Satellite Transponder Market Size, Share & Industry Analysis, By Type (Bent-Pipe Transponders and Regenerative Transponders), By Frequency Band (C- Band, Ku-Band, Ka-Band, X-Band, S-Band, & Others), By Application (Telecommunication, Internet Services, Broadcasting, Navigation & GPS, Scientific & Earth Observation, and Military & Defense Communication), By Service (Leasing, Custom Uplink/Downlink Management, Managed Network & Security Service, and Maintenance & Support), By Orbit (LEO, MEO, and GEO), By End User (Commercial, Government, and Military & Defense), & Regional Forecast, 2026-2034

Satellite Transponder Market Size and Future Outlook

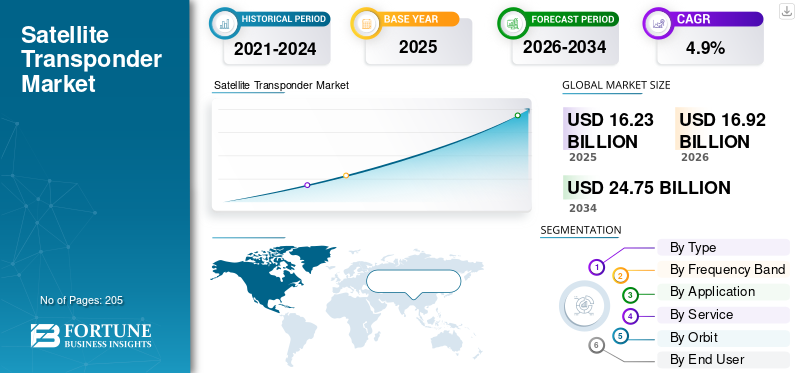

The global satellite transponder market size was valued at USD 16.23 billion in 2025. The market is projected to grow from USD 16.92 billion in 2026 to USD 24.75 billion by 2034, exhibiting a CAGR of 4.9% during the forecast period. North America dominated the global satellite transponder market with a market share of 32.16% in 2025.

A satellite transponder is a crucial system integrated into a communication satellite. It receives signals from the earth, amplifies and processes them, and then retransmits the signals back to the earth at a different frequency to prevent interference. Most modern communication satellites carry multiple transponders, each providing distinct bandwidth and power over designated frequency bands. Transponders are a critical system of satellite operations, as they support applications such as television broadcasting, data communications, internet services, and secure government networks.

The major players in the market include SES S.A., Intelsat S.A., Eutelsat Communications S.A., and others. These companies own extensive geostationary and Low Earth Orbit satellite fleets that support broadcasting, telecommunications, and broadband services worldwide. SES has a diversified satellite network and innovative O3b and SES-17 programs, which provide high-throughput and hybrid networking solutions. Intelsat offers fixed and on-demand transponders, focusing on mission-critical broadband and broadcast applications globally.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Demand for Global Broadband Connectivity in Remote and Underserved Regions to Drive Market Growth

A primary driver for the market is the increasing need for reliable broadband connectivity in remote and underserved regions worldwide. Terrestrial infrastructure limitations, especially in rural areas, maritime zones, and developing countries, create a critical demand gap for communications services. Satellite transponders, particularly those on high-throughput satellites, enable the delivery of high-speed internet, telecommunication, and broadcast services over vast geographic areas. This demand is fueled by the increasing digitalization, rising use of internet-based applications, and the growing consumption of multimedia content. Moreover, the government is also supporting programs to provide high speed internet in rural regions, which is expected to increase the demand for satellite transponders.

- For instance, in October 2025, Tamil Nadu announced the launch of BharatNet scheme to provide high-speed internet to rural households, targeting one crore homes per year by laying optical fiber cables across 12,525 gram panchayats.

MARKET RESTRAINTS:

High Capital Expenditure and Operational Costs to Limit Market Expansion

A significant restraint impacting the market is the high capital expenditure involved in launching, operating, and maintaining satellites. The construction, testing, and deployment of satellites require substantial investments for the development of advanced, high-throughput satellites equipped with multiple transponders. Such high financial requirements limit market entry and expansion opportunities, especially for smaller players and new entrants.

MARKET OPPORTUNITIES:

Expansion of High-Throughput Satellite (HTS) Technology Provides Significant Opportunities to the Market

The emergence and rapid adoption of High-Throughput Satellite (HTS) technology present a significant growth opportunity for the satellite transponder industry. HTS systems utilize advanced spot-beam and frequency reuse technologies to offer significantly higher data transmission capacities compared to traditional satellites. Thus, it enables satellite operators to provide faster, more reliable, and cost-effective broadband services globally. Such innovation encourages new commercial applications across aviation, maritime, defense, and other sectors that require high-capacity, low-latency connections.

- For instance, in September 2022, Hughes Communications India launched a High-Throughput Satellite (HTS) broadband internet service across the remote regions of India, utilizing ISRO's GSAT-11 and GSAT-29 geosynchronous satellites to provide bandwidths averaging 10 Mbps to underserved areas.

This expansion directly increases the demand for leased satellite transponder capacity, thereby bolstering the market by driving up the utilization of HTS-enabled bandwidth services in remote and hard-to-connect regions.

SATELLITE TRANSPONDER MARKET TRENDS:

Growing Integration of Satellite Networks with Terrestrial 5G and Edge Computing Infrastructure is a Significant Trend

Download Free sample to learn more about this report.

A significant trend influencing the market is the combination of satellite communications with terrestrial 5G and edge computing networks. This hybrid integration enables extended connectivity to remote and underserved regions, where traditional terrestrial infrastructure is limited or unavailable. With this combination of satellite coverage with edge computing capabilities, the service providers can offer lower latency and higher data processing efficiency closer to end-users. This development drives the design of advanced and sophisticated satellite transponders which can support diverse, high-throughput, and low-latency applications.

MARKET CHALLENGES:

Regulatory Complexities and Spectrum Licensing Issues to Present Challenges for the Market

One of the significant challenges hindering the market’s growth is the complex regulatory environment associated with spectrum licensing, frequency allocation, and coordination with international space agencies. These regulatory hurdles can cause delays in satellite launches, increase operational costs, and limit the flexibility of satellite operators in deploying and managing transponder capacity. Moreover, different regulations across countries create challenges for global operators in harmonizing transponder services efficiently, which may hinder the satellite transponder market growth.

Segmentation Analysis

By Type

Simple Design, Cost-Effectiveness, and High-Capacity Signal Transmission Efficiency Drive Bent-Pipe Transponders Segment Growth

On the basis of type, the market is bifurcated into bent-pipe transponders and regenerative transponders.

The bent-pipe transponders segment holds the largest share in the market. These transponders are widely used for various reasons, including their simple design, cost-effectiveness, and ability to transmit signals back to the earth with minimal processing. They offer large capacity and are less costly due to their simpler design. Therefore, these factors are responsible for the bent pipe transponders used in broadcast, telecom, and legacy satellite applications, which drives the growth of the segment.

- For instance, in August 2023, EM Solutions completed the initial in-orbit tests of its flexible bent pipe transponder aboard Telesat’s LEO 3 demonstration satellite. The compact Ka and V/Q-band payload supports a range of broadband SATCOM applications.

The regenerative transponders segment is the fastest-growing segment of the market, driven by its increased demand in the future due to the ability to efficiently utilize the bandwidth and power necessary for modern high-throughput satellites that handle data-intensive services. These types of transponders perform onboard signal processing including demodulating, cleaning, and re-encoding the digital signal before retransmission. Thus, such advantages offered by this transponder type makes them critical system for future satellite networks. The segment is expected to record the highest CAGR of 5.4% during the forecast period.

By Frequency Band

Surge in Demand for Reliable, Weather-Resilient Satellite TV & Enterprise Data Communications Band Supports Ku-band Segment Growth

Based on frequency band, the market is segmented into C- Band, Ku-Band, Ka-Band, X-Band, S-Band, and others.

The Ku-band segment acquires the largest share in the market due to the rising need for a reliable frequency band for satellite TV, VSAT, and enterprise data communications. The Ku band has extensive global deployment recognized for its balance of data and speed in an optimal manner as well as its weather resilience. Thus, the well-established ecosystem of this band enables the efficient scaling of existing infrastructure and integration with emerging technologies.

- For instance, in July 2024, SpaceX’s Falcon 9 launched Türksat 6A, Turkey’s first domestically built GEO Comsat, carrying 16 Ku-band transponders (plus spares) for commercial and civil telecoms and an additional X-band payload for military use.

The Ka-band segment is the fastest-growing segment of the market due to its ability to work with intensive bandwidth. Moreover, transponders installed in Ka-band satellites are widely utilized for low-latency applications such as 5G backhaul, satellite internet, telemedicine, and IoT connectivity. Therefore, these factors are expected to stimulate the segmental growth. The Ka-band segment is expected to grow with the highest CAGR of 6.3% over the forecast period.

By Application

Cost-Effective High-Definition and Ultra HD Content Delivery across Regions Fuels Broadcasting Segment Growth

Based on application, the market is segmented into telecommunication, internet services, broadcasting, navigation & GPS, scientific and earth observation, and military & defense communication.

The broadcasting segment accounted for majority of the satellite transponder market share in 2025, driven by an increasing demand for high definition and ultra-high definition content delivery across wider geographic regions. Satellite transponders enable cost-effective, reliable Direct-to-Home (DTH) and Digital Terrestrial Television (DTT) services in remote and underserved areas. Thus, there is a significant rise in the demand for transponder capacity to support diverse broadcasting needs and expanding coverage areas, which directly fuels the growth of the segment.

- For instance, in January 2025, Qatar’s Es’hailSat signed a multi-year, multi-transponder agreement with Morocco’s national broadcaster SNRT to expand Direct-to-Home, Digital Terrestrial Television, and video contribution services across the Middle East and North Africa region using the Es’hail-1 satellite.

The internet services segment is growing at the fastest growth rate due to the need for broadband connectivity in rural, maritime, and aviation sectors where traditional fiber networks are difficult to deploy. Moreover, the constant expansion of satellite constellations, including hybrid LEO/MEO/GEO networks, allows flexible bandwidth allocation and scaling of dynamic network driving segment growth in future. The segment is anticipated to record the highest CAGR of 6.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service

Rising Demand for Flexible Satellite Bandwidth to Drive Leasing Segment Growth

Based on service, the market is segmented into leasing, custom uplink/downlink management, managed network & security services, and maintenance & support.

The leasing segment holds the largest share of the market, as more telecom operators, broadcasters, and enterprises move toward flexible satellite bandwidth access for varying capacity needs without a heavy investment. This model supports complex telecommunications applications and hybrid networks, driving the demand for diverse and customizable satellite transponder packages. There is a rise in bandwidth leasing contracts to provide fixed data services in underserved and remote regions.

- For instance, in May 2024, Eutelsat Group and InterSAT finalized the leasing of additional Ku-band capacity on the EUTELSAT 7C satellite through a new multi-year agreement. This enhances fixed data services across Central and Eastern Africa.

The managed network & security services segment is the fastest-growing segment in the market, as operators and enterprises seek end-to-end solutions that ensure secure, resilient, and optimized network performance. Satellite networks face growing cybersecurity threats. This highlights the importance of integrating advanced encryption, threat detection, and response mechanisms within managed services. The segment is likely to display a considerable CAGR of 6.2% during the forecast period.

- For instance, in May 2025, Agility Beyond Space (ABS) and SpaceBridge entered into a strategic collaboration to enhance managed satellite transponder services across the Europe, the Middle East, and Africa region, with a focus on broadband and internet trunking.

By Orbit

Growing Demand for Wide-area Broadcast Coverage and Enhanced Payload Technologies Combine to Drive GEO Segment Growth

Based on orbit, the market is segmented into Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Orbit (GEO).

The GEO satellite holds the largest share of the market, as the satellites in this orbit can provide fixed, wide-area coverage with consistent, reliable connectivity, which is needed for broadcast. The expansion of satellite constellations drives the installation of GEO payload enhancements, including regenerative transponders, which is expected to propel segment growth.

- For instance, in August 2023, Panasonic Avionics announced a major expansion of its GEO Ku-band satellite capacity, adding new HTS and XTS Ku-band beams to boost in-flight internet speeds over China, Japan, and wider Asia Pacific. Such expansion involves additional Ku-band transponder capacity on multiple GEO satellites to increase throughput for airline customers.

The LEO segment is the fastest-growing in the market, due to its low-latency, high-capacity capabilities, catering especially to data-intensive commercial broadband, IoT, and mobile communications with global coverage. LEO constellations are preferred for real-time applications such as autonomous vehicles, gaming, and remote operations that require minimal delay. This segment is estimated to record the highest CAGR of 7.4% over the forecast period.

By End User

Increased Demand for High-Bandwidth Broadband, 5G Backhaul, and Enterprise VSAT Solutions to Drive Commercial Segment Growth

Based on end user, the market is segmented into commercial, government, and military & defense.

The commercial segment holds the largest share of the market due to the expanding adoption of satellite services by consumers and enterprises for broadband, media streaming, and cloud connectivity. The rise in the use of satellite internet, 5G backhaul, and enterprise VSAT solutions, which require higher bandwidth, drive the demand for satellite transponders in commercial communication applications.

The military & defense segment is the fastest-growing in the market, due to rising demand for secure, resilient, and globally scalable communication networks that support sophisticated command, control, and intelligence systems. The rise in need for satellite transponders for tactical data links, surveillance, and secure voice/data transmission across various defense sectors is expected to accelerate the market growth. The segment is anticipated to grow at the highest CAGR of 5.9% during the forecast period.

- For instance, in April 2025, Intelsat was awarded a contract by the U.S. Space Force (USSF) to provide commercial satellite communications bandwidth, equipment, and services to the U.S. Department of Defense for global maritime operations.

Satellite Transponder Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America dominated the market with a value of USD 5.22 billion in 2025. The market in the region is growing due to the increasing demand for Direct-to-Home (DTH) broadcasting services. The presence of key players such as Intelsat and EchoStar in the U.S. and Telesat in Canada has increased the regional market share. Moreover, rising investments in High-Throughput Satellites (HTS) and the adoption of advanced Ku-band and Ka-band frequencies support growing bandwidth demands. In addition, major players in the market are working on the expansion of high speed broadband and digitalization, which drives market growth during the forecast period.

- For instance, in June 2022, SES announced that SES-17, SES's newest geostationary Ka-band high-throughput satellite is operational over the Americas and the Caribbean, featuring nearly 200 digital transponder-powered user beams capable of delivering up to 2 Gbps per connection.

Europe

The market in Europe is experiencing steady growth, driven by an increasing demand for high-quality satellite communication services and the expansion of digital television broadcasting. European Union (EU) initiatives that promote the deployment of advanced satellite infrastructure, along with public-private partnerships, are key factors supporting market expansion. Countries such as the U.K., Germany, and others in the region are investing heavily in secure communication infrastructure and uninterrupted high-quality satellite broadcast services.

- For instance, in October 2025, SES renewed its multi-year, multi-million contract with Arqiva for satellite capacity on SES’s prime video neighborhood at 28.2 degrees East, continuing to provide multi-transponder bandwidth. This agreement enables Arqiva to deliver a wide range of SD and HD TV channels as well as radio services to over 10 million households across the U.K. and Ireland.

Asia Pacific

The Asia Pacific satellite transponder market is anticipated to witness rapid growth, driven by a surge in the demand for satellite-based communication, particularly in rural and remote areas. The rapid development of digital infrastructure in China, India, and Japan is driving the adoption of high-throughput satellite services. Such advancements will significantly enhance broadband connectivity and DTH broadcasting, fueling the demand for satellite transponder services. The rapid integration of satellite and 5G networks for seamless global broadband connectivity is expected to drive market expansion in the region.

- For instance, in October 2025, China Satellite Network Group (China SatNet) conducted the world's first direct 5G satellite-to-phone video call, connecting a smartphone directly to a Low Earth Orbit (LEO) satellite without ground infrastructure, in compliance with 3GPP Release 17 standards.

This innovation is expected to push the growth of the market by increasing demand for transponder capacity to support large LEO constellations and direct-to-device communication networks.

Latin America and the Middle East & Africa

The market in Latin America and the Middle East & Africa is growing due to increasing investments in telecom infrastructure, expanding broadband coverage, and the rising demand for cost-effective backhaul solutions in remote locations in Latin America. Government and military spending, along with growth in the oil and gas sectors in the Middle East region, are further driving the demand for reliable satellite-based communication.

COMPETITIVE LANDSCAPE

Key Industry Players:

Technological Innovation, Multi-Orbit Satellite Networks, and Strategic Partnerships Drive Competitive Dynamics in the Market

The market is moderately consolidated, dominated by the global satellite operators and communication technology providers. These players offer transponder capacity leasing, payload innovation, and network service integration to both commercial and military sectors.

Leading market participants include SES S.A., Intelsat Corporation, Eutelsat Communications, Telesat Canada, EchoStar Corporation, and Hispasat S.A. These companies operate extensive satellite fleets, providing global coverage and offering varied transponder services across the broadcasting, telecommunications, and broadband sectors. These firms maintain a competitive advantage by investing heavily in digital payload technology, expanding multi-orbit satellite constellations, and offering customized leasing packages that address evolving market demands.

LIST OF KEY SATELLITE TRANSPONDER COMPANIES PROFILED:

- SES S.A. (Luxembourg)

- Intelsat (U.S.)

- Eutelsat Communications SA (France)

- Telesat (Canada)

- HISPASAT, S.A. (Spain)

- Echostar Corporation (U.S.)

- Embratel (Brazil)

- Thaicom Public Company Limited (Thailand)

- APSTAR (Hong Kong)

- Viasat, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: SES and Arqiva concluded a new multi-year, multi-million-euro capacity renewal in which SES will continue to supply multi-transponder capacity at 28.2°E, supporting SD/HD TV and radio distribution for Arqiva’s broadcast customers in the U.K. and Ireland.

- January 2025: Es’hailSat signed a multi-year, multi-transponder deal with Morocco’s public broadcaster SNRT to provide DTH, DTT satellite transponder capacity. This agreement also includes video contribution services from Es’hail-1 at 25.5°E for audiences across North Africa and the wider Middle East and North Africa footprint.

- October 2024: SES and Sky extended their long-standing partnership through a multi-year renewal to provide multi-transponder capacity at 28.2°/28.5°E, ensuring continued delivery of Sky Q channels and backup services.

- September 2024: Eutelsat was selected by TVPlus in a multi-year, multi-transponder agreement on EUTELSAT 172B to deliver around 60 DTH channels across Australia and New Zealand.

- January 2024: Viasat Energy expanded its multi-transponder satellite services agreement with Es’hailSat, adding multiple Ku-band transponders on Es’hail-1 plus Doha teleport services to boost VSAT connectivity for energy-sector customers across the Middle East and North America regions.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all market segments included in the report. It includes details on market dynamics and market trends expected to drive the market during the forecast period. The market report includes Porter’s five forces analysis, which illustrates the potency of buyers and suppliers in the market. The market forecast provides information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers, and acquisitions. The market analysis also encompasses a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By Frequency Band

By Application

By Service

By Orbit

By End User

By Geography North America (By Type, By Frequency Band, By Application, By Service, By Orbit, By End User, and Country)

Europe (By Type, By Frequency Band, By Application, By Service, By Orbit, By End User, and Country)

Asia Pacific (By Type, By Frequency Band, By Application, By Service, By Orbit, By End User, and Country)

Latin America (By Type, By Frequency Band, By Application, By Service, By Orbit, By End User, and Country)

Middle East & Africa (By Type, By Frequency Band, By Application, By Service, By Orbit, By End User, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 16.23 billion in 2025 and is projected to reach USD 24.75 billion by 2034.

In 2025, the market value of North America stood at USD 5.22 billion.

The market is growing at a CAGR of 4.9% during the forecast period of 2026-2034.

The broadcasting segment led the market by application in 2025.

The key factors driving the market are rising demand for global broadband connectivity in remote and underserved regions.

SES S.A., Intelsat, Eutelsat Communications SA, and Telesat are some of the prominent players in the market.

North America dominated the market in 2025 with the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us