASA and SpaceX successfully tested Starship HLS's active docking system derived from Dragon 2's flight-proven design that extends docking probes to mechanically capture Orion or Lunar Gateway during crew transfers in lunar orbit.

Passive docking system segment is anticipated to rise with a steady long term growth of 11.1% over the forecast period.

By Mission

Economic Imperatives Boosts The On-Orbit Servicing Segment Growth

By mission, the market is segmented into on-orbit servicing, refueling, life extension, in-space assembly, and others.

On-orbit servicing segment led the market in 2025. The segment’s expansion is fueled by economic imperatives to extend satellite lifespans amid rising launch costs. Docking enables refueling, repairs, and upgrades, slashing replacement expenses while complying with debris mitigation mandates from FCC and ESA. In addition, the advancements in docking systems are primarily driven by the explosive growth of on-orbit servicing requirements across commercial, government, and military applications, which drives segment growth.

- For instance, in December 2025, Astroscale secured U.S. Patent No. 12,479,603 B2 for a novel “Method and Device for Capture of Tumbling Space Objects,” using an empty docking volume and center-of-mass control to synchronize with spinning satellites without burning fuel.

In-space assembly segment is projected to grow at a fastest growth rate of 15.3% over the forecast period.

By Orbit

Deployments Of Mega-Constellation And LEO’s Low Upfront Costs Positioned LEO in Primary Position

By orbit, the market is segmented into Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Earth Orbit (GEO).

Low Earth Orbit (LEO) segment held the largest market share in 2025. The segment growth is increasing owing to surge in mega-constellation deployments. Rise in collision risks in crowded altitudes enable development of docking systems for facilitating rapid deorbiting and maintenance. In addition, LEO's servicing economics remain unviable in higher orbits due to lower asset density and natural longevity, positioning LEO as the primary commercial viability threshold for docking technology deployment.

Medium Earth Orbit (MEO) segment to experience steady CAGR of 11.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Commercial End User Dominated Owing to Private Sector Investments and Continuous Need for In-Orbit Maintenance

Based on end user, the market is segmented into commercial, government, military, and research.

The commercial segment dominated the market in 2025. The segment is driven by substantial private sector investments and a strategic emphasis on achieving swift returns on investment. These operators, managing extensive broadband and Earth observation constellations, rely on docking technologies to ensure continuous service revenue through efficient on-orbit maintenance and life extension.

The government segment is expected to grow with a steady growth rate of 11.6% over the forecast period.

Satellite Docking System Market Regional Outlook

By geography, the market is studied across North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Satellite Docking System Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the satellite docking system market in 2025 with a valuation of USD 189.9 million, expected to touch USD 226.1 million by 2026, propelled by substantial NASA and DoD funding alongside significant private ventures. North America has established satellite industry anchored by SpaceX, Northrop Grumman, and emerging servicers targeting Starlink-scale operations. Capacity expansions in commercial constellations and defense reconnaissance fleets prioritize docking for rapid replenishment and debris compliance. The players in the industry are focused on development and testing of docking system to establish a universal docking standard that eliminates the need for proprietary adapters on every spacecraft.

- For instance, in December 2025, SpaceWorks Enterprises announced successful ground testing of its FuseBlox docking interface with Rogue Space Systems, demonstrating mechanical connection, data transfer, and power transmission between simulated spacecraft and cargo container.

U.S. Satellite Docking System Market

Based on North America’s strong contribution and the U.S. dominance within the region, Leading U.S. firms drive innovation in on-orbit servicing for mega-constellations and national security payloads, supported by advanced test facilities and regulatory frameworks favoring commercial space initiatives.

Europe

Europe is projected to record a growth rate of 12.2% during 2026 to 2034, exhibiting robust growth in the market. Major hubs advance servicer fleets to support Copernicus Earth observation continuity and IRIS broadband ambitions while adhering to stringent EU Space Debris Mitigation guidelines. Regional expansion aligns with collaborative efforts to counter U.S. dominance through interoperable docking standards.

U.K Satellite Docking System Market

The U.K. market in 2025 was valued around USD 18.5 million, representing roughly 5.1% of global market revenues.

Germany Satellite Docking System Market

Germany market reached approximately USD 25.5 million in 2025, equivalent to around 7.1% of global market sales.

Asia Pacific

Asia Pacific market reached USD 69.4 million in 2025. The market is driven by rapid satellite constellation deployments and national space ambitions. China leads with state-backed on-orbit servicing for BeiDou navigation and remote sensing fleets, complemented by India's ISRO advancements in debris removal technologies. The countries in the region are developing docking systems for extension of satellite lifespans through refueling/repairs, remove orbital debris to meet regulations. Japan and South Korea bolster the regional growth momentum through commercial LEO broadband initiatives. For instance, in January 2026, OrbitAID Aerospace launched AayulSAT aboard ISRO's PSLV-C62, deploying India's inaugural commercial satellite docking and refueling system using the patented SIDRP interface for propellant, power, and data transfer.

Japan Satellite Docking System Market

The Japan market in 2025 touched around USD 19.6 million, accounting for roughly 5.4% of global market revenues.

China Satellite Docking System Market

China’s market is projected to be one of the largest, with 2025 revenues reaching around USD 26.8 million, representing roughly 7.4% of global market sales.

India Satellite Docking System Market

The India market in 2025 is estimated at around USD 10.6 million, accounting for roughly 2.9% of global market revenues.

Rest of the World

The Rest of the World market registers modest yet steady growth valuating at USD 16.6 million in 2025, the market is driven by support from UAE's growing space sector investments and focus on regional Earth observation maintenance. Latin American operators explore docking for GEO communications satellites. Growth is further accelerated by international collaborations to build interoperable systems, addressing orbital sustainability challenges.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Are Offering Enhanced Reliable Autonomous Services, Bolstering Their Positions

The global satellite docking system market comprises established aerospace contractors and specialized orbital servicing providers offering reliable capture mechanisms, navigation software, and modular servicing systems for both commercial and government applications. Market leaders focus on autonomous approach-and-capture technologies, propellant transfer systems, and standardized docking interfaces compatible with diverse satellite designs.

- For instance, in May 2024, Sierra Space announced collaboration with IHI Aerospace and Kanematsu Corporation to integrate a Japanese passive docking system (PDS) into its commercial space station, compliant with International Docking System Standard (IDSS) for secure spacecraft connections including Dream Chaser spaceplane.

Prominent companies including Northrop Grumman, Orbit Fab, and Astroscale deliver validated solutions through NASA flight tests and ESA demonstration missions. Current developments in AI-supported navigation, efficient refueling capabilities, and common adapter standards support the transition from mission-specific servicers to scalable platforms for mega-constellation maintenance.

LIST OF KEY SATELLITE DOCKING SYSTEM COMPANIES PROFILED

- Boeing (U.S.)

- Northrop Grumman (U.S.)

- Redwire Space NV (Belgium)

- SENER (Spain)

- Astroscale (Japan)

- Orbit Fab (U.S.)

- Starfish Space (U.S.)

- Lockheed Martin Corporation (U.S.)

- ClearSpace SA (Switzerland)

- Sierra Space (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Redwire Corporation signed an eight-figure agreement with The Exploration Company (TEC) to supply two IDSS-compliant International Berthing and Docking Mechanisms (IBDM) for TEC's reusable Nyx spacecraft, enabling autonomous rendezvous and docking for sustainable orbital operations.

- October 2025: OrbitAID Aerospace (India) & Indo-Australian Space MAITRI program, OrbitAID won MAITRI support to develop and deploy India’s in-orbit docking and refuelling interface (SIDRP).

- July 2025: Mitsubishi Heavy Industries & Sierra Space won a contract to deliver ISS spacecraft docking hardware, including a Passive Common Berthing Mechanism (PCBM) and related components for future JAXA missions.

- May 2025: AFWERX/SpaceWERX & Enduralock, Enduralock received a USD 1.25 million Phase II award (FA8649-25-P-0301) to develop a universal satellite docking system featuring mechanical linkage.

- January 2025: ISRO successfully docked two small spacecraft, SDX01 Chaser and SDX02 Target, marking India as the fourth nation to master orbital docking after multiple delays from the December 30th

- August 2024: S. Space Force (SSC) & Orbit Fab, SSC designated Orbit Fab’s RAFTI refueling port as an accepted refueling interface, a standardized dock-to-refuel port intended to be integrated on future satellites.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.0% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product Type, By Mission, By Orbit, By End User, and Region |

| By Product Type |

|

| By Mission |

|

| By Orbit |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 360.2 million in 2025 and is projected to reach USD 1,064.8 million by 2034.

In 2025, the market value stood at USD 189.9 million.

The market is expected to exhibit a CAGR of 12.0% during the forecast period.

By orbit, the Low Earth Orbit (LEO) segment is expected to lead the market.

Proliferation of mega-constellations and orbital sustainability mandates are driving market expansion.

Northrop Grumman (U.S.), Lockheed Martin Corporation (U.S.), Astroscale (Japan), and Orbit Fab (U.S.), are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 201

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us