Specialty Vehicle Market Size, Share & Industry Analysis, By Vehicle Category (Emergency & Public Safety Vehicles, Municipal & Sanitation Vehicles, Utility & Service Vehicles, & Others), By Application (Emergency Response & Healthcare, Municipal & Environmental Services, Utility Maintenance & Field Services, & Others), By Manufacturing Process (OEM-built Specialty Vehicles and Refurbished Specialty Vehicles), By Ownership (Private and Commercial), By Propulsion (ICE, Electric and Others), By Gross Value Weight (Light-duty, Medium-duty and Heavy-duty), and Regional Forecasts, 2026-2034

Specialty Vehicle Market Size and Future Outlook

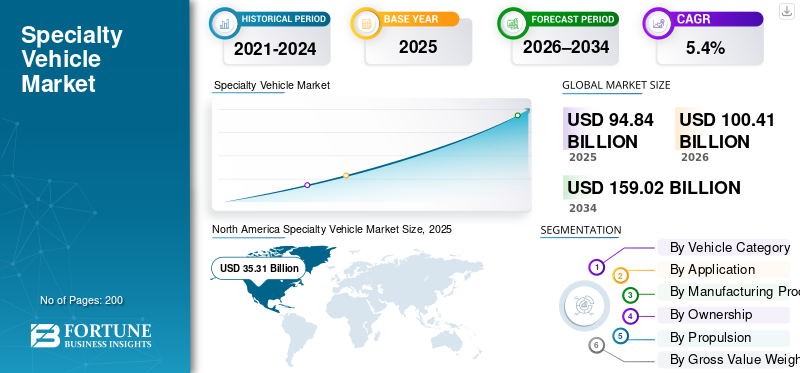

The global specialty vehicle market size was valued at USD 94.84 billion in 2025. The market is projected to grow from USD 100.41 billion in 2026 to USD 159.02 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. North America dominated the Specialty vehicle market with a market share of 37.23% in 2025.

The specialty vehicle market represents a distinct segment of the automotive industry focused on vehicles engineered for specific functional tasks rather than general transportation. These vehicles are purpose-built to support activities such as public safety, infrastructure maintenance, municipal services, logistics, and emergency response. Examples include fire truck platforms, utility service vehicles, ambulances, street sweeper units, mobile command vehicles, and certain types of recreational vehicle conversions.

The demand for specialty vehicles continues to rise as governments, municipalities, and private operators modernize fleets to improve operational efficiency, safety, and regulatory compliance. Urbanization, infrastructure expansion, and heightened emphasis on law enforcement and disaster preparedness are key factors contributing to the growing specialty vehicle market size. Additionally, industries such as utilities, telecommunications, and sanitation increasingly rely on customized vehicle platforms to support field operations.

During the forecast period, the market is projected to grow steadily due to replacement-driven demand, stricter emissions regulations, and ongoing technological advancement in vehicle design and onboard systems. The gradual integration of electric vehicle platforms is also reshaping procurement strategies, particularly for municipal and utility fleets, leading to rising interest in electric specialty vehicles for urban applications.

Applications across utility maintenance, environmental services, logistics, and emergency response are expected to remain central to market expansion. Growth is further supported by investments in fleet digitization, safety systems, and modular vehicle bodies that improve lifecycle value.

Leading manufacturers such as Oshkosh Corporation, REV Group, Rosenbauer, and other key player organizations are actively investing in new product development, electrification initiatives, and strategic partnerships to strengthen their global presence and address evolving customer requirements.

Download Free sample to learn more about this report.

SPECIALTY VEHICLE MARKET TRENDS

Integration of Advanced Technologies Enhances Specialty Vehicle Value

A major trend in the market is the integration of digital systems, telematics, and advanced safety features. Continuous technological advancement improves fleet efficiency, uptime, and operator safety, making specialty vehicles more attractive to buyers and supporting sustained market growth.

- For instance, Manufacturers are increasingly offering connected vehicle platforms for fleet monitoring.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Infrastructure Modernization and Public Safety Investments Accelerate Specialty Vehicle Adoption

Rising government spending on infrastructure and public safety is a major driver of the demand for specialty vehicles. Utility upgrades, sanitation programs, and enhanced emergency response capabilities require purpose-built fleets. Replacement of aging vehicles with technologically advanced models directly supports growth and increases the overall specialty vehicle market size.

- For instance, the U.S. Infrastructure Investment and Jobs Act allocates funding for municipal fleets and emergency services modernization.

MARKET RESTRAINTS

High Acquisition and Customization Costs Limit Market Penetration

Specialty vehicles involve complex engineering, custom bodywork, and advanced systems, resulting in higher upfront costs. Budget constraints among municipalities and smaller operators can delay procurement decisions, limiting short-term market expansion. These cost pressures particularly affect the adoption of newer technologies such as electric specialty vehicles.

MARKET OPPORTUNITIES

Electrification of Utility and Municipal Fleets Creates New Market Opportunity

The transition toward low-emission transport presents a strong market opportunity for manufacturers developing electric vehicle platforms for specialty use. Urban utilities, sanitation departments, and local governments increasingly favor electric solutions to meet sustainability goals, supporting long-term growth during the forecast period.

- For instance, Cities across Europe are piloting electric refuse and utility vehicles to reduce emissions.

MARKET CHALLENGES

Supply Chain Complexity Challenges Specialty Vehicle Manufacturing

Specialty vehicle production relies on multiple component suppliers and customized parts. Supply chain disruptions can delay deliveries and increase costs, negatively influencing market growth. Managing these complexities remains a challenge for manufacturers serving global markets.

For instance, automotive supply chain disruptions impacted specialty vehicle lead times during 2022–2023.

Segmentation Analysis

By Vehicle Category

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle category, the market is divided into emergency & public safety vehicles, municipal & sanitation vehicles, utility & service vehicles, specialty logistics vehicles, and others.

Utility & service vehicles dominate the global specialty vehicle market as they support essential activities such as power distribution, telecom maintenance, and water services. Continuous infrastructure upgrades, urban expansion, and rising demand for specialty vehicles from utilities drive consistent procurement. These vehicles offer high utilization rates and predictable replacement cycles, supporting long-term market stability.

- For instance, in December 2024, Avangrid announced it will purchase 130+ hybrid bucket trucks over three years to support utility operations and fleet electrification, underscoring sustained demand for utility specialty vehicles.

The utility & service vehicles segment is expected to grow at a CAGR of 6.7% over the forecast period.

By Application

Utility Maintenance and Field Services Lead Through Continuous Operational Demand

On the basis of application, the market is segmented into emergency response & healthcare, municipal & environmental services, utility maintenance & field services, specialty transportation & logistics and others.

Utility maintenance & field services dominate applications due to constant requirements for inspection, repair, and emergency restoration. Aging infrastructure, climate-related disruptions, and modernization programs increase reliance on specialized fleets. This application benefits from steady budgets and supports both ICE and electric specialty vehicles, reinforcing its leadership during the forecast period.

- For instance, in February 2024, Mack Trucks stated its MD Electric + Terex fully electric bucket truck targets utility fleet operations and will be available in limited quantities in 2025, showing ongoing fleet modernization activity.

Utility maintenance & field services are expected to grow at a CAGR of 7.0% over the forecast period.

By Manufacturing Process

OEM-Built Specialty Vehicles Dominate the Segmental Growth Due to Compliance and Reliability Advantages

On the basis of the manufacturing process, the market is segmented into OEM-built specialty vehicles and refurbished specialty vehicles.

OEM-built specialty vehicles dominate as buyers prioritize certified safety, durability, and regulatory compliance. OEM integration ensures optimized chassis-body compatibility, better warranties, and lifecycle support. Government agencies and private operators increasingly prefer OEM solutions over refurbished builds to reduce downtime and meet strict public safety standards.

- For instance, in December 2025, Pierce Manufacturing (an Oshkosh Corporation business) announced facility investments aimed at expanding production capacity and reducing lead times for fire apparatus, showing OEM demand and the need for scalable manufacturing.

The refurbished specialty vehicles segment is expected to grow at a CAGR of 6.5% over the forecast period.

By Ownership

Private Ownership Leads the Segment’s Growth Due to Utility and Industrial Fleet Expansion

On the basis of ownership, the market is segmented into private and commercial.

Private ownership dominates the market as utility contractors, logistics providers, and industrial service firms invest heavily in specialized fleets. Private operators emphasize productivity, fleet optimization, and return on investment, accelerating vehicle replacement and technology adoption. This trend supports growth across utility, logistics, and law enforcement support applications.

- For instance, in its 2024 annual report, Quanta Services notes it operates a fleet of owned and leased trucks plus specialty support equipment such as bucket trucks, highlighting the scale of private commercial ownership.

The private segment is expected to grow at a CAGR of 6.0% over the forecast period.

By Propulsion

ICE Vehicles Dominate Due to Proven Performance in Heavy-Duty Operations

On the basis of propulsion, the market is segmented into ICE, Electric, and others.

ICE-powered vehicles dominate the global specialty vehicle market because they offer high torque, extended range, and proven reliability for demanding applications. Many specialty uses, including emergency and sanitation services, still require ICE platforms. While electric vehicle adoption is rising, ICE remains essential for heavy-duty and remote operations.

- For instance, in February 2025, Mack Trucks said its fully electric bucket truck will be available in limited quantities in 2025, indicating EV specialty adoption is progressing but not yet replacing ICE at scale.

The electric segment is expected to grow at a CAGR of 11.3% over the forecast period.

By Gross Value Weight

Medium-Duty Vehicles Dominate by Balancing Payload and Efficiency

On the basis of gross value weight, the market is segmented into light-duty, medium-duty, and heavy-duty.

Medium-duty vehicles dominate as they provide an optimal balance between payload capacity, maneuverability, and operating cost. They are widely used across utility maintenance, sanitation, and emergency response applications. Their versatility makes them the preferred choice for both public and private fleet operators.

- For instance, in February 2025, Mack Trucks highlighted its MD Electric bucket truck built on a Class 6/7 medium-duty chassis with Terex equipment, reinforcing the role of medium-duty platforms in utility specialty applications.

Medium-duty segment is expected to grow at a CAGR of 7.3% over the forecast period.

Specialty Vehicle Market Regional Outlook

By region, the specialty vehicle market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Specialty Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 35.31 billion, and also maintained the leading share in 2024, with USD 33.75 billion. North America dominates the market due to strong investments in public safety, utility infrastructure, and fleet modernization. High replacement rates, strict safety regulations, and advanced manufacturing capabilities support regional leadership. The U.S. remains central, driven by sustained demand for fire truck fleets and emergency vehicles.

- For instance, in April 2024, Oracle expanded its U.S. TMS capabilities to support real-time logistics orchestration.

U.S. Specialty Vehicle Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 30.37 billion, representing roughly 32.0% of the market.

Asia Pacific

Asia Pacific is projected to record a growth rate of 6.6% in the coming years, which is the highest among all regions, and reach a valuation of USD 27.32 billion by 2026. The market in the Asia Pacific is projected to grow rapidly due to urbanization, infrastructure development, and expanding logistics networks. Governments are increasing investments in municipal and utility fleets, while manufacturing localization supports growth.

China Specialty Vehicle Market

China’s specialty vehicle market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 10.76 billion, representing roughly 11.3% of the market.

India Specialty Vehicle Market

India's specialty vehicle market in 2025 is estimated at around USD 4.10 billion, accounting for roughly 4.3% of market revenues.

Europe

Europe is estimated to reach USD 25.53 billion in 2026 and secure the position of the second-largest region in the market. Emissions regulations, sanitation modernization, and adoption of electric platforms drive Europe’s growth. Municipal and utility applications remain key contributors to regional expansion.

Germany Specialty Vehicle Market

Germany's specialty vehicle market in 2025 is estimated at around USD 5.80 billion, accounting for roughly 6.1% of global revenues.

U.K. Specialty Vehicle Market

The U.K. specialty vehicle market in 2025 is estimated at around USD 4.35 billion, accounting for roughly 4.6% of the global revenues.

Rest of the World

Growth in the Rest of the World is supported by infrastructure development, sanitation programs, and utility expansion, particularly in emerging economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation Shapes Competitive Specialty Vehicle Landscape

The competitive landscape of the specialty vehicle market is characterized by a mix of global manufacturers and regionally specialized players competing on customization capability, product reliability, and long-term service support. Market participants focus on delivering application-specific solutions tailored to public safety, utility operations, municipal services, and industrial logistics.

Key strategies adopted by manufacturers include portfolio diversification, expansion of modular vehicle platforms, and investments in advanced safety and digital systems. Companies are also prioritizing lifecycle services such as maintenance contracts and fleet management solutions to strengthen customer retention. The integration of electric specialty vehicles has become a differentiating factor, especially in regions with strict emissions regulations.

Mergers, acquisitions, and strategic collaborations are frequently used to enhance manufacturing capabilities and expand geographic reach. Many key player organizations are also increasing localized production to serve better regional demand in North America and the Asia Pacific.

- For instance, in January 2024, Oshkosh Corporation announced expanded electric vehicle development for vocational and specialty platforms, reinforcing its commitment to zero-emission fleet solutions.

LIST OF KEY SPECIALTY VEHICLE COMPANIES PROFILED

- Oshkosh Corporation (U.S.)

- REV Group (U.S.)

- Rosenbauer International (Austria)

- Daimler Truck AG (Germany)

- Volvo Group (Sweden)

- Iveco Group (Italy)

- PACCAR Inc. (U.S.)

- Tata Motors (India)

- Hyundai Motor Company (South Korea)

- Isuzu Motors (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Pierce Manufacturing announced major facility advancements and technology integration across its Appleton, Wisconsin operations as part of USD 150 million in manufacturing investments. The upgrades are aimed at expanding capacity and improving throughput to reduce delivery lead times for fire apparatus.

- October 2025: Volvo Trucks highlighted its expanded electric garbage truck lineup for waste management, positioning electrification as a strong fit for stop-start, short-route municipal collection. The company emphasized quiet operation and urban suitability as adoption accelerates among city fleets.

- July 2025: Oshkosh Defense (Oshkosh Corporation) reported receiving U.S. Army orders valued at USD 167 million for trucks and trailers under the Family of Heavy Tactical Vehicles contract. The announcement reinforces continued government procurement momentum for heavy-duty specialty and mission vehicles.

- April 2025: Volvo Trucks announced the sale of 35 electric trucks to PreZero, a waste-management company, to support operations such as refuse and related urban logistics. The deal signals growing fleet-scale electrification in municipal services and contractor-owned sanitation operations.

- April 2025: Rosenbauer America announced the delivery/deployment of its RTX electric fire apparatus to the Navajo Nation Department of Fire & Rescue Services. The release underscored active real-world adoption of battery-electric firefighting platforms by departments seeking lower emissions and modernized response capability.

- April 2025: REV Fire Group (REV Group) announced it would showcase 14 fire apparatus at FDIC 2025, including its Vector all-electric pumper. The company positioned the display as evidence of continuing electrification and product innovation in emergency specialty vehicles.

- February 2025: Mack Trucks announced its entry into the specialized utility segment with a Mack MD Electric + Terex Utilities fully electric bucket truck. The companies framed it as a milestone in zero-tailpipe-emissions solutions for field-service work, with limited availability timelines noted in supporting releases.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Category, Application, Manufacturing Process, Ownership, Propulsion, Gross Value Weight, and Region |

|

By Vehicle Category |

· Emergency & Public Safety Vehicles · Municipal & Sanitation Vehicles · Utility & Service Vehicles · Specialty Logistics Vehicles · Others |

|

By Application |

· Emergency Response & Healthcare · Municipal & Environmental Services · Utility Maintenance & Field Services · Specialty Transportation & Logistics · Others |

|

By Manufacturing Process |

· OEM-built Specialty Vehicles · Refurbished Specialty Vehicles |

|

By Ownership |

· Private · Commercial |

|

By Propulsion |

· ICE · Electric · Others |

|

By Gross Value Weight |

· Light-duty · Medium-duty · Heavy-duty |

|

By Region |

· North America (By Vehicle Category, Application, Manufacturing Process, Ownership, Propulsion, Gross Value Weight, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Category, Application, Manufacturing Process, Ownership, Propulsion, Gross Value Weight, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Category, Application, Manufacturing Process, Ownership, Propulsion, Gross Value Weight, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Category, Application, Manufacturing Process, Ownership, Propulsion, Gross Value Weight, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 94.84 billion in 2025 and is projected to reach USD 159.02 billion by 2034.

In 2025, the market value stood at USD 35.31 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

The Utility & service vehicles segment led the market by vehicle category.

Infrastructure modernization and public safety investments are driving the market.

Oshkosh Corporation, REV Group, Rosenbauer International, and Daimler Truck are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us