Synthetic Aperture Radar Market Size, Share, & Industry Analysis, By Offering (Hardware, Software, and Services), By Component (Antenna Subsystem, T/R modules, Timing/reference, & Others), By Frequency Band (VHF/UHF, P-band, L-band, S-band, C-band, X-band, & K/Ka/Ku-band), By Mode (Single & Multi Mode), By Technology (Frequency Modulated Continuous Wave Radar, High-Resolution Interferometry Radar, & Others), By Platform (Spaceborne, Airborne, Ground-Based/Fixed, and Maritime/Coastal) By Application (Military/Defense, Energy & Resources, & Others), By End User, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

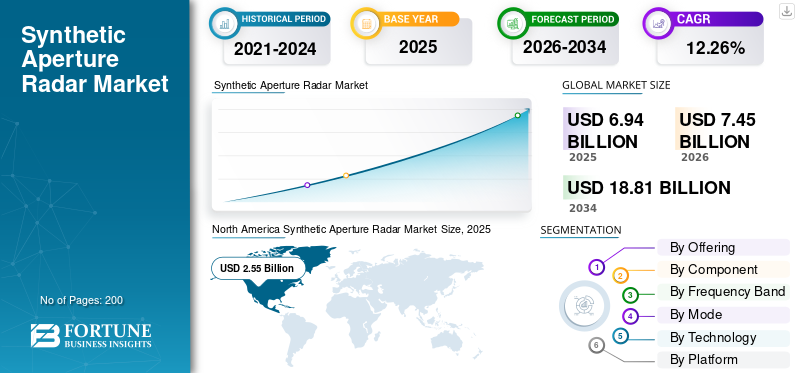

The global synthetic aperture radar market size was valued at USD 6.94 billion in 2025. The market is projected to grow from USD 7.45 billion in 2026 to USD 18.81 billion by 2034, exhibiting a CAGR of 12.26% during the forecast period. North America dominated the global synthetic aperture radar market with a market share of 36.74% in 2025.

The most important factors driving growth are high geopolitical tensions and security-related concerns that have led to increased spending by government defense and intelligence agencies on surveillance systems. Increased volatility in climate conditions and the related need for constant environmental monitoring and disaster management have ensured rising demand for the all-weather tracking capabilities of SAR in the monitoring of floods, landslides, earthquakes, and deforestation.

Moreover, technological advancements in satellite miniaturization, cost reduction in launch services, and improvements in radar processing algorithms have made SAR systems increasingly accessible and economically viable for both defense and commercial uses.

- For instance, in December 2025, Rheinmetall and ICEYE have secured a significant contract from the German military related to the space domain. Rheinmetall ICEYE Space Solutions will provide the German Armed Forces with access to reconnaissance data from a constellation of synthetic aperture radar SAR satellites.

Competitive fragmentation characterizes the SAR market, with established defense contractors such as Lockheed Martin, Northrop Grumman, Thales, Airbus, and others maintaining their dominance through government contracts, technical expertise, and integrated solutions, while new commercial space companies such as Capella Space, Synspective, and others are differentiating themselves through affordable satellite constellations and rapid data delivery models.

Download Free sample to learn more about this report.

Synthetic Aperture Radar Market Key Takeaways

- 2025 Market Size: USD 6.94 billion

- 2026 Market Size: USD 7.45 billion

- 2034 Forecast Market Size: USD 18.81 billion

- CAGR: 12.26% from 2026–2034

- North America dominated the synthetic aperture radar market with a 36.74% share in 2025.

- The military/defense segment accounted for a 59.14% share in 2025.

- The multi-mode segment held a 70.26% share in 2025.

North America

North America was valued at USD 2.55 Billion in 2025, supported by high defense spending and strong investments in space-based surveillance infrastructure.

Europe

Europe is projected to register a CAGR of 14.16% during the forecast period, driven by increasing focus on climate monitoring and disaster response applications.

Asia Pacific

Asia Pacific emerged as the second fastest-growing region, supported by investments in indigenous SAR satellite constellations and military modernization programs.

U.S.

The U.S. market was valued at USD 2.33 Billion in 2025, owing to strong defense modernization initiatives and growing ISR investments.

Japan

The Japan market was valued at USD 259.6 Million in 2025, supported by rising demand for advanced earth observation and surveillance technologies.

Read More

Synthetic Aperture Radar Market Trends

Multi-Frequency Band and Advanced Antenna Architecture Innovation Pose as Market Trends

The industry is undergoing systematic progress in the adoption of multi-frequency band SAR systems incorporating X-band, C-band, S-band, and L-band radar to support the optimization of specific applications. The developments in phased array antennas, namely the adoption of solid-state phased arrays to advance beyond conventional analog phased arrays, embody advanced beam steering, reduced power, increased reliability, and added flexibility for multi-mission systems.

The integration of high-frequency X-band radar systems with phased array antennas to enhance high resolution images and imaging sensitivity signals a profound trend toward applicable commercial or civil uses where high resolution imagery exceeds the norm for military reconnaissance uses.

- For instance, in December 2025, Three Azalea radio frequency (RF) satellites, designed and manufactured by BAE Systems, have been launched with success. Accompanying them is a Synthetic Aperture Radar (SAR) satellite capable of penetrating clouds to capture images of the earth’s surface.

Download Free sample to learn more about this report.

Market Dynamics

Market Growth

Climate Resilience and Environmental Monitoring Imperatives Drives Market Growth

The rising level of climate variability and occurrence of natural disasters has, therefore, raised unprecedented demands for uninterrupted, all-weather environmental monitoring services, which are exclusively offered by SAR technology. Many governmental and international institutions are also investing heavily to monitor key environmental aspects such as deforestation in the Amazon basin, ice melt in polar areas, permafrost degradation, and erosion dynamics.

- For instance, in June 2025, BAE Systems and Hanwha Systems have entered into a Memorandum of Understanding (MOU) aimed at developing technology and collaborative efforts to provide a multi-sensor satellite system for global markets. The companies intend to collaborate by merging BAE Systems’ ultra-wide band Radio Frequency (RF) sensors with Hanwha Systems’ expertise in the space domain for next-generation Synthetic Aperture Radar (SAR) to establish an advanced intelligence, surveillance, and reconnaissance (ISR) capability.

Market Restraint

Capital-Intensive Development and Deployment Economics Hamper Market Growth

The forbidden zone of cost related to development, production, and implementation of the SAR system is believed to be the most significant impediment to market development, especially among smaller military entities and commercial players with restricted budget allocations. The development of functional SAR systems would necessarily involve sophisticated infrastructure, specialized materials with limited supply chains, and precise engineering, which cumulatively lead to production costs much higher than typical satellite systems.

Market Opportunity

Artificial Intelligence-Augmented Image Analysis and Autonomous Decision Systems

Advances in the maturity of generative AI, deep learning, and Physics-Informed Machine Learning processes have significantly altered the SAR data domain, allowing it to evolve from raw images to fully functional intelligence. AI-powered object recognition in SAR images has led to the analysis of terrain, target recognition, and recognition within complex scenes, with the false positives achieved being significantly lower than in manual analysis processes. The area of threat recognition in intelligence has thus been directly impacted by this advancement.

- For instance, in February 2024, the aviation office of the U.S. Defense Logistics Agency has granted a significant contract worth USD 121.5 million to Northrop Grumman Corp. to provide AN/APQ-164 offensive radar low observable antennas for the U.S.

Market Challenges

Technical Complexity Barriers and Algorithm Development Resource Requirements

The inherent technical difficulty in SAR imagery analysis and algorithm development represents a severe shortage in expertise in both the defense and industry sectors. Speckle noise reduction, which is the challenge in generating high-quality SAR imagery, requires refinement in algorithms that are computationally intensive and must keep adapting based on new mission scenarios that trigger new failure modes.

SEGMENTATION ANALYSIS

By Offering

Critical Role in System Performance and Imaging Fidelity Fuels Segment Growth

Based on the offering, the market is divided into hardware, software, and services.

The dominance of the hardware sub-segment lies fundamentally in the irreplaceable role that the hardware sub-segment plays in defining the performance parameters of the SAR system. The role that the hardware sub-segment plays through its components such as the advanced radar antennas, transmitters, and receiver modules defines the resolution capacity, and processing rates.

The services sub-segment is estimated to be the fastest growing with a highest CAGR of 12.95%.

By Component

Irreplaceable Function in Phased Array Architecture and System Integration Boosts Segment Growth

Based on the component, the market is divided into antenna subsystem, T/R modules, timing/reference, data handling & storage, power distribution system, and others.

The T/R modules sub-segment accounted for the largest market share of 27.23% in 2025. The growth is dominated by T/R capability distributed among thousands of discrete modules, each handling the transmit and receive for designated antenna elements. Such architecture mitigates inherent performance bottlenecks found in central architectures: the inability to concurrently carry out multiple modes of the radar, limited frequency agility, as well as susceptibility to electronic jamming based on a single transmit beam.

The antenna subsystem sub-segment is estimated to be the fastest growing with a highest CAGR of 13.15%.

By Frequency Band

Unmatched Resolution Capabilities Driving Precision Targeting and Object Detection

Based on the frequency band, the market is divided into VHF/UHF, P-band, L-band, S-band, C-band, X-band, and K/Ka/Ku-band.

X-band sub-segment is estimated to be the fastest growing at a highest CAGR of 13.27% during the forecast and dominating with a highest share of 33.39%. This dominance due to X-band SAR technology possesses much improved spatial resolution based on the use of its shorter electromagnetic wave, compared to longer wavelengths in other frequency bands, with the capacity to distinguish between features as small as 1-3 meters in conventional operational systems and below 0.5 meters in commercial systems.

The L-band sub-segment is estimated to be the fastest growing with a highest CAGR of 12.89%.

By Mode

Operational Flexibility and Real-Time Mission Adaptation Enabling Operational Superiority

Based on the mode, the market is divided into single mode and multi-mode.

The multi mode sub-segment accounted for the largest market share of 70.26% in 2025. Multi-mode SAR offers transcendent flexibility of operation by leveraging the capability of seamlessly switching between imaging modes during operation missions, thereby enabling swift changes of mission tasking objectives without the need to relocate the platforms. This flexibility of architecture is based on an electronically steered phased array antenna, which offers flexibility of pointing and elevation steering of the antenna beams by means of software on the processor that controls the operation.

The single mode sub-segment is estimated to be the fastest growing with a CAGR of 11.34%.

By Technology

Resolution-Swath Trade-off Resolution through Multi-Beam Architecture

Based on the technology, the market is divided into frequency modulated continuous wave radar, high-resolution interferometry radar, remote sensing technology, 3D radar, duel band sensors, and digital beam forming.

The digital beam forming sub-segment is estimated to be the fastest growing with a highest CAGR of 13.31% and accounted for the largest market share of 24.00%. This growth and dominance due to such a transition of the DBF technology represents the recognition of the fact that the DBF method in every way overcomes the natural limitations of analog phased array systems, especially the conflict between the resolution and the width of the coverage swath, which has dictated the design of SAR systems for the past forty years.

The remote sensing technology sub-segment is estimated to be the second fastest growing with a highest CAGR of 13.29%.

By Platform

Global Coverage and Persistent Monitoring Capabilities Transcending Airborne Limitations

Based on the platform, the market is divided into spaceborne, airborne, ground-based/fixed, and maritime/coastal.

The spaceborne sub-segment is estimated to be the fastest growing with a highest CAGR of 13.05% during the forecast period. The growth is driven by space-based SAR systems that offer unparalleled geographic reach through their use in orbit, which facilitates witnessing distant, politically insecure, or otherwise inaccessible areas without need for airfield access or overfly approvals and without need for sustained flight operations. Satellite orbit paths enable satellites to provide a constant seeking for geometry over identified areas on the surface independent of surface topographic features that could impede airborne flight.

The airborne sub-segment is estimated to be the second fastest growing with a highest CAGR of 12.24%.

By Application

All-Weather Intelligence and Reconnaissance Providing Irreplaceable Military Value

Based on the application, the market is divided into military/defense, energy & resources, infrastructure monitoring, environment & climate, agriculture, mapping & geospatial, and others.

The military/defense sub-segment accounted for the largest market share of 59.14% in 2025. This dominance due to the military/defense establishes a leading position in the market based on the sole ability of SAR to provide high-resolution images regardless of the environmental conditions that will interfere with other observation systems, thus preventing them from performing uninterrupted ISR missions.

The infrastructure monitoring sub-segment is estimated to be the second fastest growing with a highest CAGR of 14.32%.

By End User

To know how our report can help streamline your business, Speak to Analyst

Defense Modernization Programs and Multi-Year Procurement Commitments

Based on the end user, the market is divided into defense & national security, civil government, commercial, and academic/research.

The defense & national security sub-segment accounted for the largest market share of 61.09% in the year 2025. The dominance reflects the geo-political landscape shaped by sustained military modernization investments across major defense establishments globally. The U.S. Department of Defense, NATO allies, and Asia-Pacific military forces are expanding their investments in SAR for platform modernization (F-22 Raptor, F-35 Lightning II, Eurofighter, naval combat systems) and the development of space-based surveillance systems. Multi-year defense contracts for military system procurements, development of satellite constellations, and ISR capability expansion ensure sustained revenue streams, supported by government defense budgets resistant to commercial market fluctuations.

The civil government sub-segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 12.84% during the forecast period.

Synthetic Aperture Radar Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Synthetic Aperture Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America region is accounted for the largest share with valued around USD 2.55 billion and holding the 36.74% of the global market share. Fueled by an unmatched regional presence of defense budgets, resource allocations, and technological developments within the space-based reconnaissance systems infrastructure. The dominance of the regional presence is underscored by the commitment of the DoD, National Reconnaissance Office, U.S. Space Force, and all intelligence agencies, which comprise the world's most sophisticated infrastructure within the space-based surveillance systems network headquartered within North America.

U.S. Synthetic Aperture Radar Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.33 billion in 2025, estimated growth rate roughly 10.34% of global synthetic aperture radar market growth.

Europe

Europe is estimated to be the fastest growing region with a highest CAGR of 14.16% during the forecast period. The market expansion is accelerating through a focused emphasis on applications related to monitoring climate change, environment protection, and disaster response. This has positioned it as the world leader in the area of civilian earth observation applications, with unique competitive positioning, distinct from the defense-oriented key players' market focus.

U.K. Synthetic Aperture Radar Market

The U.K. market in 2025 is estimated at around USD 251.3 million, representing growth rate at 14.32% of global market.

Germany Synthetic Aperture Radar Market

The Germany market in 2025 is estimated at around USD 327.6 million, representing growth rate 15.04% of global market.

Nordic Countries Synthetic Aperture Radar Market

The Nordic Countries market in 2025 is estimated at around USD 159.4 million, representing growth rate at 16.44% of global market.

Asia Pacific

Asia Pacific estimated to be the second fastest growing region in the global market. This growth is fueled by the emerging emphasis that governments are placing in supporting indigenous SAR satellite constellations that assist in military reconnaissance, disaster response, and resource management, which aligns with their space dominance strategies.

India Synthetic Aperture Radar Market

The India market in 2025 is estimated at around USD 209.3 million, representing growth rate at 16.29% of global market.

Japan Synthetic Aperture Radar Market

The Japan market in 2025 is estimated at around USD 259.6 million, representing growth rate at 12.11% of global market.

Australia Synthetic Aperture Radar Market

The Australia market in 2025 is estimated at around USD 161.8 million, representing growth rate at 14.47% of global market.

Middle East & Africa

Regional security justification for the use of space-based reconnaissance in the region, as a consequence mostly oriented in a regional context, has generated the potential for regional cooperation as development in space is a region of low friction where technologies and commercial partnerships can emerge despite regional tensions.

Israel Synthetic Aperture Radar Market

The Israel market in 2025 is estimated at around USD 157.4 million, representing growth rate at 12.82% of global market.

Latin America

Latin America is a moderate-growing market for SAR, expanding from USD 410.9 million in 2025 to USD 757.9 in 2034. It is based on the steadily growing commercial demand for services that relate to agricultural insurance, supply chain, and environmental protection.

COMPETATIVE ANALYSIS

Key Industry Players

Market Consolidation, Fragmentation and Asymmetric Competition among Defense and Commercial Players

The international synthetic aperture radar market share has a complex competitive framework as there is moderate consolidation and also persistent fragmentation. As a result, there is a bifurcated competitive environment with divergent operation models. The competitive environment is asymmetric as there is a major segment comprising major aerospace and defense contractors (Lockheed Martin, Northrop Grumman, Airbus Defense and Space, Thales Group, and Raytheon Technologies) that hold major market share due to their integrated defense strategy, historical ties with governments, and successful technology models within several application areas for SAR.

The development of the market from a state monopolized market to a pluralistic competitive market in the sectors of defense, civil government, and commercial markets has brought about a major structural change that is increasingly reducing the competitive advantage that has traditionally been characteristic of the incumbent defense companies.

LIST OF KEY SYNTHETIC APERTURE RADAR COMPANIES PROFILED

- Airbus Defense and Space GmbH (Germany)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- BAE Systems plc (U.K.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Saab AB (Sweden)

- HENSOLDT AG (Germany)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (Israel)

- Mitsubishi Electric Corporation (Japan)

- Hanwha Systems Co., Ltd. (South Korea)

- Bharat Electronics Limited (India)

- MDA Space Ltd. (Canada)

- Kongsberg Satellite Services AS (KSAT) (Norway)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Finnish satellite operator Iceye, specializing in SAR technology, and Japan's aerospace and defense firm IHI Corporation have recently entered into an agreement to create a constellation of Earth observation satellites for security, civilian, and commercial applications.

- September 2025: Rocket Lab Corporation has obtained a second multi-launch agreement with Synspective, a prominent company specializing in Synthetic Aperture Radar (SAR) satellite data and analytics.

- May 2025: Capella Space Corp. revealed a collaboration with the U.S. Department of Defense's Defense Innovation Unit (DIU) to create new modes for synthetic aperture radar (SAR) imaging acquisition that will aid the Hybrid Space Architecture (HSA).

- February 2025: The U.K. Ministry of Defense (MoD) has granted Airbus the Oberon contract to develop and construct two synthetic aperture radar (SAR) satellites, which will deliver continuous, all-weather, day-and-night space-based intelligence, surveillance, and reconnaissance (ISR) capabilities.

- January 2025: Hensoldt, a sensor solutions firm based in Germany, has been awarded a contract by the DLR Quantum Computing Initiative (DLR QCI) to join the QUA-SAR research project, aimed at enhancing radar remote sensing technology.

REPORT COVERAGE

The global synthetic aperture radar market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and global market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.26% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Offering · Hardware · Software · Services By Component · Antenna Subsystem · T/R modules · Timing/reference · Data Handling & Storage · Power Distribution System · Others By Frequency Band · VHF/UHF · P-band · L-band · S-band · C-band · X-band · K/Ka/Ku-band By Mode · Single Mode · Multi-Mode By Technology · Frequency Modulated Continuous Wave Radar · High-Resolution Interferometry Radar · Remote Sensing Technology · 3D Radar · Duel Band Sensors · Digital Beam Forming By Platform · Spaceborne · Airborne · Ground-Based/Fixed · Maritime/Coastal By Application · Military/Defense · Energy & Resources · Infrastructure Monitoring · Environment & Climate · Agriculture · Mapping & Geospatial · Others By End User · Defense & National Security · Civil Government · Commercial · Academic/Research By Region

· U.S. (By Platform) · Canada (By Platform)

· U.K. (By Platform) · Germany (By Platform) · France (By Platform) · Nordic Countries (By Platform) · Eastern Europe (By Platform) · Rest of Europe (By Platform)

· China (By Platform) · India (By Platform) · Japan (By Platform) · Australia (By Platform) · Southeast Asia (By Platform) · Rest of Asia Pacific (By Platform)

· Israel (By Platform) · Saudi Arabia (By Platform) · United Arab Emirates (By Platform) · Turkey (By Platform) · South Africa (By Platform) · Rest of Middle East & Africa (By Platform)

· Brazil (By Platform) · Argentina (By Platform) · Rest of Latin America (By Platform) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.94 billion in 2025 and is projected to reach USD 18.81 billion by 2034.

In 2025, the market value stood at USD 1.75 billion.

The market is expected to exhibit a CAGR of 12.26% during the forecast period.

By application, the military/defense segment is expected to lead the market.

The climate resilience and environmental monitoring imperatives drives the market growth.

Lockheed Martin, Northrop Grumman, Thales, and Airbus, are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us