Smart Shelves Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Integration & Services), By Organization Size (Large Enterprises and Small and Medium-Sized Enterprises (SMEs)), By End-Use (Hypermarkets/Supermarkets, Department Stores, Warehouses, and Others), By Application (Planogram Management, Inventory Management, Pricing Management, Content Management, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

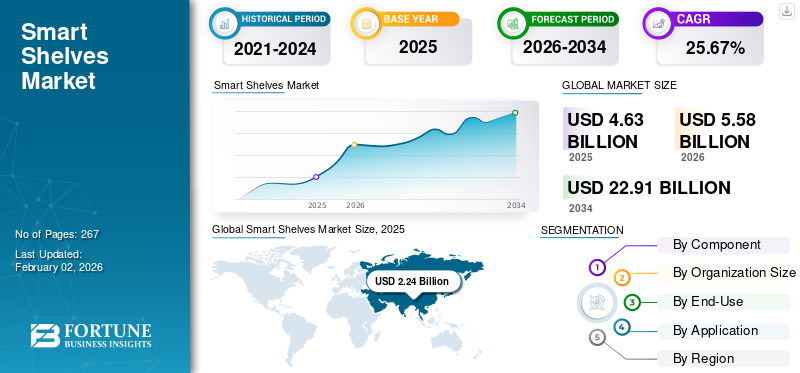

Smart Shelves Market Size and Future Outlook

The global smart shelves market size was valued at USD 4.63 billion in 2025 and is projected to grow from USD 5.58 billion in 2026 to USD 22.91 billion by 2034, exhibiting a CAGR of 25.67% during the forecast period. Asia Pacific dominated the global market with a share of 48.35% in 2025.

Smart shelves are IoT-enabled retail shelving systems equipped with RFID tags, electronic shelf labels (ESLs), weight sensors, cameras, and connectivity that provide real-time data on shelf activity. They automate functions such as optimize inventory management, planogram compliance, dynamic pricing, and digital content display. For example, Walmart partnered with E Ink and SES-imagotag to test ESL-based smart shelves for instant price changes across thousands of SKUs, while Carrefour has rolled out more than 500,000 ESLs in European stores to enhance pricing and promotion efficiency. Smart shelves are now deployed in supermarkets, hypermarkets, department stores, warehouses, and pharmacies, combining features such as automatic stock alerts, synchronized pricing, and analytics on shopper interactions to streamline store operations and improve customer experience.

The market is growing rapidly as retailer’s push for automation and real-time visibility. Retailers are increasingly adopting technology to enhance inventory management and customer experiences, enabling real-time stock visibility while delivering personalized promotions and seamless in-store interactions. The U.S. National Retail Federation (NRF) estimated that labor costs in the retail environment represent 15% of operating expenses, and smart shelves directly reduce manual stock checks and pricing updates. China’s Ministry of Commerce reported national retail sales of consumer goods surpassing approximately USD 6.8 trillion in 2024, highlighting the scale of opportunity in Asia Pacific where adoption is fastest. Meanwhile, VusionGroup (SES-imagotag) reported over 350 million ESLs deployed globally by 2023, growing at double-digit rates annually, underscoring large-scale adoption. Falling sensor/display costs and increased demand for dynamic pricing during inflationary periods have further accelerated deployments.

Major players, including Pricer AB, VusionGroup, Displaydata Ltd, Opticon Sensors Europe B.V., and Solum are some of the well-established brands in the market. Expanding beyond hardware into software & value-added services, forging retail media partnerships and scaling global rollouts with flagship contracts are the major strategies adopted by players in the market.

Download Free sample to learn more about this report.

Smart Shelves Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.63 billion

- 2026 Market Size: USD 5.58 billion

- 2034 Forecast Market Size: USD 22.91 billion

- CAGR: 25.67% from 2026–2034

- Asia Pacific dominated the smart shelves market with a 48.35% share in 2025.

- The hardware segment is expected to lead the market with a 58.06% share in 2026.

- The leading deployment/application segment is projected to account for a 64.16% share in 2026.

Asia Pacific

Asia Pacific accounted for USD 2.24 billion in 2025 and is projected to reach USD 2.71 billion in 2026, supported by rapid retail digitalization.

Europe

Europe generated USD 1.08 billion in revenue in 2025 and is expected to grow to USD 1.30 billion in 2026 due to increasing adoption of smart retail technologies.

North America

Europe generated USD 1.08 billion in revenue in 2025 and is expected to grow to USD 1.30 billion in 2026 due to increasing adoption of smart retail technologies.

U.S.

U.S. The market is projected to reach USD 1.05 billion by 2026, supported by strong investments in automated and connected retail solutions.

Japan

Japan The market is projected to reach USD 0.35 billion by 2026, fueled by growing demand for intelligent inventory management systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Demand for Real-Time Inventory Visibility and Operational Efficiency to Drive Market Growth

A major driver of smart shelves adoption is retailers’ need to gain real-time visibility into stock levels and reduce costly inefficiencies as manual stock checks consume significant labor. The National Retail Federation (NRF) notes that retail labor represents approximately 15% of operating costs in the U.S., making automation a key savings lever. During the pandemic, out-of-stocks surged underscoring the urgency for automated shelf monitoring. Leading players such as Carrefour deployed over 500,000 ESLs in Europe to automate price and stock updates, and Walmart partnered with VusionGroup (SES-imagotag) to roll out smart shelves at scale for inventory accuracy and dynamic pricing. These instances demonstrate how the need for efficiency and accuracy is directly translating into accelerated smart shelves market growth.

MARKET RESTRAINTS:

High Upfront Investment and Integration Complexity to Restrict Market Expansion

Upfront cost of adoption of smart shelves, hardware deployment, and system integration is significantly high, which limits penetration especially among small and mid-sized retailers, hampering market growth. Each store requires thousands of electronic shelf labels (ESLs) or sensors, plus installation, software integration, and connectivity infrastructure which increases the cost overall.

- For instance, VusionGroup (SES-imagotag) reported contracts worth around more than USD 10 million for single large retail chains, highlighting the capital intensity of full-scale rollouts. Smaller retailers often find it difficult to justify these investments, especially when hardware margins are thin and ROI depends on scale.

MARKET OPPORTUNITIES:

Expansion of Smart Shelves into Retail Media and In-Store Advertising to Create Lucrative Growth Opportunities

A significant growth opportunity in the market lies in their evolution from operational enablers to revenue-generating retail media platforms. Equipped with electronic shelf labels and connected digital displays, smart shelves can deliver targeted promotions, branded content, and advertising directly at the point of purchase, where a substantial share of consumer buying decisions occur. This trend is gaining momentum, as demonstrated by VusionGroup’s strategic partnership with Criteo to integrate in-store retail media on connected shelves, enabling brands to engage shoppers in real time. Similarly, Walmart has expanded its in-store media network through Walmart Connect, leveraging digital shelf assets to offer advertising opportunities to consumer goods companies. With global retail media spending projected to exceed USD 100 billion by 2026 (GroupM), the integration of advertising functions into smart shelf infrastructure presents retailers with a compelling opportunity to enhance return on investment while simultaneously diversifying revenue stream.

Smart Shelves Market Trends

Integration of AI and Computer Vision into Smart Shelves

Integration of artificial intelligence (AI) and computer vision technologies to enhance shelf intelligence beyond basic optimizing inventory tracking is the major trend in the market. Retailers are increasingly adopting AI-powered cameras and analytics to detect out-of-stock items, monitor planogram compliance, and analyze shopper behavior in real time. For example, Pricer partnered with Focal Systems to combine ESLs with AI-driven shelf vision, enabling automated stock detection and dynamic pricing. Similarly, Trax Retail, headquartered in Singapore, uses image recognition to provide retailers with accurate shelf data across thousands of stores globally. By embedding AI and vision into smart retail shelves, retailers are transforming them from passive data collectors into active decision-support tools, accelerating efficiency and driving higher ROI on store digitization investments.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

High Volume of Physical Device Deployment Drives Growth of Hardware Component

On the basis of component, the market is segmented into hardware, software, and integration services.

To know how our report can help streamline your business, Speak to Analyst

Hardware will continues to dominate the market with share of 58.06% in 2026, as it forms the essential foundation for any deployment, comprising electronic shelf labels (ESLs), RFID tags, sensors, and digital displays. These components account for the majority of upfront investment since thousands of units are required per store rollout, making hardware the largest revenue contributor. High-volume adoption by leading retailers such as Walmart and Carrefour, which have installed millions of ESLs globally, further reinforces this dominance. Although software and integration services are experiencing faster growth due to rising demand for analytics, dynamic pricing, and retail media platforms, the critical role and scale of physical infrastructure ensure hardware maintains its leading position in the market.

The software component is projected to expand at a CAGR of 23.02% over the projected years.

By Organization Size

Extensive Resources and Store Networks Boosted Large Enterprises’ Dominance

By organization size, the market is categorized into large enterprises, small and medium-sized enterprises (SMEs), and fabric.

The large enterprises segment captured the largest smart shelves market share in 2025. In 2026, the segment is anticipating to dominate with a 64.16% share. Large enterprises possess the financial capacity to absorb high upfront investments in ESLs, RFID, sensors, and integration projects, which often require millions of dollars per rollout. In addition, their extensive store networks and global operations create both the scale and the ROI justification for deploying digitally connected shelves widely.

- For instance, retailers including Walmart, Carrefour, and Tesco have already invested in large-scale ESL installations to optimize pricing, enhanced inventory management, and in-store efficiency. Their ability to form strategic partnerships with leading vendors and to integrate advanced shelves into broader digital transformation initiatives further reinforces their market leadership compared to SMEs, which face cost and resource constraints.

The small and medium-sized enterprises (SMEs) segment is expected to grow at a CAGR of 22.78% over the forecast period. Small and Medium-Sized Enterprises (SMEs) remains an attractive but much smaller segment.

By End-Use

High SKU Volume and Frequent Price Updates Fuel Adoption of Advanced Shelf Systems in Hypermarkets & Supermarkets

Based on end-use, the market is segmented into hypermarkets/supermarkets, department stores, warehouses, and others.

Hypermarkets and supermarkets will account for the largest market share of 49.28% in 2026 since they manage tens of thousands of SKUs across large store footprints, requiring constant price updates and real-time inventory visibility. Advanced shelves with electronic shelf labels (ESLs), RFID, and sensors help automate these labor-intensive tasks, reducing errors and saving operating costs. Frequent promotions, seasonal discounts, and competitive pricing strategies in grocery retail further drive adoption, as dynamic pricing and instant updates are critical for customer retention. Large chains such as Carrefour and Walmart have deployed millions of ESLs across stores, showing how the scale and complexity of hypermarket operations directly support their leading share in the industry. Also, supermarkets are leveraging dynamic pricing to automatically adjust product prices in real time based on demand, competition, and inventory levels.

The warehouses end-use segment is projected to grow the fastest due to the surging need for automation in inventory tracking and fulfillment operations. The rapid expansion of e-commerce and omnichannel retailing is pushing warehouses to adopt smart and intelligent shelves for real-time stock accuracy and faster order processing. These shelves also support micro-fulfillment centers and dark stores, which are increasingly used by retailers to meet same-day delivery demand. This combination of rising volumes, speed requirements, and digital transformation initiatives supports warehouses’ position as the fastest-growing end-user segment.

By Application

High Demand for Real-Time Stock Accuracy Drives Inventory Management’s Segmental Growth

Based on application, the market is segmented into planogram management, inventory management, pricing management, content management, and others.

In 2024, the global market was dominated by inventory management since retailers’ primary need is accurate, real-time visibility of stock levels to avoid out-of-stocks, shrinkage, and overstocking. Electronic shelf systems are equipped with RFID tags, weight sensors, and ESLs automate manual stock checks, which are time-consuming and labor-intensive. With studies showing that stockouts cost U.S. retailers over USD 80 billion annually, retailers prioritize inventory management applications to improve efficiency and reduce losses. This fundamental operational requirement makes inventory management the leading application segment. Furthermore, the segment is expected to hold a 40.32% share in 2026.

In addition, content management is the fastest-growing channel and is projected to grow at a CAGR of 23.63% during the study period.

Smart Shelves Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

ASIA PACIFIC

Global Smart Shelves Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 2.24 billion in 2025, representing 48.35% of the global industry, and is expected to reach USD 2.71 billion in 2026. Combination of rapid retail modernization, large consumer bases, and strong digital adoption across key markets such as China, Japan, India, and South Korea. The region’s dominance is supported by the sheer scale of organized retail, with China’s retail sales of consumer goods surpassing USD 6.8 trillion in 2024, providing vast deployment opportunities. Retailers in the region are also early adopters of IoT and ESLs, driven by government-led digital transformation initiatives and high demand for contactless, automated shopping experiences. In 2026, the China market is estimated to reach USD 1.33 billion. The Japan market is projected to reach USD 0.35 billion by 2026, the India market is projected to reach USD 0.5 billion by 2026

EUROPE & NORTH AMERICA

Other regions, such as the Europe and North America market, are anticipated to witness steady growth in the coming years. During the forecast period, North America maintained a strong presence in the global market, reaching USD 1.04 billion in 2025, accounting for 22.50% share, and is expected to reach USD 1.25 billion in 2026. The region’s growth is fueled by early technology adoption and strong retail digitization investments led by major chains such as Walmart, Kroger, and Target. Retailers face high labor costs in the U.S., labor accounts for around 15% of operating expenses, making automation through digital shelves a priority to reduce manual tasks such as price updates and stock checks. In 2025, Europe generated USD 1.08 billion, contributing 23.44% to global market revenue, and is projected to grow to USD 1.3 billion in 2026. In the region, Germany and the U.K. both are estimated to reach USD 0.28 and 0.24 billion each in 2026. Early adoption of electronic shelf labels (ESLs), with leading retailers such as Carrefour, Tesco, and Metro already rolling out large-scale deployments drives growth of the European market. The push for operational efficiency and sustainability, supported by European Union regulations on digital pricing and eco-friendly retail practices, further accelerates adoption. Additionally, Europe hosts major smart shelf innovators including VusionGroup (France) and Pricer (Sweden), whose strong local presence fosters faster technology penetration across the region. The U.S. market is projected to reach USD 1.05 billion by 2026.

LATIN AMERICA & MIDDLE EAST & AFRICA

Over the forecast period, Latin America and Middle East and Africa regions would witness a moderate growth in this marketspace. The Latin America market in 2025 is set to record USD 0.14 billion as its valuation. Growing modern retail expansion and adoption of automation in supermarkets drive South America’s automated shelves market growth. In 2025, Middle East & Africa represented USD 0.12 billion, accounting for 2.63% of the worldwide market, and is projected to grow to USD 0.15 billion in 2026.

South America

In 2025, South America held 3.08% of the global market, reaching a valuation of USD 0.14 billion, and is projected to grow to USD 0.17 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Intensifying Competition Drives Innovation and Strategic Partnerships in Market

Major players include Sonoco ThermoSafe, B Medical Systems, va-Q-tec AG, Softbox Systems, Igloo Products, and YETI. These firms compete by continuously innovating insulation materials and cooling technologies (e.g. vacuum insulation, advanced foams), diversifying product portfolios across consumer, pharmaceutical, and food-logistics segments, forming strategic partnerships and acquisitions to expand geographically, and focusing on sustainability and regulatory compliance (especially in pharma cold chain). For instance, Sonoco ThermoSafe (U.S.) markets temperature-controlled packaging solutions for pharma and life sciences, emphasizing innovative insulation design, container rental models, and sustainability initiatives in their service offerings

Apart from this, few other prominent players in the market include CSafe, Envirotainer, Softbox Systems, Igloo Products, and YETI Holdings.

LIST OF KEY SMART SHELVES COMPANIES PROFILED:

- Sonoco ThermoSafe (U.S.)

- va-Q-tec AG (Germany)

- Igloo Products Corp. (U.S.)

- YETI Holdings, LLC (U.S.)

- Pelican Products, Inc. (U.S.)

- B Medical Systems S.à r.l. (Luxomberg)

- Softbox Systems Ltd. (U.K.)

- Sofrigam Group (France)

- Coldchain Technologies, Inc. (U.S.)

- Blowkings (India)

KEY INDUSTRY DEVELOPMENTS:

- February 2025: Captana launched its ShelfWatch solution, which uses machine learning and sensor-camera fusion to automate real-time shelf monitoring. The system identifies product vacancies and misplacements, visualizes shelf status against planograms (“Realogram”), and guides employees via geolocation to stock items all without requiring manual label scanning.

- January 2024: SES-imagotag officially rebranded as VusionGroup, a name change ratified by shareholders in its June 2023 AGM, signaling its transformation from an ESL-centric firm into a diversified solutions group. The parent retains SES-imagotag as its core ESL / digital shelf label brand, while also embracing a wider portfolio including VusionCloud, Captana (AI/vision), Memory (data analytics), Engage (retail media), and PDidigital (industrial & logistics).

- February 2023: Captana, a shelf analytics subsidiary of VusionGroup, finalized an agreement to acquire Belive.ai, a company specializing in computer vision and AI-driven image analysis. This acquisition is intended to enhance Captana’s ability to deliver real-time shelf intelligence, such as vacancy detection and product placement insights by embedding Belive.ai’s algorithms into its shelf-monitoring platform.

- January 2023: SES-imagotag (now operating under VusionGroup) entered exclusive negotiations to acquire In The Memory, a French startup specializing in retail data analytics and decision-making platforms. This acquisition is aimed at strengthening SES-imagotag’s data and analytics capabilities by integrating Memory’s tools into its VUSION platform, thereby enabling more automated, cross-channel decision support for retailers and brand managers.

REPORT COVERAGE

The global smart shelves market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses porters five forces analysis, a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 25.67% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component

By Organization Size

By End-Use

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.58 billion in 2026 and is projected to reach USD 22.91 billion by 2034.

In 2025, the market value stood at USD 2.24 billion.

The market is expected to exhibit a CAGR of 25.67% during the forecast period of 2026-2034.

The hardware segment led the market by component.

The key factors driving the market are rising demand for real-time inventory visibility, operational efficiency and combination of rapid retail modernization, large consumer bases, and strong digital adoption across key regions.

Sonoco ThermoSafe, B Medical Systems, va-Q-tec AG, Softbox Systems, Igloo Products, and YETI are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Evolution from operational enablers to revenue-generating retail media platforms and equipped with electronic shelf labels and connected digital displays expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 267

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us