Space Electronics Market Size, Share & Industry Analysis, By Platform (Satellite, Launch Vehicles, Deep Space Probes, and Ground Equipment), By Application (Communication Systems, Data Handling/Computing, Power Management and Distribution, and Others), By Purpose (Communication, Earth Observation, Navigation, Global Positioning System (GPS) and Surveillance, Technology Development and Education, and Others), By Component (Microprocessors and Controllers, Sensors, Application Specific Integrated Circuits (ASIC), Memory Chips, Discrete Semiconductors, and Other), and Regional Forecast, 2026-2034

Space Electronics Market Size and Future Outlook

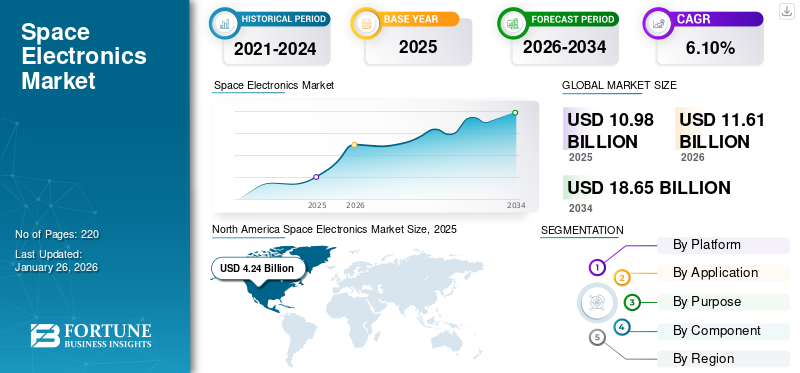

The global space electronics market size was valued at USD 10.98 billion in 2025. The market is projected to grow from USD 11.61 billion in 2026 to USD 11.61 billion by 2034, exhibiting a CAGR of 6.10% during the forecast period. North America dominated the space electronics market with a market share of 38.59% in 2025.

The market encompasses specialized electronic components and systems engineered to function in extreme space environments, including radiation, vacuum, and temperature extremes. These electronics are essential for ensuring the reliability and performance of space missions across various platforms such as satellites, ground equipment, launch vehicles, and deep space probes.

Satellites depend on processors, memory chips, sensors, and power systems to enable communication, navigation, and Earth observation. Launch vehicles utilize avionics, guidance systems, and telemetry electronics to ensure accurate payload delivery. Deep space probes require radiation-hardened processors and autonomous systems for long-duration missions beyond Earth’s orbit. Ground equipment, though less exposed to harsh environments, relies on advanced electronics for mission control, data handling, and communication.

Prominent players operating in the market are bae systems, Northrop Grumman, Thales Alenia Space, Honeywell, STMicroelectronics, Microchip Technology, Cobham, TT Electronics, teledyne e2v uk ltd, and Airbus Defense & Space. With growing satellite deployments, defense needs, and deep space exploration, space electronics form the backbone of the modern space economy.

Download Free sample to learn more about this report.

Space Electronics Market KEY TAKEAWAYS

- 2025 Market Size: USD 10.98 billion

- 2026 Market Size: USD 11.61 billion

- 2034 Forecast Market Size: USD 11.61 billion

- CAGR: 6.10% from 2026–2034

- North America dominated the space electronics market with a 38.59% share in 2025.

- The satellite segment is projected to account for the largest market share with 38.93% in 2026.

- The communication systems segment is projected to hold a 40.19% share in 2026.

Asia Pacific

Asia Pacific reached USD 2.89 billion in 2025, driven by rising investments in military and commercial space missions.

North America

North America accounted for USD 4.24 billion in 2025, supported by strong government funding and leading commercial space companies.

Europe

Europe accounted for USD 2.96 billion in 2025, driven by growing investments in satellite technologies and space exploration.

U.S.

The U.S. market is projected to reach USD 3.15 billion by 2026, supported by NASA programs and expanding private space initiatives.

Japan

The Japan market is projected to reach USD 0.51 billion by 2026, driven by increasing investments in satellite development and advanced space technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Surge in Satellite Constellations and Rising Demand of Satellite Communications Expected to Boost Market Growth

The growing number of large-scale satellite constellations, particularly in low Earth orbit (LEO), is significantly boosting demand for advanced space electronics. Mega-constellation programs such as SpaceX’s Starlink, Amazon’s Project Kuiper, and OneWeb collectively plan to deploy thousands of satellites in the coming years, each requiring specialized electronics for communication, data handling, navigation, and power source management.

Moreover, the constellation of satellites is expanding as space agencies and companies launch new satellites to grow their networks. For instance, SpaceX expanded its Starlink satellite network with the successful launch of 28 new satellites on May 6 2025, bringing the total to over 7,200 in low Earth orbit. This latest deployment strengthens Starlink’s position as a leader in global satellite internet, especially as demand for reliable connectivity grows.

MARKET RESTRAINTS

Supply Chain Disruptions, High Cost, and Regulations Associated are Expected to Hinder Market Growth

The global supply market is poised to face challenges as it contends with supply chain disruptions and geopolitical tensions. Supply chain disruptions, stemming from factors such as raw material shortages, transportation issues, and geopolitical instabilities, pose a significant threat to the smooth operation of the space electric supply industry. These disruptions can result in delays, increased costs, and hampered production efficiency, impacting the overall growth of the market.

The high cost of designing and manufacturing Space electric that can withstand extreme space conditions is a significant challenge that is hindering the global space electronics market growth. The space industry is highly regulated, and all components require stringent quality inspections and legal documentation before use in a spacecraft, which adds to the cost. Additionally, the use of sophisticated control systems and the high performance testing and raw material prices also contribute to the high cost of space electronics.

MARKET OPPORTUNITIES:

Rising Investments In Deep Space Exploration and Shift Toward Commercial Space Exploration Are Prominent Market Opportunities

In-Situ Resource Utilization (ISRU) is a crucial idea and technique in space exploration that entails harnessing resources found on extraterrestrial bodies such as the Moon, Mars, asteroids, or other planets to support human missions and settlements. Instead of relying only on Earth-based supplies, ISRU intends to lower mission costs, boost self-sufficiency, and enable long-duration space exploration by utilizing accessible resources in space.

ISRU using space-based resources for deep space exploration can increase safety for crew and enhance mission capabilities, allowing it to explore farther from Earth with more independence.

SPACE ELECTRONICS MARKET TRENDS:

Rise of On-Board Processing and AI in Space Electronics are Major Market Trends

One of the most transformative trends shaping the market is the integration of on-board processing and artificial intelligence (AI) into satellites and space systems. Traditionally, satellites functioned as passive collectors of data, capturing imagery or signals and then transmitting them back to Earth for processing.

This model created a heavy reliance on ground stations, often leading to significant delays between data capture and actionable insights. However, with the rapid advancements in space-grade electronics, including radiation-tolerant processors and machine learning accelerators, satellites are increasingly shifting toward autonomous, edge-based intelligence.

The U.S. National Aeronautics and Space Administration (NASA), the European Space Agency (ESA), and private players such as Northrop Grumman and Lockheed Martin are actively investing in missions that test and implement on-board processing.

MARKET CHALLENGES:

Radiation Resilience in Space to Hamper Market Growth

One of the key challenges facing the market is radiation resilience. Electronic components deployed in space are continuously exposed to high levels of cosmic radiation and charged particles that can degrade performance or lead to complete failure. Developing radiation-hardened (rad-hard) systems is technologically demanding, requiring specialized design, testing, and qualification, which limits the pace of innovation compared to terrestrial electronics.

Russia Ukraine War Impact

Beginning in February 2022, the conflict between Russia and Ukraine led to widespread sanctions and a reorganization of the world's defense and aerospace supply lines. Once heavily involved in the international space sector through component trade, satellite cooperation, and launch services, Russia was subject to stringent regulations.

While the Russian Soyuz rocket, which served as the foundation for European and commercial launches, was removed from the Guiana Space Centre in French Guiana, the European Space Agency (ESA) halted cooperation missions with Roscosmos, including the ExoMars program.

US Tariff War Impact

The U.S. government has enacted multiple tariff and export-control measures affecting advanced electronics, including those used in space systems. Under section 301 tariffs, imports from China across semiconductor categories such as HTS 8541 (semiconductor devices) and HTS 8542 (integrated circuits) have faced additional duties since 2018, which were extended and expanded in 2024.

Tariffs increased costs by adding duty margins of up to 25% on certain imports, raising the bill of materials (BOM) for satellite, probe, and launch vehicle electronics.

Export controls further restrict the availability of advanced logic and memory chips, lengthening supply lead times and complicating global partnerships.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Expansion of Satellite Constellations Contributed to Segmental Growth

On the basis of the segmentation of platform, the market is classified into satellite, launch vehicles, deep space probes, and ground equipment.

The satellite segment is expected to capture the largest share of the market contributing 38.93% globally in 2026. The growth of space electric for satellites is being driven by the unprecedented expansion of satellite constellations, particularly in low Earth orbit (LEO).

To know how our report can help streamline your business, Speak to Analyst

The deep space probe segment accounted for the significant space electronics market share in 2024. The revival of deep space exploration missions is significantly boosting demand for specialized space electronics.

By Application

Increasing Demand for Broadband Connectivity Fuels Growth of Communication Systems Segment

In terms of application, the market is categorized into communication systems, data handling/computing, power management and distribution, and others.

The communication systems segment is projected to capture the largest share of the market contributing 40.19% globally in 2026. In 2025, the segment is anticipated to dominate with 40.42% share. The growth of space electric in communication systems is being fueled by the increasing demand for global broadband connectivity through satellite networks. Large constellations, such as SpaceX’s Starlink and Amazon’s Kuiper.

The data handling/computing segment is expected to grow at a CAGR of 6.5% over the forecast period.

By Purpose

Increased Focus on Communication Satellite Constellations Supplemented Communication Segment Growth

Based on purpose, the market is segmented into communication, Earth observation, navigation, global positioning system (GPS) and surveillance, technology development and education, and others.

The communication segment is estimasted to hold the dominating position contributing 33.18% globally in 2026. The demand for space electric in communication is expanding rapidly due to the deployment of broadband satellite constellations that aim to close the global digital divide.

The segment of Earth observation is set to flourish and is growing at a CAGR of 6.1% growth across the forecast period.

By Component

Complex Satellite Payload Anticipated for Microprocessors and Controllers Segment Growth

Based on component, the market is segmented into microprocessors and controllers, sensors, application specific integrated circuits (ASIC), memory chips, discrete semiconductors, and other.

The microprocessors and controllers using AI segment is projected to hold the dominating position contributing 21.90% globally in 2026. The demand for hardened and radiation tolerant microprocessors and controllers is rising due to the increasing complexity of satellite payloads and mission requirements.

The segment of sensor is set to flourish with a growth rate of 6.7% growth across the forecast period.

Space Electronics Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Space Electronics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 4.24 billion, contributing 38.59% to global market revenue, and is projected to grow to USD 4.45 billion in 2026. The North American market for space electronics is strongly driven by the presence of major space agencies such as NASA and the U.S. Space Force, alongside leading commercial players such as SpaceX, Northrop Grumman, and Lockheed Martin. In 2026, the U.S. market is estimated to reach USD 3.15 billion.

Europe and Asia Pacific

Other regions such as Europe and Asia Pacific are anticipated to witness a notable growth in the coming years. The Europe market accounted for USD 2.96 billion in 2025, representing 26.05% of the global industry, and is expected to reach USD 3.13 billion in 2026. During the forecast period, Asia Pacific recorded a market size of USD 2.89 billion in 2025, capturing 26.34% of the global market share, and is projected to reach USD 3.09 billion in 2026. This is primarily due to the higher investment in space missions for military and commercial applications. Backed by these factors, countries including China anticipate to record the valuation of USD 0.91 billion, Japan to record USD 0.51 billion, and India to record USD 0.76 billion in 2026. After Asia Pacific, the UK market is estimated value at USD 0.89 billion by 2026, and the Germany market will value at USD 0.8 billion by 2026.

Rest of the World

Over the forecast period, rest of the world regions would witness a moderate growth in this marketspace. The Middle East & Africa market generated USD 0.89 billion in 2025, representing 8.12% of the global market landscape, and is expected to reach USD 0.94 billion in 2026. Latin America is set to attain the value of USD 0.27 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Product Innovation and Specialized Suppliers Drive Market Growth

The market is characterized by a mix of established aerospace defense contractors, semiconductor companies, and niche specialized suppliers. Competition is driven by innovation in radiation-hardened (rad-hard) electronics, cost reduction through commercial off-the-shelf (COTS) components, and the ability to meet the rigorous standards of space missions.

Major players such as Northrop Grumman, BAE Systems, Thales Alenia Space, Airbus Defense and Space, and Honeywell dominate the supply of mission-critical systems for satellites, launch vehicles, and probes.

LIST OF KEY SPACE ELECTRONICS COMPANIES PROFILED:

- BAE Systems (U.K.)

- Cobham Limited (U.K.)

- Honeywell International Inc. (U.S.)

- Infineon Technologies (Germany)

- Microchip Technology (U.S.)

- Northrop Grumman Corporation (U.S.)

- RUAG International AG (Switzerland)

- STMicroelectronics (Switzerland)

- Texas Instruments (U.S.)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: BAE awarded a USD 1.2 billion contract by U.S. Space Force (Space Systems Command) under the “Resilient Missile Warning & Tracking – Medium Earth Orbit Epoch 2” program: to design, build, and support 10 satellites, including ground operations.

- July 2025: Thales Alenia Space and the Italian Space Agency (ASI) signed to develop the first human lunar outpost (Multipurpose Habitation Module) as part of NASA’s Artemis program.

- December 2024: Honeywell selected by MDA Space Ltd. to deliver satellite Attitude Control Systems (reaction wheels, 3-axis space rate sensors, magnetometer unit) for the MDA AURORA product line.

- October 2024: European Space Agency (ESA) ordered 6 additional radar-based satellites from Thales Alenia Space for the Italian Earth observation constellation IRIDE.

- May 2024: Microchip introduces a new family of Radiation-Tolerant isolated DC-DC 50W converters (LE50-28 family) for LEO market needs, plus enhancements to its PolarFire RT SoC FPGA line with real-time Linux capability, and new power / reliability features.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The space electronics market report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.10% from 2026 to 2034 |

|

Segmentation

|

By Platform

|

|

By Component

|

|

|

By Application

|

|

|

By Purpose

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 10.98 billion in 2025 and is projected to reach USD 11.61 billion by 2034.

In 2025, the market value stood at USD 4.24 billion.

The market is expected to exhibit a CAGR of 6.10% during the forecast period.

Satellite segment led the market by platform.

Surge in satellite constellations coupled with rising demand of satellite communications is expected to boost the market growth.

Northrop Grumman, BAE Systems, Thales Alenia Space, Airbus Defense and Space, and Honeywell are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us