Satellite NTN Market Size, Share, Industry Analysis, By Orbit Type (LEO, MEO, GEO, and Others), By Architecture (Transparent (Bent Pipe) Payload and Regenerative payload), By Application (Broadband Services, Emergency & Disaster Response, IOT, Government and military, Aviation and Maritime, 5G NTN, and Others) By Service Type (Fixed Satellite Service (FSS), Mobile Satellite Service (MSS), Broadband Satellite Service (BSS), and Others (Backhaul/fronthaul)), By End User (Telecommunication Operators, Government and Defense, Aviation, and Others), and Regional Forecast Report, 2026-2034

Satellite NTN Market Summary

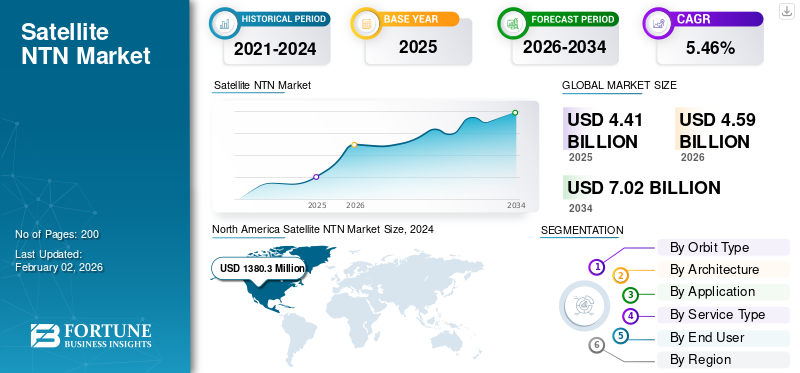

The global satellite NTN market size was valued at USD 4.41 billion in 2024 and is projected to grow from USD 4.59 billion in 2026 to USD 7.02 billion by 2034, exhibiting a CAGR of 5.46% during the study period. North America dominated the satellite NTN market with a market share of 32.73% in 2025.

Wireless communication systems known as non-terrestrial networks (NTN) function above the surface of the planet, utilizing satellites in low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO), high-altitude platforms (HAPS), and drones. The market is experiencing transformative growth, driven by the integration of satellite and terrestrial network technologies to deliver seamless, global connectivity. Advances in LEO satellite constellations, high-throughput architectures, and 5G standards are enabling the provision of low-latency, high-speed broadband services.

Download Free sample to learn more about this report.

Key players in the market include leading satellite operators such as SpaceX, OneWeb, and Amazon. These companies are pioneering large-scale LEO constellations, direct-to-device services, and hybrid network solutions.

The COVID-19 pandemic caused supply chain disruptions, delaying mission deployments and slowing the delivery of new products for the majority of the major space producers which impacted the market share globally. In response, space agencies have provided significant administrative and financial help to government contractors in Asia, Europe, and North America through expedited and advanced payments.

Download Free sample to learn more about this report.

Satellite NTN Market Key Takeaways

- 2025 Market Size: USD 4.41 billion

- 2026 Market Size: USD 4.59 billion

- 2034 Forecast Market Size: USD 7.02 billion

- CAGR: 5.46% from 2026–2034

- North America dominated the satellite NTN market with a 32.73% share in 2025.

- The LEO segment is projected to account for 39.27% of the market share in 2026.

- The broadband services segment is projected to account for 23.98% of the market share in 2026.

North America

North America was valued at USD 1.44 Billion in 2025 and is projected to reach USD 1.51 Billion in 2026.

Europe

Europe was valued at USD 1.33 Billion in 2025 and is projected to reach USD 1.39 Billion in 2026.

Asia Pacific

Asia Pacific was valued at USD 0.88 Billion in 2025 and is projected to reach USD 0.92 Billion in 2026.

U.S.

The U.S. is projected to reach USD 1.02 Billion in 2026.

Japan

Japan is projected to reach USD 0.19 Billion in 2026.

Read More

Market Dynamics

Market Drivers

Growing Demand for Connectivity in Remote Regions to Bolster Market Growth

The primary driver for the satellite NTN market growth is the demand for connectivity in remote areas. Traditional terrestrial networks (Fiber and 4G/5G towers) are often cost-prohibitive or geographically impractical in regions such as rural areas, mountainous terrains, and scattered island nations. Satellite NTN systems, particularly those in LEO, offer a cost-effective alternative, enabling mobile network operators to expand coverage without the need for large-scale infrastructure investments. Major tech players such as SpaceX and Amazon are aggressively launching large-scale constellations for these regions.

Furthermore, the emergence of 3GPP 5G standards allows true direct-to-device (D2D) satellite communications, which connect ordinary mobile devices to satellites without specialized hardware.

Market Restraints

High Cost of Launching and Operating Satellite Constellations to Restrict Market Expansion

Launching and operating satellite constellations require significant capital expenditure, frequent replenishment due to the shorter orbital lifespans of LEO satellites, and ground segment upgrades. In addition, satellite payloads must support advanced onboard processing, adding to system complexity and operational risk. These factors restrict smaller players from entering the market.

Additionally, spectrum allocation and regulatory compliance remain major bottlenecks. Satellite operators must coordinate with terrestrial mobile networks to avoid interference, especially as both operate within sub-6-GHz and mmWave bands in NTN scenarios. Regulatory bodies such as the National and International Telecommunication Union (ITU), FCC, and others have varying timelines and priorities, contributing to delays in commercial rollouts, restraining the global expansion of the market.

Market Opportunities

Global Partnership Between Satellite Constellation Operators and Telecom Companies for Untapped Sectors Offers Major Growth Opportunity

By leveraging hybrid NTN infrastructure, telecom operators/companies can offer seamless coverage to customers, while satellite operators gain subscriber access without the need to build their own retail channels. Companies such as AT&T, Vodafone, and others have already signed agreements with OneWeb, AST Space Mobile, and Starlink to pilot direct-to-cell services.

Furthermore, there is also strong market demand in sectors such as logistics, maritime, and aviation, particularly for applications involving remote tracking, M2M telemetry, and trial time alerts.

Satellites operating NTNs are well-positioned to fill connectivity gaps for IoT devices operating in remote, unmanned, or hostile environments. Another emerging area is government and military adoption, where nations are investing in secure NTN constellations such as IRIS in Europe and Guowang in China. These advancements are key drivers of the satellite NTN market growth.

Market Challenges

Cross-Industry Integration in Satellite NTN Can Hinder Market Growth

Cross-industry integration of satellite NTN is widely recognized as a key catalyst for expanding connectivity across sectors such as transportation, agriculture, logistics, and maritime. However, as more industries adopt satellite NTN solutions, the complexity of integration and the need for seamless interoperability between diverse systems and standards can introduce significant growth challenges in the market.

Each sector has a unique requirement for data rates, latency, reliability, and security. For instance, the aviation sector demands low latency and highly reliable connectivity for safety-critical communications, while the agriculture sector may prioritize low-cost, wide-area IoT monitoring solutions. Additionally, the use of different frequency bands, communication protocols, and hardware specifications across industries can result in compatibility issues, leading to higher integration costs and longer deployment timelines.

Satellite NTN Market Trends

Growth of LEO Satellite Constellation is a Key Market Trend

A major trend in the satellite NTN market is the rapid expansion of LEO satellite constellations. Companies such as SpaceX, oneweb, and Amazon are launching thousands of small satellites to provide high-speed, low-latency internet access worldwide. This trend is transforming global connectivity by offering improved coverage, especially in remote and underserved regions, and enabling new applications such as direct-to-device communications and enhanced IoT services. The increased affordability and efficiency of satellite launches, driven by reusable rocket technology, are further accelerating this shift, making satellite internet more accessible for a broader range of users.

Use Case - Satellite NTN Market

September 2023- Vodafone Collaborated with Amazon's Project Kuiper to Increase 5G Coverage

- In order to improve its 4G and 5G networks in Europe and Africa, Vodafone announced a partnership with Amazon's Project Kuiper, a low Earth orbit satellite constellation. This collaboration would make use of Project Kuiper's satellites to connect mobile base stations in isolated locations, eliminating the requirement for conventional fiber-based or fixed wireless reliable connections. Amazon plans to launch manufacturing satellites in 2024, positioning its network as a competitor to Elon Musk's Starlink, OneWeb, and others.

- It will soon begin testing prototype satellites. Together, Amazon and Vodafone are working to deliver high-speed broadband to underserved regions around the world and give firms connection options.

- In June 2024 Vodafone signed with AST spaceMobile, this partnership would complement their current partnership with AST SpaceMobile to create a space-based mobile network that can be accessed using common mobile phones.

SEGMENTATION ANALYSIS

By Orbit Type

LEO Segment Dominated the Market Owing to its Low Latency and High Speed Connectivity Services

By orbit type, the market is classified into LEO, MEO, GEO, and others.

The LEO segment led the market accounting for 39.27% market share in 2026. LEO satellites provide low latency and high-speed connectivity, making them ideal for broadband and IOT applications. Their lower altitude reduces signal delay, making LEO constellations well-suited for real-time services.

The MEO segment is anticipated to show significant growth during the study period. MEO constellations are valuable for navigation and certain communication services. The deployment of MEO satellites is supported by the demand for resilient, wide-area networks and the need to balance latency and coverage in a hybrid multi-orbit architecture.

To know how our report can help streamline your business, Speak to Analyst

By Architecture

Transparent Payloads Segment Led the Market due to Its Lower Complexity

Based on architecture, the market is segmented into transparent (bent pipe) payload and regenerative payload.

The transparent (bent pipe) payload segment will account for 63.71% market share in 2026. Its lower complexity and faster time-to-market make it an attractive option for commercial operators looking to quickly expand network coverage.

The regenerative payload segment is anticipated to witness significant growth during the study period. These payloads enable direct satellite-to-satellite communication, improve spectrum utilization, and allow more flexible and scalable network architectures. The increasing demand for regenerative payload is driven by the need for higher performance in 5G integration, IoT, and government/defense applications, where secure and reliable connectivity is important.

By Application

Broadband Services Segment Led due to its Ability to Support Remote Work in Hard-to-Reach Areas

By application, the segment is categorized into broadband services, emergency & disaster response, IOT, government and military, aviation and maritime, 5G NTN, and others.

The broadband services segment will account for 23.98% market share in 2026. Satellite broadband is becoming a critical tool for bridging the digital divide and supporting remote work in hard-to-reach areas. The deployment of LEO constellations is making satellite broadband more affordable and accessible, driving adoption among consumers, enterprises, and government agencies.

The IoT segment is anticipated to show moderate growth during the study period. IoT applications are expanding rapidly, as satellite NTN enables reliable, global connectivity for sensors, devices, and machines across industries such as logistics, energy, and environmental monitoring. Furthermore, the growth of satellite-based IoT is driven by increasing digitalization of industries and the need for seamless end-to-end connectivity across regions.

By Service Type

Broadband Satellite Services Segment Dominated due to Advancements in Satellite Technology

By service type, the segment is categorized into Fixed Satellite Service (FSS), Mobile Satellite Service (MSS), Broadband Satellite Service (BSS), and others (Backhaul/fronthaul).

The broadband satellite services segment will account for 39.10% market share in 2026. Innovations in satellite technology, such as phased array antennas and advanced modulation schemes, are improving service quality and reducing operational costs, accelerating product adoption.

The mobile satellite service segment is anticipated to show moderate growth during the study period. These services are expanding steadily, providing essential connectivity for maritime, aviation, and terrestrial mobile users in areas lacking cellular coverage.

By End User

Telecommunication Operators Segment Led due to its Ability to Reach New Customer Segments

By end user, the market is categorized into telecommunication operators, government and defense, aviation, and others.

The telecommunication operators segment dominated the global market in 2024. Satellite connectivity enables operators to reach new customer segments, support hybrid network architectures, and ensure continuity of service. Unless terrestrial networks, which can be vulnerable to natural disasters, 5G NTN offers enhanced resilience, ensuring the ongoing functioning of vital infrastructure and emergency response systems.

The government and defense sectors segment is anticipated to show significant growth during the study period. Satellite networks provide essential connectivity for remote military operations, border surveillance, and emergency communications. The increasing focus on space-based assets and the integration of satellites with terrestrial networks are fueling adoption in this segment.

SATELLITE NTN MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Satellite NTN Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 1.44 billion in 2025, representing 32.73% of the global market landscape, and is expected to reach USD 1.51 billion in 2026. The region leads the market, driven by its robust technological infrastructure, significant investments, and a favorable regulatory environment. The region benefits from early adoption and advanced development of 5G technology, which is increasingly integrated with satellite networks to extend coverage into remote and undeserved areas. Companies such as oneweb and Amazon are at the forefront of deploying large-scale LEO satellite constellations, supported by strong venture capital and strategic partnerships. The U.S. market is projected to reach USD 1.02 billion by 2026.

The U.S. government plays a vital role by streamlining licensing processes through the Federal Communication Commission (FCC), allocating spectrum resources, and promoting public-private collaboration.

Europe

Europe contributed 30.27% to the global market in 2025, with a valuation of USD 1.33 billion, and is projected to reach USD 1.39 billion in 2026. The European Union and national governments are investing in satellite projects to reduce reliance on foreign infrastructure and to ensure secure, high-speed broadband access across the continent. European companies are actively deploying multi-orbit satellite solutions and are involved in standardization efforts. The UK market is projected to reach USD 0.42 billion by 2026, while the Germany market is projected to reach USD 0.37 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 0.88 billion in 2025, representing 20.01% of the global market share, and is projected to reach USD 0.92 billion in 2026. The market in Asia Pacific is emerging as a high-growth region, accounting for a significant share during the study period. Rapid urbanization, increasing internet penetration, and government-led digital inclusion initiatives are key growth drivers. Countries such as India and China are ramping up investments in satellite-based services to enhance communication infrastructure. The Japan market is projected to reach USD 0.19 billion by 2026, the China market is projected to reach USD 0.25 billion by 2026, and the India market is projected to reach USD 0.23 billion by 2026.

Rest of the World

In 2025, the Rest of the World market stood at USD 0.75 billion, representing 17.00% of global demand, and is projected to grow to USD 0.77 billion in 2026. Rest of the World, which includes Latin America and Middle East & Africa, is experiencing increasing demand for mobile and internet connectivity in remote areas, driving expansion of the market. The Middle East & Africa is making substantial investments in satellite technology to support telecommunications and defense sectors. Latin America is witnessing growing demand for effective communication solutions; however, market penetration is challenged by funding constraints and regulatory barriers that limit broader adoption and deployment.

COMPETITIVE LANDSCAPE

Key Market Players

Key players Focus on Partnerships to Enhance Communication Network

Key players in the market are focused on strategic partnerships, with partnerships from both established aerospace companies and emerging tech-driven entrants. The market is currently dominated by companies investing in large-scale LEO constellations, Direct-to-Device (D2C) reliable connectivity, and integration with terrestrial 5G networks. Key growth drivers include the demand for global broadband coverage, expanding IoT connectivity needs, and increasing government/defense requirements for secure communication networks.

LIST OF KEY SATELLITE NTN PLAYERS PROFILED

- SpaceX (U.S.)

- OneWeb (U.K.)

- Amazon (U.S.)

- Airbus Defence and Space (Germany)

- AST SpaceMobile (U.S.)

- Telesat (Canada)

- SES (Luxembourg)

- Viasat (U.S.)

- Hughes Network Systems (U.S.)

- Apple Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025 – The telecommunications sector's first standardized billing framework for NTN connectivity has been introduced by Syniverse, the world's most connected company®, and Sateliot, the first business to provide 5G standard-based non-terrestrial networks (NTNs) on its low-Earth orbit (LEO) satellite constellation.

- January 2025 – Creotech Instruments SA, a major DeepTech player in Poland and Europe, signed a deal with the European Space Agency (ESA) to create essential elements that would facilitate the convergence of terrestrial private mmWave 5G networks with satellite-based 5G NTN (Non-Terrestrial Networks) services. The goal of the Creotech-led initiative is to assess the viability of extremely accurate time and frequency synchronization in mmWave 5G network infrastructure.

- October 2023 – The non-terrestrial network (NTN) service provider, Skylo Technologies, revealed a strategic alliance with Samsung Electronics' System LSI Business, a global leader in cutting-edge semiconductor technologies. By including NTN capability on Samsung's top 5G chipsets, which have been created specifically for seamless interoperability between cellular and Skylo's satellite network, this strategic partnership elevates the next generation of connectivity to new heights.

- March 2025 – Space42 and Viasat signed a memorandum of understanding (MOU) to explore collaboration prospects in creating a 5G non-terrestrial network (NTN) project.

- February 2025 – Eutelsat revealed the successful completion of the world’s first test of a 5G Non-Terrestrial Network (NTN) connection via its OneWeb network. OneWeb, a constellation of 654 small satellites in Low Earth Orbit (LEO), was commercially integrated with Eutelsat in 2023 and now operates as Eutelsat OneWeb.

REPORT COVERAGE

The report explores market segmentation, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. Besides this, the report offers insights into the global market trends, porter’s five forces analysis, supply chain trends, factors increasing demand for Satellite NTN, company profile and highlights key industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.46% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Orbit Type

|

|

By Architecture

|

|

|

By Application

|

|

|

By Service Type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market was valued at USD 4.59 billion in 2026 and is anticipated to reach USD 7.02 billion by 2034.

The market is likely to grow at a CAGR during the forecast period of 5.46%.

The top ten leading players are SpaceX (U.S.), OneWeb (U.K.), Amazon (U.S.), Airbus Defence and Space (Germany), AST SpaceMobile (U.S.), Telesat (Canada), SES (Luxembourg), Vaisat (U.S.), Hughes Network Systems (U.S.), and Apple Inc. (U.S.)

North America dominated the market in 2025.

Rise in growing global demand for broadband connectivity in remote and underserved regions is a key factor driving market growth.

Technical Complexity and regulatory Issues are key factors restraining market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us