Satellite Mega Constellations Market Size, Share, Industry Analysis, By Orbit Type (LEO, MEO, GEO, and Others), By Application (Broadband Connectivity, Earth Observation, Navigation & Positioning, and Others), By Constellation Size (Small (100-500), Medium (501-1000), Large (1001-3000), and Very large (Above 3000)), By Constellation Program (Starlink, Oneweb, Kuiper, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

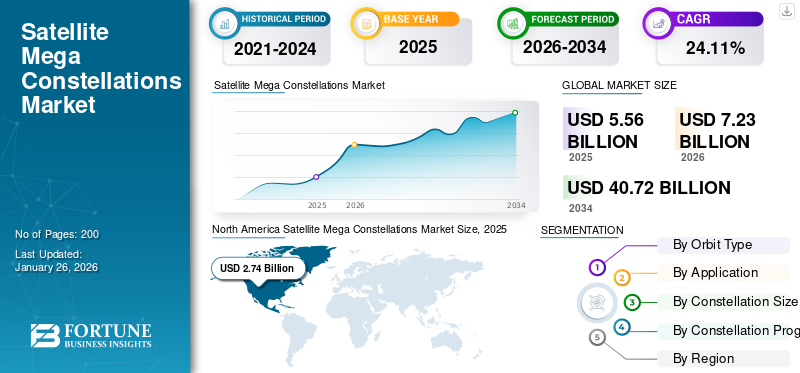

The global satellite mega constellations market size was valued at USD 5.56 billion in 2025. The market is projected to grow from USD 7.23 billion in 2026 to USD 40.72 billion by 2034, exhibiting a CAGR of 24.11% during the forecast period. North America dominated the satellite mega constellations market with a market share of 49.28% in 2025.

Satellite network constellations represent a transformative leap in global communications infrastructure, consisting of hundreds to tens of thousands of satellites working together in coordinated orbits, primarily in Low Earth orbit (LEO), to deliver broadband internet and advanced Earth observation services worldwide. Unlike traditional geostationary satellites, which offer coverage to fixed, large areas from high altitudes, satellite mega constellations leverage the advantages of lower orbits, including reduced latency, higher bandwidth, and continuous near-global coverage, as the satellites move rapidly across the sky. This architecture enables real-time connectivity and data collection, making it possible to bridge the digital divide in remote and underserved regions, support disaster response, and fuel innovations in fields such as agriculture, climate monitoring, and logistics.

Key players include SpaceX’s Starlink, which leads with thousands of operational satellites and ambitious plans for further expansion. OneWeb focuses on serving enterprise and government markets. Amazon’s Project Kuiper aims to deploy a network of 3,236 satellites, while China’s GuoWang plans to launch nearly 13,000 satellites.

The COVID-19 pandemic had a twin impact on the global market. While it initially disrupted supply chains and delayed some launches, the crisis underscored the critical importance of resilient, high-speed connectivity as remote work, online education, and telemedicine became essential across the globe.

Download Free sample to learn more about this report.

Satellite Mega Constellations Market KEY TAKEAWAYS

- 2025 Market Size: USD 5.56 Billion

- 2026 Market Size: USD 7.23 Billion

- 2034 Forecast Market Size: USD 40.72 Billion

- CAGR: 24.11% from 2026–2034

- North America dominated the satellite mega constellations market with a 49.28% share in 2025.

- The LEO segment held 78% of the market share in 2025 and is projected to account for 79.87% in 2026.

- The broadband connectivity segment is projected to account for 46.59% of the market in 2026.

North America

North America generated USD 2.74 billion in 2025 and is projected to reach USD 3.60 billion in 2026.

Europe

Europe generated USD 1.25 billion in 2025 and is projected to reach USD 1.63 billion in 2026.

Asia Pacific

Asia Pacific generated USD 0.92 billion in 2025 and is projected to reach USD 1.19 billion in 2026.

U.S.

The satellite mega constellations market is projected to reach USD 2.9 billion in 2026.

Japan

The satellite mega constellations market is projected to reach USD 0.18 billion in 2026.

Read More

Market Dynamics

Market Drivers

Rise in Commercial Broadband Demand along with Government Initiatives to Bolster Market Growth

The rapid rise in commercial broadband demand, coupled with robust government initiatives, is fundamentally reshaping the satellite mega constellations market growth. Satellite mega constellations, such as those deployed by SpaceX, OneWeb, and Amazon, are bridging this digital divide by providing low-latency, high-speed broadband access globally. These networks, comprised of hundreds or even thousands of Low Earth Orbit (LEO) satellites, offer a transformative alternative to geostationary satellites, drastically reducing signal delay and increasing coverage capacity.

Government initiatives further amplify this momentum. National and regional authorities recognize the strategic importance of universal connectivity for economic development, public safety, and social inclusion. For instance, in September 2024, the Canadian government recently provided a USD 1.54 billion loan to Telesat for its Lightspeed mega-constellation, marking the country’s largest space program to date. This constellation, consisting of 198 LEO satellites, is designed to deliver affordable, reliable internet to even the most remote parts of Canada, including Indigenous communities and critical industries. The government’s support accelerates deployment and stimulates job creation and technological advancement, with Telesat’s project expected to generate 2,000 jobs and inject USD 3.17 billion into the Canadian economy.

Market Restraints

Rise in Space Debris and Collision Risk Ought to Restrict Market Expansion

The rapid expansion of satellite mega constellations faces significant headwinds from escalating space debris and collision risks, threatening long-term market viability. In March 2025, as per a patentPC article, with over 60% of active satellites in Low Earth orbit (LEO) belonging to mega-constellations such as Starlink and OneWeb, the orbital environment is becoming increasingly congested. Studies project that a single collision within a satellite mega constellation could generate thousands of debris fragments.

Furthermore, a 2023 study found that mega-constellations could increase LEO collision rates by 30-50% by 2030, raising insurance premiums for operators by up to 25%. The 2019 near-miss between Starlink satellites and ESA’s Aeolus satellite, requiring last-minute maneuvers, highlighted the operational disruptions caused by congested orbits. Additionally, proposed “polluter-pays” principles under international space law could impose USD 20-50 million fines per debris-generating event, eroding profit margins for constellations with thousands of satellites.

Market Opportunities

Hybrid Network and 5G Integration Offer Major Growth Opportunity

Hybrid networks that integrate Low Earth Orbit (LEO) satellite mega constellations with terrestrial 5G infrastructure are emerging as a major growth opportunity in global connectivity. This integration addresses the limitations of terrestrial networks, particularly in remote, rural, and hard-to-reach regions where deploying high-speed internet or dense 5G small cells is economically or physically unfeasible. By leveraging the expansive coverage of satellites and the high capacity and low latency of 5G, hybrid networks can deliver seamless, global connectivity.

The synergy between LEO satellites and 5G is particularly valuable for industries and applications requiring reliable, high-speed, and low-latency connections. For example, sectors such as aviation, maritime, mining, and agriculture benefit from the ability to connect IoT sensors, autonomous vehicles, and mission-critical systems far from urban centers. LEO satellites, operating at altitudes of 500–2,000 km, provide latency as low as 20–40 milliseconds, comparable to terrestrial 5G, making them suitable for video calls, online gaming, and remote work.

The business case for hybrid networks is further strengthened by the ongoing deployment of mega-constellations by companies such as SpaceX (Starlink), Amazon (Project Kuiper), and OneWeb, which are rapidly increasing the availability of satellite bandwidth. As these constellations mature, they are expected to play a central role in the 5G and even 6G ecosystem, enabling new applications and revenue streams for both satellite and telecom operators.

Market Challenges

Regulatory Fragmentation Between Countries Can Lead to Growth Challenges

Regulatory fragmentation between countries presents a significant challenge to the growth and sustainability of the global market. Unlike geostationary satellites, which are coordinated through the International Telecommunication Union (ITU), the deployment and management of Low Earth orbit (LEO) satellite mega constellations are primarily governed by national regulators such as the U.S. Federal Communications Commission (FCC). This “first-come, first-served” approach to orbital shell and frequency allocation allows national actors to saturate certain orbital regions, often without a comprehensive assessment of the global impacts or consultation with other countries. Without international cooperation and harmonized rules, the proliferation of satellite mega constellations could lead to increased interference, operational conflicts, and environmental risks. This scenario restricts market expansion by raising barriers for new entrants and smaller nations and heightens the potential for disputes and accidents in an already congested orbital environment.

Satellite Mega Constellations Market Trends

Integration of Advanced Technologies in Satellite Mega Constellations is a Key Market Trend

The integration of advanced satellite technology is fundamentally transforming the satellite mega constellations market, driving both operational efficiency and the expansion of services. One of the most significant advancements is the use of high-speed inter-satellite links, particularly laser communication systems. These links allow satellites within a satellite mega constellation to communicate directly with each other, dramatically increasing data transfer speeds and reducing dependence on ground stations. As a result, networks can deliver lower latency and more reliable global coverage, which is essential for real-time applications such as broadband internet, remote sensing, and disaster response.

Artificial Intelligence (AI) and automation are also playing a pivotal role in the management and optimization of mega constellations. AI-driven systems are being used for dynamic network management, collision avoidance, and efficient resource allocation. For example, automated collision avoidance technology is now essential given the sheer number of satellites in orbit, helping to reduce the risk of space debris and ensuring the safety and sustainability of these vast networks. Additionally, AI supports predictive maintenance and autonomous operations, minimizing human intervention and enhancing the longevity and reliability of satellite assets.

Impact of Tariff

Tariffs have had a profound impact on the satellite mega constellations market, particularly for operators deploying large fleets of satellites in Low Earth Orbit (LEO). The imposition of tariffs-especially those targeting critical imports from China, has increased the cost of essential components such as rare earth elements, semiconductors, solar panels, and precision electronics. Many of these components are not readily available domestically at scale, making satellite manufacturing and deployment significantly more expensive. This cost pressure is particularly acute for mega constellation projects, which rely on mass production and rapid deployment to achieve commercial viability and global coverage.

In April 2025, U.S. tariffs accelerated China’s efforts to replace 30% of specialized satellite components previously sourced from the U.S. despite higher production costs from smaller-scale domestic manufacturing. Beijing’s retaliatory tariffs (up to 125% on U.S. goods) and subsidies for local firms aim to reduce reliance on foreign technology, fostering competition with U.S.-led projects such as Starlink.

Moreover, tariffs have introduced delays and unpredictability, as components subjected to new taxes, customs inspections, or outright export controls face longer lead times and occasional shipment blocks. These disruptions cascade through manufacturing workflows, causing delays in satellite builds and launch schedules.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Orbit Type

LEO Dominated Market Owing to Its Escalating Demand for Earth Observation, Internet Connectivity, and Voice Communications

The market is classified by orbit type into LEO, MEO, GEO, and Others.

The LEO segment dominated the global market of 79.87% in 2026 and is expected to be the fastest-growing segment during the 2026-2034 period. The segment is expected to acquire 78% of the market share in 2025. The proliferation of LEO satellites is driven by the escalating demand for Earth observation, internet connectivity, and voice communications, as well as the evolution of the Internet of Things (IoT) and increased commercial and defense sector applications. The ability of LEO commercial satellites to deliver low-latency, high-speed broadband, especially in underserved and remote areas, positions them as a transformative force in the global connectivity landscape.

The GEO segment is anticipated to show significant growth during the study period. The segment is likely to exhibit a CAGR of 10.81% during the forecast period. Geostationary Earth Orbit (GEO) satellites continue to play a vital role in established communication and broadcasting services. Their growth is comparatively moderate due to higher latency and deployment costs.

By Application

Advancements and Expansion in Internet of Things (IoT) Boosted Broadband Connectivity Segment Growth

Based on application, the market is segmented into broadband connectivity, Earth observation, navigation & positioning, and others.

The broadband connectivity segment dominated the global satellite mega constellations market share by 46.59% in 2026 and is expected to be the fastest-growing segment over the 2026-2034 period. IoT adoption is accelerating across industries, driven by innovations in edge computing, smart sensors, and digital twins. The demand for robust, real-time, and high-speed broadband connectivity is reaching new heights.

The Earth observation segment is anticipated to witness significant growth during the study period. Earth observation is another key application, leveraging LEO satellites to deliver high-resolution, real-time imagery for environmental monitoring, disaster management, and urban planning. This segment benefits from the satellites’ ability to revisit specific areas frequently, providing critical data for diverse industries.

To know how our report can help streamline your business, Speak to Analyst

By Constellation Size

Increased Deployment of Mega Constellation by Key Players Bolstered Very Large (Above 3000) Segment Expansion

By constellation size, the market is categorized into small (100-500), medium (501-1000), large (1001-3000), and very large (above 3000).

The very large (above 3000) segment dominated the global market expected for 42.89% market share in 2026. The segment is expected to hold 42% of the market share in 2025. Constellation size: very large constellations, those with more than 3,000 satellites, are experiencing the most significant growth. The deployment and satellite launches of mega-constellations, particularly by Starlink, are reshaping the market by enabling global coverage, network redundancy, and improved reliability. The scale of these constellations allows for continuous technological upgrades and cost efficiencies, further accelerating their expansion.

The large (1001-3000) segment is anticipated to show a CAGR of 42% during the study period. In February 2025, as per an article by the UN agency for digital technologies, the space sector has attracted more than USD 60 billion in investment, with nearly USD 50 billion coming in the last five years alone, enabling ambitious projects from companies such as SpaceX, OneWeb, and Amazon's Project Kuiper to move forward aggressively. These investments have accelerated innovation and market entry, further propelling the growth of this segment.

By Constellation Program

Aggressive Deployment Strategy, Technological Innovation Boosted Starlink Segment

By constellation program, the market is categorized into Starlink, OneWeb, Kuiper, and others.

The Starlink segment is expected to account for 43.93% of the market in 2026. Starlink has established itself as the leading constellation program due to its unprecedented scale and aggressive deployment strategy. As of 2025, Starlink operates nearly 7,000 satellites in Low Earth orbit (LEO) at altitudes of 550 km.

The Oneweb segment is anticipated to show moderate growth during the study period. OneWeb ranks second, with 648 satellites deployed at a higher orbit of 1,200 km, enabling broader coverage per satellite but slightly higher latency (sub-100 ms). Its focus is on enterprise and government markets via partnerships with Eutelsat and strategic contracts in the aviation and maritime sectors.

SATELLITE MEGA CONSTELLATIONS MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America Satellite Mega Constellations Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 2.74 billion in 2025, capturing 49.28% of the global market share, and is projected to reach USD 3.6 billion in 2026, driven by massive private-sector investments and government initiatives to boost the space economy. The region’s growth is fueled by defense applications (e.g., missile tracking, border surveillance) and consumer broadband demand, with the U.S. Space Force and NASA prioritizing satellite-based security and research. The United States dominates the market due to a combination of technological leadership, aggressive private-sector investment, and strategic policy frameworks. The U.S. market is projected to reach USD 2.9 billion by 2026.

Europe

In 2025, Europe represented USD 1.25 billion, accounting for 22.49% of the worldwide market, and is projected to grow to USD 1.63 billion in 2026. The region is expected to be the second-largest market with a value of USD 0.95 billion in 2025. Europe’s market is characterized by public-private partnerships and strategic mergers, such as OneWeb’s merger with Eutelsat to enhance GEO-LEO synergies. The European Space Agency (ESA) is investing in secure connectivity initiatives, including the IRIS² constellation for defense and government use. The region focuses on sustainability, with regulations addressing space debris mitigation and AI-driven satellite operations.The UK market is projected to reach USD 0.51 billion by 2026, while the Germany market is projected to reach USD 0.33 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 0.92 billion in 2025, representing 16.56% of the global market landscape, and is expected to reach USD 1.19 billion in 2026. The region is expected to be the third-largest market with a value of USD 0.71 billion in 2025. The growth is driven by China’s GuoWang constellation (13,000+ planned satellites) and India’s Space Policy 2023, which encourages private-sector participation. Companies such as GalaxySpace (China) and Skyroot Aerospace (India) are advancing low-cost satellite manufacturing and miniaturization technologies. Japan’s Space Compass aims to deploy LEO satellite communications for IoT and maritime connectivity, while Australia’s Fleet Space focuses on mining and defense applications. The region’s growth is bolstered by rising demand for rural broadband and government-funded space programs, though geopolitical tensions and spectrum allocation challenges pose risks. The Japan market is projected to reach USD 0.18 billion by 2026, the China market is projected to reach USD 0.37 billion by 2026, and the India market is projected to reach USD 0.31 billion by 2026.

Middle East & Africa

The Middle East & Africa is an emerging market, with growth centered on telecom expansion and earth observation. The region is expected to be the fourth-largest market with a value of USD 0.51 billion in 2025. UAE leads with Yahsat’s Thuraya-4 satellite and MBRSC’s collaboration with SpaceX for lunar missions. Saudi Arabia’s NEOM project integrates satellite IoT for smart city infrastructure, while Africa’s SAOCOM (South Africa) and Rwanda’s partnership with OneWeb aim to bridge digital divides. However, limited domestic launch capabilities and high infrastructure costs constrain growth, with most nations relying on foreign operators such as Starlink for connectivity. The UAE market size is expected to be USD 0.18 billion in 2025.

Rest of the World

The market in Rest of the World reached USD 0.65 billion in 2025, representing 11.66% of total market revenue, and is projected to reach USD 0.81 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players are Focused on Planning Collaboration and Partnerships in Deploying Mega Satellite Constellations

Key players in the market are focused on planning long-term collaboration and partnerships in deploying mega satellite constellations, recognizing that the scale and complexity of these projects demand shared expertise, resources, and infrastructure. Major industry leaders such as SpaceX (Starlink), Amazon (Project Kuiper), OneWeb, and Telesat are investing heavily in their satellite networks. They are also forming strategic alliances with launch providers, satellite manufacturers, and telecommunications companies to accelerate deployment and expand service reach.

LIST OF KEY SATELLITE MEGA CONSTELLATION COMPANIES PROFILED

- SpaceX (U.S.)

- OneWeb (U.K.)

- Amazon (U.S.)

- China Aerospace Science and Technology Corporation (CASC) (China)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Airbus Defence and Space (Germany)

- Thales Alenia Space (France)

- Boeing (U.S.)

- ICEYE (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2025 – United Launch Alliance announced to launch of 27 Kuiper satellites into low Earth orbit with the initiation of a comprehensive rollout of the Project Kuiper satellite internet network. Project Kuiper aims to provide high-speed, low-latency internet access to nearly every spot on the globe.

- February 2025 – EnSilica declared that it received funding from the U.K. Space Agency through its connectivity in Low-Earth Orbit (“C-LEO”) programme. After a competitive selection process, EnSilica was granted USD 13.82 million for a development project that it will lead over the next three years.

- February 2025 – DA Space announced that it is constructing over 50 satellites for Globalstar’s Apple-supported next-generation Low Earth orbit (LEO) constellation under a USD 768 million agreement.

- December 2024 – Telesat and MDA Space announced that they have finalized a crucial phase in the Telesat Lightspeed Low Earth orbit (LEO) constellation program with the successful achievement of the spacecraft Preliminary Design Review (PDR).

- November 2024 – Apple committed funding of USD 1.5 billion to Globalstar for a next-gen LEO constellation to enhance iPhone satellite connectivity. This supports Globalstar’s expansion into direct-to-cell services. The agreement between the tech giant and Globalstar involves USD 1.1 billion in cash, with USD 232 million designated for the satellite company's existing debt, along with a 20% equity ownership.

REPORT COVERAGE

The report outlines competitive dynamics by assessing market segmentation, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. It provides detailed insights into the market segmentation. Besides this, it offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, factors increasing demand for satellite mega constellations, and company profile, and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors that have contributed to the growth of the developed market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 24.11% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Orbit Type

|

|

By Application

|

|

|

By Constellation Size

|

|

|

By Constellation Program

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global market size was valued at USD 5.56 billion in 2025 and is anticipated to record a valuation of USD 40.72 billion by 2034.

The market is likely to grow at a CAGR of 24.11% during the forecast period of 2026-2034.

The top players in the industry are SpaceX, OneWeb, Amazon, China Aerospace Science and Technology Corporation (CASC), and Lockheed Martin Corporation.

North America dominated the market in 2025.

The rise in commercial broadband demand, along with government initiatives, is expected to bolster the market growth.

The rise in space debris and collision risk is expected to restrict market expansion.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us