Smart Finance Hardware Market Size, Share & Industry Analysis, By Hardware Type (Smart POS (Point of Sale) Terminals, Smart ATMs (Automated Teller Machines), Kiosks & Self-Service Terminals, Payment Cards & Terminals with Embedded Chips, IoT-Enabled Devices & Sensors, Digital Signage & Display Hardware), By Deployment Type (On-Premises, Cloud-Based / Hybrid, & Field-Based Deployment), By End User (Banks & Financial Institutions, Independent ATM Deployers, Non-Banking Financial Companies, Corporate & Institutional Banks, Government Institutions, Fintech Companies) & Regional Forecast, 2026-2034

SMART FINANCE HARDWARE MARKET SIZE AND FUTURE OUTLOOK

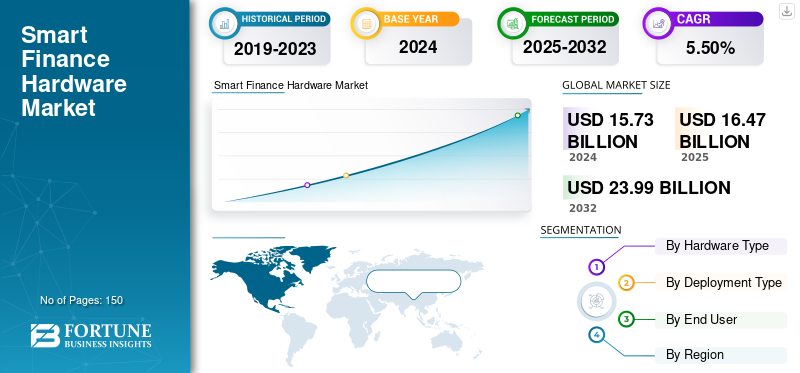

The global smart finance hardware market size was valued at USD 16.47 billion in 2025 and is projected to grow from USD 17.29 billion in 2026 to USD 26.43 billion by 2034, exhibiting a CAGR of 5.45% during the forecast period. Asia Pacific dominated the global smart finance hardware market with a market share of 36.2% in 2025.

Smart finance hardware is referred to the backbone of modern financial systems that aids in integrating digital solutions into physical infrastructure. It includes smart POS terminals, ATMs, biometric payment systems, and blockchain powered hardware which enhances financial transactions through security, automation and connectivity.

The market is experiencing a rapid growth due to rising demand for fraud prevention, digital payments, adoption of contactless technologies, and increasing fintech and bank collaborations. Moreover, regulatory pushes for secure authentication and growth of e-commerce also boosts the overall market growth.

Key players operating in the market include Diebold Nixdorf, NCR Atleos, Hyosung TNS, GRG Banking Equipment Co. Ltd., PAX Technology Inc., Ingenico Group, VeriFone Systems Inc., Hitachi Channel Solutions Corp. and others. These players are adopting strategies including partnerships with banks and retailers, integration of AI and biometrics and expansion into emerging markets across the globe to sustain the market competition.

Download Free sample to learn more about this report.

Smart Finance Hardware Market Key Takeaways

- 2025 Market Size: USD 16.47 Billion

- 2026 Market Size: USD 17.29 Billion

- 2034 Forecast Market Size: USD 26.43 Billion

- CAGR: 5.45% from 2026–2034

- Asia Pacific dominated the smart finance hardware market with a 36.20% share in 2025.

- Smart POS terminals segment is projected to account for 33.65% of the market in 2026.

- On-premises segment is projected to account for 63.45% of the market in 2026.

Asia Pacific

Asia Pacific led the market with USD 5.96 billion in 2025 and is projected to reach USD 6.32 billion in 2026.

North America

North America generated USD 5.13 billion in revenue in 2025 and is projected to reach USD 5.42 billion in 2026.

Europe

Europe was valued at USD 4.15 billion in 2025 and is estimated to reach USD 4.28 billion in 2026.

U.S.

The market is expected to reach USD 4.23 billion in revenue by 2026.

Japan

Rising adoption of digital payment and smart banking technologies is supporting market growth.

Read More

MARKET DYNAMICS

Market Drivers

Rising Adoption of Digital and Contactless Payments Drives the Market Development

The growing adoption of digital and contactless payments is a prominent driver for smart finance hardware market growth. Consumers are growingly preferring secure, fast and cashless transactions, allowing businesses to deploy smart POS terminals, advanced ATMs and biometric payment devices.

This shift is further aided by the government initiatives that promote digital payment ecosystems, financial inclusion programs, and improved internet connectivity. Banks and fintech firms are also growingly investing in connected and secure hardware to reduce the fraud occurrence and enhance customer experience. With mobile wallets and tap-to-pay methods gaining attention, the demand for reliable, efficient and secure smart finance hardware tends to accelerate.

Market Restraints

High Initial Investment and Security Concerns to Deters the Market Growth

Higher initial investment is a crucial restraint for the market growth, as integrating, deploying and maintaining advanced devices demands substantial capital. Different small and mid-sized financial institutions tend to struggle to justify these costs thus slowing its adoption. Additionally, sensitive security concerns including risks of biometric misuse, data breaches, and cyberattacks generates hesitation among the companies handling sensitive financial information. Compliance with stringent regulations also increases the expenses. These factors together, hampers the overall market growth.

Market Opportunities

Expansion in Emerging Markets and Financial Inclusion Programs Offers Lucrative Growth Opportunities

Developing markets tend to offer a strong opportunity for smart finance hardware as banks, governments and fintech work to enhance the financial inclusion. Wide unbanked populations generate demand for IoT based POS devices, portable microfinance terminals, and biometric authentication tools that are capable of operating in remote regions.

Additionally, the expansion of agent banking networks as well as rural digital infrastructure also accelerates the product adoption. Financial institutions are highly investing in low-cost payment devices, mobile kiosks, and safe onboarding systems to aid small businesses and microfinance.

SMART FINANCE HARDWARE MARKET TRENDS

Integration of AI and IoT in Financial Hardware Has Emerged as a Prominent Market Trend

One of the major market trends is surging integration of IoT and AI into a smart finance hardware that transforms the way financial transactions and devices operate. AI-based analytics allow for intelligent decision-making, fraud detection, and personalized services, whereas IoT connectivity enables devices including ATMs and POS terminals to communicate in real time. This combination also aids in predictive maintenance, ensures faster and secure transactions and reduces downtime. Financial institutions are benefiting from ongoing monitoring, improved operational efficiency and automated update.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Hardware Type

Versatility of Smart POS Terminals Integrating Inventory Management, Payment Processing, and Data Analytics into a Single Device Boosts the Segment Growth

Based on hardware type, the market is segmented into smart POS (Point of Sale) terminals, smart ATMs (Automated Teller Machines), kiosks & self-service terminals, payment cards & terminals with embedded chips, IoT-enabled devices & sensors, digital signage & display hardware, and others.

In 2024, smart POS terminals segment held the largest smart finance hardware market share and with a revenue of USD 5.23 billion. This dominance is driven by its versatility in integrating inventory management, payment processing, and data analytics into a single device. Additionally, the growing trend of digital payments and need for secure, seamless and contactless transaction solutions across hospitality and retail sectors also augments the segment growth. The smart POS terminals segment will account for 33.65% market share in 2026.

On the other hand, the IoT-enabled devices & sensors segment held the highest CAGR of 7.4% in 2024. This growth is owing to their expanding use in real-time monitoring, predictive maintenance and automation across the industries. Additionally, the growing adoption of connected ecosystems in logistics, smart cities and financial infrastructure also accelerates the segment growth.

By Deployment Type

Larger Upfront Infrastructure Drives On-Premise Segment Growth

The market is divided into on-premises, cloud-based / hybrid, and field-based deployment, based on deployment type.

Among these, on-premises segment dominated the market with a revenue share of USD 10.03 billion in 2024. This segment includes a larger upfront infrastructure, integration services and maintenance contracts. This aids in the segment’s growth even though field based systems are increasing in terms of adoption and installation rate. The on-premises segment will account for 63.45% market share in 2026.

The field-based deployment segment held highest CAGR of 6.5% in 2024. This segmental growth is attributed to the growing adoption of portable and mobile financial hardware that aids in doorstep banking, remote payment services and microfinance. Additionally, growth in demand for contactless transactions, IoT based field devices, and agent based banking in emerging markets accelerates this trend, thus enabling financial institutions to reach remote population.

By End User

Increasing Adoption of Secure and Automated Transaction Systems Drive Banks & Financial Institution Segment Growth

The market is divided into banks & financial institutions, independent ATM deployers, non-banking financial companies, corporate & institutional bank, government institution, fintech companies, and others, based on end user.

Among these, the banks & financial Institutions segment dominated the market with a revenue share of USD 6.76 billion in 2024. Increasing adoption of secure and automated transaction systems, integration of AI-enabled analytics and rising demand for fraud prevention tends to drive the overall market growth. Additionally, these institutions are also investing heavily in biometric authentication, smart POS devices and IoT connected hardware to enhance compliance and efficiency. The banks & financial Institutions segment is expected to account for 42.21% of the market in 2026.

The fintech companies segment held highest CAGR of 7.4% in 2024. This segmental growth is attributed to growing demand for advanced payment infrastructure, secure authentication hardware and AI-enabled transaction systems.

To know how our report can help streamline your business, Speak to Analyst

SMART FINANCE HARDWARE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America accounted for USD 5.13 Billion in 2025, representing 31.10% of the global market share, and is projected to reach USD 5.42 Billion in 2026. This growth is due to advanced digital payment adoption, higher investment in AI and IoT technologies and stronger fintech innovation. Additionally, the growing use of contactless payments, supportive regulations and robust cybersecurity infrastructure in the U.S. also contributes to the regional market growth. The U.S. leads the regional market with an expected revenue share of USD 4.23 billion in 2026.

Europe

The Europe market was valued at USD 4.15 Billion in 2025, capturing 25.17% of global revenue, and is estimated to reach USD 4.28 Billion in 2026. This growth is attributed to the strong regulatory support for safe digital payments, increasing adoption of contactless and biometric technologies as well as the presence of different advanced banking infrastructure. U.K., Germany, and France are some of the major contributors to the market growth with an expected revenue share of USD 0.82 billion, USD 0.83 billion, and USD 0.39 billion respectively by 2026.

Asia Pacific

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 36.20% of the global market, reaching a valuation of USD 5.96 Billion, and is projected to grow to USD 6.32 Billion in 2026. The region also held highest CAGR of 6.6% in 2024. This regional growth is due to stronger mobile payment adoption, growing digital economy, and a shift of unbanked population toward digital finance. Additionally, supporting government policies, heavy investment in AI-IoT financial infrastructure and fintech growth also boosts the regional market growth. India and China are the major contributors for the market growth with an expected revenue share of USD 1.05 billion and USD 2.23 billion by 2026.

South America and Middle East & Africa

Middle East & Africa contributed approximately USD 0.68 Billion to the global market in 2025, accounting for 4.10% share, and is expected to reach USD 0.69 Billion in 2026. The regional growth is attributed to expanding digital payment adoption, rising mobile banking and government initiatives for financial inclusion. GCC countries are predicted to have a market share of USD 0.22 billion by 2025.

Latin America

The Latin America region captured 3.37% of the global market in 2025, generating USD 0.56 Billion in revenue, and is projected to reach USD 0.58 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Adopting Innovative Strategies to Retain their Market Positions

The management consulting services industry features different global giants including Diebold Nixdorf, NCR Atleos, Hyosung TNS, GRG Banking Equipment Co. Ltd., PAX Technology Inc., Ingenico Group, VeriFone Systems Inc., Hitachi Channel Solutions Corp., and others. These companies are focusing on innovating their product portfolio, adoption new technologies and other strategies to sustain the competition and retain market position.

LIST OF KEY SMART FINANCE HARDWARE COMPANIES PROFILED:

- Diebold Nixdorf (U.S.)

- NCR Atleos (U.S.)

- Hyosung TNS (South Korea)

- GRG Banking Equipment Co. Ltd. (China)

- PAX Technology Inc. (China)

- Ingenico Group (France)

- VeriFone Systems Inc. (U.S.)

- Hitachi Channel Solutions Corp. (Japan)

- OKI Electric Industry Co., Ltd. (Japan)

- Castles Technology Co., Ltd. (China)

- Nexgo (SZ Xinguodu Technology) (China)

- AURES Group (France)

KEY INDUSTRY DEVELOPMENTS:

- In October 2025, Ant International launched world’s first iris authentication feature in smart-glasses payment solution. Alipay+ GlassPay, Ant International’s smart glasses-embedded payment solution, will add iris authentication to its security verification capabilities, alongside voiceprint authentication.

- In October 2025, DIB, the world’s first Islamic bank and the largest in the UAE, has announced a strategic partnership with HCLTech, a leading global technology company, to accelerate the adoption of Artificial Intelligence (AI) across its ecosystem. Announced at GITEX GLOBAL 2025, the partnership reinforces DIB’s commitment to shaping the future of Islamic finance through responsible innovation.

- In September 2025, Electronics manufacturing services firm Optiemus Infracom and Ordinary Theory LLC USA have announced to set up a joint venture for manufacturing, market development, and sales of smart enterprise hardware and integrated industrial solutions. The joint venture will focus on creating smart enterprise hardware solutions spanning payments, retail, logistics, and AI.

- In August 2025, STC Bank launched its first financing product, "Smart Finance" a fully electronic, Sharia compliant product, available within minutes and with a maximum limit of USD 13,330.85. The new financing product aims to meet the financial needs of the bank's customers and support individuals by offering quick financing solutions, flexible terms, and simple steps.

- In July 2022, Huawei Cloud launched its Cloud Native Core Banking solution which is designed to serve as a foundation for agile innovation in the both the traditional and new digital banking industries.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, hardware type, deployment type and end user of the product. Besides this, it offers insights into the smart finance hardware market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 5.45% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD billion) |

| Segmentation |

By Hardware Type

By Deployment Type

By End User

By Region

|

Frequently Asked Questions

The market is expected to exhibit steady growth at a CAGR of 5.45% during the forecast period.

Rising adoption of digital and contactless payments drives the market growth.

Diebold Nixdorf, NCR Atleos, Hyosung TNS, GRG Banking Equipment Co. Ltd., PAX Technology Inc., Ingenico Group, VeriFone Systems Inc., Hitachi Channel Solutions Corp. and others are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 5.96 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us