Silicon Carbide (SiC) Devices Market Size, Share & Industry Analysis, By Product Type (SiC MOSFETs, SiC Diodes/SBDs, and SiC Modules), By Voltage Rating (Up to 650V, 650V–1200V, 1200V–1700V, and Above 1700V), By Power Range (Low Power (<1 kW), Medium Power (1 kW–50 kW), and High Power (>50 kW)), By Application (Automotive, Industrial, Energy & Utilities, Aerospace & Defense, and Others), and Regional Forecast, 2026- 2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

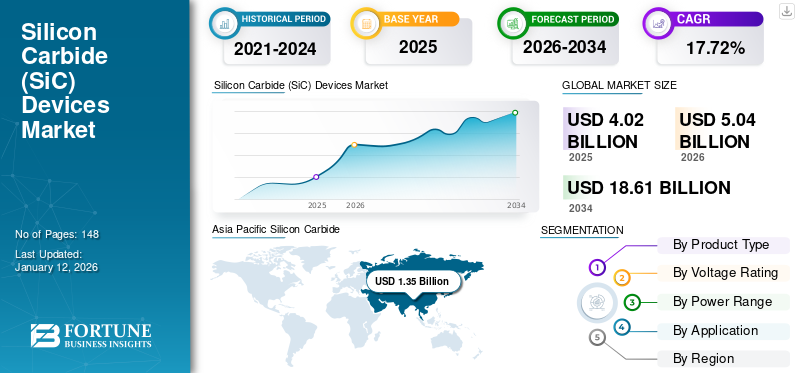

The global Silicon Carbide (SiC) devices market size was valued at USD 4.02 billion in 2025. The market is projected to grow from USD 5.04 billion in 2026 to USD 18.61 billion by 2034, exhibiting a CAGR of 17.72% during the forecast period. Asia Pacific dominated the Silicon Carbide (SiC) devices market with a market share of 31.84% in 2025.

Silicon Carbide (SiC) devices are a class of semiconducting materials manufactured from the crystalline structure known as silicon carbide. It is used in many applications to increase the overall efficiency of energy use and decrease the amount of energy lost while transferring it from one place to another, such as electric vehicles and automotive power train systems, renewable energy, industrial drive systems and other power conversion equipment. The market is witnessing significant growth due to rising electrification in EVs, renewable energy solutions, fast charging stations and efficient industrial power electronics. This is due to SiC devices’ unique ability to operate at higher voltage and thermal levels along with having greater efficiency than standard silicon semiconductors. This factor plays an important role in fueling the market growth.

Furthermore, many key market players, such as STMicroelectronics, Infineon Technologies AG, Wolfspeed, Inc., ROHM Co., Ltd., and Semiconductor Components Industries, LLC, operating in the market, are focusing on forming strategic partnerships with leading companies in the electric vehicle (EV), renewable energy, and industrial sectors. These collaborations focus on integrating SiC-based solutions with advanced technologies to enhance efficiency. Also, these partnerships help companies expand their market reach and gain access to new applications.

Download Free sample to learn more about this report.

Silicon Carbide (SiC) Devices Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.02 Billion

- 2026 Market Size: USD 5.04 Billion

- 2034 Forecast Market Size: USD 18.61 Billion

- CAGR: 17.72% from 2026–2034

- Asia Pacific accounted for 31.84% market share in 2025.

- Automotive segment dominated the market in 2025.

- SiC Modules are expected to grow at a CAGR of 26.5% during the forecast period.

Asia Pacific

Asia Pacific reached USD 1.28 billion in 2025 and is projected to grow to USD 1.42 billion in 2026, driven by EV adoption and semiconductor growth.

North America

North America is projected to reach USD 1.14 billion in 2026, supported by domestic SiC manufacturing and supply chain expansion.

Europe

Europe is projected to reach USD 1.00 billion in 2026, driven by SiC manufacturing investments and automotive demand.

U.S.

The U.S. market is projected to reach USD 0.77 billion by 2026, fueled by semiconductor and EV applications.

Japan

The Japan market is projected to reach USD 0.36 billion by 2026, supported by power semiconductor and electric mobility growth.

Read More

IMPACT OF GENERATIVE AI

Rising Generative AI Integration in Semiconductor Design Driving Efficiency and Innovation in Market

As a strategic catalyst fueling innovation in the silicon carbide device market, generative AI also has an impact on improving production efficiencies that strengthen the overall competitiveness of the market through the ability of generative AI methodologies to simulate new materials based on their electrical, thermal, and mechanical properties as well as to optimize their structure for enhanced performance. For instance,

- In June 2025, Siemens AG introduced an AI-enhanced EDA toolset at DAC 2025 to accelerate semiconductor and PCB design. The new system integrates generative and agentic AI, including NVIDIA NIM microservices and Nemotron models, to improve productivity and accelerate time-to-market.

The combination of generative AI with existing trial-and-error material discovery techniques can shrink the time associated with discovering new materials or developing prototypes of new devices. In device design, AI-assisted simulation tools help engineers optimize MOSFETs, diodes, and power modules by evaluating performance under varied operating conditions, thereby improving reliability and accelerating time-to-market. Furthermore, AI-based analytics can improve supply chain planning, demand forecasting, and inventory optimization, strengthening overall market resilience. Collectively, the integration of generative AI enhances efficiency, lowers cost structures, and accelerates commercialization, thereby positively influencing the long term growth trajectory of the market.

SILICON CARBIDE DEVICES MARKET TRENDS

Increasing Adoption of SiC Devices in 5G Technology is Boosting Market Growth

Rapid expansion of 5G infrastructure through 2025 is increasing demand for higher efficiency power electronics across base stations, radio units, and telecom power supply systems. 5G cellular networks require many small cells deployed close together; large numbers of multiple "inputs and outputs" from many antennas with higher frequencies, all of which require greater power density and require thermal management. Silicon carbide devices are becoming more important in the manufacture of rectifiers for telecoms as they exhibit lower switching losses and have superior efficiency under high load conditions. For instance,

- According to a GSMA study in 2025, global 5G connections surpassed 2.7 billion by the end of 2025, reflecting strong subscriber growth and large scale infrastructure deployment.

The rollout phase of 5G telecom networks is increasing the energy consumed by each site; thus pointing out the necessity for efficient semiconductor solutions to assist with reducing total operational expenses. When compared to earlier generations of telecom base stations, 5G base stations will consume significantly greater amounts of energy compared with previous generations. This increases the value of advanced energy efficient semiconductor devices within telecommunications energy systems such as electricity in urban and industrial settings.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Efficient Power Electronics to Propel Market Growth

The rise in demand for electrical power will have a major impact on the amount of energy that must go through the conversion process at all levels including; transmission systems, industry, and digital infrastructure. The lower the conversion losses and wasted heat, the better the overall economics of the system, as thermal constraints will be off-loaded onto individual power systems. These types of changes provide a favorable operating environment for the widespread use of SiC MOSFET's, diodes, and power modules in high voltage and high-frequency systems aimed at minimizing electrical losses.

- In a 2025 study, the International Energy Agency projects global electricity demand growth of approximately 2.4% in 2025, with emerging economies accounting for nearly 85% of the incremental demand, driven by electrification and data center expansion.

The expanding market for EV is driving the demand for more efficient traction inverters, on-board chargers, and fast charging systems. This demand for efficient conversion will result in lower range limitations due to conversion losses, as well as less burden on cooling systems. The need to operate at higher voltages will create additional value in using efficient switching and power density, further enabling SiC devices to penetrate deeper into EVs and charging infrastructures. Such an expansion in demand will create a stronger long-term demand pull for SiC devices across automotive and charging infrastructure supply chains. For instance,

- In a 2025 study, the International Energy Agency estimates that global electric car sales will exceed 20 million units in 2025, representing more than 25% of total new-car sales worldwide, up from roughly 14 million units in 2023.

MARKET RESTRAINTS

High Production Costs and Integration Complexity Restraining Broader SiC Adoption

Silicon carbide devices continue to carry a higher upfront cost versus silicon as wafer substrates and epi processes remain more expensive, even with recent price declines in parts of the supply chain. Additionally, input cost volatility presents procurement risks to OEMs and tier suppliers, which hinders large-scale deployment of silicon carbide devices except for those that require premium performance or have critical performance requirements. Consequently, slower adoption has occurred among industrial users who are price sensitive and are evaluating how long it will take to recover the investment cost based on slack time for deployment.

Finally, yield and defectivity remain significant constraints on manufacturing economics, which cause the effective cost per usable die to increase and the qualification durations to increase. Also, poor yields at the wafer and epitaxy phases result in higher scrap and rework rates, particularly for automotive grade components, which must undergo extremely rigorous reliability testing. These combined factors limit scalability in the next few years, and, therefore, keep price levels for silicon carbide devices above those that would allow the devices to achieve mass market penetration across all voltage and power classes.

MARKET OPPORTUNITIES

Increasing Advancements in Automotive and Electric Vehicles to Create New Market Opportunities

Electric vehicles have been experiencing rapid growth over the past few years and are generating demand for more efficient power electronics for traction inverters, onboard chargers, and DC fast charging systems. Many automakers are expanding their electrification strategies to include higher voltage architectures (800V platforms) with the goal of boosting the efficiency of electric vehicles, increasing the driving range and decreasing the time required to charge them. Due to their lower switching losses, higher thermal tolerances and superior power density, silicon carbide devices offer outstanding advantages for these developments.

- For instance, according to the International Energy Agency 2025 study, global electric car sales exceeded 17 million units in 2024, accounting for more than 20% of total global car sales, compared to about 18% in 2023.

Regional dominance in EV production and sales continues to strengthen supply chain scale and promote long-term Silicon Carbide (SiC) devices market growth opportunities. The Asia Pacific region has been the largest EV market globally due primarily to various government incentives, infrastructure-related investments, and domestic production capacity.

Segmentation Analysis

By Product Type

High Efficiency and Superior Switching Performance of SiC MOSFETs Driving Their Dominance

Based on the product type, the market is categorized into SiC MOSFETs, SiC diodes/SBDs, and SiC modules.

SiC MOSFETs are expected to account for the largest market share. This is owing to their superior efficiency, high switching speed, and ability to operate at high voltages and temperatures, making them ideal for power conversion applications. This has made them ideal for many power conversion applications. The success of SiC MOSFETs in traction inverters for electric vehicles, charging systems for fast charging, renewable energy inverters, and industrial motor drives resulted in more demand for these devices as opposed to other types of SiC devices.

SiC modules are anticipated to grow at the highest CAGR of 26.5% over the forecast period. This is owing to their increasing integration in high-power applications such as EV traction inverters, fast-charging infrastructure, renewable energy systems, and industrial power converters that require compact and high-efficiency power solutions.

By Voltage Rating

Growing Adoption of 650V–1200V Power Electronics in EVs and Renewable Energy Systems Driving Segment Dominance

Based on the voltage rating, the market is divided into up to 650V, 650V–1200V, 1200V–1700V, and above 1700V.

650V–1200V is anticipated to account for the largest Silicon Carbide (SiC) devices market share. This is owing to its widespread application in electric vehicle traction inverters, onboard chargers, solar inverters and industrial motor drives which utilize this voltage range with the ideal combination of high-efficiency and power-carrying capacity. The adoption of 800V electric vehicle architectures and the growing use of high-efficiency power conversion systems has helped reinforce the demand for SiC devices in this voltage range.

1200V–1700V is anticipated to grow at the highest CAGR of 27.0% over the forecast period. This is owing to its increasing deployment in high-power applications such as EV fast-charging infrastructure, renewable energy inverters, grid systems, and heavy industrial motor drives that require higher voltage and efficiency levels.

By Power Range

Growing Electrification in EV Charging, Solar Inverters, and Industrial Drives Driving Dominance of the 1 kW–50 kW Segment

Based on power range, the market is categorized into low power (<1 kW), medium power (1 kW–50 kW), and high power (>50 kW).

Medium Power (1 kW–50 kW) is anticipated to witness a dominating market share in 2025. This is due to its extensive use in electric vehicle onboard chargers, solar inverters, industrial motor drives, and energy storage systems, where efficient power conversion within this range is critical. Growing electrification across transportation and industrial automation has significantly increased the deployment of SiC devices in this power range.

High Power (>50 kW) is projected to grow at the highest CAGR of 25.4% over the forecast period. This is due to the increasing transition toward 800V and higher voltage power architectures in electric mobility and large-scale electrification systems, which require advanced SiC devices to handle higher power density and thermal performance efficiently.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rapid Adoption of Electric Vehicles and Advanced Powertrain Architectures Driving Automotive Segment Dominance

Based on the application, the market is classified into automotive, industrial, energy & utilities, aerospace & defense, and others (consumer electronics, etc.).

Automotive is expected to witness a dominating market share in 2025 and is expected to grow at the highest CAGR of 26.1% in coming years. This is due to a growing number of companies offering electric cars; silicon carbide (SiC) components provide better power efficiency and range in electric traction inverters, onboard chargers, and DC to DC converters. The installation of 800V and other electric vehicle powertrain solutions has also sped up the use of SiC power devices in passenger and commercial electric vehicles.

Energy & Utilities are anticipated to grow at a prominent CAGR of 24.8% during the forecast period. This is owing to the increasing need for high-voltage and high-temperature capable power semiconductors in modern transmission systems, HVDC networks, and next-generation power distribution infrastructure.

Silicon Carbide Devices Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

Asia Pacific

Asia Pacific Silicon Carbide (SiC) Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the largest share of the market in 2024, valuing at USD 1.03 billion, and also maintained the leading share in 2025, with USD 1.28 billion. The market in Asia Pacific is expected to increase, due to its leadership in electric vehicle production and adoption. A growing penetration of electric vehicles will lead to a corresponding increase in SiC content per electric vehicle due to their use in traction inverters, onboard chargers, and DC fast-charging stations; this will directly contribute to the continued growth of demand for SiC devices in Asia Pacific. Strong Original Equipment Manufacturer (OEM) ecosystems within China, Japan, and South Korea are accelerating the rate of semiconductor integration into next-generation vehicle architectures. In the region, India and China are both estimated to reach USD 0.20 billion and USD 0.48 billion, respectively, in 2026.

- For example, according to the International Energy Agency 2025 study, China accounted for nearly two-thirds of global electric car sales in 2024, and almost 50% of total car sales in China were electric.

These factors play a significant role in fueling the market growth.

China Silicon Carbide Devices Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.48 billion, representing roughly 10.5% of global sales.

Japan Silicon Carbide Devices Market

The Japan market in 2026 is estimated at around USD 0.36 billion, accounting for roughly 7.9% of global revenues. This is owing to the country’s strong power semiconductor manufacturing ecosystem and increasing investment in next-generation electric mobility, smart grid infrastructure, and advanced industrial power electronics.

India Silicon Carbide Devices Market

The Indian market size in 2026 is estimated at around USD 0.20 billion, accounting for roughly 4.4% of global revenues.

North America

North America is estimated to reach USD 1.14 billion in 2026 and secure the position of the second-largest region in the market. As the region is developing a much stronger domestic SiC supply chain, therefore increasing availability while allowing customers to qualify faster. By adding to the local capacity base, it will also reduce lead-time risks for both automotive and industrial customers that need multiple year supply commitments. Supply side momentum boosts both device shipments and overall revenue capture for the region. For instance,

- In October 2024, the U.S. Department of Commerce announced preliminary terms for up to USD 750 million in proposed CHIPS Act direct funding for Wolfspeed, tied to the expansion of domestic silicon carbide wafer manufacturing.

U.S. Silicon Carbide Devices Market

Based on North America’s significant contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.77 billion in 2026, accounting for roughly 16.8% of global sales.

Europe

Europe is projected to grow at a CAGR of 25.0% in the coming years, which is the third-highest among all regions, and reach a valuation of USD 1.00 billion by 2026. The market is observing significant growth in the region, the region is actively strengthening domestic SiC manufacturing and supply chain resilience, thereby supporting a stable supply for automotive and industrial customers. Public support systems and state aid approval mechanisms are helping to speed up the capacity buildouts and to reduce the commercialization timelines of SiC Power Devices produced locally. The continued growth of SiC. Manufacturing is providing more revenue captured across the region by discrete devices and power modules.

U.K. Silicon Carbide Devices Market

The U.K. market in 2026 is estimated at around USD 0.20 billion, representing roughly 4.4% of global revenues.

Germany Silicon Carbide Devices Market

Germany’s market is projected to reach approximately USD 0.21 billion in 2026, equivalent to around 4.6% of global sales.

South America

South America is expected to witness moderate growth in this market space during the forecast period and the market is set to reach a valuation of USD 0.33 billion in 2026. This is owing to the regional electric vehicle penetration remaining comparatively low, limiting near-term demand for SiC MOSFETs and modules in traction inverters and onboard chargers. Automotive OEMs and tier suppliers, therefore, have fewer large-scale electrified platforms in the region that require high-voltage, high-efficiency power semiconductors.

Middle East and Africa

The Middle East & Africa is estimated to reach USD 0.51 billion in 2026 and expected to grow at a prominent growth rate in the coming years. This is owing to expanding demand for high-efficiency inverters, converters, and power conditioning systems that increasingly benefit from SiC devices. Gulf and North Africa's large-scale solar and wind projects require high-density power and low-loss switching to improve plant operations and reduce cooling requirements. As a result, renewable build-out will create sustainable procurement cycles for advanced power semiconductors for utility-scale and commercial power generation assets. In the Middle East & Africa, the GCC is set to reach a value of USD 0.19 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Presence of Established Semiconductor Manufacturers and Continuous Product Innovations Driving Market Expansion

The global SiC devices market holds a semi-consolidated market structure, with prominent players such as STMicroelectronics, Infineon Technologies AG, Wolfspeed, Inc., ROHM Co., Ltd., and Semiconductor Components Industries, LLC holding significant positions. These companies maintain dominance through vertically integrated operations, global customer networks, and strong positioning in electric vehicle traction inverters, on-board chargers (OBCs), renewable energy systems, and industrial motor drives. Their ability to scale production while improving cost competitiveness remains a decisive factor in fueling market growth.

- In April 2025, ROHM launched high power-density SiC molded modules optimized for PFC and LLC converters in xEV on-board chargers, strengthening its module-level value proposition and supporting improved thermal performance and power density in compact system designs.

Other notable players in the global market include Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Microchip Technology Inc., NXP Semiconductors, and Coherent Corp. These companies benefit from regional manufacturing strengths, industrial and rail traction exposure, and selective automotive participation, gradually expanding their presence through module-focused strategies.

LIST OF KEY SILICON CARBIDE DEVICES COMPANIES PROFILED

- STMicroelectronics (Switzerland)

- Infineon Technologies AG (Germany)

- Wolfspeed, Inc. (U.S.)

- ROHM Co., Ltd. (Japan)

- Semiconductor Components Industries, LLC (Onsemi) (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Microchip Technology Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Coherent Corp. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Infineon announced that CoolSiC MOSFETs were adopted in Toyota’s new bZ4X, integrated into the on-board charger and DC/DC converter. The news underscores SiC’s role in reducing losses and improving efficiency in EV power conversion. It also acts as a high-visibility automotive validation for Infineon’s CoolSiC device lineup.

- November 2025: Wolfspeed launched 1200 V SiC six-pack power modules designed for e-mobility propulsion systems, targeted at delivering high performance and system efficiency for electric vehicle traction converters and other power electronics.

- September 2025: Infineon and ROHM signed a MoU to collaborate on SiC power electronics packages and enable second-sourcing for selected SiC products. The stated intent is to make switching between certain Infineon and ROHM parts easier for customers, improving procurement flexibility and reducing qualification risk.

- July 2025: Microchip Technology has partnered with Delta Electronics to integrate Microchip’s mSiC silicon carbide solutions into Delta’s energy-efficient power management designs. The collaboration aims to accelerate sustainable, high-efficiency applications for AI, mobility, automation, and infrastructure, leveraging SiC’s advantages for smaller, lower-cost, high-voltage systems.

- April 2025: Rohm unveiled its new high power density EcoSiC power modules, showcasing SiC devices with greater efficiency and performance for power conversion applications across automotive and industrial segments.

- November 2024: ROHM entered into a collaboration agreement with Valeo for optimizing and proposing the advanced power modules for electric motor inverters by utilizing their joint expertise in power electronics management.

- September 2024: STMicroelectronics launched its 4th generation STPOWER silicon carbide MOSFET technology. The new technology is adopted for traction inverters, the key component of EV powertrains. The company is planning to launch cutting-edge SiC technology innovations by 2027 as a commitment to innovation.

REPORT COVERAGE

The global silicon carbide devices market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key SiC industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 24.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Voltage Rating, Power Range, Application, and Region |

| By Product Type |

|

| By Voltage Rating |

|

| By Power Range |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.73 billion in 2025 and is projected to reach USD 26.13 billion by 2034.

In 2025, the market value stood at USD 1.28 billion.

The market is growing at a CAGR of 24.3% during the forecast period.

By application, automotive sector is expected to lead the market.

The rising demand for efficient power electronics to propel market growth.

STMicroelectronics, Infineon Technologies AG, Wolfspeed, Inc., ROHM Co., Ltd., and Semiconductor Components Industries, LLC are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 125

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us