Smart Pills Market Size, Share & Industry Analysis, By Application (Diagnostic Imaging, Drug Delivery, and Patient Monitoring), By Disease Indication (Gastrointestinal Disorders, Cancer, Neurological Disorders, Infectious Diseases, and Others), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Smart Pills Market Size and Future Outlook

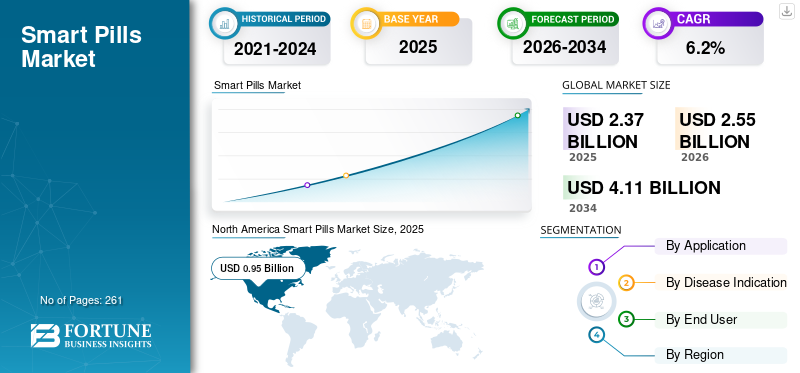

The global smart pills market size was valued at USD 2.37 billion in 2025 and is projected to grow from USD 2.55 billion in 2026 to USD 4.11 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the smart pills market with a market share of 40.08% in 2025.

Smart pills are ingestible capsules containing sensors, microelectronics, or cameras that help diagnose chronic conditions, monitor vital signs, or confirm medication adherence. The rising prevalence of chronic conditions, increasing demand for minimally invasive diagnostics, and technological advancements in digital health and capsule endoscopy products are resulting in a growing adoption rate of these products in the market. The ever-increasing healthcare expenditure and improving healthcare access are further supporting the demand for smart pills in the market.

- For instance, according to the data published by the Global TB Report, it was reported that about 2.8 million people were estimated to have been affected by tuberculosis in India in 2023.

Additionally, the growing research and development activities among major players, such as Medtronic and Olympus Corporation, for these capsule endoscopy products are further driving demand in the market.

Download Free sample to learn more about this report.

Smart Pills Market Key Takeaways

- 2025 Market Size: USD 2.37 billion

- 2026 Market Size: USD 2.55 billion

- 2034 Forecast Market Size: USD 4.11 billion

- CAGR: 6.2% from 2026–2034

- North America dominated the smart pills market with a 40.08% share in 2025.

- Hospitals & ASCs dominated the market and are projected to hold a 69.1% share in 2026.

- The gastrointestinal disorders segment accounted for 74.1% of the market in 2025.

North America

North America led the market at USD 0.95 billion in 2025.

Asia Pacific

Asia Pacific is the fastest-growing region, projected to reach USD 0.62 billion by 2026.

Europe

Europe is projected to reach USD 0.69 billion by 2026.

U.S.

The U.S. market is projected to reach USD 0.90 billion by 2026.

Japan

The Japan market is projected to reach USD 0.17 billion by 2026.

Read More

Smart Pills Market Trends

Technological Advancements in the Smart Pill Products to Fuel the Demand

The advancements in digital health, capsule endoscopy, and smart pill technologies represent a global market trend, as advanced ingestible devices are evolving from passive imaging tools into artificial intelligence-enabled, data-driven diagnostic devices. The advancements, such as high-resolution imaging sensors, coupled with extended battery life, are resulting in complete small bowel and colon visualization. The incorporation of artificial intelligence into capsule reading software has enhanced diagnostic accuracy and improved patient care.

Additionally, next-generation products are integrating multi-sensor technologies, including pH, pressure, and temperature monitoring. They are being studied for controlled drug delivery applications, which is anticipated to boost adoption in the market further.

- In January 2026, Researchers at Massachusetts Institute of Technology (MIT) developed an ingestible smart pill that uses radio frequency to communicate from the stomach when patients have taken their medications.

Other Prominent Trends

- Miniaturization of multisensor ingestible devices enabling multi‑parameter monitoring.

- Rise of digital therapeutics and decentralized clinical trials using ingestible sensors.

- Regulatory approvals and payer-backed adherence programs for commercial scaling.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Prevalence of Chronic Disorders to Boost Market Growth

The growing prevalence of chronic diseases, including cancer, gastrointestinal disorders, and others, is resulting in the increasing demand for minimally invasive diagnostic solutions among the patient population, subsequently fueling the adoption of smart pills in the market.

- For instance, according to 2021 data published by the Oxford Academic, it was reported that about 1 in 4 patients has gastrointestinal cancer globally.

This, coupled with growing investments in advanced remote patient monitoring diagnostic technologies capable of complete gastrointestinal tract visualization, early detection, and enhanced patient compliance, is also supporting the adoption rate of ingestible diagnostic solutions in the market. Therefore, the factors mentioned above, along with the increasing focus of investment in R&D activities to launch novel products, are anticipated to drive the demand for these products, thereby supporting the global smart pills market size.

Market Restraints

High Device & Procedure Costs to Limit the Market Growth

The high device and procedure costs are a major restraint in the market, especially for capsule endoscopy and related ingestible diagnostic products. The costs associated with the disposable capsule device, fees for specialist interpretation, facility charges, and associated clinical services increase the cost per patient. The financial burden is further increased with an inadequate reimbursement framework, making it challenging for patients and smaller healthcare facilities in emerging regions to adopt smart pills. Therefore, rising costs may hamper the market penetration of these products despite clinical advantages, including non-invasiveness and enhanced patient comfort.

- For instance, according to the 2025 data published by Biology Insights, it was reported that the total billed cost for a capsule endoscopy typically ranges from USD 1,000 to over USD 3,000 before any adjustments from insurance or self-pay discounts are applied.

Market Opportunities

Growing Healthcare Expenditure & Screening Programs

The rising healthcare expenditure and the expansion of organized screening programs present a lucrative market opportunity for the global market. Increasing investments in healthcare infrastructure among private and public organizations, preventative care, and early detection initiatives are fueling demand for minimally invasive diagnostic products, including smart pills and capsule endoscopy, further supporting the adoption rate of these products in the market.

The growing allocation of resources to healthcare is increasing access to routine screening services and further enabling the adoption of technologically advanced tools that enhance early diagnosis, improve patient outcomes, and reduce long-term treatment costs.

- According to data published by the World Bank, global healthcare expenditure reached USD 12.4 trillion in 2022.

Market Challenges

Limited Healthcare Access in Developing Nations to Hamper the Market Growth

There is a growing demand for minimally invasive diagnostics among the patient population. However, shortage of technologically advanced products, limited healthcare expenditure, coupled with an inadequate reimbursement framework, especially in developing countries, are resulting in limited access to healthcare facilities among the patient population.

Furthermore, a limited number of healthcare settings and limited professionals, among others, are some of the crucial factors, resulting in the adoption of smart pills among the patient population, particularly in developing markets, including Mexico, Brazil, among others.

- For instance, according to the 2025 data published by the World Bank Group (WBG), the combined government and donor spending on health averaged just USD 17.0 per capita in low-income countries.

Other Prominent Challenges

- Stringent regulatory approval pathways and limited patient acceptance in emerging countries.

SEGMENTATION ANALYSIS

By Application

Increasing Prevalence of Chronic Conditions Led to the Diagnostic Imaging Segmental Dominance

Based on the application, the market is classified into diagnostic imaging, drug delivery, and patient monitoring.

To know how our report can help streamline your business, Speak to Analyst

The diagnostic imaging segment held the largest revenue share in 2025. The growth is owing to the growing prevalence of chronic conditions among the patient population, resulting in a rising number of diagnostic procedures and demand for smart pills globally. This, along with the increasing focus of key players on launching novel solutions, is further expected to support the global smart pills market growth.

- For instance, according to 2022 statistics published by the Centers for Disease Control & Prevention (CDC), about 1.9 million cancer cases were reported in the U.S.

The patient monitoring segment is expected to grow at a CAGR of 6.4% over the forecast period.

By Disease Indication

Increasing Prevalence of Gastrointestinal Disorders Led to the Dominance of the Segment

Based on disease indication, the market is segmented into gastrointestinal disorders, cancer, neurological disorders, infectious diseases, and others.

The gastrointestinal disorders segment dominated the global market in 2025. By disease indication, the segment accounted for 74.1% of the market in 2025. The growth is due to the increasing prevalence of gastrointestinal disorders such as Crohn’s disease and others, resulting in a growing demand for capsule endoscopy products, thereby supporting the adoption rate of these solutions in the market.

- For instance, according to data published by the National Center for Biotechnology Information (NCBI), it was reported that about 783.95 million cases were registered for gastroesophageal reflux disease (GERD) worldwide in 2019.

The segment of cancer is set to flourish with a growth rate of 8.2% across the forecast period.

By End-user

Increasing Number of Ambulatory Surgical Centers Led to the Hospitals & ASCs Segmental Dominance

Based on end user, the market is categorized into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025. The growing prevalence of chronic conditions, rising number of hospitals and ambulatory surgical centers, among others, are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold an 69.1% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 6.8% CAGR during the forecast period.

Smart Pills Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Smart Pills Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 0.89 billion, and also led the leading share in 2025 with USD 0.95 billion. The increasing prevalence of chronic conditions, strong clinical adoption, and trials, among others, are some of the factors contributing to the growth of the segment in the market.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), the prevalence of inflammatory bowel disease (IBD) is estimated between 2.4 and 3.1 million among patients in the U.S.

U.S. Smart Pills Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.90 billion in 2026, accounting for roughly 35.5% of global sales.

Europe

Europe is projected to record a growth rate of 5.4% in the coming years, which is the second highest among all regions, and expected to reach a valuation of USD 0.69 billion by 2026. The significant adoption and regulatory pilots, strong R&D presence are likely to support the market growth.

U.K Smart Pills Market

The U.K. market in 2026 is estimated at around USD 0.12 billion, representing roughly 4.7% of global revenues.

Germany Smart Pills Market

Germany’s market is projected to reach approximately USD 0.15 billion in 2026, equivalent to around 5.9% of global sales.

Asia Pacific

The Asia Pacific market is estimated to reach USD 0.62 billion in 2026 and secure the position of the third-largest region. The fastest growth potential due to large patient populations and rising healthcare access is likely to support the development of the market. In the region, India and China are both estimated to reach USD 0.07 billion and USD 0.17 billion, respectively, in 2026.

Japan Smart Pills Market

The Japan market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 6.7% of global revenues. Japan has historically reported a relatively high prevalence of chronic conditions, along with a growing adoption rate of these products.

China Smart Pills Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.17 billion, representing roughly 6.7% of global sales.

India Smart Pills Market

The Indian market size in 2026 is estimated at around USD 0.07 billion, accounting for roughly 2.8% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are anticipated to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.12 billion by 2026. The growth is owing to the increasing public healthcare investment and healthcare expenditure in the region. The Middle East & Africa are also expected to grow due to rising research and development activities aimed at launching novel products. In the Middle East & Africa, the GCC is set to reach a value of USD 0.05 billion by 2026.

South Africa Smart Pills Market

The South Africa market is projected to reach around USD 0.02 billion by 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Adoption of Products to Strengthen the Key Players’ Growth Strategies

A robust product portfolio, along with a significant focus on inorganic growth strategies worldwide, is one of the key factors supporting the dominance of these companies in the market. Medtronic and Olympus Corporation are major companies in the market in 2025. Furthermore, the growing focus of major companies on strategic initiatives to increase the adoption of these products is anticipated to strengthen their presence, further supporting the global smart pills market share.

- For instance, in December 2024, Medtronic announced that the University of Miami Health System (UHealth) successfully performed the first-ever patient procedure ingestion using its next-generation PillCam Genius SB capsule endoscopy kit, which offers physicians and patients improved flexibility during the procedure.

Other key players, including CapsoVision, Inc., and others, are also growing in the market, primarily owing to their growing emphasis on collaborations among the other players to strengthen their brand presence in the market.

List of Key Smart Pills Companies Profiled in the Report

- Medtronic (U.S.)

- Olympus Corporation (Japan)

- CapsoVision, Inc. (U.S.)

- INTROMEDIC (South Korea)

- JINSHAN Science & Technology (China)

- AnX Robotics (U.S.)

- etectRx (U.S.)

- Shenzhen Zifu Medical Technology Co., Ltd. (China)

- Ankon Technologies (Wuhan) Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- November 2025 – CapsoVision, Inc., submitted an application to the U.S. FDA requesting Breakthrough Device Designation (BDD) to accelerate development of the company’s CapsoCam UGI capsule endoscopy system for use in early-stage pancreatic cancer detection.

- June 2025 – California Institute of Technology researchers developed a smart capsule called PillTrek, which can measure pH, temperature, and a variety of different biomarkers with an aim to provide novel solutions.

- May 2025 – AnX Robotica received FDA 510(k) approval of MotiliCap and its companion software, MotiliScan. This approval accelerates the company’s growth in GI motility monitoring, offering clinicians an advanced, non-invasive tool for assessing whole-gut transit times.

- January 2025 – CapsoVision, Inc., a company in innovative endoscopic capsule technology, received U.S. FDA approval for the CapsoCam Plus, a capsule endoscopy system for remote ingestion. This helped the company in strengthening its presence.

- June 2024 – USC Viterbi innovations in wearable electronics and AI have led to the development of ingestible sensors that not only detect stomach gases but also provide real-time location tracking with an aim to advance the small pill technology.

- April 2022 – AARDEX Group partnered with etectRx to combine etectRx’s smart pill, the ID-Cap System, and AARDEX Group’s MEMS Adherence Software (MEMS AS) to track medication-taking behaviors.

- December 2019 – etectRx received U.S. FDA approval for the etectRx ID-CAP System, a pill loaded with sensors that wirelessly communicates to a system outside the body without physical contact, to offer innovative solutions.

REPORT COVERAGE

The report provides a detailed global smart pills market analysis and focuses on key aspects such as leading companies and market segmentation, including application, disease indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Application, Disease Indication, End User, and Region |

| By Application |

|

| By Disease Indication |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.37 billion in 2025 and is projected to reach USD 4.11 billion by 2034.

In 2025, North Americas market value stood at USD 0.95 billion.

Growing at a CAGR of 6.2%, the market will exhibit steady growth over the forecast period.

By application, the diagnostic imaging segment is the leading segment in this market.

The introduction of advanced smart pills is one of the major factors driving the market's growth.

Medtronic and Olympus Corporation are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic diseases, the rising demand for minimally invasive diagnostics, among others, are some of the crucial factors anticipated to boost the adoption of these products globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us