Silicon Carbide (SiC) Module Market Size, Share & Industry Analysis, By Module Type (SiC MOSFET Modules, SiC Schottky Diode Modules, and Hybrid SiC Modules), By Voltage Range (<600V, 600V – 1200V, and >1200V), By Application (Automotive, Energy & Utilities, Industrial, Telecommunications, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

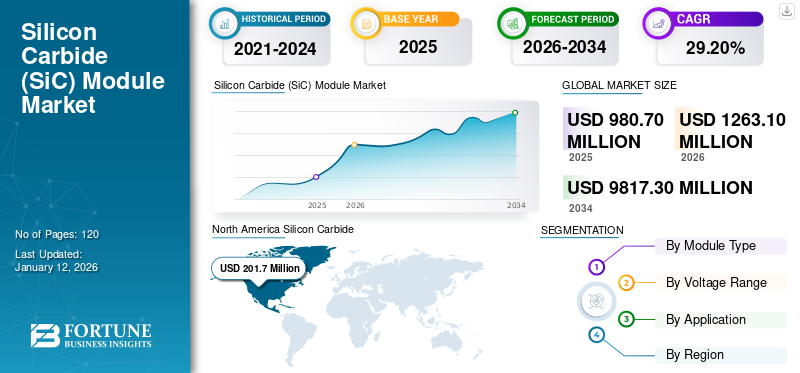

The global Silicon Carbide (SiC) module market size was valued at USD 980.7 million in 2025. The market is projected to grow from USD 1263.1 million in 2026 to USD 9817.3 million by 2034, exhibiting a CAGR of 29.20% during the forecast period. North America dominated the market with a share of 26.06% in 2024.

The global silicon carbide (SiC) module market refers to the industry focused on the development, production, and commercialization of power modules that utilize silicon carbide as a semiconductor material. These modules are designed to efficiently manage and convert electrical energy in a wide range of applications, including automotive, energy & utilities, industrial, telecommunications, aerospace & defense, and others. These modules offer superior properties compared to traditional silicon-based power modules, including higher energy efficiency, lower switching losses, improved thermal conductivity, and compact design.

The growing demand for energy-efficient and high-performance power electronics across electric vehicles, renewable energy systems, and industrial applications drives the growth of the silicon carbide (SiC) module market. For instance,

- Industry experts estimate that achieving a 60% share of battery-electric and plug-in hybrid vehicles on the road could result in a reduction of over 60 billion tons of CO2 by 2050. This shift in vehicle adoption is seen as a significant step toward reducing global carbon emissions.

Additionally, advancements in SiC devices and the rising global emphasis on reducing carbon emissions are further accelerating market adoption.

The Wolfspeed, Inc., STMicroelectronics, Infineon Technologies AG, ROHM Semiconductor, ON Semiconductor, Microchip Technology, Inc., Mitsubishi Electric Corporation, Hitachi Energy, Fuji Electric Co., Ltd., and Littelfuse, Inc. are among the top companies operating in the market.

Download Free sample to learn more about this report.

Impact of Reciprocal Tariffs on Silicon Carbide (SiC) Module Market

Reciprocal tariffs imposed between key trading nations can unfavorably impact the silicon carbide module market by increasing the cost of raw materials and essential components. These cost booms can affect manufacturing expenses, thereby reducing the price competitiveness of silicon carbide (SiC) modules in the global market. Companies may be forced to pass these additional costs onto consumers, slowing down the adoption of SiC technology across various applications.

Moreover, these tariffs can disrupt global supply chains, leading to delays in production and extended delivery timelines. Manufacturers dependent on international suppliers may face logistical challenges and reduced operational flexibility. Such disruptions may force companies to review and rearrange their sourcing and manufacturing strategies, resulting in increased capital expenditure. In the long term, trade barriers may discourage investment, limit innovation, and hamper the global silicon carbide (SiC) module market growth.

Silicon Carbide (Sic) Module Market Trends

Expansion of 5G and Data Centers to Propel Market Growth

The rapid global rollout of 5G networks and the increasing demand for high-performance data centers are significantly fueling the growth of the market. SiC modules are being adopted in telecom and data infrastructure due to their superior energy efficiency, high switching frequency, and excellent thermal conductivity. These characteristics enable more compact and reliable power supply systems, which are essential for dense and energy-intensive environments like 5G base stations and hyperscale data centers. Therefore, telecom operators and data center providers are investing in SiC-based solutions to meet performance and sustainability goals. This trend is expected to continue accelerating, contributing to a sustained increase in SiC module demand over the coming years.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Electric Vehicles (EVs) to Propel Market Growth

The rising demand for EVs drives the implementation of silicon carbide modules in these vehicles. For instance,

- The electric vehicle (EV) market saw substantial growth in 2024, with global sales rising by 25% year-over-year. Total sales exceeded 17 million units, marking a significant milestone in the industry's expansion.

SiC modules provide enhanced energy efficiency, higher voltage handling, and superior thermal conductivity, making them ideal for EV applications. Automotive manufacturers are increasingly integrating SiC modules into powertrains and charging systems to improve performance, reduce energy loss, and extend battery life. This shift toward SiC technology increases the industry's focus on achieving greater range and faster charging in EVs.

Government policies supporting electric mobility, including subsidies, emission regulations, and infrastructure development, are further accelerating EV adoption globally. As a result, the demand for reliable and efficient power electronics has increased, making SiC modules an essential part of EV innovation. The expansion of the EV market across passenger cars, commercial vehicles, and public transportation systems continues to boost SiC module requirements.

MARKET RESTRAINTS

High Cost of SiC Materials and Complex Manufacturing Processes Can Hamper Market Growth

Compared to traditional silicon-based modules, SiC modules require advanced fabrication techniques and specialized equipment, which contribute to higher production costs and limited scalability. Additionally, the limited availability of high-quality SiC substrates and the technical challenges associated with device packaging and reliability further hinder widespread adoption. These factors collectively pose barriers for small and medium-sized manufacturers and slow the penetration of SiC modules in cost-sensitive applications, thereby restraining overall market growth.

MARKET OPPORTUNITIES

Rise in Renewable Energy Systems to Create Significant Opportunities for Market

The rapid growth of renewable energy systems is driving substantial opportunities as these technologies require high-efficiency power electronics for optimal performance. For instance,

SiC modules are beneficial for renewable energy applications such as solar inverters, wind power systems, and energy storage solutions. They offer higher voltage handling, efficiency, and thermal management. The global push for clean energy intensifies the demand for SiC modules in renewable energy infrastructure.

Government initiatives promoting renewable energy adoption further fuel the demand for advanced power solutions, positioning SiC modules as a crucial technology in energy conversion. The expansion of solar, wind, and storage systems increases the need for efficient and reliable power electronics. For instance,

- India's installed non-fossil fuel capacity has grown by an impressive 396% over the past 8.5 years, surpassing 205 GW, which includes large hydro and nuclear power. This growth reflects significant progress in the country's transition to cleaner energy sources.

Moreover, the growing reliance on SiC modules to enhance the performance and scalability of renewable energy systems will provide significant growth prospects for the market in the coming years.

Segmentation Analysis

By Module Type

Increasing High-power Applications to Drive Growth of SiC MOSFET Module Segment

Based on module type, the market is segmented into SiC MOSFET modules, SiC Schottky Diode modules, and hybrid SiC modules.

SiC MOSFET modules dominate the market due to their superior efficiency, reduced conduction losses, and ability to operate at higher switching frequencies and temperatures, making them ideal for high-power applications. For instance,

- In March 2025, onsemi introduced its first-generation 1200V SiC MOSFET-based SPM 31 Intelligent Power Modules (IPMs). It offers the highest energy efficiency and power density in the smallest form factor, delivering a lower total system cost.

Hybrid SiC modules, which combine the features of SiC and silicon technologies, are expected to experience the highest CAGR due to their cost-effectiveness, providing a balance of performance and affordability.

By Voltage Range

Wide Use Across Various Applications to Propel Growth of 600V-1200V Segment

By voltage range, the market is classified as <600V, 600V – 1200V, and >1200V.

The 600V-1200V holds the largest share in the market due to its wide usage in industrial motor drives, power supplies, and consumer electronics, where these voltage levels deliver optimal performance for medium-power applications.

Modules with voltages above 1200V are expected to grow at the highest CAGR as they are increasingly adopted in high-power applications, such as EVs and renewable energy installations, which require higher voltage for efficient energy conversion. For instance,

- In February 2024, Qorvo launched four 1200V SiC modules. These high-efficiency modules are designed for use in Electric Vehicle (EV) charging stations, energy storage systems, industrial power supplies, and solar power applications.

By Application

Energy & Utilities to Have Highest CAGR Leads Owing to Need for Efficient Power Conversion

By application, the market is divided into automotive, energy & utilities, industrial, telecommunications, aerospace & defense, and others.

Energy & utilities are expected to grow at the highest CAGR due to the increasing focus on renewable energy sources, smart grid technologies, and energy storage solutions, which rely on SiC modules for efficient power conversion and management.

The automotive sector leads the market due to the rapid growth of EVs. SiC components provide significant benefits in terms of energy efficiency, power density, and compactness for high-performance inverters and electric drivetrains.

Silicon Carbide (SiC) Module Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America

North America Silicon Carbide (SiC) Module Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the market due to its established automotive, industrial, and energy sectors, where SiC technology is widely adopted to meet energy efficiency and sustainability targets. Key industries in the U.S., such as EV manufacturing and renewable energy, have accelerated the deployment of SiC-based systems, driving the region's leadership.

Europe

Europe holds a significant share of the market due to its strong focus on sustainable technologies and the widespread adoption of Electric Vehicles (EVs), where SiC modules are crucial for improving energy efficiency and power density in EV drivetrains. For instance,

- In 2023, Europe experienced a notable increase in Electric Vehicle (EV) registrations, with nearly 3.2 million new EVs registered. This represented an almost 20% year-over-year growth compared to the previous year.

Additionally, its leadership in renewable energy integration and smart grid development has driven the demand for high-performance power electronics, further bolstering the market presence.

Asia Pacific

Asia Pacific is projected to grow at the highest CAGR as a result of rapid industrialization, increasing investments in electric vehicle production, and growing adoption of renewable energy technologies across major markets such as China, India, Japan, and South Korea. The region's emphasis on energy efficiency, coupled with government initiatives to promote green technologies, is contributing to the accelerated demand for SiC modules. For instance,

- India has set ambitious renewable energy targets, aiming to generate 50% of its electricity from non-fossil fuel sources by 2030. This goal is part of the country's commitment to the Paris Agreement on climate change.

Middle East & Africa and South America

The Middle East & Africa and South America are expected to grow at an average rate in the market due to the relatively slower adoption of electric vehicles and advanced power electronics compared to other regions. However, gradual investments in renewable energy infrastructure and industrial development are contributing to steady market expansion across these emerging economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Products to Strengthen Their Market Positioning

Players launch new product portfolios to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. Such strategic product launches help companies maintain and grow their Silicon Carbide (SiC) module market share in a rapidly evolving industry.

LIST OF KEY SILICON CARBIDE (SiC) MODULE COMPANIES PROFILED

- Wolfspeed, Inc. (Cree Inc.) (U.S.)

- STMicroelectronics (Switzerland)

- Infineon Technologies AG (Germany)

- ROHM Semiconductor (Japan)

- ON Semiconductor (U.S.)

- Microchip Technology, Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Hitachi Energy (Switzerland)

- Fuji Electric Co., Ltd. (Japan)

- Littelfuse, Inc. (U.S.)

- Navitas Semiconductor (U.S.)

- Qorvo (U.S.)

- Danfoss Silicon Power (Germany)

- Global Power Technologies Group (U.S.)

- Toshiba Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Wolfspeed, Inc. launched its new Gen 4 technology platform, aimed at enhancing durability and efficiency while lowering system costs and development time. The platform supports a long-term product roadmap across power modules, discrete components, and bare die products, with offerings in the 1200V, 750V, and 2300V voltage classes.

- September 2024: Wolfspeed, Inc. introduced a new 2300V baseplate-less silicon carbide power module designed for 1500V DC Bus applications. The module aims to enhance efficiency, reliability, durability, and scalability across renewable energy, fast-charging, and energy storage sectors.

- September 2024: STMicroelectronics introduced its fourth-generation STPower silicon carbide MOSFET technology, offering higher power efficiency, density, and robustness. The technology is specifically optimized for traction inverters, a critical component in Electric Vehicle (EV) powertrains.

- May 2024: Littelfuse, Inc. released the IX4352NE low-side gate driver, designed for use with SiC MOSFETs and high-power insulated gate bipolar transistors (IGBTs). This advanced driver targets industrial applications, offering optimized performance for efficient power switching.

- February 2024: Kempower introduced its next-generation charger platform, which incorporates SiC technology across its entire product portfolio. The platform delivers high performance and is designed further to improve the Electric Vehicle (EV) charging experience.

REPORT COVERAGE

The market research report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, product types, and leading applications of Silicon Carbide (SiC) module solutions. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, it encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 29.20% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Module Type

By Voltage Range

By Application

By Region

|

Frequently Asked Questions

The market is projected to record a valuation of USD 9817.3 million by 2034.

In 2026, the market was valued at USD 1263.1 million.

The market is projected to grow at a CAGR of 29.20% during the forecast period.

SiC MOSFET modules are expected to lead the market with the highest CAGR.

The rising adoption of Electric Vehicles (EVs) is anticipated to propel market growth.

Wolfspeed, Inc., STMicroelectronics, Infineon Technologies AG, and ROHM Semiconductor are the top players in the market.

North America dominated the market with a share of 26.06% in 2024.

By application, the energy & utilities application is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us