Scleroderma Therapeutics Market Size, Share & Industry Analysis, By Drug Class (Endothelin Receptor Antagonists (ERAs), Phosphodiesterase-5 (PDE-5) Inhibitors, Prostacyclin Pathway Agents, Immunosuppressants, Interleukin-6 (IL-6) Inhibitors, Antifibrotic Agents), By Disease Indication (Systemic Scleroderma & Localized Scleroderma), By Age Group (Pediatric, Adult, & Geriatric), By Type (Branded & Generic), By Route of Administration (Oral, Intravenous, Subcutaneous, Topical), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), & Regional Forecast, 2026-2034

Scleroderma Therapeutics Market Size and Future Outlook

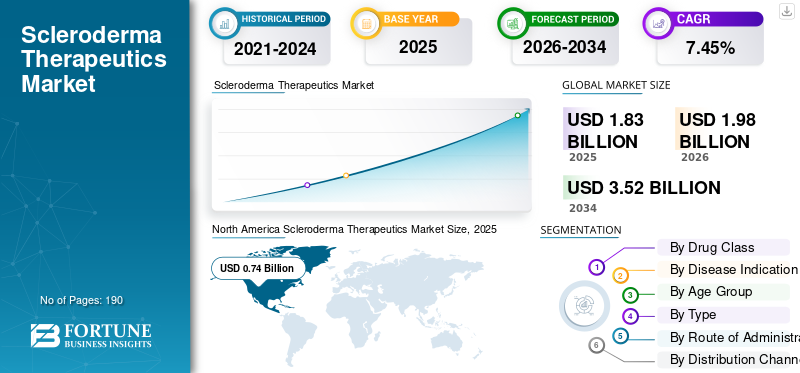

The global scleroderma therapeutics market size was valued at USD 1.83 billion in 2025. The market is projected to grow from USD 1.98 billion in 2026 to USD 3.52 billion by 2034, exhibiting a CAGR of 7.45% during the forecast period. North America dominated the scleroderma therapeutics market with a market share of 40.43% in 2025.

The global market is expected to grow steadily, driven by the ongoing need for advanced therapies to manage fibrosis, inflammation, vascular complications, and organ damage associated with systemic sclerosis. As diagnosis improves and physicians identify patients earlier, demand is increasing for treatments that can slow lung function decline, control disease progression, and support long-term symptom management. At the same time, ongoing clinical research and label expansion activities are strengthening industry interest, as companies witness a clear opportunity to address a high unmet need in the rare and complex autoimmune disease market. Approved therapies such as OFEV and ACTEMRA already have positions in SSc-ILD, showing that the market is moving beyond supportive care toward more targeted therapies.

Key companies such as Boehringer Ingelheim International GmbH, F. Hoffmann-La Roche Ltd., and Kyowa Kirin Co., Ltd., are focusing on expanding their offerings and investing in research and pipeline expansion, followed by regulatory approval, to boost their respective positions.

- For instance, in June 2025, Galderma initiated two new clinical trials investigating nemolizumab in patients with systemic sclerosis (SSc) and chronic pruritus of unknown origin. The development highlighted how companies are expanding pipeline activity in scleroderma-related indications to address unmet clinical needs and build future growth opportunities in the market.

Download Free sample to learn more about this report.

SCLERODERMA THERAPEUTICS MARKET TRENDS

Rising Focus on Targeted Therapies for Scleroderma is an Emerging Trend Observed

The global scleroderma therapeutics market is witnessing a clear shift toward targeted treatment development, as companies are moving beyond broad immunosuppression and focusing on therapies that intervene more precisely in the immune and fibrotic mechanisms underlying systemic sclerosis. This trend is increasing market interest as targeted approaches have the potential to improve clinical outcomes, address high unmet needs, and create stronger differentiation in a rare disease area with limited approved options.

As more companies invest in advanced biologics, cell therapies, and mechanism-based programs, the market is gradually evolving from supportive disease management toward more specialized and innovation-driven treatment strategies.

- For instance, in March 2026, Quell Therapeutics Ltd announced the initiation of the phase 1/2 CHILL study of QEL-005 in patients with refractory rheumatoid arthritis and systemic sclerosis, following CTA approval in the U.K. Such developments are expanding the innovation pipeline and reinforcing the market’s shift toward more precise, next-generation treatment approaches.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Burden of Systemic Sclerosis is Driving Product Demand

A key factor driving the global scleroderma therapeutics market growth is the rising burden of systemic sclerosis and its progression to serious organ complications such as interstitial lung disease, pulmonary arterial hypertension, gastrointestinal involvement, and renal complications. As these complications increase disease severity, hospitalization risk, and long-term treatment needs, physicians are placing greater focus on earlier diagnosis and proactive therapeutic intervention. These factors drive demand for drugs that can slow lung function decline, modulate immune activity, and manage organ-specific complications, thereby supporting market growth. Key companies are focusing on the research and development of innovative therapies to meet these clinical needs.

- For instance, in December 2024, Zura Bio Limited launched its global Phase 2 TibuSURE study evaluating tibulizumab in adults with systemic sclerosis. The development reflected the growing burden of systemic sclerosis and its organ-related complications, encouraging innovation, which, in turn, strengthened market growth momentum.

MARKET RESTRAINTS

Limited Availability of Disease-modifying Therapies is Restricting Market Expansion

A major factor restraining market growth is the limited availability of disease-modifying therapies for systemic sclerosis. Treatment options are still limited, and most currently available therapies are used to manage specific complications such as interstitial lung disease, pulmonary arterial hypertension, skin involvement, or inflammation rather than controlling the full progression of the disease. This creates a gap in treatment outcomes, as physicians often rely on symptom-focused or organ-based management instead of broad disease-modifying intervention. As a result, treatment response remains inconsistent across patients, long-term disease control remains difficult, and commercial expansion is slower than in autoimmune markets. Furthermore, the lack of consistently positive late-stage clinical trial outcomes has hindered the development of breakthrough therapies, thereby hampering market growth.

- For instance, in September 2020, Corbus Pharmaceuticals Holdings, Inc. initiated its Phase 3 RESOLVE-1 study evaluating Lenabasum in patients with systemic sclerosis, but the study did not show significant differences in primary or secondary endpoints compared with placebo. This outcome highlighted the difficulties associated with developing effective disease-modifying therapies for systemic sclerosis and reinforced a key market restraint that continues to slow treatment expansion in this field.

MARKET OPPORTUNITIES

High Unmet Need for Disease-modifying Therapies is Creating Strong Growth Opportunities

The global scleroderma therapeutics market is creating strong growth opportunities, as there are still very limited therapies that can meaningfully alter the overall course of systemic sclerosis. Most currently used treatments focus on managing specific complications, such as vascular complications, or inflammation. This treatment gap is increasing demand for newer therapies that can address fibrosis, immune dysfunction, and broader disease progression more effectively. As a result, companies are recognizing stronger commercial potential in this space, as any therapy demonstrating meaningful efficacy in systemic sclerosis can attract physician interest, regulatory attention, and premium rare-disease positioning. Published research also continues to describe systemic sclerosis as a disease area with a high unmet need, especially due to its heterogeneity, significant organ damage burden, and lack of broadly effective disease-modifying therapies.

- For instance, in February 2025, Adicet Bio, Inc. announced that the U.S. FDA granted Fast Track Designation to ADI-001 for the treatment of systemic sclerosis (SSc). This development represents a positive market signal, showing regulatory recognition of the significant unmet need in this disease area, which can help accelerate development timelines and strengthen investor and industry confidence. In turn, such progress expands future growth opportunities by encouraging continued innovation in disease-modifying and next-generation therapies for scleroderma.

MARKET CHALLENGES

Complex Trial Design and Limited Biomarker Validation Remain a Key Market Challenge

The global scleroderma therapeutics market faces a major challenge, as conducting clinical trials in systemic sclerosis is difficult and interpreting trial results is even harder. The disease is highly heterogeneous, with progression varying widely from one patient to another, and patient pools remain relatively small, making it difficult to select uniform trial populations and generate clear efficacy signals. At the same time, biomarker development is still evolving, and the market lacks widely validated biomarkers that can consistently predict progression, treatment response, or the appropriate patient subgroup. Due to these limitations, companies face higher development risks, longer timelines, and a greater chance of late-stage clinical trial setbacks, which ultimately slow innovation and delay the introduction of new therapies.

- For instance, in September 2025, Springer Nature published an article titled ‘‘Revolutionizing Clinical Trials in Systemic Sclerosis” highlighted that several recent clinical studies have produced negative results. The study also highlighted that endpoint selection, patient selection, and trial design remain major barriers in this disease area. These findings reinforce the market challenge, as limited trial optimization tools and incomplete biomarker validation continue to make successful product development more difficult.

Segmentation Analysis

By Drug Class

Strong Clinical Reliance on Immunosuppressants for Disease Management to Boost Segment Growth

Based on drug class, the market is categorized into Endothelin Receptor Antagonists (ERAs), phosphodiesterase-5 (PDE-5) inhibitors, prostacyclin pathway agents, immunosuppressants, interleukin-6 (IL-6) inhibitors, antifibrotic agents, and others.

The immunosuppressants segment is poised to dominate the market. The segment dominates as systemic scleroderma is driven by immune dysfunction and chronic inflammation, prompting physicians to rely on immunosuppressive therapies to control skin involvement, interstitial lung disease, and overall disease activity. Drugs such as mycophenolate mofetil, cyclophosphamide, and rituximab remain central to treatment practice, especially for patients with progressive or organ-involved disease. As these therapies are already integrated into routine management and are used across a broad portion of the treatable patient population, they continue to account for a larger share of prescribing compared with newer, more selective options. This strong clinical dependence has helped the segment maintain its market leadership. Underscoring their continued importance, key companies are focusing on research and development activities to refine this drug class and offer innovative products.

- For instance, in October 2025, Bristol Myers Squibb presented encouraging Phase 1 Breakfree-1 data in chronic autoimmune diseases, including systemic sclerosis, stating that 94% of evaluable patients remained off chronic immunosuppressive therapy at the time of analysis. These developments highlight how the market is still shaped by immunosuppression-based care strategies.

The interleukin-6 (IL-6) inhibitors are expected to grow at a CAGR of 11.57% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Higher Treatment Intensity of Systemic Scleroderma Encouraged the Segment Growth

Based on disease indication, the market is segmented into systemic scleroderma and localized scleroderma.

In 2025, the systemic scleroderma segment dominated the market. It represents the more severe, clinically significant form of the disease, with involvement extending beyond the skin into organs such as the lungs, heart, kidneys, and gastrointestinal tract. This leads to higher treatment intensity, longer duration of therapy, and greater use of advanced drugs. As a result, systemic scleroderma contributes the largest share of drug demand, especially due to complications such as SSc-ILD and pulmonary vascular disease, which require continuous specialist treatment. These factors are encouraging key players to invest in developing innovative therapies for the disease.

- For instance, in July 2025, Adicet Bio, Inc. announced that the first systemic sclerosis patient was dosed in the second cohort of its ongoing Phase 1 clinical trial of ADI-001 in autoimmune diseases.

The localized scleroderma segment is projected to grow at a CAGR of 5.17% during the forecast period.

By Age Group

Adult Segment Dominated due to Higher Disease Prevalence and Treatment Demand

Based on age group, the market is segmented into pediatric, geriatric, and adult.

In 2025, the adult segment dominated the market, as systemic scleroderma primarily affects patients in adulthood. Additionally, most diagnosed patients requiring long-term pharmacological management fall within this age group. Adults receive continuous therapy for skin fibrosis, interstitial lung disease, vascular complications, and other organ complications, which makes them the primary revenue-generating population in the market. Ongoing clinical studies focusing on adult patients further strengthen this segment’s leading position.

- For instance, in December 2024, Zura Bio Limited launched its global Phase 2 TibuSURE study, evaluating tibulizumab in adults with systemic sclerosis. The development reflects a strong clinical and commercial focus on adult patients, reinforcing why this segment holds the leading share.

The geriatric segment is projected to grow at a CAGR of 8.46% during the forecast period.

By Type

Branded Segment Led the Market, driven by High-Value Branded Therapies

Based on type, the market is segmented into branded and generic.

In 2025, the branded segment dominated the market, as a limited number of high-value branded therapies continue to shape the scleroderma therapeutics landscape. Approved products, such as OFEV for SSc-ILD and other branded biologic options used in systemic sclerosis-related care benefit from strong physician recognition, greater clinical confidence, and well-established positioning within specialist treatment pathways. In addition, a large portion of the development pipeline is focused on novel biologics, cell therapies, and rare-disease products, leading market value being increasingly driven by branded therapies. This structure has helped branded products maintain their leading position. Additionally, regulatory approvals from governing bodies continue to strengthen segment growth.

- For instance, in February 2025, Adicet Bio, Inc. received Fast Track Designation from the U.S. FDA for ADI-001 to treat systemic sclerosis. The development supports the dominance of branded products, as the pipeline is increasingly built around innovative, premium-positioned therapies that reinforce the commercial importance of branded products in the market.

The generic segment is projected to grow at a CAGR of 5.75% during the forecast period.

By Route of Administration

Oral Segment Led the Market due to Convenience

Based on route of administration, the market is segmented into oral, intravenous, subcutaneous, topical, and others.

In 2025, the oral segment dominated the market. Several commonly used therapies for scleroderma treatment and complication management are available in oral form, making long-term administration easier in outpatient settings. Oral therapies offer better convenience, reduce administration burden, and support regular chronic use, especially in adults. This ease of use improves patient acceptance and prescription continuity. As scleroderma is usually managed over a long period, convenience-driven oral treatments have remained commercially strong.

- For instance, in March 2025, Boehringer Ingelheim International GmbH received approval from the European Commission for OFEV, indicated for children and adolescents aged 6 to 17 years with progressive fibrosing ILDs and for SSc-ILD in pediatric patients. As an oral therapy, this label expansion underscores the continued role of oral treatment formats in broadening access and supporting long-term disease management in the market.

The others segment is projected to grow at a CAGR of 10.47% during the forecast period.

By Distribution Channel

Retail Pharmacies Segment Dominated due to its Ability to Improve Geographic Access

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others.

The retail pharmacies segment accounted for the largest scleroderma therapeutics market share. Many scleroderma patients are treated outside the hospital setting and require repeated dispensing of long-term therapies, especially oral maintenance drugs and chronic complication-management medicines. Retail and specialty retail pharmacy networks improve refill convenience, geographic access, patient counseling, and therapy continuity, making them highly relevant for chronic rare-disease treatment pathways.

- For instance, in August 2025, Walgreens Specialty Pharmacy expanded its drug distribution network to 265 products, strengthening its position in dispensing complex therapies for patients with rare disease states and chronic conditions. The development supported the role of retail pharmacy channels in specialty therapeutics, as wider specialty retail access helps improve continuity, convenience, and patient reach for long-term disease management.

The online pharmacies segment is projected to grow at a CAGR of 11.83% over the study period.

Scleroderma Therapeutics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Scleroderma Therapeutics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market held the dominant share in 2024 at USD 0.69 billion and maintained its leading position in 2025 at USD 0.74 billion. The region is witnessing growth due to higher diagnosis rates, stronger specialist access, and earlier treatment of serious complications such as SSc-ILD, which remains a major cause of morbidity and mortality. Wider use of approved and guideline-supported therapies is also supporting demand across the region.

U.S. Scleroderma Therapeutics Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 0.72 billion by 2026, accounting for roughly 36.60% of the global sales.

Europe

Europe is projected to grow at a CAGR of 6.97% over the coming years, the second-highest among all regions. The market is expected to reach a valuation of USD 0.56 billion by 2026. Growth in the region is supported by greater clinical focus on early screening, multidisciplinary management, and broader adoption of treatments for organ complications, especially lung involvement.

U.K. Scleroderma Therapeutics Market

The U.K. market is estimated at around USD 0.11 billion in 2026, representing roughly 5.78% of the global market.

Germany Scleroderma Therapeutics Market

Germany's market is projected to reach approximately USD 0.14 billion by 2026, equivalent to around 6.85% of the global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.43 billion by 2026 and secure the position of the third-largest region in the market. The market is growing as awareness, epidemiological research, and the diagnosis of systemic sclerosis are improving across the region, making the patient population more visible for treatment in the region.

Japan Scleroderma Therapeutics Market

The Japanese market is estimated to touch around USD 0.09 billion by 2026, accounting for approximately 4.75% of the global sales.

China Scleroderma Therapeutics Market

China's market is projected to be one of the largest worldwide, with 2026 revenue estimates at around USD 0.14 billion, representing approximately 6.86% of global sales.

India Scleroderma Therapeutics Market

The Indian market is estimated at around USD 0.04 billion by 2026, accounting for roughly 2.09% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.13 billion during the study period. Growth is being driven by improving recognition of rare autoimmune diseases, gradual expansion of specialist care, and increasing need to manage severe systemic complications earlier.

In the Middle East & Africa, the GCC is set to reach USD 0.03 billion by 2026.

South Africa Scleroderma Therapeutics Market

The South African market is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.94% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Emphasize Strategic Collaborations to Boost Their Market Position

The global scleroderma therapeutics market is semi-consolidated, with companies such as Boehringer Ingelheim International GmbH, F. Hoffmann-La Roche Ltd., and Kyowa Kirin Co., Ltd., holding significant global scleroderma therapeutics market share, alongside other emerging players. Strategic partnerships, new product launches, and regulatory approvals in the sector drive these companies' market share gains.

- For instance, in December 2021, Kyowa Kirin Co., Ltd. announced that it had filed an application with the Japanese Ministry of Health, Labor and Welfare for a partial change in the approved indication of LUMICEF [KHK4827, generic name: brodalumab (genetical recombination)] for systemic sclerosis in Japan.

Other notable players in the global market include GALDERMA, Adicet Bio, Zura Bio Ltd., and Novartis AG. These companies are expected to prioritize strategic collaborations and new product launches to strengthen their market positions during the forecast period.

LIST OF KEY SCLERODERMA THERAPEUTICS COMPANIES PROFILED

- Boehringer Ingelheim International GmbH (Germany)

- Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Cumberland Pharmaceuticals Inc. (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

- GALDERMA (Switzerland)

- Zura Bio Ltd. (U.K.)

- Adicet Bio (U.S.)

- Certa Therapeutics (Australia)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Boehringer Ingelheim acquired an exclusive license for a preclinical, small-molecule program from Sitryx Therapeutics. The program offered a novel, oral, potentially disease-modifying treatment approach across multiple autoimmune and inflammatory disease indications.

- February 2026: Adicet Bio, Inc. received Fast Track Designation from the U.S. FDA for ADI-001 for the potential treatment of adult patients with systemic sclerosis (SSc).

- October 2025: Merck & Co., Inc. received approval from the U.S. FDA for the U.S. product label based on the Phase 3 ZENITH trial for WINREVAIR. WINREVAIR, an activin signaling inhibitor, is indicated for the treatment of adults with pulmonary arterial hypertension to improve exercise capacity and WHO functional class (FC), and to reduce the risk of clinical worsening events, including hospitalization for PAH, lung transplantation, and death.

- July 2025: Adicet Bio, Inc. dosed its first systemic sclerosis (SSc) patient in the second cohort of the Phase 1 clinical trial evaluating ADI-001 in autoimmune diseases.

- December 2024: Zura Bio Limited launched TibuSURE, a Phase 2 global study evaluating tibulizumab for the treatment of systemic sclerosis (SSc) in adults.

REPORT COVERAGE

The report provides a detailed global analysis of the scleroderma therapeutics market, focusing on the major clinical and commercial factors shaping market growth. It covers market size and forecast assessment, key growth drivers, restraints, challenges, and emerging opportunities influencing the competitive landscape. The study also examines how rising scleroderma prevalence, the growing adoption of targeted biologics, and the continued need for long-term disease control are driving market expansion. In addition, it reviews recent developments, including product approvals, label expansions, clinical progress, collaborations, partnerships, and acquisitions, that are influencing competition and future growth across the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.45% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.83 billion in 2025 and is projected to reach USD 3.52 billion by 2034.

In 2025, the market value stood at USD 0.74 billion.

The market is expected to grow at a CAGR of 7.45% over the forecast period.

By drug class, the immunosuppressants segment is expected to lead the market.

The rising burden of systemic sclerosis-related organ complications is the key factor driving the market.

Boehringer Ingelheim International GmbH, F. Hoffmann-La Roche Ltd., and Kyowa Kirin Co., Ltd., are the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us