Satellite Ground Station Market Size, Share & Industry Analysis, By Offering (Hardware, Software, and Ground Station as a Service [GSaaS]), By Hardware Sub-Segment (Antenna Systems, Tracking Equipment, Receivers & Transmitters, Ground Station Terminal, and Others), By Function (Telemetry, Tracking & Command (TT&C), Data Reception & Processing, Communication & Backhaul, and Network Management & Integration), By Frequency Band (C Band, Ku Band, Ka Band, S Band/X Band, Others), By Orbit (LEO, MEO, and GEO), By Application, By Platform, By End User, and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

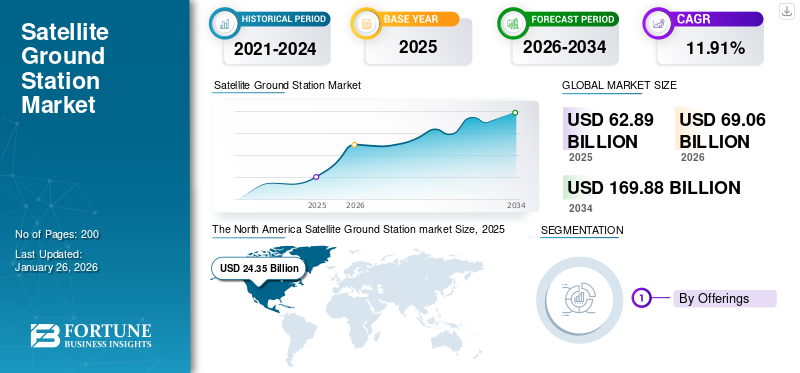

Satellite Ground Station Market Size and Future Outlook

The global satellite ground station market size was valued at USD 62.89 billion in 2025. The market is projected to grow from USD 69.06 billion in 2026 to USD 169.88 billion by 2034, exhibiting a CAGR of 11.91% during the forecast period.North America dominated the global market with a share of 38.72% in 2025.

A satellite ground station is a crucial terrestrial facility that enables communication between satellites in orbit and users or control centers on Earth. These stations are equipped with advanced antennas, receivers, transmitters, and control systems. Ground stations are designed for various applications such as satellite communication, Earth observation, navigation, military operations, space research, and others. They are deployed in various settings such as dedicated space agency facilities, defense installations, mobile units, and commercial sites, and are essential for receiving, processing, and relaying large volumes of satellite data.

Leading key players in the market, such as Kratos Defense Security Solutions, Kongsberg Satellite Services (KSAT), General Dynamics Mission Systems, Gilat Satellite Networks, and Airbus Defence and Space, are focusing on developing advanced and cost-effective ground station solutions with high reliability and automation. These firms are integrating cloud-based architectures, software-defined networking, and AI-driven signal management to enhance operational flexibility and reduce latency. In addition, there is a rise in building advanced ground stations to enhance connectivity service is expected to drive the satellite ground station market demand. For instance, in October 2025, Amazon was granted permission to build satellite ground station infrastructure in Cork, Ireland, for its Project Kuiper venture. This new facility will support Amazon's effort to expand its satellite broadband network.

Download Free sample to learn more about this report.

Satellite Ground Station Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 62.89 billion

- 2026 Market Size: USD 69.06 billion

- 2034 Forecast Market Size: USD 169.88 billion

- CAGR: 11.91% from 2026–2034

- North America dominated the satellite ground station market with a 38.72% share in 2025.

- The hardware segment accounted for the largest 51.51% market share in 2025.

- The Low Earth Orbit (LEO) segment is projected to hold a 52.18% share in 2026.

North American

Valued at USD 24.35 billion in 2025 and projected to reach USD 26.70 billion in 2026.

Europe

Reached USD 12.36 billion in 2025 and is expected to grow to USD 13.63 billion in 2026.

Asia Pacific

Stood at USD 16.30 billion in 2025 and is projected to reach USD 18.05 billion in 2026.

U.S.

The market is projected to reach USD 22.25 billion in 2026.

Japan

The market is projected to reach USD 2.61 billion in 2026.

Read More

Regulatory Support & Initiatives for Expansion of Satellite Ground Station Infrastructure:

Regulatory support and initiatives are playing a crucial role in accelerating the expansion of satellite ground station infrastructure globally. Governments and space agencies are creating streamlined licensing frameworks, promoting public-private partnerships, and developing policies that encourage private sector investment in ground station setups.

- For instance, in July 2025, the U.S. Federal Communications Commission (FCC) proposed a new order to streamline processes for space stations and earth stations, aimed especially at boosting the Ground-Station-as-a-Service (GSaaS) model.

In addition, countries across the world are introducing rules to tighten security and data sovereignty, requiring satellite operators to invest in local ground-segment capabilities. This is expected to drive increased demand for locally manufactured ground station equipment and infrastructure.

- For instance, in May 2025, as part of its “Make in India” and space security push, India now requires satellite communication operators to source at least 20% of their ground infrastructure equipment locally within five years of launching in the country.

Such developments are strengthening satellite ground infrastructure through cooperative and regulatory efforts.

MARKET DYNAMICS

MARKET DRIVERS:

Rise in Deployment of LEO Satellites to Propel Market Growth

The rising deployment of Low Earth Orbit (LEO) satellite constellations is a significant driver for the market. As companies and governments launch a large number of small satellites in LEO, the demand for satellite ground stations capable of tracking, communicating with, and managing these rapidly moving satellites increases dramatically. This has led to an increase in the need for globally distributed ground stations to support the rising number of LEO satellites.

- For instance, in February 2025, Globalstar announced plans to install around 90 new Earth station antennas across 35 gateway sites in 25 countries to support its next-generation LEO constellation.

Such developments highlight that the rapid proliferation of LEO systems is driving the expansion of the satellite communications ecosystem.

MARKET RESTRAINTS:

High Infrastructure and Maintenance Costs to Restrict Market Expansion

The high infrastructure and maintenance costs of ground stations remain a major restraint on market expansion. Building and operating advanced RF systems, large antenna arrays, and mission control facilities requires capital investment and ongoing operational expenditure. These costs are further increased by the need for redundant systems, secure network connectivity, and environmental hardening in remote or harsh locations. Smaller operators may find it financially challenging to match the scale and technology sophistication of global providers. However, there are initiatives that help lower administrative barriers, although the fundamental cost of equipment, energy, and technical expertise remains high.

MARKET OPPORTUNITIES:

Integration of AI and Automation in Ground Operations to Present Key Market Opportunities

The increasing adoption of artificial intelligence (AI) and automation presents a major opportunity for efficiency and innovation in ground station operations. AI algorithms can optimize satellite scheduling, automate telemetry and tracking tasks, and predict maintenance needs to minimize downtime. Automation also enables operators to manage multiple satellite networks simultaneously while reducing human intervention and error. The integration of AI into ground control systems is expected to enhance scalability, reliability, and responsiveness.

SATELLITE GROUND STATION MARKET TRENDS

Emergence of Digitalization, Automation, and Remote Operations is a Significant Satellite Ground Station Market Trends

A key emerging trend in the satellite ground station market is the transition toward optical and hybrid communication systems. Traditional RF-based ground stations are increasingly being complemented by laser communication links, which offer higher data throughput, enhanced security, and reduced latency. Optical systems also enable more efficient communication with the growing number of high-bandwidth LEO satellites. However, they require advanced signal stabilization and atmospheric compensation technologies.

- For instance, in March 2025, Cailabs unveiled its Tilba-L10 optical ground station, designed to maintain stable laser communication links with LEO satellites even under turbulent atmospheric conditions.

Such developments and innovations reflect a broader industry movement toward hybrid architectures that combine RF and optical capabilities. As optical technology matures, these systems are expected to redefine the design and performance standards for future ground station networks.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Spectrum Coordination and Regulatory Complexity to Hamper Market Growth

Spectrum coordination and complex regulatory frameworks continue to pose significant challenges for the satellite ground station market. Operators must secure frequency licenses and comply with regulations across multiple jurisdictions, often facing long approval timelines. Managing interference, ensuring compliance with international standards, and coordinating frequencies among LEO, MEO, and GEO systems add further complexity. These challenges slow infrastructure deployment and increase administrative costs. The lack of unified frequency management continues to challenge industry growth.

Segmentation Analysis

By Offering

Expansion of Global Satellite Networks and Infrastructure Modernization Fueled the Growth of Hardware Segment

On the basis of offering, the market is classified into hardware, software, and Ground Station as a Service (GSaaS). The hardware segment is further segmented into antenna systems, tracking equipment, receivers & transmitters, ground station terminal, and others.

The hardware segment accounted for the largest satellite ground station market share of of 51.51% in 2025. The segment’s growth is attributed to the demand for antennas, RF chains, transceivers, and tracking systems, which form the core physical layer of every ground station. Additionally, long-term service contracts for hardware upgrades, maintenance, and calibration ensure steady revenue streams for suppliers. The continued development of advanced, compact, and electronically steerable antennas further supports the growth of this segment.

- For instance, in October 2025, Galileo R&D announced successful testing of a new electronically steerable uplink antenna designed for the next-generation satellite ground link.

The Ground Station as a Service (GSaaS) segment is the fastest-growing segment in the market during the forecast period. This growth is driven by a rapid industry shift from capital-intensive infrastructure ownership to on-demand, cloud-connected ground network access. Through the service, there is integration with cloud-based data processing and AI-driven mission management. In January 2025, Viasat was selected by NASA to provide ground segment services under its Near Space Network (NSN) contract, a program structured around the GSaaS model that delivers antenna access and ground operations as a managed service.

To know how our report can help streamline your business, Speak to Analyst

By Function

Data Reception & Processing Segment to Showcase Fastest Growth due to Rise of Data-Intensive Applications

In terms of function, the market is categorized into telemetry, tracking & command (TT&C),

data reception & processing, communication & backhaul, and network management & integration.

The communication & backhaul segment with a share of 39.6% in 2026 is experiencing robust growth within the satellite ground station market, driven by expanding connectivity demands, data-intensive applications, and the proliferation of satellite constellations. The primary role of this segment is to enable high-capacity data relay between satellite technology and terrestrial networks, supporting broadband, mobility, and defense communications.

- For instance, in August 2025, Globalstar announced the expansion of its ground station in Singapore by adding two new 6-meter tracking antennas to support its third-generation C-3 mobile satellite system. The C-3 system will support applications such as emergency SOS messaging, asset tracking, Internet of Things connectivity for industries, and critical backup communications.

Such developments highlight the growing use of ground stations for communication and backhaul.

The data reception & processing segment is expected to grow at the fastest rate during the forecast period. The rise of data-intensive applications such as broadband communication, hyperspectral imaging, and real-time Earth observation is driving demand for data reception & processing. Modern ground stations must process massive data volumes efficiently and distribute them to analytics or storage platforms with minimal delay.

By Frequency Band

Increase in Demand for High Reliability Boosted the Growth of the C Band Segment

Based on frequency band, the satellite ground station market is segmented into C-band, Ku-band, Ka-band, S / X bands, and others.

The C-band segment held the dominating position in 2024. This segment accounted for the largest share in 2024 due to its long-established use in satellite communication and ground station networks, owing to its high reliability, wide coverage, and lower susceptibility to rain fade compared to higher-frequency bands. The S Band/X Band segment is expected to lead the market, contributing 30.98% globally in 2026.

The Ka band segment is expected to grow at the fastest rate during the forecast period. This growth is primarily driven by the surge in high-throughput satellite (HTS) deployments and broadband constellations requiring higher data capacity and faster transmission speeds. Moreover, Ka band is becoming a popular choice for low-latency satellite communication, which is expected to drive growth in the segment.

- For instance, in September 2025, Eutelsat partnered with French startup Skynopy to test using idle Ka-band antennas from its global OneWeb ground stations to offer Earth observation operators much faster, near-real-time data downlinks.

By Orbit

Proliferation of Mega-Constellations Accelerated the Growth of the Low Earth Orbit (LEO) Segment

Based on orbit, the market is segmented into Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Orbit (GEO).

The Low Earth Orbit (LEO) segment will account for 52.18% market share in 2026, due to the rapid expansion of satellite constellations for broadband internet, Earth observation, and IoT connectivity. The orbit’s proximity to Earth enables lower latency, faster data transmission, and reduced signal attenuation, making it ideal for emerging high-throughput and real-time applications. The surge in launches by commercial operators such as SpaceX, OneWeb, and Amazon’s Kuiper Project has significantly expanded the demand for LEO ground stations capable of frequent handovers and global coverage.

- For instance, in August 2025, Tata Group’s Nelco partnered with Eutelsat to roll out OneWeb’s LEO (Low Earth Orbit) satellite services in India, aiming to deliver secure, low-latency broadband connectivity. Such developments support the building of LEO-compatible ground stations for fast and reliable backhaul.

In 2024, the Geostationary Orbit (GEO) segment holds the second-largest share in the market. GEO satellites remain vital for television broadcasting, weather monitoring, and fixed communication services that benefit from their constant position relative to Earth.

By Application

Rising Demand for High-Speed Satellite Broadband Boosted the Growth of the Communication Segment

Based on application, the market is segmented into communication, earth observation, navigation & positioning, military & intelligence, scientific research, space exploration, and others.

In 2024, the communication segment maintained the largest share and is also the fastest-growing segment in the market, owing to the surging demand for high-speed satellite broadband, data relay, and backhaul connectivity across both commercial and government sectors. Ground stations supporting communication satellites are critical for enabling global coverage, low-latency links, and integration with terrestrial 5G and cloud networks. The increasing number of LEO and GEO communication constellations such as Starlink, OneWeb, and Viasat-3 is significantly boosting investments in multi-band and cloud-connected ground infrastructure.

- For instance, in February 2025, OneWeb expanded its global ground station network in partnership with Kongsberg Satellite Services (KSAT) to enhance real-time broadband access and network redundancy across the polar region.

By Platform

Multi-Mission Capability Encouraged the Growth of the Fixed Segment

Based on platform, the market is segmented into fixed, transportable, and mobile.

In 2024, the fixed segment accounted for the largest share in the market, attributed to the extensive global network of permanent ground stations that serve as the backbone of satellite communication, Earth observation, and TT&C operations. Fixed stations are typically equipped with high-capacity antennas, advanced RF systems, and multi-band support, making them ideal for continuous operations across GEO, MEO, and LEO missions.

The mobile segment is expected to witness the fastest growth rate during the forecast period.

The segment growth is driven by the rising demand for mobile satellite connectivity in aviation, maritime, and defense applications, where flexible and on-the-move communication is essential. Mobile ground stations and terminals mounted on aircraft, ships, and land vehicles are increasingly being deployed to ensure continuous connectivity for data transfer, navigation, and mission-critical operations.

To know how our report can help streamline your business, Speak to Analyst

By End User

Rapid Expansion of Private Satellite Operators Propelled the Growth of the Commercial Segment

Based on end user, the market is segmented into commercial, government, and defense.

The commercial segment captured the largest share of the satellite ground station market in 2024 and is projected to record the fastest growth during the forecast period. The segment’s leadership is driven by the rapid expansion of private satellite operators, cloud service providers, and telecommunication companies investing in advanced and scalable ground infrastructure. Commercial players are increasingly adopting Ground Station-as-a-Service (GSaaS) and cloud-based network management solutions to support high-throughput LEO and GEO constellations for broadband, IoT, and Earth observation applications.

The defense segment continues to hold a significant share of the market, supported by consistent investment in secure, resilient, and mission-critical communication networks. The increasing focus on space-based situational awareness (SSA) and the need for encrypted, multi-band communication systems are encouraging defense modernization programs across the globe. There is also a rise in the expansion and modernization of ground infrastructure critical for national security and missile defense operations.

- For instance, in May 2025, Northrop Grumman secured a USD 244 million contract from the U.S. Space Force to develop advanced relay ground stations in the U.S. and U.K., supporting the Next-Generation Overhead Persistent Infrared (Next-Gen OPIR) program.

Satellite Ground Station Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The North America Satellite Ground Station market Size, 2025(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the largest share of the global market and continues to dominate due to its well-established commercial, defense, and government space infrastructure. The market in North America reached USD 24.35 billion in 2025, representing 38.72% of total market revenue, and is projected to reach USD 26.7 billion in 2026. The U.S. leads global investment in satellite communication, deep-space missions, and ground-station modernization through both federal agencies and private companies. The region hosts major Ground Station-as-a-Service (GSaaS) providers and cloud-integrated networks that enable real-time satellite data access and low-latency downlinks. The presence of companies such as AWS Ground Station, SpaceX, and NASA, along with the DoD’s deep-space networks, strengthens the region’s leadership. Additionally, strategies and developments by key players such as Viasat, General Dynamics Corporation, and others keep the region at the forefront of market innovation. The U.S. market is valued at USD 22.25 billion by 2026.

- For instance, in October 2025, Viasat was awarded an initial design contract by the U.S. Space Force under the Protected Tactical SATCOM-Global (PTS-G) program to develop a dual-band (X/Ka) satellite and anchor station architecture that supports secure, anti-jam communications for military users.

Europe

Europe contributed approximately USD 12.36 billion to the global market in 2025, accounting for 19.66% share, and is expected to reach USD 13.63 billion in 2026. Europe accounted for the second-largest share of the satellite ground station market, driven by strong investments from the European Space Agency (ESA) and national agencies. The region is focused on building secure, interoperable, and green ground networks capable of supporting high-data-rate communication, TT&C, and space exploration missions. Countries such as Germany, France, the U.K., and Italy are leading infrastructure upgrades and research in optical ground station networks. The UK market is valued at USD 3.13 billion by 2026, while the Germany market is valued at USD 2.8 billion by 2026.

- For example, in April 2025, Heriot-Watt University launched a USD 3.33 million Quantum Communications Hub Optical Ground Station (HOGS) in Edinburgh, designed to enable ultra-secure, high-speed laser communications between satellites and Earth.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 16.3 billion, representing 25.91% of global demand, and is projected to grow to USD 18.05 billion in 2026. Asia Pacific is emerging as the fastest-growing region in the satellite ground station market, driven by rapid expansion in satellite launch activity and ground network development in China, India, Japan, and South Korea. Governments and private operators are establishing new TT&C and data-reception facilities to support Earth observation, broadband connectivity, and navigation systems. National programs such as China’s SatNet, India’s NavIC, and Japan’s Quasi-Zenith constellation continue to drive investments in regional ground infrastructure. The Japan market is valued at USD 2.61 billion by 2026, the China market is valued at USD 6.54 billion by 2026, and the India market is valued at USD 4.84 billion by 2026.

Latin America

The Latin America market accounted for USD 4.44 billion in 2025, representing 7.06% of the global industry, and is expected to reach USD 4.76 billion in 2026. Latin America represents a smaller yet steadily expanding market, supported by growing demand for Earth observation and communication services. Countries such as Brazil, Argentina, and Chile are investing in national ground facilities and entering public-private partnerships to strengthen satellite data reception capabilities. Efforts to enhance agricultural monitoring, disaster management, and rural connectivity are driving new ground station installations across the regions.

- For instance, in December 2021, AWS expanded its satellite ground station network to South America by launching a new antenna location in Punta Arenas, Chile, connected to its São Paulo cloud region.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 5.44 billion in 2025, accounting for 8.66% share, and is expected to reach USD 5.91 billion in 2026. The Middle East & Africa region holds a modest share of the global market but is witnessing strategic growth driven by defense modernization and space exploration initiatives. The Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are investing in new satellite networks and ground stations for national communications and remote sensing. Meanwhile, several African nations are engaging in international collaborations to host ground stations that support global LEO constellations for climate monitoring and broadband access.

COMPETITIVE LANDSCAPE

Key Industry Players:

Rising Satellite Deployments, Expansion of Global GSaaS Networks, and Strategic Collaborations with Cloud & Defense Sectors Drive Market Leadership among Key Players

The global market is driven by the surge in satellite constellations, increasing demand for real-time data connectivity, and the expansion of Ground Station-as-a-Service (GSaaS) networks. Key players such as Viasat Inc., Kongsberg Satellite Services (KSAT), SES S.A., Airbus Defence & Space, Thales Group, General Dynamics Mission Systems, and Kratos Defense & Security Solutions are at the forefront of developing advanced ground communication infrastructure and intelligent network management solutions.

These companies offer comprehensive portfolios spanning antenna systems, RF front ends, telemetry & tracking (TT&C) equipment, mission control software, and integrated GSaaS networks supporting a diverse satellite operation from low Earth orbit (LEO) broadband constellations to deep-space exploration missions.

Market leaders are increasingly focusing on cloud integration, software-defined networking, and optical communication technologies to enhance the interoperability, scalability, and resilience of ground systems. Strategic partnerships with satellite operators (SpaceX, OneWeb, Amazon Kuiper) and cloud providers (AWS, Azure Orbital, Google Cloud) are reshaping the market landscape, enabling flexible access models and global coverage.

LIST OF KEY SATELLITE GROUND STATION COMPANIES PROFILED:

- Kongsberg Satellite Services (Norway)

- Viasat Inc. (U.S.)

- Airbus Defence and Space (Germany)

- Thales Group (France)

- General Dynamics Mission Systems (U.S.)

- Kratos Defense & Security Solutions (U.S.)

- SES S.A. (Luxembourg)

- Swedish Space Corporation SSC (Sweden)

- Lockheed Martin Corporation (U.S.)

- Cobham SATCOM (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: The U.S. Space Force awarded contract worth USD 17.6 million to Colorado-based defense firms Boecore (operating as Auria) and Sphinx Defense for the development of prototype cloud-based marketplaces called the Joint Antenna Marketplace (JAM).

- May 2025: Telesat announced a partnership to build and manage an extensive ground station network valued at up to USD 1 billion, aimed at supporting its advanced Lightspeed low Earth orbit (LEO) satellite constellation.

- July 2025: Kongsberg Satellite Services (KSAT) announced the expansion of its collaboration with Amazon Web Services (AWS) by integrating AWS Ground Station capabilities into its commercial offerings.

- July 2024: Dhruva Space, based in Hyderabad, received authorization from the Indian National Space Promotion and Authorisation Center (IN-SPACe) to offer Ground Station as a Service (GSaaS). This marks a significant advancement in its commercial ground segment capabilities.

- May 2024: KSAT Inc., a subsidiary of Kongsberg Satellite Services, announced that it is conducting a study with NOAA to evaluate future satellite ground network architectures for demanding mission applications. The study would examine advances in phased array antennas, APIs, ground network virtualization, and data processing.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. Satellite ground station market analysis includes Porter’s five forces analysis, which illustrates the potency of buyers and suppliers in the market. Station ground station market forecast offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.91% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Offerings

By Function

By Frequency Band

By Orbit

By Application

By Platform

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 62.89 billion in 2025 and is projected to reach USD 169.88 billion by 2034.

In 2025, the market value stood at USD 24.35 billion.

The market is expected to exhibit a CAGR of 11.91% during the forecast period (2026-2034).

The communication segment led the market by application.

The key factors driving the market are the rise in the deployment of LEO satellites.

Kongsberg Satellite Services (Norway), Viasat Inc. (U.S.), Airbus Defence, Space (Germany), and others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us