Space Infrastructure Market Size, Share & Industry Analysis, By Component (Satellites, Ground Station, Launch Vehicles, and Others), By Application (Earth observation, Telecommunication, Research, and Others), By End-User (Commercial, Government, and Private Agencies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

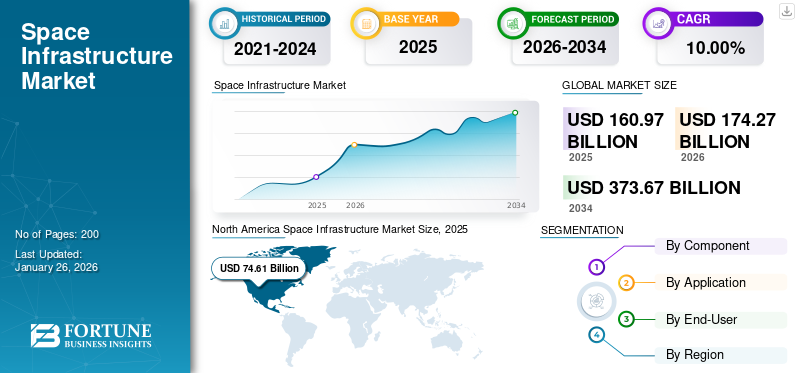

The global space infrastructure market size was valued at USD 160.97 billion in 2025. The market is projected to grow from USD 174.27 billion in 2026 to USD 373.67 billion by 2034, exhibiting a CAGR of 10.00% during the forecast period. North America dominated the space infrastructure market with a market share of 46.35% in 2025.

The space infrastructure encompasses the facilities, technologies, and systems that support various activities in outer space. The market is integral to the broader space economy and includes all public and private entities involved in developing and providing space-enabled products and services.

The development of space infrastructure is critical for enhancing capabilities in various sectors, including telecommunications, navigation, weather forecasting, and scientific research. As the demand for space-based services grows, the need for robust infrastructure to support these activities also increases. The orbital infrastructure market plays a pivotal role in advancing human activities in space by providing the necessary frameworks for operational efficiency and innovation within the space economy.

Companies, such as SpaceX and United Launch Alliance (ULA) provide the necessary infrastructure for launching satellites into orbit. These offer satellite communication and data services. Additionally, entities, such as Axiom Space and Blue Origin are developing platforms for research and habitation in space.

The COVID-19 pandemic significantly affected the market, leading to delays, financial losses, and structural changes within the industry. The impact varied across different segments, with Small and Medium-Sized Enterprises (SMEs) facing challenges. The pandemic exposed vulnerabilities in the space sector, particularly affecting SMEs that constitute a significant portion of the industry. Many of these firms struggled with cash flow issues, leading to potential market consolidation as larger companies engrossed SMEs or as smaller firms exited the market altogether.

Overview

The development of spaceports, particularly in Norway and Sweden, is a significant advancement for the Arctic, where traditional terrestrial communication infrastructure is limited. The development of spaceports in Norway and Sweden aims to facilitate small satellite launches and improve connectivity in areas traditionally underserved by terrestrial communication networks.

- Andoya Spaceport (Norway) - In 2021, the Norwegian government decided to extend budgetary financial assistance to Andoya Spaceport, situated on the coast of Northern Norway, to create a launch base for small satellites. Andoya Space provided the services for the launch infrastructure, while companies facilitated launches for international clients.

- Esrange spaceport (Kiruna in Sweden) - Esrange is situated far north of Sweden, beyond the Arctic Circle. The space center launched rockets for microgravity and atmospheric studies as well as high-altitude balloons for astronomy, atmospheric analysis, and drop testing of space and aerial craft. In October 2020, the Swedish government announced the creation of the ability to launch small satellites from Esrange.

Challenges

The expansion of spaceports poses risks to fragile Arctic ecosystems. Concerns include noise pollution, air and water contamination from rocket launches, and potential habitat disruption for wildlife, particularly endangered species. Effective management of these challenges requires robust international collaboration, particularly through bodies, such as the Arctic Council, to ensure that developments align with sustainability goals and address shared concerns across nations. The operational activities of these spaceports can disrupt local industries, particularly fishing and tourism.

For instance, Andoya Space's launch operations necessitate the activation of safety zones, which can limit access to crucial fishing grounds during key seasons, such as winter cod fishing. This poses a challenge in balancing spaceport activities with the livelihoods of local communities.

Download Free sample to learn more about this report.

SPACE INFRASTRUCTURE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 160.97 Billion

- 2026 Market Size: USD 174.27 Billion

- 2034 Forecast Market Size: USD 373.67 Billion

- CAGR: 10.00% from 2026–2034

- North America dominated the market with a 46.35% share in 2025.

- Ground station segment accounted for a 38.39% share in 2026.

- Earth observation segment held a 37.11% share in 2026.

North America

North America generated USD 74.61 Billion in 2025 (46.35% share) and is projected to reach USD 81.36 Billion in 2026.

Europe

Europe reached USD 35.84 Billion in 2025 (22.27% share) and is expected to grow to USD 38.86 Billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 25.08 Billion in 2025 (15.58% share) and is projected to reach USD 27.06 Billion in 2026.

U.S.

The market is projected to reach USD 69.22 Billion by 2026.

Japan

The market is projected to reach USD 5.54 Billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Technological Advancements, Investments from the Private Sector, and Growing Demand for Space Data are Transforming the Market

A significant contributor to growth of the space infrastructure industry is the advancement of technologies, such as reusable launch systems, SmallSats (low-weight and size satellites, typically below 2,600 lbs.), and CubeSats (miniaturized satellites with a cubic shape). Such innovation has reduced costs associated with creating new space systems and launching payloads into orbit, thereby allowing a broader array of organizations to engage in the market. The advancement of SmallSats and CubeSats has notably heightened the interest of private enterprises and government organizations in funding this sector, as it offers more cost-effective access to space and innovative business models, including constellations.

Another key factor contributing to growth in the market has been the rise in private-sector investments. A large number of venture capital firms and private equity firms are investing in the space industry, and private companies are entering the market to offer space-related products and services. By the end of 2022, the worldwide space industry had drawn in approximately USD 272 billion in PE investments across 1,791 distinct companies since 2013. Simultaneously, investments in the area of national security are also growing swiftly. For example, in the U.S., the FY23 national security space budget designated USD 20.8 billion for National Security Space investment accounts, marking a 19.5% rise from FY22.

Firms including SpaceX, Blue Origin, and Relativity Space are investing their resources into the creation and marketing of innovative technologies, such as reusable launch vehicles. For example, SpaceX secured approximately USD 2 billion in 2022 with a bold agenda for 2023 that features 87 rocket launches, ongoing lunar exploration initiatives, and the growth of Starlink internet service. Such private firms are also growing into different sectors, including satellite-based services.

The rapidly expanding space data-as-a-service sector, where specialized firms provide high-quality data to their clients, is another major contributor to space infrastructure market growth. Government entities, private businesses, and research organizations are progressively utilizing space-derived data to assist in various applications, including satellite internet. Communication and earth observation service providers are expected to gain benefits from the data produced by satellites. Specialized space firms can construct, possess, and manage satellites, providing data and communications for clients and allowing end-users to concentrate on improving their primary business. This solution allows customers to subscribe to space-based data services with personalized data sets for specific use cases.

Market Restraints

Economic Uncertainty, Spectrum Regulations and Technological Barriers are Impeding Market Expansion

Wider economic uncertainty may hinder investment in space infrastructure initiatives, especially in the Space as a Service (SPaaS) sector. Firms might be reluctant to allocate resources during economic declines, impacting the overall market expansion.

The growing Direct-to-Device (D2D) connectivity market encounters challenges concerned with spectrum regulations, which may restrict the operational potential of satellite services and pose obstacles for newcomers seeking to implement their technologies. The necessity for thorough regulatory structures overseeing private space endeavors can hinder the speed of innovation and investment. Though nations, including India, are progressing with new strategies, the worldwide scenario continues to be divided, hindering international cooperation.

Creating sophisticated satellite technologies and infrastructure necessitates significant financial investment. The expenses related to launching satellites and supporting infrastructure can be difficult for numerous startups and smaller firms. As the sector moves toward cohesive systems, established companies might find it challenging to adjust to the emerging business models and technologies. This shift may create issues as traditional firms compete with startups that utilize creative solutions.

Market Opportunities

Government Efforts in Advancing and Funding Space Infrastructure Offer Major Growth Opportunity

The market growth is associated with ongoing updates and significant advancements occurring worldwide. This includes a trial of a new rocket system, the deployment of a cutting-edge satellite, and a robotic mission successfully landing on the moon.

The World Economic Forum projects that the worldwide space economy will reach USD 1.8 trillion by 2035 (considering inflation), increasing from USD 630 billion in 2023. This includes ‘backbone’ applications - including those for satellites, launch vehicles, and services such as broadcasting TV or GPS—and ‘reach’ applications—where space technology assists businesses in various sectors in generating income. For instance, Uber depends on the integration of satellite signals and smartphone chips to link drivers with riders and offer navigation in every city.

As per the World Economic Forum, in 2023, backbone applications accounted for USD 330 billion, which is over 50% of the global space economy, whereas reach applications totaled USD 300 billion. The anticipated yearly growth rate for backbone and reach applications is double the forecasted GDP growth rate for the next ten years. In comparison, the value projections for space resemble those of semiconductors (valued at around USD 600 billion in 2021, with an annual growth of 6 to 8% over the 2030s). They are about 50 % of the forecast for the global payments sector (expected to hit USD 3.2 trillion in revenue by 2027).

The factors fueling the expansion of the space economy include the need for enhanced connectivity through satellites, a growing need for positioning and navigation services on smartphones, and a rise in demand for AI and machine learning-driven insights. These advancements are providing enhanced advantages to a broader array of stakeholders, encompassing firms in sectors from food and drink to transport.

SPACE INFRASTRUCTURE MARKET TRENDS

Advancements in Additive Manufacturing and the Integration of AI and ML are Significantly Transforming the Market

Additive manufacturing, commonly known as 3D printing, is revolutionizing the aerospace industry by enabling on-demand production of components. This technology allows the creation of parts directly from digital designs, which can drastically reduce lead times and enhance mission flexibility.

By minimizing waste and allowing complex geometries, additive manufacturing can lower production costs. Traditional manufacturing often results in significant material waste due to subtractive processes. In contrast, additive techniques can achieve a buy-to-fly ratio close to 1:1, compared to ratios as high as 10:1 in conventional methods. Lighter components contribute to reduced fuel consumption and increased payload capacity. Additive manufacturing enables the design of lightweight structures without compromising on strength, which is crucial for aerospace applications.

- The recent collaboration between LEAP 71 and The Exploration Company is focusing on using additive manufacturing for high-performance rocket engines, indicating a shift toward more innovative and cost-effective production methods in space exploration.

The incorporation of AI and ML into satellite systems and additive manufacturing processes further enhances operational efficiency. AI algorithms can analyze vast amounts of data generated during manufacturing processes, ensuring quality control and optimizing production workflows. This leads to higher reliability in component performance.

AI can streamline the design phase by optimizing parts specifically for additive manufacturing, reducing complexity and material usage while speeding up time-to-market. Machine learning models are flexible as they can adapt based on real-world performance data, leading to ongoing enhancements in component design and manufacturing processes.

These advancements not only improve the efficiency of producing space components but also enable more flexible mission planning and execution. As the aerospace industry continues to embrace these technologies, the potential for innovation and cost savings grows significantly.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Ground Station Segment Dominated the Market Owing to Increasing Demand for Satellite Services

By component, the market is classified into satellites, ground station, launch vehicles, and others.

In 2026, the ground station segment is projected to lead the market with a 38.39% share and will be the fastest-growing segment for the 2026-2034 period. Ground stations are essential for telemetry, tracking, and command operations, which are essential for maintaining satellite functionality and data transmission. Various key players leverage the satellite service model, rapidly increasing the number of operational ground stations.

The satellite segment is anticipated to show significant growth during the forecast period. The applications for satellites are diversifying beyond traditional communication services and include earth observation, climate monitoring, and military uses. This expansion further drives investment and interest in satellite deployment as various sectors recognize the value of satellite data.

By Application Analysis

Increasing Demand for Environmental Monitoring Boosts the Need for Earth Observation in the Market

Based on application, the market is segmented into earth observation, telecommunication, research, and others.

The earth observation segment is anticipated to hold a dominant market share of 37.11% in 2026 and will be the fastest-growing segment for the 2026-2034 period. There is a rising global emphasis on environmental issues, such as climate change, deforestation, and disaster management. Governments and organizations are increasingly relying on satellite-based Earth observation data to monitor these challenges effectively. For instance, in June 2023 the European Commission implemented regulations requiring detailed geographical information to track commodities associated with deforestation, thereby boosting demand for Earth observation services. The segment is poised to hold 37% of the market share in 2025.

The telecommunication segment is projected to show significant growth during the study period. Advancements in communication technologies, such as High-Throughput Satellites (HTS) and Low-Earth Orbit (LEO) systems, are enhancing the efficiency and capacity of satellite telecommunications. These innovations are making it feasible to offer competitive pricing models for broadband services, which attracts more users and drives the global market.

The research segment is anticipated to record a significant CAGR of 9.83% during the forecast period (2026-2034).

To know how our report can help streamline your business, Speak to Analyst

By End-User Analysis

Expansion of New Markets in Developing Regions Boosted Commercial Segment Growth

By end-user, the market is categorized into commercial, government, and private agencies.

The commercial segment is expected to account for 43.52% of the market in 2026. The rise of new markets, particularly in developing regions, is contributing to the growth of commercial applications in space infrastructure. As economies grow and urbanize, there is a greater need for satellite services to support infrastructure development, logistics, and supply chain management. Companies are investing in satellite technology to gain competitive advantages in these emerging markets. The segment is expected to attain 43% of the market share in 2025.

The government segment is anticipated to show moderate growth during the study period. Governments across the globe are investing heavily in space infrastructure for national security purposes, including surveillance, reconnaissance, and communication capabilities. The growing emphasis on defense spending has led to increased demand for satellites that can support military operations and intelligence gathering. This segment is foreseen to grow with a considerable CAGR of 9.75% during the forecast period (2026-2034).

SPACE INFRASTRUCTURE MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

North America Space Infrastructure Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America recorded a market size of USD 74.61 billion in 2025, capturing 46.35% of the global market share, and is projected to reach USD 81.36 billion in 2026. The U.S. is anticipated to dominate the country level market in the region. North America is home to major companies such as SpaceX, Blue Origin, and Boeing, which are at the forefront of satellite launches, space logistics, and innovative technologies. The region benefits from substantial government investment through NASA and the Department of Defense, driving advancements in satellite servicing and in-orbit refueling. The presence of a robust technological infrastructure supports research and development in space technologies. The focus on commercial mega-constellations, such as SpaceX's Starlink, has created an enormous demand for satellite services, further solidifying North America's leadership position. The U.S. space infrastructure is rapidly evolving to meet growing demands in national security, commercial space activities, and scientific exploration. The government is investing heavily in modernizing launch facilities, such as Cape Canaveral and Vandenberg Space Force Base, to support the increasing volume and complexity of orbital launches. The U.S. market is projected to reach USD 69.22 billion by 2026.

Europe

In 2025, Europe represented USD 35.84 billion, accounting for 22.27% of the worldwide market, and is projected to grow to USD 38.86 billion in 2026. Europe is anticipated to have a significant market share during the forecast period, driven by growing investments in a wide range of applications, including Earth observation, telecommunications, and scientific research. The region has strong international partnerships and initiatives led by the European Space Agency (ESA). The ESA collaborates on major projects such as NASA's Artemis program and various lunar missions, enhancing Europe's capabilities in space infrastructure. The UK market is projected to reach USD 12.54 billion by 2026, while the Germany market is projected to reach USD 9.88 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 25.08 billion in 2025, representing 15.58% of the global market landscape, and is expected to reach USD 27.06 billion in 2026. Countries, such as China, India, and Japan are significantly investing in their space programs with ambitious goals for satellite deployment, lunar exploration, and commercial space activities. The region has seen a surge in private sector participation in space technology. Companies from Asia Pacific are increasingly involved in satellite manufacturing and launch services, capitalizing on the growing demand for connectivity and Earth observation data. This trend positions Asia Pacific as a key player in the global space economy. The Japan market is projected to reach USD 5.54 billion by 2026, the China market is projected to reach USD 12.3 billion by 2026, and the India market is projected to reach USD 3.07 billion by 2026.

Rest of the World

The market in Rest of the World reached USD 25.44 billion in 2025, representing 15.80% of total market revenue, and is projected to reach USD 26.99 billion in 2026. Regions outside North America, Europe, and Asia Pacific are gradually emerging as potential markets for space-based infrastructure. Countries in South America and parts of Africa have begun to invest in satellite technology primarily for telecommunications and Earth observation purposes. Government initiatives aimed at enhancing national capabilities in space technology are becoming more common in these regions. For instance, investments in satellite communications can help improve connectivity and support economic development efforts.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Players Are Focusing on Integrating Advanced Technologies to Gain Strong Foothold

The main participants in the space infrastructure market have experienced considerable growth in recent years as numerous players compete to take advantage of the increasing opportunities in space exploration, satellite communications, and other associated fields. Firms such as SpaceX have realized numerous milestones, including the creation of the Falcon 1, Falcon 9, Falcon Heavy rockets, and the Dragon spacecraft. SpaceX has profoundly altered the market by launching reusable rocket technology, reducing launch expenses, and creating new opportunities for commercial space endeavors.

LIST OF KEY SPACE INFRASTRUCTURE COMPANIES PROFILED

- Airbus SE (Netherlands)

- Astra Space Inc. (U.S.)

- Beijing Commsat Technology Development Co. Ltd. (China)

- Blue Origin LLC (U.S.)

- Boeing (U.S)

- China Aerospace Science and Technology Corporation (China)

- General Dynamics Corporation (U.S.)

- Hedron (U.K.)

- Hindustan Aeronautics Limited (India)

- Honeywell International Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025 – The Indian Space Research Organisation (ISRO) has commenced construction on its second spaceport in Kulasekarapattinam, Tamil Nadu, specifically designed for Small Satellite Launch Vehicle (SSLV) missions.

- August 2024 – BP America made a pact with NASA to collaborate on shared objectives in space exploration and energy generation. Under the terms of the agreement, both parties will exchange digital technologies and specialized knowledge gained from years of working in challenging conditions.

- June 2023 – Sierra Space, a prominent commercial space firm developing the inaugural comprehensive business and technology framework in space, received a Space Act Agreement (SAA) from NASA as part of the second Collaborations for Commercial Space Capabilities (CCSC-2) program.

- April 2023 – Northrop Grumman Corporation finalized the design of its Tranche 1 Transport Layer (T1TL), which is a component of the Space Development Agency's low-Earth orbit network. The objective was to create a device that relays essential information as required to safely and swiftly assist U.S. forces on the field efficiently and promptly.

- September 2022 – Space Foundation, a nonprofit advocacy group established in 1983 for the worldwide space ecosystem, and Singapore Space & Technology Limited (SSTL) recently entered into a Memorandum of Understanding aimed at enhancing collaborations in space science research, educational initiatives, innovation, and space-related endeavors.

REPORT COVERAGE

The global space infrastructure market research report outlines competitive dynamics by assessing business segments, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The report provides a detailed analysis of the market insights. It focuses on key aspects such as leading companies, applications, payload capacity, long-term and short-term contracts, and space launches. Besides this, the report offers insights into the market trends and supply chain trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the developed market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.00% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Component

|

|

By Application

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global market size was valued at USD 160.97 billion in 2025 and is anticipated to be USD 373.67 billion by 2034.

The market is likely to grow at a CAGR of 10.00% over the forecast period (2026-2034).

The top ten leading players in the industry are Airbus SE (Netherlands), Astra Space Inc. (U.S.), Beijing Commsat Technology Development Co. Ltd. (China), Blue Origin LLC (U.S.), Boeing (U.S), China Aerospace Science and Technology Corporation (China), General Dynamics Corporation (U.S.), Hedron (U.K.), Hindustan Aeronautics Limited (India), and Planet Labs (U.S.).

The U.S. dominated the market in 2025.

By application, the earth observation segment leads the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us