Shotcrete Market Size, Share & Industry Analysis, By Process (Dry Mix and Wet Mix), By Application (Underground Construction, Water Retaining Structures, Repair and Rehabilitation, Protective Coatings, and Others), and Regional Forecast, 2026-2034

SHOTCRETE MARKET SIZE AND FUTURE OUTLOOK

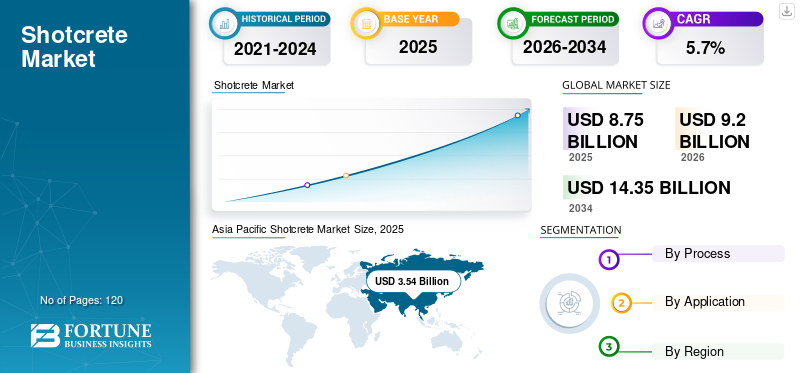

The global shotcrete market size was valued at USD 8.75 billion in 2025. The market is projected to grow from USD 9.20 billion in 2026 to USD 14.35 billion by 2034 at a CAGR of 5.7% during the forecast period. Asia Pacific dominated the shotcrete market with a market share of 40.46% in 2025.

The global shotcrete (sprayed concrete) market is a specialized, application-driven segment within concrete construction, enabling rapid placement, adhesion, and structural build-up on complex geometries such as tunnel crowns, vertical faces, and irregular rock surfaces. It is not a discretionary material choice in many cases; rather, it is a construction method that improves cycle time, ground stabilization, and structural rehabilitation performance, particularly where conventional formwork and cast-in-place concreting are impractical.

The market growth is closely linked to underground construction activity, asset rehabilitation cycles, and water infrastructure expansion, with value growth influenced by specification intensity (fiber reinforcement, accelerators, low-rebound mixes, and mechanized spraying). The segment process indicates the market is structurally weighted toward wet mix, reflecting higher adoption in mechanized and higher-volume works, while underground construction dominates application demand, keeping the market tightly correlated with tunneling, mining development, and underground transit projects. Key players operating in the market include Sika AG, Master Builders Solutions, Normet Group, Putzmeister, Mapei Group, among others.

Download Free sample to learn more about this report.

Shotcrete Market Key Takeaways

- 2025 Market Size: USD 8.75 billion

- 2026 Market Size: USD 9.20 billion

- 2034 Forecast Market Size: USD 14.35 billion

- CAGR: 5.7% from 2026-2034

- Asia Pacific dominated the shotcrete market with a 40.46% share in 2025.

- The wet mix segment held the dominant market share in 2025.

- The repair and rehabilitation segment accounted for a significant market share in 2025.

Asia Pacific

Asia Pacific led the market due to increasing underground infrastructure and rehabilitation projects.

North America

North America is growing steadily with rising investments in structural rehabilitation and tunneling activities.

Europe

Europe is witnessing strong demand driven by renovation projects and stringent quality standards.

U.S.

The market reached USD 1.40 billion in 2025, supported by strong residential and commercial construction activity.

Japan

Infrastructure maintenance and tunnel development projects are driving demand for shotcrete solutions.

Read More

SHOTCRETE MARKET TRENDS

Wet-Mix Mechanization and Productivity Optimization is a Key Market Trend

The wet-mix product continues to expand its value share as modern projects increasingly prioritize consistent quality, higher output rates, and reduced rebound/waste. Mechanized spraying systems, improved pumpability, and jobsite digital controls are driving adoption in large infrastructure projects, especially underground works, where schedule adherence and safety are central.

In parallel, the market is seeing stronger pull for fiber-reinforced shotcrete, alkali-free accelerators, and performance-tailored mixes to meet higher durability and early-strength requirements. This supports value growth beyond volume, as project owners increasingly specify performance outcomes (bond strength, toughness, early strength gain, and permeability) rather than only compressive strength.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Underground Construction Expansion Drives Core of Product Demand

Underground construction remains the primary driver of shotcrete market growth, as it supports ground and initial lining, enabling faster excavation cycles and stabilizing weak rock zones without full formwork systems. As new metro systems, rail tunnels, road tunnels, and underground utilities expand globally, product demand rises directly with tunneling meters and support intensity, particularly where geological uncertainty requires flexible support designs.

Underground construction accounts for a major share of the market value, far exceeding other applications. This makes demand resilient in regions with sustained underground project pipelines and raises the importance of contractor capability, equipment availability, and reliable admixture/fiber supply.

MARKET RESTRAINTS

Cost and Logistics Constraints in Specialized Inputs and Equipment to Restrain Market Growth

Shotcrete economics are influenced by project access, mobilization requirements, and the need for specialized inputs such as accelerators, fibers, and spraying equipment. In constrained underground environments, higher costs for ventilation, safety systems, and downtime amplify total installed cost, which can limit adoption where budgets are tight or project owners opt for lower-spec alternatives.

This restraint is more visible in applications outside the core underground segment, where alternative repair methods or conventional concreting may compete more directly. It can also delay upgrades from manual to mechanized spraying in emerging markets where capex constraints remain high.

MARKET OPPORTUNITIES

Water Infrastructure Expansion Creates Value Growth in Specialized Shotcrete Systems

Water retaining structures represent an attractive opportunity as utilities and municipalities expand and rehabilitate reservoirs, canals, treatment units, and containment structures. Shotcrete is well-suited for lining geometries and constrained retrofit zones, and demand for low-permeability, crack-resistant systems is rising. The water-retaining segment often supports higher-value specifications due to durability and sensitivity to leakage risk, creating room for premium mix designs and advanced reinforcement.

MARKET CHALLENGES

Specification Complexity and Performance Compliance Raise Execution Risk

As projects move toward performance specifications, early-strength gain, energy absorption (toughness), permeability limits, and durability metrics, contractors face greater execution complexity. Mix selection, accelerator compatibility, curing control, and QA/QC testing must be tightly managed, especially in underground conditions.

This challenge is magnified in large-scale projects, where variability across crews and shifts can lead to inconsistent results. It increases the importance of trained nozzle operators, standardized procedures, and supplier technical support, and can slow adoption in markets where testing and compliance infrastructure is limited.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade tensions and geopolitical uncertainty can increase volatility in raw material prices, logistics costs, and cross-border supply chains. Many sealing materials and components rely on globally traded inputs, making manufacturers sensitive to tariffs, sanctions, and regional trade restrictions.

These factors can affect sourcing strategies, production economics, and regional pricing dynamics, particularly for companies operating manufacturing facilities across multiple geographies. As a result, supply chain resilience and regional diversification are becoming increasingly important strategic considerations.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in sprayed concrete focuses on improving pumpability, early strength development, reduced rebound, and long-term durability, particularly for underground and water infrastructure use-cases. Innovations increasingly target fiber optimization, rheology control of mixtures, and admixture systems that perform consistently across varying temperature and humidity conditions.

Sustainability-linked R&D is also accelerating, including lower-cement-intensity mixes, improved compatibility with Supplementary Cementitious Materials (SCMs), and durability improvements that extend service life and reduce lifecycle emissions. Mechanization and automation (spraying control, data logging, quality tracking) are also rising as owners demand predictable outcomes and reduced execution risk.

SEGMENTATION ANALYSIS

By Process

Wet Mix Segment Dominates Market Due to Higher Output, Quality Consistency, and Mechanized Application Fit

Based on process, the global market is segmented into dry mix and wet mix.

Among these, wet mix holds the dominant shotcrete market share. The growth is primarily due to better alignment with the productivity and quality-control expectations of large-scale construction programs. In the wet mix process, concrete is fully batched and mixed before pumping, which typically improves mix uniformity, water-cement control, and repeatability during spraying. This makes it the preferred method for high-volume, schedule-sensitive projects, especially in underground construction, which is the largest application segment.

Dry mix accounts for a notable market share and remains an important segment due to its operational flexibility and suitability for specialized or constrained jobs. In the dry mix process, dry materials are conveyed through the hose, and water is introduced at the nozzle, allowing crews to start/stop quickly, handle smaller or intermittent spray quantities, and operate effectively in confirmed access-limited zones. This process is especially relevant in repair and rehabilitation, where work may be fragmented across multiple structural sections and where rapid mobilization is important. The segment is anticipated to grow at a CAGR of 5.2% during the study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Underground Construction Segment Dominates Market Due to High Shotcrete Intensity in Tunnels and Ground Support

Based on application, the market is segmented into underground construction, water retaining structures, repair and rehabilitation, protective coatings, and others.

Underground construction represents the dominant application segment. The concrete is a core method for initial ground support, face stabilization, and temporary-to-semi-permanent linings in tunnels and caverns. The segment also tends to be value-intensive as underground specifications often require early strength gain, fiber reinforcement, and accelerator systems to control deformation and improve safety.

Repair and rehabilitation holds a significant share and is set to register a CAGR of 5.0% over the forecast period. Sprayed concrete is widely used in structural restoration, including bridge substructures, retaining walls, marine repair zones, industrial structures, and deteriorated concrete sections where access is difficult or overhead placement is required.

Water retaining structures account for positive growth and are typically driven by reservoir linings, canals, water treatment assets, storage tanks, and containment structures, where leakage control and long-term durability are critical. Sprayed concrete is often preferred as it enables efficient lining of curved or irregular geometries and can be applied with reinforcement strategies that reduce the risk of cracking. The value contribution in this segment can increase faster than volume as water infrastructure often demands tighter permeability control and more durable mix designs to minimize lifecycle maintenance.

Others consist of niche and mixed applications, such as specialty structural works, architectural or shaped concrete elements, localized slope stabilization packages, and certain industrial containment or repair uses that do not cleanly fit into the main buckets. The segment is smaller but can be important in markets where specific construction practices or local project types create demand pockets.

SHOTCRETE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Shotcrete Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading market share in 2025, supported by large-scale underground infrastructural development and growing rehabilitation requirements. The region’s mix increasingly favors wet-mix solutions aligned with productivity and performance control. China, Japan, South Korea, and India are key contributors, with China representing one of the largest single-country markets due to its underground construction.

China Shotcrete Market

China’s market is one of the largest globally, with 2025 revenue valued at USD 1.71 billion, representing roughly 19.5% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is experiencing positive growth, supported by structural rehabilitation programs and targeted tunneling/underground works. Contractor specialization and specification discipline typically support higher-value shotcrete systems.

U.S. Shotcrete Market

In 2025, the U.S. market represented USD 1.40 billion in North America, driven primarily by strong demand for shotcrete from the residential and commercial construction sectors. The U.S. accounts for roughly 16.0% of global market sales.

Europe

Europe is experiencing significant growth, driven by a value-intensive project environment in which compliance, durability, and quality validation influence product choice. Underground works and renovation cycles support stable demand.

Germany Shotcrete Market

The Germany market was at USD 0.48 billion in 2025, representing roughly 5.5% of global market revenues.

U.K. Shotcrete Market

The U.K. market was at around USD 0.38 billion in 2025, representing roughly 4.3% of global market revenues.

Latin America

Latin America is growing rapidly through construction booms, wastewater projects, and disaster mitigation, with Brazil leading with projects including the Monte Dam. Infrastructure and mining activities in Argentina contribute to increasing demand for the product. Emphasis on durable solutions in challenging environments supports expansion.

Brazil Shotcrete Market

The Brazil market was valued at around USD 0.28 billion in 2025, representing roughly 3.2% of global market revenues.

Middle East & Africa

High demand stems from mega-projects in Saudi Arabia (mining and oil), the UAE, and Qatar for urban development and high-rises. Natural resources drive quarrying needs, while transportation networks add momentum. Investments in utilities and GCC infrastructure propel usage.

GCC Shotcrete Market

The GCC market was at around USD 0.45 billion in 2025, representing roughly 5.2% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Admixture-Led Multinationals and Underground Specialists Shape Competition through Performance Specs and Contractor Support

The market is characterized by the presence of large multinational players with strong engineering capabilities and global manufacturing footprints. Leading companies focus on material innovation, application engineering, and long-term OEM partnerships to maintain a competitive advantage. Leading producers, such as Sika AG, Master Builders Solutions, Normet Group, Putzmeister, and Mapei Group are directing capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY SHOTCRETE COMPANIES PROFILED IN REPORT

- Sika AG (Switzerland)

- Master Builders Solutions (Germany)

- Normet Group (Finland)

- Putzmeister (Germany)

- Mapei Group (Italy)

- BASF Construction Chemicals (Germany)

- GCP Applied Technologies (U.S.)

- Euclid Chemical Company (U.S.)

- The Dow Chemical Company (U.S.)

- BarChip Inc. (Ireland)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Master Builders Solutions announced the expansion of its tail sealants line, specifically citing rising demand for underground construction (subways and highway tunnels). While tail sealants are not shotcrete, this development is a strong indicator of continued tunneling/TBM investment, which supports sustained wet-mix shotcrete demand and adjacent underground consumables.

- December 2023: Sika announced new production lines for Sigunit shotcrete accelerator at Kirchberg (Switzerland), positioning the site as a technology and capacity upgrade to serve tunnel projects more efficiently and reduce transport distances. This is a direct signal of investment into shotcrete-specific admixture supply capacity.

REPORT COVERAGE

The shotcrete report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, process, and application. Additionally, it offers valuable insights into the market and current industry trends, and highlights key developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 5.7% from 2026 to 2034 |

| Segmentation | By Process, By Application, By Region |

| By Process |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 8.75 billion in 2025 and is projected to reach USD 14.35 billion by 2034.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The underground construction segment is leading the market.

Asia Pacific held the highest market share in the market.

Underground construction production and electrification drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us