Silicon Dioxide Market Size, Share & Industry Analysis, By Type (Precipitated Silica, Fumed Silica, Colloidal Silica, and Others), By Application (Industrial Manufacturing, Automotive, Consumer Goods, Electrical & Electronics, and Others), and Regional Forecast, 2026-2034

SILICON DIOXIDE MARKET SIZE AND FUTURE OUTLOOK

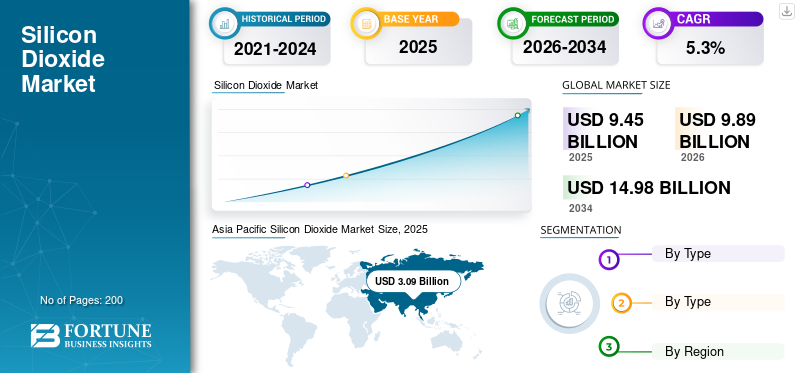

The silicon dioxide market size was valued at USD 9.45 billion in 2025. The market is projected to grow from USD 9.89 billion in 2026 to USD 14.98 billion by 2034 at a CAGR of 5.3% during the forecast period. Asia Pacific dominated the silicon dioxide market with a market share of 32.69% in 2025.

The market showcases global industry engaged in the production, distribution, and consumption of specialty silica materials across product types such as precipitated silica, fumed silica, colloidal silica, and other processed silica forms. The market growth is driven by its diversified application base across industrial manufacturing, automotive, consumer goods, and electrical & electronics sectors. Growth is primarily driven by rising use of silica in green tires, precision polishing, coatings, adhesives, and advanced industrial formulations, where performance requirements increasingly favor specialty silica materials with controlled purity, surface behavior, and application-specific functionality. Key players operating in the market include Evonik Industries AG, Wacker Chemie AG, Nouryon, Solvay S.A., PQ Corporation, and Tokuyama Corporation.

Download Free sample to learn more about this report.

SILICON DIOXIDE MARKET TRENDS

Shift Toward Application-Specific Specialty Silica and Precision Surface Engineering are Emerging Market Trends

A prominent trend in the global market is the move away from treating silica as a simple filler and toward application-specific specialty grades designed around rheology, polishing precision, reinforcement, flow behavior, purity, and surface functionality. Evonik positions precipitated silica as a performance material for tires, oral care, and industrial uses. WACKER sells pyrogenic silica for coatings, adhesives, printing inks, cosmetics, and food-related uses, and Nouryon positions colloidal silica for electronics polishing, coatings, foundry, and fire-resistant glass applications. This suggests that suppliers are increasingly differentiating their portfolios by particle form, surface properties, dispersion behavior, and application performance rather than competing only on bulk tonnage.

Another trend is the growing strategic importance of silica in energy-efficiency, electronics, and advanced industrial processing. Evonik states that synthetic amorphous silica is indispensable in tire manufacture and industrial rubber goods, especially in “green tires” that reduce rolling resistance while improving grip. Nouryon also highlights colloidal silica as a precision abrasive for shaping, smoothing, and polishing silicon, metals, sapphire, and other substrates, thus showing how silica demand is increasingly tied to technically demanding applications rather than commodity-only uses. This does not eliminate traditional industrial demand, but it shows that value growth is shifting toward engineered silica materials with higher technical content and stricter end-use requirements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Diversified End-Use Demand Across Tires, Industrial Processing, Electronics, and Consumer Applications Supports Market Growth

One of the strongest drivers for the Silicon Dioxide market growth is its broad downstream application base across industrial manufacturing, automotive, electrical and electronics, consumer goods, and other specialty uses. Specialty silica is not dependent on a single end-use outlet. Evonik states that synthetic amorphous silica is indispensable in tires and industrial rubber goods, while its dental silica products support oral care formulations. That diversified use pattern helps support baseline demand even when one end-use sector softens.

Automotive remains particularly important as specialty silica plays a direct performance role in tire systems. Evonik states that silica is an essential component in green tires and notes that lower rolling resistance can cut fuel consumption while improving grip. This is commercially meaningful as it links silica demand not only to tire production volumes but also to regulatory and OEM pressure for energy efficiency and performance. At the same time, electrical and electronics demand continues to strengthen the market, as Nouryon highlights colloidal silica for precision polishing and planarization of high-performance substrates used in electronics and advanced manufacturing. That combination of large industrial demand and growing high-value technical uses makes the market more resilient than a narrowly defined specialty additive market.

MARKET RESTRAINTS

Health, Environmental, and Process-Control Pressures Can Limit Expansion and Raise Compliance Costs

A major restraint for the market growth is the regulatory and operational pressure associated with silica exposure, environmental handling, and process discipline. The U.S. Geological Survey notes that the industrial sand and gravel industry remained concerned in 2024 about safety and health regulations and environmental restrictions, especially those related to crystalline silica exposure. OSHA’s crystalline silica rules define respirable crystalline silica hazards in workplace settings, and MSHA’s silica final rule adds tighter exposure control requirements for mines. Even though the market includes synthetic and processed forms beyond crystalline sand, the broader silica industry still operates under increasing scrutiny around worker safety, dust handling, and process controls.

This restraint is also relevant on the production side as specialty silica manufacturing can involve wastewater, by-products, washing, drying, and energy-intensive processing steps that add cost and complexity. The European Commission-backed LIFE project on precipitated silica wastewater states that precipitated silica production generates a high-conductivity salt stream and significant water demand due to washing needs. This makaes producers invest heavily in environmental management, process optimization, and compliance systems, which can limit margin flexibility and raise barriers for smaller suppliers.

MARKET OPPORTUNITIES

Green Tires, Electronics Polishing, and Higher-Performance Industrial Formulations Create Premium Growth Space

One of the significant opportunities for market growth is the continued expansion of specialty silica in tire and rubber applications, especially in fuel-efficient and EV-oriented tire systems. Evonik states that synthetic amorphous silica is indispensable in the treads of green tires and notes that improved silica-silane technology can reduce rolling resistance while maintaining wet grip and durability. This creates a strong opportunity for silica suppliers as performance requirements are rising, and customers are increasingly willing to use higher-value formulations that support safety, energy efficiency, and lower emissions.

Another major opportunity lies in electrical and electronics uses. Nouryon states that colloidal silica is used as a high-tech abrasive for shaping, smoothing, and polishing silicon, metals, sapphire, and other precision substrate materials. As semiconductor manufacturing, advanced packaging, optical materials, and precision surface finishing continue to expand, suppliers of high-consistency colloidal and high-purity silica materials should be well placed to capture incremental demand. Similar opportunity lies in personal care, healthcare, and industrial coatings, where silica is used for texture control, thickening, flow improvement, polishing, and formulation stability.

MARKET CHALLENGES

Demand Diversity Helps, but the Market Remains Technically Fragmented and Application-Specific

A major challenge for the market is that although silica serves many applications, those applications often require very different performance profiles and processing characteristics. Precipitated silica, fumed silica, colloidal silica, and other specialty forms are not interchangeable across all end uses. Evonik’s oral care silica is engineered for controlled cleaning performance, Nouryon’s colloidal silica is positioned for polishing and foundry bonding, and WACKER’s pyrogenic silica is tailored to rheology, flow, and reinforcement functions in coatings, adhesives, elastomers, and powders. That fragmentation means suppliers cannot rely on a one-grade-fits-all strategy, and customers often require strict application-specific qualification.

The market also faces the challenge that high-value uses are attractive but technically demanding. Product consistency, particle-size control, surface treatment, dispersion behavior, and contamination control can materially affect performance in electronics, healthcare, premium coatings, or advanced elastomer systems. As a result, growth is supported by application diversity, but the market remains more complex than many volume-based filler market as it depends on technical service, process know-how, and ongoing product development rather than on scale alone.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions can affect the market by increasing uncertainty around raw-material access, specialty chemical trade flows, energy costs, and downstream manufacturing competitiveness. The OECD’s 2024 inventory states that export restrictions on industrial raw materials are becoming increasingly prevalent and more prohibitive, with spillover effects across downstream supply chains. Silicon dioxide is not always treated as a headline critical mineral, but it sits inside trade-sensitive industrial systems tied to chemicals, minerals processing, automotive manufacturing, electronics, and advanced materials. That means tighter export controls, higher logistics risk, or regional industrial policy shifts can influence availability and delivered pricing.

This effect is especially relevant where silica demand is connected to globally integrated industries such as tires, coatings, adhesives, semiconductors, and precision manufacturing. Regions dependent on imported specialty silica grades or application-specific intermediates can face greater supply-chain sensitivity than commodity market size alone would suggest. Thus, the market is influenced not only by direct silica trade, but also by the broader geopolitical stability of automotive, electronics, and industrial manufacturing ecosystems.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly centered on particle engineering, surface functionality, purity optimization, dispersion behavior, and application-specific performance rather than on a simple expansion of filler volume. Evonik’s dental silicas are designed around different cleaning levels and oral care needs, while its tire silica work focuses on reinforcement and rolling-resistance performance. Nouryon highlights colloidal silica functionality in polishing, planarization, foundry, and protective coatings, and WACKER emphasizes the role of pyrogenic silica in rheology control, storage stability, and flow optimization. This shows that silica R&D is becoming more targeted toward how the material behaves in a finished system rather than just how much is consumed.

That makes silicon dioxide R&D highly application-led. In electronics, the focus is on defect-free polishing and controlled particle interaction. In tires and elastomers, the focus is on balancing reinforcement, energy efficiency, and processability. In coatings, adhesives, cosmetics, and industrial powders, the focus is on rheology, thixotropy, free-flow properties, and stability. Across the market, development priorities are likely to remain centered on better functional performance, cleaner processing, and tighter specification control.

SEGMENTATION ANALYSIS

By Type

Precipitated Silica Dominates Due to Its Broad Suitability Across Tires, Rubber, Oral Care, and Industrial Applications

Based on type, the market is segmented into precipitated silica, fumed silica, colloidal silica, and others.

Among these, precipitated silica is expected to hold the dominant silicon dioxide market share as it has the broadest commercial footprint across tires, industrial rubber goods, oral care, and other industrial applications. Evonik explicitly positions precipitated silica as an essential component in green tires and also markets dental silicas for oral care, showing its wide end-use relevance. This breadth of use supports its leadership in volume terms within the market.

The fumed silica segment also holds an important position due to its strong value contribution in coatings, adhesives, sealants, printing inks, cosmetics, and high-performance formulations. WACKER’s HDK pyrogenic silica portfolio highlights its use in rheology control, flow modification, and elastomer reinforcement.

The colloidal silica segment remains commercially important due to its use in electronics polishing, foundry binders, fire-resistant glass, and precision surface treatment.

The others segment includes silica gel and other specialty processed silica forms used in niche industrial and consumer applications.

By Application

To know how our report can help streamline your business, Speak to Analyst

Industrial Manufacturing Leads Due to Silica’s Broad Functional Role Across Process Industries, Coatings, Foundry, Rubber, and Surface Treatment

Based on application, the market is segmented into industrial manufacturing, automotive, consumer goods, electrical & electronics, and others.

Among these, industrial manufacturing is expected to hold the leading share of the global market. This dominance is supported by silica’s broad use in coatings, adhesives, printing inks, foundry, polishing, refractory-related systems, process materials, and industrial formulations. WACKER and Nouryon both position specialty silica products across a wide range of manufacturing uses, indicating increasing demand from multi-industries.

The automotive segment is also expected to account for a significant share of the market as precipitated silica plays a central role in tire and rubber performance.

Electrical & electronics remains an important high-value segment as colloidal silica is widely used for polishing and planarization of precision substrates.

The others segment includes healthcare, food-related uses, and additional specialty markets where performance requirements and purity levels can support premium pricing.

SILICON DIOXIDE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Silicon Dioxide Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region benefits from deep manufacturing intensity across automotive, consumer goods, industrial production, and electronics, as well as strong relevance in tire demand and precision materials processing. This makes Asia Pacific the largest market by volume in a specialty silica framework, especially as silica demand here is linked to multiple large downstream sectors rather than one niche application alone. The region also benefits from strong supply-chain integration in electronics polishing and rubber processing applications.

China Silicon Dioxide Market

China’s market is one of the largest globally, with 2025 revenue at USD 1.22 billion, representing roughly 12.9% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to register steady growth during the forecast period. The region benefits from strong automotive demand, industrial coatings and adhesives use, and a developed market for consumer and technical formulations. North America is also relevant through advanced industrial processing and premium application requirements, which support value realization for higher-performance silica grades.

U.S. Silicon Dioxide Market

In 2025, the U.S. represented a USD 1.73 billion market, driven primarily by increasing demand from the industrial sector. The U.S. accounts for roughly 18.3% of global market sales.

Europe

Europe is expected to maintain a significant position in the market due to its mature tire, coatings, specialty chemicals, industrial manufacturing, and consumer-products base. The region is especially relevant in high-performance silica applications where energy efficiency, emissions reduction, formulation quality, and regulatory performance are significant. This supports stable demand for precipitated and fumed silica grades used in advanced manufacturing and premium end products.

Germany Silicon Dioxide Market

The Germany market in 2025 was valued at around USD 0.66 billion, representing roughly 7.0% of global market revenues.

U.K. Silicon Dioxide Market

The U.K. market in 2025 was valued at around USD 0.37 billion, representing roughly 3.9% of global market revenues.

Latin America

Latin America is a smaller but relevant market, supported by industrial manufacturing, automotive demand, and consumer-related applications. The region does not stand out as the largest global center for specialty silica, but it remains commercially meaningful as silica is used across several downstream sectors rather than depending on a single demand outlet. Growth in this region is likely to be tied to broader industrial expansion and localized formulation demand.

Brazil Silicon Dioxide Market

Brazil market in 2025 was valued at around USD 0.42 billion, representing roughly 4.4% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller, but opportunities exist in industrial manufacturing, coatings, adhesives, construction materials applications, and selected consumer uses. Growth is likely to depend more on industrial diversification, project activity, and import accessibility than on the presence of a large domestic specialty silica production base.

GCC Silicon Dioxide Market

GCC market in 2025 was valued at around USD 0.29 billion, representing roughly 3.0% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key players are Competing Through Application-Led Product Positioning and Capacity Expansion

The global silicon dioxide market is moderately fragmented across specialty silica producers, colloidal silica suppliers, fumed silica manufacturers, high-purity quartz / fused silica specialists, and broader minerals companies with silica-focused portfolios. Competition is shaped by purity control, surface treatment, rheology performance, polishing performance, reinforcement capability, and the ability to supply application-specific grades for industrial manufacturing, automotive, consumer goods, electrical & electronics, and other specialty uses. Evonik highlights a broad silica portfolio spanning standard grades and specialty grades for regulated uses, WACKER positions pyrogenic silica in high-performance formulation markets, Nouryon is expanding colloidal silica capacity, Solvay is pushing circular silica, PQ is scaling specialty silica in Asia, and Tata Chemicals continues to expand tyre and rubber-focused precipitated silica offerings.

LIST OF KEY SILICON DIOXIDE COMPANIES PROFILED

- Evonik Industries AG (Germany)

- Wacker Chemie AG (Germany)

- Nouryon (U.S.)

- Solvay S.A. (Belgium)

- PQ Corporation (U.S.)

- Tokuyama Corporation (Japan)

- Cabot Corporation (U.S.)

- OCI Company Ltd. (South Korea)

- Tata Chemicals Limited (India)

- Madhu Silica Pvt. Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Nouryon completed a nearly 50% capacity expansion for Levasil colloidal silica at Green Bay, Wisconsin, to address rising demand and expand its global colloidal silica footprint.

- January 2024: Evonik announced a 50% expansion of precipitated silica production at its Charleston, South Carolina site, driven by strong U.S. demand, especially for green tires.

- November 2024: PQ Corporation completed the expansion of its silica production facility in Pasuruan, Indonesia, including a new micronizer to serve growing Asian demand for high-quality silicas.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, Type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 5.3% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 9.45 billion in 2025 and is projected to reach USD 14.98 billion by 2034.

Recording a CAGR of 5.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The industrial manufacturing segment is expected to lead market during the forecast period.

Asia Pacific held the highest market share in 2025.

Diversified end-use demand across tires, industrial processing, electronics, and consumer applications are driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us