Space based C4ISR Market Size, Share & Industry Analysis, By Capability (Command & Control (C2) Systems, Communications (SATCOM), and Intelligence, Surveillance & Reconnaissance (ISR)), By Orbit (LEO, MEO, and GEO), By Platform (Small Satellite, Medium Satellite, and Large Satellite), By End User (Defense Forces & Intelligence Agencies and Space Agencies), and Regional Forecast, 2026-2034

Space Based C4ISR Market Size and Future Outlook

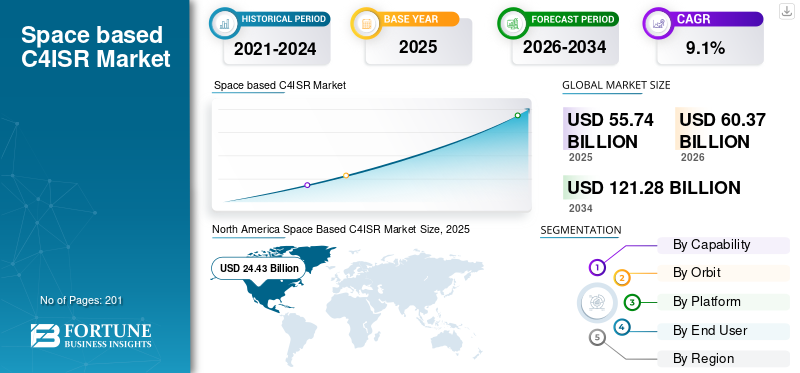

The global space based C4ISR market size was valued at USD 55.74 billion in 2025. The market is projected to grow from USD 60.37 billion in 2026 to USD 121.28 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period. North America dominated the space based C4ISR market with a market share of 43.82% in 2025.

The global market is experiencing robust growth, fueled by increasing space domain awareness needs and rising investments in satellite constellations for resilient communications. The swift deployment of unmanned orbital systems across military forces, intelligence, and national security operations is another factor propelling industry expansion.

- For instance, in December 2025, The Space Development Agency awarded Lockheed Martin a contract worth over USD 1 billion for 18 Tranche 3 Tracking Layer satellites, enhancing the Proliferated Warfighter Space Architecture (PWSA) with advanced missile warning, tracking, and fire-control capabilities against hypersonic threats from low Earth orbit.

Prominent players such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, L3Harris Technologies, and Thales Group are focused on innovations such as multi-orbit sensor fusion for contested space environments and advanced sensors for missile tracking and surveillance. They are also integrating AI for real time intelligence and secure communication technologies.

Download Free sample to learn more about this report.

SPACE BASED C4ISR MARKET TRENDS

Shift toward Proliferated LEO Constellations and AI-Driven Data Fusion is a Prominent Trend

The shift toward proliferated low-Earth orbit (LEO) constellations and AI-driven data fusion is accelerating the product demand for military, intelligence, and national security operations. The market expansion is driven by the rising demand for real time actionable intelligence, resilient global coverage, low-latency communications, and persistent surveillance in contested orbital environments. An increase in space domain awareness propel market growth as nations deploy mega-constellations for real-time threat, and threat assessment, countering satellite jamming and anti-satellite weapons. Moreover, military organizations emphasize resilient architectures for enhancing accuracy during orbital congestion, countering cyber/electronic warfare threats, and enabling hypersonic tracking, space traffic management.

- For instance, in September 2025, Israel successfully launched its latest military surveillance satellite, Ofek 19, into Earth orbit from a classified site. Built by Israel Aerospace Industries, the highly advanced synthetic aperture radar (SAR) satellite offers enhanced all-weather imaging and intelligence-gathering capabilities for monitoring regional threats.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Escalation of Space Domain Threats and Investment in Resilient Satellite Architectures to Drive Market Growth

A primary driver for the market is the escalation of orbital threats such as anti-satellite weapons, cyber attacks, and orbital congestion. The market is growing significantly due to accelerated investments in resilient, proliferated satellite architectures across military, intelligence, and national security sectors. Such threat proliferation propels the demand for proliferated LEO constellations with AI-driven orbit determination, autonomous evasion algorithms, and optical inter-satellite links for denial-resistant operations. Space traffic management systems integrate with C4ISR platforms to enable real-time conjunction assessments in ground stations. As militaries seek contested-space dominance, deploying sensor swarms and debris mitigation tools, the demand for space based C4ISR solutions increases, driving the market growth.

MARKET RESTRAINTS

High Costs of Satellite Development to Limit Market Expansion

High development and launch costs for space-based C4ISR systems pose a significant restraint, limiting adoption especially among smaller nations and emerging space powers. Building proliferated LEO constellations requires billions in upfront investment for satellite buses, radiation-hardened sensors, and dedicated launches, deterring budget-constrained militaries. Export controls and ITAR restrictions further complicate international collaborations, slowing technology transfer to allies, which is anticipated to slow market penetration and hamper the space based C4ISR market growth.

MARKET OPPORTUNITIES

Development of Multi-Orbit Resilient C4ISR Architectures to Present Growth Opportunities

The shift toward multi-orbit resilient space-based C4ISR architectures is emerging as one of the most commercially significant opportunities in the defense and space domain. Modern military operations can no longer rely on single-orbit or single-provider satellite systems, as these are increasingly vulnerable to jamming, cyber intrusion, and kinetic counterspace threats. As a result, defense agencies are prioritizing architectures that integrate LEO, MEO, and GEO assets into a unified operational framework. By combining ISR satellites, secure tactical communications, cost effective PNT solutions, and cloud-enabled ground segments, operators can ensure redundancy, faster revisit rates, and assured data delivery, which is expected to present significant opportunities for market growth.

MARKET CHALLENGES

Cybersecurity Vulnerabilities Acts a Challenge for the Market

Cybersecurity vulnerabilities in space-based C4ISR networks present a critical challenge, as satellites face sophisticated hacking, spoofing, and supply-chain attacks from state actors. Ground stations and inter-satellite links remain prime targets, risking data compromise in contested orbits. Quantum computing threats loom over legacy encryption, demanding costly upgrades to post-quantum cryptography. Orbital congestion amplifies risks, with mega-constellations creating larger attack surfaces for jamming or kinetic strikes. These factors are together expected to create challenges for the growth of the market.

Segmentation Analysis

By Capability

Rising Product Demand to Support Faster Decisions to Propel ISR Segment Growth

Based on capability, the market is divided into Command & Control (C2) Systems, Communications (SATCOM), and Intelligence, Surveillance & Reconnaissance (ISR).

The Intelligence, Surveillance & Reconnaissance (ISR) segment is anticipated to account for the largest market share. ISR segment is expanding as modern operations require persistent, wide-area space based C4ISR to support faster decisions. The segment growth is reinforced by the demand for multi-phenomenology sensing (EO/IR, SAR, RF) to mitigate weather, concealment, and daytime limitations.

The command & control (C2) systems segment is anticipated to expand at a steady CAGR of 7.6% over the analysis period.

To know how our report can help streamline your business, Speak to Analyst

By Orbit

GEO Segment to Lead Owing to Continuous Coverage over Extensive Areas

By orbit, the market is segmented into LEO, MEO, and GEO.

The GEO segment is anticipated to account for the largest market share. The segment is expanding as it provides continuous coverage over wide areas, which is highly valued for strategic communications and theater-wide command connectivity. Its altitude enables very large footprints, reducing the number of satellites needed for sustained regional coverage compared to lower orbits.

The LEO segment is projected to surge at a steady CAGR of 10.7% over the forecast period.

By Platform

Large Satellite Segment Dominates with Rising Demand in Missions Requiring Larger Apertures and High Payload Power

Based on platform, the market is segmented into small satellite, medium satellite, and large satellite.

The large satellite segment accounts for the largest space based C4ISR market share for missions requiring high payload power, larger apertures, and higher throughput to achieve superior sensing and protected communications performance. Large satellite platforms can host more capable payload suites and provide better thermal and power margins for advanced onboard processing and secure networking. Large satellites are often selected for strategic coverage, long service life, and assured performance under stringent security and reliability requirements.

The small satellite segment is expected to grow at the fastest CAGR of 10.5% over the forecast period.

By End User

Secure Access Demand to C4ISR to Push Defense Forces & Intelligence Agencies Segment Growth

Based on end user, the market is segmented into defense forces & intelligence agencies and space agencies.

The defense forces & intelligence agencies segment held the largest share in market in 2025. This segment is growing as defense and intelligence users have the strongest requirement for secure, assured access to C4ISR in contested environments. Investment is driven by modernization toward joint and multi-domain operations, where space-based data must be integrated rapidly into command-and-control workflows.

The space agencies segment is projected to emerge as the fastest-growing segment, expanding at a CAGR of 10.0% over the forecast period.

Space Based C4ISR Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

North America

North America Space Based C4ISR Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025 with a valuation of USD 24.43 billion and is anticipated to reach USD 26.36 billion in 2026. The market expansion is driven by sustained defense space budgets and a clear shift toward resilient, proliferated architectures that keep C4ISR functioning under jamming, cyber, and counterspace threats.

U.S. Space Based C4ISR Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market value touched around USD 22.56 billion in 2025. High defense allocations fuel upgrades in infrared sensor fusion, AI-driven orbit analytics, and PWSA Tranche 2 satellites, enhancing real-time tracking in contested orbits. The U.S. military advances space superiority by adopting denial-resistant architectures against ASAT threats and cyber vulnerabilities.

- For instance, in August 2024, Space Development Agency of U.S. awarded USD 424 million to build and operate 20 Tranche 2 Transport Layer-Gamma satellites, expanding advanced tactical SATCOM/data transport for C4ISR missions.

Europe

The Europe market is projected to record a growth rate of 8.3% during 2026 to 2034. The regional market growth is driven by priorities around strategic autonomy, secure connectivity, and alliance-grade interoperability. Governments are investing in sovereign Earth observation, protected SATCOM, and ground infrastructure that can support coalition operations with consistent security standards. The threat environment has increased urgency for persistent ISR, rapid dissemination, and resilient communications driving the market growth in the region.

U.K. Space Based C4ISR Market

The U.K. market touched a value of around USD 2.46 billion in 2025, representing roughly 4.4% of global revenues.

Germany Space Based C4ISR Market

The Germany market reached approximately USD 1.79 billion in 2025, equivalent to around 3.2% of global sales.

Asia Pacific

The Asia Pacific market reached a value of USD 14.76 billion in 2025 and secured the position of the second-largest region in the market. The regional market expansion is powered by maritime domain awareness requirements, contested borders, and dispersed operating theaters that make space-based ISR and SATCOM operationally essential. Regional militaries are pursuing networked, multi-domain force structures, which increase the demand for real-time ISR cueing, data relay, and assured connectivity. Several countries in the region are investing in constellations and hosted payload approaches to improve revisit and reduce vulnerability.

Japan Space Based C4ISR Market

The Japan market reached a value of around USD 1.93 billion in 2025, accounting for roughly 3.5% of global revenues.

China Space Based C4ISR Market

The China market is projected to be one of the largest worldwide, with 2025 revenues hitting around USD 6.70 billion, representing roughly 12.0% of global sales.

India Space Based C4ISR Market

In 2025, the India market reached a valuation of around USD 2.34 billion, accounting for roughly 4.2% of global revenues.

Latin America and the Middle East & Africa

Latin America exhibits steady market growth during 2026-2034, supported by defense modernization efforts and peacekeeping operations across Brazil, Colombia, and Chile. The Latin America market reached a valuation of USD 3.17 billion in 2025. The regional market growth is more selective and program-led, shaped by budget realities and the need to address border security, maritime monitoring, and disaster response with dual-use benefits. The Middle East & Africa market growth is driven by sovereign ISR ambitions, persistent border and maritime security needs, and the requirement for reliable communications across large areas with uneven terrestrial infrastructure.

For instance, in September 2025, Israel Ministry of Defense / IAI successfully launched Ofek 19, enhancing Israel’s space-based reconnaissance / intelligence collection coverage.

Saudi Arabia Space Based C4ISR Market

The Saudi Arabia market reached a value of around USD 0.60 billion in 2025, representing roughly 1.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players’ Focus on AI-fused Sensor Networks and Resilient Platforms to Solidify their Standing

The global space-based C4ISR market is consolidated, led by prominent players such as Lockheed Martin, Northrop Grumman, BAE Systems, L3Harris Technologies, RTX Corporation, and Boeing, which command significant shares through innovations in proliferated satellite constellations and AI-fused orbital sensor networks. These firms boost market expansion with strategic contracts from space commands and international partnerships, emphasizing development of resilient SATCOM relays, real-time space domain awareness (SDA) analytics, and software-defined payloads for proliferated low-Earth orbit (LEO) architectures.

- For instance, in March 2025, Airbus' CSO-3 Earth observation satellite completed France's three-satellite CSO fleet under the MUSIS program. It delivers extremely high-resolution optical intelligence for French Armed Forces surveillance, reconnaissance, and national security through agile, secure space-based imaging.

Other prominent players comprise Planet Labs PBC, Maxar Technologies, General Dynamics Mission Systems, Israel Aerospace Industries, and Thales Alenia Space. These are focusing on scalable high-resolution imaging swarms, edge AI for GEOINT processing, and hardened ground segments for counter-space operations and hypersonic tracking.

LIST OF KEY SPACE BASED C4ISR COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- L3Harris Technologies (U.S.)

- Raytheon (RTX) (U.S.)

- Airbus (France)

- BAE Systems (U.S.)

- Thales Alenia Space (France)

- Leonardo (Italy)

- Maxar Technologies (U.S.)

- Planet Labs (U.S.)

- BlackSky (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Space Development Agency (SDA) awarded USD 3.5 billion in contracts for Tranche 3 Tracking Layer to Lockheed Martin, Northrop Grumman, Rocket Lab, and L3Harris to build 72 missile-warning / tracking satellites supporting resilient space-based sensing.

- December 2025: Rheinmetall and ICEYE secured a Bundeswehr order to deliver exclusive access to a SAR satellite constellation, expanding Germany’s sovereign all-weather space-based reconnaissance capability.

- December 2025: HawkEye 360 received additional NRO funding/extension to expand space-based RF intelligence strengthening commercial RF contributions to national security ISR.

- November 2025: Planet Labs signed a renewal contract with an international defense & intelligence customer for assured tasking and high resolution imagery to support persistent ISR monitoring.

- October 2025: SpaceX launched SDA’s Tranche 1 data transport mission (Transport Layer) to LEO, expanding resilient, low-latency connectivity that moves ISR/C2 data across the battlespace.

- September 2025: SDA completed the first Tranche 1 Transport Layer launch, placing 21 data-transport satellites on orbit for the Proliferated Warfighter Space Architecture (PWSA).

REPORT COVERAGE

The global space based C4ISR market analysis provides an in-depth study of market size & forecast by all the segments included in the report. It includes details on the market dynamics, market trends, and regional analysis expected to drive the market over the forecast period. The market report includes Porter’s five forces analysis which illustrates the potency of buyers and suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers, and acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Capability, By Orbit, By Platform, By End User, and By Region |

| By Capability |

|

| By Orbit |

|

| By Platform |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 55.74 billion in 2025 and is projected to reach USD 121.28 billion by 2034.

In 2025, the North America market value stood at USD 24.43 billion.

The market is expected to exhibit a CAGR of 9.1% during the forecast period of 2026-2034.

By capability, the intelligence, surveillance & reconnaissance (ISR) segment is expected to lead the market.

The escalation of space domain threats and investment in resilient satellite architectures is a key factor driving market expansion.

Lockheed Martin (U.S.), Northrop Grumman (U.S.), and Raytheon Technologies Corporation (U.S.), among others, are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 201

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us