Software-Defined Satellite Market Size, Share & Industry Analysis, By Payload Architecture (Transparent/Bent-Pipe, Regenerative/On-Board Processed, & Hybrid Transparent-Regenerative), By Application (Broadband Connectivity, Mobility Connectivity, Government & Defense, Enterprise/Backhaul Connectivity & Broadcast), By End User (Commercial Satellite Operators, Government/Civil Agencies, Military, Network Service, Enterprise/Mobility Service), By Orbit, By Throughput Class (Conventional, High, Very High, & Multi-Terabit/Extreme-Capacity), and Regional Forecast, 2026-2034

Software-Defined Satellite Market Size and Future Outlook

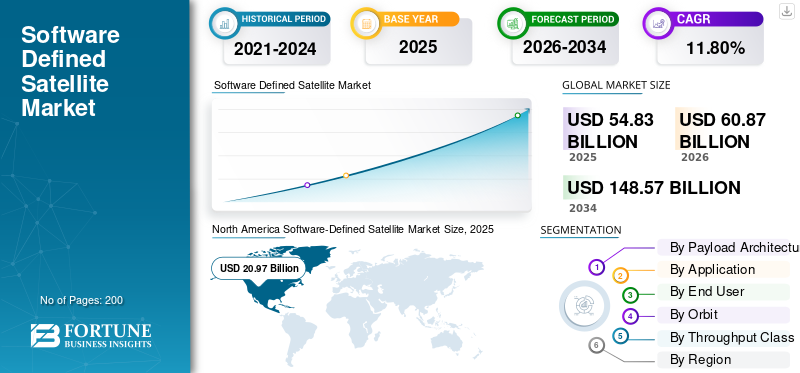

The global software-defined satellite market size was valued at USD 54.83 billion in 2025. The market is projected to grow from USD 60.87 billion in 2026 to USD 148.57 billion by 2034, exhibiting a CAGR of 11.80% during the forecast period. North America dominated the global market with a market share of 38.25% in 2025.

Software-defined satellites (SDS) are advanced space platforms that utilize programmable payloads, including Field Programmable Gate Array (FPGAs) and Digital Signal Processors (DSPs), to allow remote reconfiguration of communication frequency, power allocation, and coverage beams after launch. This technology incorporates versatile hardware capable of supporting multiple missions such as broadband, defense, and Earth observation through software updates rather than static, hardware locked functions. These systems are essential for agile connectivity, IoT, and disaster response where operational flexibility is critical. Adoption is primarily driven by the need for mission adaptability, reduced lifecycle costs, and seamless integration with terrestrial 5G and cloud networks.

Key players include Airbus, which integrates flexible payloads into its OneSat platforms for adaptable orbital service. Moreover, Thales Alenia Space is known for developing highly reconfigurable digital processors for space applications. Northrop Grumman focuses on advanced software-defined payloads for military and commercial communication, among other players.

Download Free sample to learn more about this report.

Software-Defined Satellite Market Key Takeways

- 2025 Market Size: USD 54.83 billion

- 2026 Market Size: USD 60.87 billion

- 2034 Forecast Market Size: USD 148.57 billion

- CAGR: 11.80% from 2026–2034

- North America dominated the software-defined satellite market with a 38.25% share in 2025.

- The hybrid transparent-regenerative segment is expected to account for the largest market share in 2026.

- The government & defense communications segment dominated the global market in 2025.

North America

North America maintained its market leadership, with the regional market estimated at USD 20.97 billion in 2026.

Europe

Europe is projected to grow at a 11.84% CAGR during the forecast period, reaching USD 14.10 billion by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 13.52 billion in 2026 and remain the fastest-growing regional market.

U.S.

U.S. The U.S. software-defined satellite market is estimated to reach USD 14.54 billion in 2026.

Japan

Japan The Japan software-defined satellite market is estimated at USD 2.46 billion in 2026.

Read More

SOFTWARE-DEFINED SATELLITE MARKET TRENDS

Integration of Artificial Intelligence into Software-defined Satellites is a Market Trend

The integration of artificial intelligence into software-defined satellites is transforming space satellite operations by enabling autonomous, real time decision-making. AI-driven onboard processing, using machine learning models for adaptive beamforming and dynamic resource allocation, optimizes signal quality and spectral efficiency, overcoming the limitations of rigid, legacy systems. Furthermore, research demonstrates that deep reinforcement learning allows satellites to manage flight control and attitude adjustments independently.

- In April 2026, the Defense Research and Development Organization (DRDO) introduced "Pragya," an AI-enabled satellite imaging system designed to process vast amounts of data into actionable security intelligence for Indian agencies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Multi-Mission Constellations is Anticipated to Drive Market Growth

The shift toward multi-mission constellations is fundamentally driven by the need for resilient, high-throughput, and adaptable global connectivity. Governments are deploying these tiered architectures to secure critical navigation, missile warning, and communication services, ensuring mission continuity even during system failure. Commercially, the proliferation of LEO networks meets surging demands for low-latency broadband and IoT coverage in underserved regions. Reduced launch costs and advancements in satellite miniaturization enable the mass deployment of these systems, further influencing the software-defined satellite market growth.

- In July 2025, the USSF awarded a USD 2.8 billion contract to Boeing for the Evolved Strategic Satellite Communications (ESS) program, which utilizes agile, software-defined acquisition pathways to modernize nuclear command and control capabilities.

MARKET RESTRAINTS

Limited Onboard Buffer Capacity is a Market Restraint

Limited onboard buffer capacity acts as a critical bottleneck for modern software-defined satellites, particularly in Low-Earth-Orbit (LEO) constellations. As these satellites must process and route bursty data traffic across dynamic inter-satellite links, small buffers frequently lead to queue overflows and packet loss, disrupting deterministic data transmission. This storage limitation also forces satellites to prioritize mission-critical data over general traffic, as insufficient memory prevents the accumulation of large high-resolution datasets before downlink opportunities occur.

MARKET OPPORTUNITIES

Integration of 5G and 6G Creates New Market Opportunities

The integration of 5G and 6G with satellite constellations, termed Non-Terrestrial Networks (NTN), creates significant market opportunities by establishing a unified, global communication fabric. This shift allows satellites to transition from simple backhaul providers to active nodes, enabling direct-to-device connectivity that extends coverage to previously unreachable maritime, rural, and mountainous regions. By leveraging LEO architectures and 3GPP standards, operators can offer low-latency, resilient services that seamlessly bridge gaps in terrestrial cellular infrastructure.

MARKET CHALLENGES

High Initial Research And Development Costs Present a Major Market Challenge

High initial Research And Development (R&D) costs represent a significant market challenge for SDS adoption. Developing these advanced platforms requires substantial financial investment in designing complex, programmable hardware and robust software-centric architectures that can withstand harsh space environments. Furthermore, the lack of industry-wide standardization for these systems increases development cycles and prevents interoperability between new SDS platforms and legacy ground infrastructure. While these systems aim to lower long-term operational costs through remote reconfiguration, the steep upfront capital requirements continue to pose high barriers to entry for smaller market participants.

Segmentation Analysis

By Payload Architecture

Payload Flexibility to Boost Hybrid Transparent-Regenerative Segment Growth

Based on the payload architecture, the market is segmented into transparent/bent-pipe, regenerative/on-board processed, and hybrid transparent-regenerative.

The hybrid transparent-regenerative segment is anticipated to account for the largest software-defined satellite market share. The segmental growth in the market is owing to hybrid transparent-regenerative payloads, as they provide the crucial agility needed to switch between traditional bent-pipe relay and sophisticated onboard digital processing for optimized spectral efficiency.

The regenerative/on-board processed segment is anticipated to rise with a high CAGR of 12.37% over the forecast period.

By Application

Enhanced Security Demands to Boost Government & Defense Communications Segment Growth

Based on application, the market is segmented into broadband connectivity, mobility connectivity, government & defense communications, enterprise/backhaul connectivity, and broadcast/media/others.

In 2025, the government & defense communications segment dominated the global market. These missions require highly secure, anti-jam, and reconfigurable links to maintain the resilient, real-time tactical situational awareness and communication reliability demanded by modern military operations.

The government & defense communications segment is projected to grow at a high CAGR of 12.36% over the forecast period.

By End User

Scalability Requirements to Boost Commercial Satellite Operators Segment Growth

Based on the end user, the market is segmented into commercial satellite operators, government/civil agencies, defense/military, telecom/network service providers, enterprise/mobility service providers, and others.

The commercial satellite operators segment is anticipated to witness a dominating market share over the forecast period. These systems provide the rapid, cost-effective service scalability and remote reconfiguration capabilities necessary to align orbital assets with shifting global terrestrial market demands.

The defense/military segment is projected to grow at a high CAGR of 12.52% over the forecast period.

By Orbit

Low-Latency Connectivity to Boost LEO Segment Growth

Based on orbit, the market is segmented into GEO, MEO, LEO, and HEO/specialized orbit.

The Low-Earth-Orbit (LEO) segment dominated the market share. The segmental growth is owing to LEO’s proximity to provide the essential low-latency and high-bandwidth connectivity needed for real-time data streaming, massive IoT coverage, and agile, globally distributed network architectures.

In addition, the Geostationary Orbit (GEO) segment is projected to grow at a high CAGR of 11.54% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Throughput Class

High-Capacity Bandwidth to Boost Very High Throughput Satellites (VHTS) Segment Growth

Based on throughput class, the market is segmented into conventional throughput software-defined satellites, High-Throughput Satellites (HTS), Very High Throughput Satellites (VHTS), and multi-terabit / extreme-capacity software-defined satellites.

The Very High Throughput Satellites (VHTS) segment dominated the market share. The segmental growth is owing to these platforms’ ability to deliver the massive, flexible data capacity required to support the surging demand for high-definition enterprise services and seamless, multi-gigabit broadband integration.

In addition, the multi-terabit / extreme-capacity software-defined satellites segment is projected to grow at a high CAGR of 12.25% during the forecast period.

Software-Defined Satellite Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Software-Defined Satellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 18.92 billion, and also maintained the leading share in 2025, with USD 20.97 billion. North America dominates the SDS market, fueled by high demand for agile architectures and robust ecosystems. Industry leaders and agencies such as NASA and the DoD drive innovation through strategic R&D investments.

U.S. Software Defined Satellite Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 14.54 billion in 2026. Further, accounting for roughly 12.04% of CAGR during the forecast period. The U.S. is the primary hub, with massive federal backing from the DoD and Space Development Agency (SDA). These agencies fund large-scale, dual-use satellite constellations.

Europe

Europe is projected to record a steady growth rate of 11.84% during the forecast period, the second highest among all regions, and reach a valuation of USD 14.10 billion by 2026. Europe prioritizes strategic autonomy via the IRIS² constellation initiative. The European Space Agency (ESA) supports this through the "Space Systems for Safety and Security (4S)" Programme, funding R&D for secure, reconfigurable connectivity.

U.K. Software-Defined Satellite Market

The U.K. market in 2026 is estimated at around USD 4.48 billion, representing roughly 12.31% of CAGR during the forecast period. The U.K. fosters growth through the National Space Innovation Programme and C-LEO Programme. Furthermore, government backing supports collaborative research into 5G/6G satellite-terrestrial integration.

Germany Software-Defined Satellite Market

Germany’s market is projected to reach approximately USD 3.91 billion in 2026. Germany’s growth is driven by the need for flexible, high-bandwidth connectivity, significant investments in defense and commercial space.

Asia Pacific

The Asia Pacific region is estimated to reach USD 13.52 billion in 2026, securing the third-largest position in the market, while also being the fastest-growing region during the forecast period. The region’s growth is driven by the need to bridge connectivity gaps in remote regions. However, rapid expansion in satellite communication and military modernization projects fuels SDS adoption.

Japan Software-Defined Satellite Market

The Japan market in 2026 is estimated at around USD 2.46 billion, accounting for roughly 12.32% of CAGR during the forecast period. Japan emphasizes miniaturization and dual-use, autonomous constellations through strong public-private partnerships. R&D initiatives focus on advanced remote sensing and real-time mission management software.

China Software-Defined Satellite Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.47 billion. China’s state-directed model emphasizes massive LEO constellation deployments and dual-use AI-integrated satellite systems.

India Software-Defined Satellite Market

The Indian market size in 2026 is estimated at around USD 3.62 billion. India has accelerated its space sector through initiatives such as Project "Pragyashakti," focusing on AI-driven imaging and secure communication. Increased government funding for ISRO and defense research supports indigenous software-defined hardware development.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America regions. Growth in these regions is primarily driven by international collaborations and the adoption of LEO networks for basic connectivity. Investment often focuses on building infrastructure for environmental monitoring and secure government links. The Middle East & Africa and Latin America market is set to reach a valuation of USD 6.05 billion and USD 3.95 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and AI-driven Connectivity Enhancements Fuel Market Expansion

The software-defined satellite market is moderately consolidated, with specialized aerospace technology leaders such as Airbus, Thales Alenia Space, Northrop Grumman, Maxar Technologies, and Boeing. These companies are holding significant shares through complex, reprogrammable payload architectures and high-performance, modular satellite bus designs tailored for diverse government and commercial missions.

These players focus on advancing digital signal processing, programmable FPGA integration, and AI-driven autonomous resource management to address evolving demands for mission agility and seamless terrestrial network connectivity. Strategic partnerships are accelerating market expansion as Boeing collaborates with government agencies on modular, high-capacity strategic communication constellations, while Thales Alenia Space integrates reconfigurable processors into multi-mission European infrastructure projects. Further, Maxar Technologies provides high-power, reprogrammable bus designs for rapidly scaling commercial broadband networks.

LIST OF KEY SOFTWARE-DEFINED SATELLITE COMPANIES PROFILED

- Airbus (Netherlands)

- Boeing (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- Thales Group (France)

- Maxar Technologies (U.S.)

- L3Harris Technologies (U.S.)

- NEC Corporation (Japan)

- BAE Systems (U.K.)

- SWISSto12 (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The ninth and tenth Boeing-built O3b mPOWER satellites have entered commercial operation, improving global connectivity with their sophisticated, software-defined capabilities, according to global space solutions provider SES.

- February 2026: Airbus Defense and Space has given Kratos a contract to supply a ground segment for its client Space Communication Technologies (SCT), according to Kratos Defense & Security Solutions, Inc. OmanSat-1 software-defined satellite will be supported by SPC.

- November 2025: Airbus Defence and Space has been given a contract by Space Communication Technologies (SCT) for OmanSat-1, a cutting-edge, completely reconfigurable, high throughput OneSat communications satellite and related system.

- September 2024: Thaicom Public Company Limited (Thaicom) has granted Kratos Defense & Security Solutions, Inc. a contract for its end-to-end ground system. Thaicom will be able to optimize the sophisticated features of its new software-defined satellite, THAICOM-10, by configuring the satellite and ground system in tandem to deliver services to clients on demand.

- May 2024: A contract to construct JSAT-31, a new generation of software-defined satellite based on Thales Alenia Space's Space INSPIRE (INstant SPace In-orbit REconfiguration) platform, was announced by SKY Perfect JSAT and Thales Alenia Space, a joint venture between Thales (67%) and Leonardo (33%).

REPORT COVERAGE

The global industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, porter’s five forces analysis, company profiles, and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The global software-defined satellite market report include a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.80% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Payload Architecture,Application, End User, Orbit, Throughput Class, and Region |

| By Payload Architecture |

|

| By Application |

|

| By End User |

|

| By Orbit |

|

| By Throughput Class |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 54.83 billion in 2025 and is projected to reach USD 148.57 billion by 2034.

In 2025, the market value stood at USD 20.97 billion.

The market is expected to exhibit a CAGR of 11.80% during the forecast period.

By payload architecture, the hybrid transparent-regenerative segment is expected to dominate the market.

An increasing demand for multi-mission constellations is anticipated to drive market growth.

Airbus, Thales Alenia Space, Northrop Grumman, Maxar Technologies, and Boeing are a few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us