Space Militarization Market Size, Share, Russia Ukraine War & Industry Analysis, By Technology (Missile Defense Systems, Satellite Communication Systems, Surveillance & reconnaissance (ISR) systems, Space-based Missile Warning Systems, Directed-energy Weapons, and Anti-satellite (ASAT) Weapons), By Solution (Space Based, and Ground Based), By Architecture (Hardware, and Software), By Application (Surveillance & Reconnaissance, Navigation, Communication, Space Situational Awareness (SSA), Early Missile Warning, and Targeting & Weapon Guidance), By Platform, and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

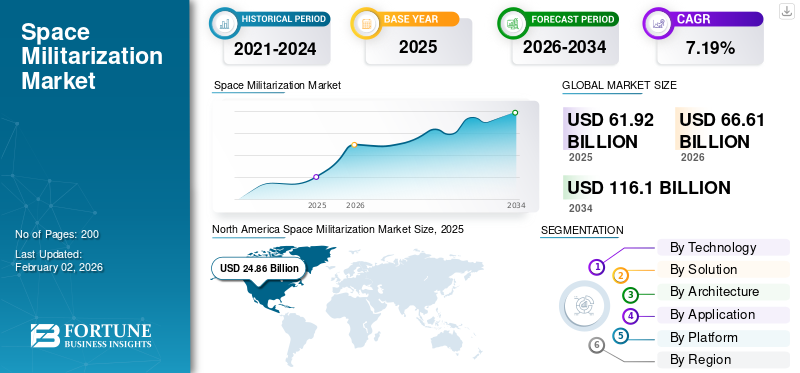

The global space militarization market size was valued at USD 61.92 billion in 2025 and is projected to grow from USD 66.61 billion in 2026 to USD 116.1 billion by 2034, exhibiting a CAGR of 7.19% during the forecast period. North America dominated the space militarization market with a market share of 40.15% in 2025.

Space militarization includes the deployment and use of space technologies for military applications such as reconnaissance, communications, navigation, and others. It involves satellites, ground systems, and related technologies for defense. Various countries in the world use space and counter space capabilities and regularly integrate them into military exercises. With space militarization, countries integrate space assets such as satellites, ground stations, and launch systems into defense operations. These factors are driving the overall market growth.

Furthermore, major players in the market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies, Airbus Defence and Space, and others. Lockheed Martin in the U.S. leads with advanced missile-warning satellites and secure communication platforms used by the U.S. Space Force. Boeing Defense, Space & Security provides military satellite buses, launch integration services, and protected communication systems for allied forces.

Download Free sample to learn more about this report.

SPACE MILITARIZATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 61.92 billion

- 2026 Market Size: USD 66.61 billion

- 2034 Forecast Market Size: USD 116.1 billion

- CAGR: 7.19% from 2026–2034

- North America dominated the space militarization market with a 40.15% share in 2025.

- The missile defense systems segment is projected to hold a 26.4% market share in 2026.

- The surveillance & reconnaissance applications segment is expected to account for 28.7% of the market in 2026.

North America

North America generated USD 24.86 billion in 2025 and is projected to reach USD 26.81 billion in 2026.

Europe

Europe generated USD 11.46 billion in 2025 and is projected to reach USD 12.16 billion in 2026.

Asia Pacific

Asia Pacific recorded USD 18.49 billion in revenue in 2025 and is expected to reach USD 20.08 billion in 2026.

U.S.

The U.S. space militarization market is projected to reach USD 24.05 billion by 2026.

Japan

Japan’s market is expected to reach USD 2.96 billion by 2026.

Read More

Impact of Russia Ukraine War

Russia Ukraine Was Has Led to Increase in Investments in Space Militarization

The Russia Ukraine conflict has significantly increased global investments in space militarization, as the war highlighted the critical role of satellites and space-based assets in modern warfare. Moreover, the reliance of Ukraine on commercial satellite constellations such as SpaceX’s Starlink for battlefield communications, real-time reconnaissance, and civilian infrastructure resilience increased and showcased the strategic importance of space systems.

The conflict also revived concerns about anti-satellite (ASAT) threats, as Russia conducted demonstrations of such capabilities in recent years, pushing the U.S., Europe, and Asia Pacific countries to strengthen defensive and deterrence mechanisms in orbit. Thus, this ongoing war has increased the significance of development of space military assets to improve defense capabilities and strengthen national security during war.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Geopolitical Rivalry and Security Threats Propels Market Growth

There is increasing geopolitical tension, rivalries and escalating security threats across the globe. This situation is expected to promote countries to strengthen space-based defense capabilities. Regional tensions such as India-Pakistan/China, Iran-Israel, North Korea and also push countries to develop space-enabled defenses such as missile warning and precision strike. Military forces of various nations require resilient satellites and space systems to maintain secure communications, surveillance, and navigation under hostile conditions. This demand drives procurement of hardened, redundant, and cyber-secure space infrastructure. Hence, these factors are contributing to the space militarization market growth.

- For instance, in July 2025, Chinese military and government researchers suggested active exploration of strategies to counter Elon Musk’s Starlink satellite network as it is observed as a critical U.S. military and intelligence asset.

MARKET RESTRAINTS

International Treaties and Legal Constraints to Restrict Market Expansion

The use of outer space technologies is regulated by a set of international law framework which focuses on peaceful use of space and bans weapons of mass destruction in orbit and space.

- For instance, the 1967 Outer Space Treaty (OST) treaty prohibits the establishment of mass destruction in outer space. Moreover, Partial Test Ban Treaty (1963) bans conducting tests of nuclear weapons in outer space.

The use of weapons that lead to mass destruction are not directly banned, but their over use is restricted under these laws. According to the treaty, placing nukes in orbit or on the Moon, establishing military bases on celestial bodies, and conducting military maneuvers in space that involve weapons for mass destruction are prohibited. The legal restrictions may limit the use and testing of space based military weapon systems as countries fear international sanctions and arms control response. Therefore, the international treaties and strict regulations regarding the use of outer space for destructive military weapons is expected to deter the market during the forecast period.

MARKET OPPORTUNITIES

Emergence of Allied and International Programs to Create Lucrative Growth Opportunities

With the security concern rising, there is an increase in the opportunity for allied programs where multiple countries contribute resources for shared capabilities. Various countries form different mechanisms and agreements to collaborate with allies on space operations and other activities.

- For instance, APSS, NATO's largest multinational investment in space-based capabilities was launched in 2023. It is NATO’s initiative for Alliance Persistent Surveillance from Space (APSS), which aims to have a consortium of members contributing satellites or data for collective use. In a similar manner, countries such as the U.S. are inviting partners (Japan, Canada, and others) into its combined missile warning and tracking architecture.

- Moreover, NATO’s STARLIFT initiative aims to strengthen and enable responsive space operations.

Such collaborations are expected to create opportunities for the development of military space systems. Moreover, partnerships between countries push the standardizing interfaces and data sharing among allied systems.

MARKET CHALLENGES

High Costs and Budget Constraints to Hamper Market Growth

The cost associated with space militarization is higher with programs that require large amounts of financial resources at every stage. Huge investment is required for development of advanced military satellites, space-based surveillance systems, and directed-energy other weapons. Such high costs present barriers for countries as it is difficult to manage defense spending priorities along with space capabilities expenditure. Moreover, countries with tight defense budgets cannot invest in space military systems due to their high cost. Therefore, such high cost and budget constraints restricts the pace of capability deployment in the market and creates a competitive disadvantage.

SPACE MILITARIZATION MARKET TRENDS

Adoption of LEO Constellations and Dual Use of Space Systems is a Significant Market Trends

Low Earth Orbit (LEO) satellite constellations is a critical system for civilian and defense end users owing to their low latency and global coverage. The surge in LEO deployments is driving demand for advanced anti-jamming, encryption, and space situational awareness systems. Moreover, the military sector across the globe is increasingly utilizing commercial LEO networks for various applications such as secure communications, reconnaissance, and rapid data transfer. Such dual-use approach in which civil or commercial space systems are shared for military purposes reduces costs and accelerates deployment timelines.

- For instance, SpaceX’s Starlink is a commercial satellite constellation. SpaceX developed Starshield specifically for U.S. government and defense use, building on the same core technology and manufacturing base as Starlink.

Moreover, there is a surge in the launch of space based systems that will serve both military and civilian organizations. Dual-use observation satellite systems designed for military and civilian purposes are gaining higher traction which is expected to propel the market growth.

For instance, in August 2025, SpaceX launched NAOS (National Advanced Optical System) which is expected to provide high-resolution optical imagery for military intelligence gathering, security, humanitarian efforts, as well as applications for NATO, EU, and the UN. Therefore, this trend is expected to reshape the market by combining commercial innovation and national defense infrastructure.

Download Free sample to learn more about this report.

Segmentation Analysis

By Technology

Increase in Investment in Small Satellite Constellations for Military Communication Contributes to Segmental Growth

On the basis of technology, the market is classified into missile defense systems, satellite communication systems, surveillance & reconnaissance (ISR) systems, space-based missile warning systems, directed-energy weapons, and anti-satellite (ASAT) weapons.

In 2026, the missile defense systems segment is projected to lead the market with a 26.4% share. Demand for missile defense systems is growing due to the increasing threat of ballistic and hypersonic missiles. Various countries are giving priority to space-based sensors and interceptors to detect and neutralize these potential threats. In addition, the continuous advancement in space-based missile warning and tracking technologies are improving the accuracy and responsiveness of missile defense networks.

- For instance, in May 2025, the Pentagon announced creation of its Golden Dome missile defense initiative, a large-scale program designed to establish a four-layer protection system against evolving missile threats. Valued at around USD 175 billion, the initiative aims to safeguard the continental U.S., Alaska, and Hawaii by using satellite-based sensing and interception technologies, in coordination with advanced ground interceptors, radar networks, and potentially directed-energy weapons.

Surveillance & reconnaissance (ISR) is expected to be the fastest growing segment in the market during the forecast period. Countries across the globe are investing heavily in development and deployment of ISR constellations to monitor rival satellite activity, track space debris, and detect hostile maneuvers. In addition, defense programs are increasingly funding advanced space surveillance and situational awareness projects to monitor orbital activities, detect threats, and secure critical space assets.

- For instance, in June 2025, the European Commission funded the SAURON project under the European Defense Industrial Development Program (EDIDP). It achieved its technical objectives in developing next-generation sensors for space surveillance and threat detection.

By Solution

Increase in Military Space Budget Fuels Growth of Space Based Segment

In terms of solution, the market is categorized into space based and ground based.

The space based segment is forecast to represent 56.49% of total market share in 2026. The space-based segment dominates the market and is the fastest growing segment due to their strategic importance in national defense. These systems offer continuous surveillance, communication, and early warning capabilities. Such systems are extremely necessary for modern military operations. The segment is growing due to advancements in satellite technology, increased defense budgets, and the rising need for secure and resilient communication systems.

- For instance, U.S. national security space spending increased to USD 49.58 billion in 2024, up from USD 45.98 billion in 2023. This represents a 56% increase since 2020, when spending was USD 27.7 billion.

By Architecture

Rise in Demand for Advanced Satellites, Sensors and Missile Defense Systems Supplemented Segment Growth

Based on architecture, the market is segmented into hardware and software.

The hardware segment is expected to hold a dominant position in 2026, accounting for a market share of 63.96%. Hardware components, including satellites, launch vehicles, and ground stations, constitute the largest share of the market. These hardware assets are essential for establishing and securing national security. Such hardware system are increasingly being used in various military applications such as reconnaissance, communication, and missile defense.

- For instance, in May 2025, Northrop Grumman invested USD 50 million in Firefly Aerospace to develop a new medium-lift launch vehicle called Eclipse, combining technologies from Northrop’s Antares and Firefly’s Alpha rockets. This vehicle is designed to support national security missions by deploying defense satellites.

The software segment is anticipated to be the fastest growing segment during the forecast period. Software solutions are the fastest-growing segment owing to the rise in complexity of space missions and the need for real-time data processing. Moreover, countries are backing innovations occurring in AI, machine learning, and cybersecurity which are expected to improve the capabilities of the space system. Such development encourages the creation of efficient operations and enhanced mission outcomes.

- For instance, in September 2025, the U.S. Space Force published its 2025 Data and Artificial Intelligence Strategic Action Plan which aims to enhance data-driven and AI-enabled capabilities to achieve space superiority.

By Application

Surge in Need for Secure & Reliable Military Satellite Communications Propels Segment Growth

Based on application, the market is segmented into surveillance & reconnaissance, navigation, communication, space situational awareness (SSA), missile defense & early warning, and others.

The surveillance & reconnaissance applications segment is expected to account for the largest share of 28.7% in the market in 2026, owing to increasing demand for real time intelligence and space monitoring. Moreover, the surge in hypersonic and long-range missile threats due to rising geopolitical tensions is encouraging the defense sector to develop and deploy more advanced ISR satellites which is expected to propel the growth of the segment.

- For instance, in April 2025, Umbra, a California-based manufacturer of synthetic aperture radar (SAR) satellites received a contract from the U.S. army to develop and supply next-generation sensor satellites for maritime surveillance.

In 2024, communication applications held the second largest share in the market, due to increasing need for secure and reliable communication channels in military operations. The military sector is required to ensure the integrity and functionality of communication satellites for coordinating defense activities and maintaining national security.

- For instance, in May 2025, the U.S. Army awarded a USD 640 million contract to SES Government Solutions to provide high-capacity, secure military satellite communications across multiple regions.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Increase in Deployment of Advanced Ground Based Systems for Space Monitoring Propels Segment Growth

Based on application, the market is segmented into ground-based systems, space-based systems, airborne systems, and naval (sea-based) systems.

In 2024, Space-based platforms held the largest share in the market due to their unparalleled ability to provide global surveillance and monitoring capabilities. Their strategic significance in national defense and space operations contributes to their dominant position.

- For instance, in June 2025, U.S. Space Development Agency (SDA) successfully launched the Dragoon satellite, the first of 12 experimental tactical communications satellites under the Tranche 1 Demonstration and Experimentation System (T1DES) program. Such development highlights the growing reliance on space based platforms, driving the segment growth.

Ground-based platforms are the fastest-growing segment, with projections indicating significant market expansion. This growth is attributed to the development of advanced ground-based sensors and tracking stations, which complement space-based systems and provide critical data for space situational awareness.

- For instance, in June 2025, Turion announced the operational readiness of its ground-based sensor node in California, designed for wide-area, dawn/dusk low Earth orbit space surveillance.

Space Militarization Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Space Militarization Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the dominant market share and is expanding rapidly. North America contributed approximately USD 24.86 billion to the global market in 2025, accounting for 40.15% share, and is expected to reach USD 26.81 billion in 2026. Governments of countries including the U.S. make huge investments in developing & designing of military satellites, space-based missile warning systems, and anti-satellite (ASAT) technologies with the help of the Department of Defense and the U.S. Space Force. Moreover, the presence of private key players such as Lockheed Martin, Northrop Grumman, Boeing, and others is expected to promote technological innovation and deployment of satellite constellations and defense payloads. The factors that are responsible for the growth of the market in the region are geopolitical concerns, particularly the need to counter space capabilities of other advanced countries such as China and Russia. The U.S. market is valued at USD 24.05 billion by 2026.

- For instance, in August 2025, Lockheed Martin completed successful testing of the first Next-Gen OPIR GEO missile warning satellite. The satellite is designed for surveillance and early warning of missile threats.

Europe

In 2025, the Europe market stood at USD 11.46 billion, representing 18.50% of global demand, and is projected to grow to USD 12.16 billion in 2026. Europe is anticipated to witness a notable growth during the forecast period. Countries across the region are investing in secure communications, ISR satellites, and missile defense capabilities. European companies such as Airbus Defence and Space, Thales Group, and Leonardo S.p.A. play a critical role in developing and providing technologically advanced satellite payloads and ground systems. Factors attributing to the growth of the market in the region are initiatives to reduce dependence of European countries on the U.S. and improve space defense capabilities. In addition, the surge in investment in space situational awareness, secure satellite communications, and dual-use technologies is increasing, thus driving the growth of the market in Europe. The UK market is valued at USD 3.84 billion by 2026, while the Germany market is valued at USD 2.23 billion by 2026.

- For instance, in May 2025, owing to increasing threat and innovation in defense & space technologies, European Investment Fund (EIF) announced investment of USD 46.6 million in Keen’s European Defence and Security Tech Fund for companies developing secure satellite communications, satellite image analysis, and defence of space assets.

Asia Pacific

The Asia Pacific region captured 2985.50% of the global market in 2025, generating USD 18.49 billion in revenue, and is projected to reach USD 20.08 billion in 2026. The Asia Pacific region is witnessing rapid growth in space militarization, driven primarily by China, India, Japan, and South Korea. China Aerospace Science and Technology Corporation (CASC) in China develops advanced ISR satellites, the Beidou navigation system, and ASAT programs which is driving the expansion of the market in the region. Moreover, countries such as India are focusing on enhancing defense capabilities with development of satellite-based surveillance systems. The Japan market is valued at USD 2.96 billion by 2026, the China market is valued at USD 8.25 billion by 2026, and the India market is valued at USD 5.2 billion by 2026.

- For instance, in June 2025, India accelerated the development of the launch of 52 dedicated military surveillance satellites under the USD 3.2 billion SBS-III program to enhance border and coastline monitoring.

Latin America and Middle East & Africa

During the forecast period, Latin America and Middle East & Africa regions would witness a moderate market growth. In 2025, Middle East & Africa generated USD 4.38 billion, contributing 7.07% to global market revenue, and is projected to grow to USD 4.68 billion in 2026. Latin America recorded a market size of USD 2.74 billion in 2025, capturing 4.42% of the global market share, and is projected to reach USD 2.88 billion in 2026. Governments in the region are investing in ISR satellites, secure communications, and early warning systems to strengthen national security and regional defense capabilities. In addition, the rise in strategic partnerships with other countries and regions such as the U.S., Europe, and Israel is expected to push the innovation and advancement of modern technologies and technical expertise. Market growth is driven by geopolitical security concerns, modernization of armed forces, and the development of indigenous satellite programs.

- For instance, in September 2025, Israel launched the Ofek 19 reconnaissance satellite to enhance its surveillance capabilities across the Middle East, including Iran and Yemen.

COMPETITIVE LANDSCAPE

Key Industry Players

Defense Investments, Satellite Programs and Government Contract with Defense Technology Providers Supports Expansion of Key Players

The global market is influenced by rising technological advancements and investments from both governmental and private sectors. Key players in this market include Lockheed Martin, Northrop Grumman, Airbus Defence and Space, Thales Alenia Space, and Boeing, and others each contributing through innovative solutions in satellite communications, missile defense systems, and space-based surveillance technologies.

Companies offer a range of products such as missile warning system, advanced satellite communications solutions and other space based defense technologies. Moreover, for market expansion the key players are investing in next-generation technologies, forming strategic partnerships, and enhancing interoperability among allied nations. Additionally, they are focusing on developing scalable and resilient space-based systems to meet the evolving demand of national security.

LIST OF KEY SPACE MILITARIZATION COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies Corporation (RTX) (U.S.)

- The Boeing Company (U.S.)

- Airbus SE (Airbus Defence and Space) (Netherlands)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems plc (UK)

- Thales Group (France)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- SAAB AB (Sweden)

- Leonardo S.p.A. (Italy)

- China Aerospace Science and Technology Corporation (CASC) (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Israel successfully launched the Ofek 19 reconnaissance satellite, enhancing its surveillance capabilities across the Middle East. It is equipped with synthetic aperture radar and high-resolution electro-optical imaging systems.

- September 2025: China showcased its full nuclear triad, including land, sea, and air-launched nuclear weapons, at a military parade marking the 80th anniversary of the end of World War II. The display featured advanced technologies such as hypersonic missiles, drone submarines, and autonomous robotic systems.

- September 2025: During its military parade, China unveiled the HQ-29 anti-satellite system, capable of targeting foreign satellites. The large size of the system suggests an extreme range, potentially similar to the U.S. Navy’s SM-3 Block IIA, and can be launched from land or ship.

- August 2024: The U.S. Space Force conducted its inaugural "Resolute Space 2025" exercise, simulating orbital warfare scenarios involving space electromagnetic warfare, space domain awareness, and navigational warfare.

- October 2024: Ministry of Defense of Russia announced the completion of the Mozhaets-6 military satellites, which are set to operate as part of the country's orbital squadron. These satellites are designed to enhance Russia's space surveillance and reconnaissance capabilities.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.19% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology · Missile Defense Systems · Satellite Communication Systems · Surveillance & reconnaissance (ISR) systems · Space-based Missile Warning Systems · Directed-energy Weapons · Anti-satellite (ASAT) weapons |

|

By Solution · Space Based o Satellites o Space Stations o Orbital Platforms o Space Based Sensors o Others · Ground Based o Ground Stations o Control Centers o Launch Facilities o Others |

|

|

By Architecture · Hardware · Software |

|

|

By Application · Surveillance & Reconnaissance · Navigation · Communication · Space Situational Awareness (SSA) · Early Missile Warning · Targeting & Weapon Guidance |

|

|

By Platform · Ground-based Systems · Space-based Systems · Airborne Systems · Naval (sea-based) Systems |

|

|

By Geography · North America (By Technology, By Solution, By Architecture, By Application, By Platform, and Country) o U.S. o Canada · Europe (By Technology, By Solution, By Architecture, By Application, By Platform, and Country) o U.K. o Germany o France o Italy o Rest of Europe · Asia Pacific (By Technology, By Solution, By Architecture, By Application, By Platform, and Country) o China o India o Japan o Australia o South Korea o Rest of Asia-Pacific · Latin America (By Technology, By Solution, By Architecture, By Application, By Platform, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Technology, By Solution, By Architecture, By Application, By Platform, and Country) o UAE o Saudi Arabia o Israel o South Africa · Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 61.92 billion in 2025 and is projected to reach USD 116.1 billion by 2034.

In 2025, the market value stood at USD 24.86 billion.

The market is expected to exhibit a CAGR of 7.19% during the forecast period of 2026-2034.

The space based segment led the market by solution.

The key factors driving the market are geopolitical rivalry and security threats and increase in demand for resilient space systems for military operations.

Lockheed Martin Corporation, Northrop Grumman, Raytheon Technologies, Boeing, and others are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us