Hydrostatic Transmission Market Size, Share & Industry Analysis, By Transmission Type (Closed-Loop Hydrostatic Transmission and Open-Loop Hydrostatic Transmission), By Component (Hydraulic Pumps, Hydraulic Motors and Control & Auxiliary Components), By Power Output (Low Power (Up to ~30 kW), Medium Power (~30–100 kW) and High Power (Above ~100 kW)), By Application (Agricultural Machinery, Construction Equipment, Industrial & Material Handling Equipment, and Others), and Regional Forecast, 2026-2034.

KEY MARKET INSIGHTS

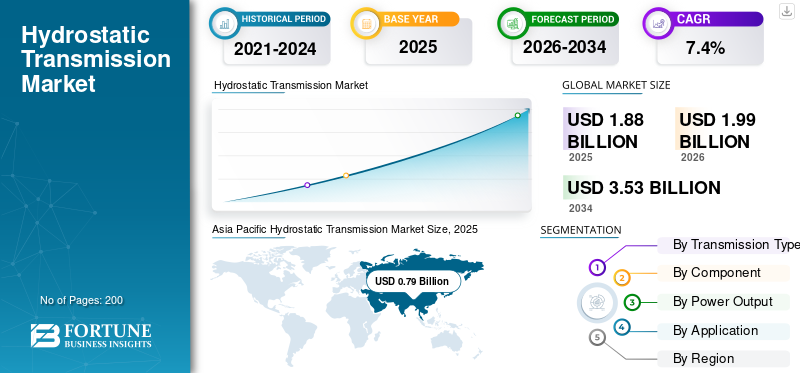

The global hydrostatic transmission market size was valued at USD 1.88 billion in 2025. The market is projected to grow from USD 1.99 billion in 2026 to USD 3.53 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period. Asia Pacific dominated the global market with a market share of 42.02% in 2025.

The market encompasses the global ecosystem of manufacturers, suppliers, and distributors engaged in the design, production, and commercialization of hydrostatic transmission systems that transmit power through pressurized hydraulic fluid rather than mechanical gearing. These systems are widely adopted in agricultural machinery, construction equipment, material handling equipment, and lawn and garden machinery due to their ability to deliver smooth, stepless speed variation, high torque at low speeds, and precise control. The market includes complete transmission units and key components such as hydraulic pumps, motors, valves, and control systems, and includes both OEM installations and aftermarket replacements and upgrades.

The market is characterized by the presence of established global players with strong engineering capabilities, broad product portfolios, and long-standing relationships with equipment manufacturers characterizes the market. Key market players focus on continuous product innovation, efficiency improvement, compact system design, and system integration with electronic and electro-hydraulic controls to address evolving end-user requirements and regulatory expectations.

Download Free sample to learn more about this report.

HYDROSTATIC TRANSMISSION MARKET TRENDS

Increasing Integration of Electro-Hydrostatic and Electronically Controlled Transmission Systems is One of the Significant Market Trends

The increasing integration of electro-hydrostatic and electronically controlled transmission systems is emerging as a prominent trend in the market. Equipment manufacturers are progressively incorporating electronic controls, sensors, and software-driven systems into hydrostatic transmissions to achieve higher precision, improved responsiveness, and enhanced operational efficiency. These advanced systems enable real-time adjustment of speed, torque, and load handling based on operating conditions, supporting automation and intelligent machine functions. Additionally, electronic integration facilitates compatibility with telematics, diagnostics, and advanced operator-assist features, which are becoming standard in modern agricultural and construction equipment. As end users increasingly demand smarter, more efficient, and easier-to-operate machinery, OEMs are increasingly adopting electro-hydrostatic solutions, positioning this trend as a key driver of technological differentiation and long-term market evolution.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Advanced Agricultural and Construction Machinery is Accelerating Market Growth

The increasing adoption of advanced agricultural and construction machinery is a key factor driving the growth of the market. As end-users focus on improving operational efficiency, productivity, and precision, the demand for modern equipment with enhanced controllability and ease of operation is rising. Hydrostatic transmission systems support these requirements by enabling smooth, variable-speed control, high torque at low speeds, and improved maneuverability, making them well-suited for technologically advanced machinery. As mechanization levels increase across both developed and emerging economies, OEMs are increasingly integrating the product into next-generation equipment, thereby accelerating the hydrostatic transmission market growth.

- For instance, in October 2025, Danfoss Power Solutions announced the launch of its Hybrid Load Control technology, designed to enhance hydrostatic propel performance in mobile machinery used in agriculture and construction. This development underscores the industry’s growing focus on advanced hydrostatic systems to meet evolving productivity and efficiency demands.

MARKET RESTRAINTS

Lower Overall Energy Efficiency in Certain High-Speed or Long-Duty Applications May Limit Market Growth

Lower overall energy efficiency in certain high-speed or long-duty applications is a key factor restraining the growth of the market. Unlike mechanical transmissions, hydrostatic systems experience inherent energy losses due to hydraulic fluid friction, leakage, and heat generation, particularly during prolonged operation at high speeds or under continuous heavy loads. These efficiency losses can lead to increased fuel consumption and higher operating costs, making hydrostatic transmissions less attractive for applications where energy efficiency is a key performance criterion. As end users in agriculture and construction increasingly prioritize fuel economy and reduced emissions, OEMs may prefer alternative transmission technologies for high-duty cycles. This limitation can restrict the adoption of hydrostatic systems in select heavy-duty and high-performance equipment segments, constraining overall market expansion.

MARKET OPPORTUNITIES

Rising Demand for Compact and Electric Off-Highway Equipment to Create Lucrative Growth Opportunities

Rising demand for compact and electric off-highway equipment is creating a strong growth opportunity for the market. Compact machinery used across agriculture, construction, and material handling requires precise speed control, smooth maneuverability, and flexible power management, all of which are key advantages of hydrostatic transmission systems. Additionally, the gradual electrification of off-highway equipment is encouraging the adoption of hydrostatic and electro-hydrostatic drivetrains, as these systems integrate efficiently with electric motors and advanced control systems. As manufacturers focus on developing smaller, energy-efficient, and low-emission machines to meet regulatory and operational requirements, hydrostatic transmissions are being favored for their design flexibility and controllability. This trend is expected to open new avenues for system suppliers and OEMs, supporting long-term market growth.

MARKET CHALLENGES

Meeting Stringent Emission and Energy-Efficiency Regulations Across Regions is a Challenging Factor for the Market

Meeting stringent emission and energy-efficiency regulations across regions represents a significant challenge for the market. Governments and regulatory bodies in North America, Europe, and parts of the Asia Pacific are enforcing stricter emission norms and fuel-efficiency standards for off-highway equipment, compelling manufacturers to reduce energy losses and overall system inefficiencies. Hydrostatic transmissions, which inherently experience hydraulic losses and heat generation, are subject to increased scrutiny under these regulations. As a result, OEMs and system suppliers must invest heavily in advanced materials, optimized hydraulic designs, and electronic control technologies to improve efficiency and compliance. These additional development and validation requirements can increase costs and extend product development cycles, creating challenges for manufacturers to balance regulatory compliance with performance targets and affordability expectations.

Segmentation Analysis

By Transmission Type

Closed-Loop Hydrostatic Transmission Segment to Dominate owing to Superior Control

Based on transmission type, the market is categorized into closed-loop and open-loop hydrostatic transmissions.

The closed-loop hydrostatic transmission segment is anticipated to account for the largest share of the market. This dominance is primarily attributed to the superior control, responsiveness, and efficiency offered by closed-loop systems compared to open-loop counterparts, particularly in variable-load and precision-driven applications. Closed-loop configurations provide continuous feedback between the hydraulic pump and motor, enabling precise torque control, reduced energy losses, and improved machine performance, which are critical performance for modern agricultural and construction equipment. Additionally, the growing integration of electronic controls and the demand for smoother variable-speed operation further strengthen the preference for closed-loop systems across OEMs and end-users.

By Component

Hydraulic Pumps Segment to Dominate due to its Critical Role in Power Generation

Based on component, the market is segmented into hydraulic pumps, hydraulic motors, and control & auxiliary components.

The hydraulic pumps segment is expected to dominate the market due to its critical role in power generation and flow regulation within hydrostatic systems. Hydraulic pumps form the core of hydrostatic transmissions, as they convert mechanical energy into hydraulic energy, directly influencing system efficiency, responsiveness, and torque delivery. The rising demand for high-performance and variable-displacement pumps, particularly axial piston pumps, across agricultural and construction machinery is a key factor supporting this segment’s dominance. Moreover, continuous advancements in pump design aimed at improving pressure handling, durability, and efficiency further strengthen adoption among OEMs.

The hydraulic motors segment is projected to grow at a CAGR of 7.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Power Output

Low-Power Segment to Lead owing to its Extensive Adoption in Compact and Light-Duty Equipment

Based on power output, the market is segmented into low power (up to 30 kW), medium power (30–100 kW), and high power (above 100 kW).

The low-power segment is expected to hold the largest hydrostatic transmission market share, driven by its extensive adoption in compact and light-duty equipment. Low-power hydrostatic transmissions are widely used in lawn and garden equipment, compact tractors, utility vehicles, and small construction machinery due to their ability to deliver smooth operation, precise speed control, and ease of handling. Additionally, the growing demand for compact and electrically powered off-highway equipment further supports the dominance of this segment, as low-power hydrostatic systems offer efficient integration with electric and hybrid drivetrains.

Medium Power (30–100 kW) is projected to grow at a CAGR of 7.9% over the forecast period.

By Application

Agricultural Machinery Segment to Lead due to Widespread Use of Hydrostatic Systems in Tractors

Based on application, the market is segmented into agricultural machinery, construction equipment, industrial & material handling equipment, and others.

The agricultural machinery segment is expected to dominate the market, driven by the widespread use of hydrostatic systems in tractors, harvesters, and other farm equipment. Hydrostatic transmissions offer key advantages, including smooth variable speed control, high torque at low speeds, and ease of operation, which are critical for agricultural applications that require frequent speed changes and precise maneuverability. The increasing adoption of advanced and compact agricultural machinery to improve productivity and reduce labor dependency further supports the strong demand for the product in this segment.

The Construction Equipment segment is projected to grow at a CAGR of 8.0% over the forecast period.

Hydrostatic Transmission Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Hydrostatic Transmission Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest market share and is expected to witness the fastest growth in the market, fueled by rapid agricultural mechanization, expanding construction activities, and increasing infrastructure investments. Emerging economies, such as China and India, are experiencing a rising demand for tractors, excavators, and compact construction equipment to support urbanization and agricultural productivity. Additionally, government initiatives promoting modern farming practices and equipment upgrades are accelerating the adoption of the product. The growing presence of regional OEMs, coupled with increasing manufacturing capacity and cost-competitive production, is further supporting market growth across the Asia Pacific region.

Europe

Europe represents a mature and technology-driven market for hydrostatic transmissions, supported by stringent emission regulations and a strong focus on energy efficiency and sustainability. Equipment manufacturers in the region increasingly adopt advanced hydrostatic and electronically controlled transmission systems to comply with regulatory standards while enhancing machine performance. The presence of leading hydraulic system suppliers and strong R&D capabilities further strengthens the market. Moreover, growing adoption of compact and electric off-highway equipment, particularly in Western Europe, is driving demand for efficient and flexible hydrostatic solutions, positioning Europe as a key contributor to market expansion.

North America

North America holds a significant share of the market, driven by the strong presence of advanced agricultural and construction equipment manufacturers and a high level of mechanization across various end-use sectors. The region benefits from early adoption of technologically advanced machinery, including compact tractors, skid-steer loaders, and lawn & garden equipment, where hydrostatic transmissions are widely used. Additionally, increasing emphasis on operator comfort, productivity, and automation supports the integration of electro-hydrostatic systems. Continuous investments in precision agriculture and infrastructure development, along with a well-established aftermarket ecosystem, further contribute to sustained market growth in North America.

Rest of the World

The Rest of the World region, including Latin America and the Middle East & Africa, is experiencing gradual growth in the market. The increasing adoption of mechanized agricultural equipment in Latin America and the rising number of infrastructure and construction projects in the Middle East are key growth drivers. In Africa, growing awareness of modern farming equipment and gradual improvements in agricultural productivity are supporting market expansion. However, cost sensitivity and limited access to advanced machinery may restrain rapid adoption. Despite this, improving economic conditions and expanding equipment fleets are expected to create steady growth opportunities over the forecast period.

COMPETITIVE LANDSCAPE

Competitive Analysis

Focus on Product Innovation and Electronic Controls by Key Players to Shorten OEM Development Cycles

The global market reflects a moderately consolidated competitive structure, supported by established hydraulics and drivetrain specialists such as Danfoss Power Solutions, Parker Hannifin, Bosch Rexroth, Eaton, Poclain Hydraulics, Bucher Hydraulics, Linde Hydraulics, Kawasaki Precision Machinery, Dana, and dedicated hydrostatic drive manufacturers such as Hydro-Gear (notably strong in outdoor power equipment drivetrains). Competitive positioning is largely shaped by technology depth and OEM alignment, with Major players prioritizing electro-hydrostatic integration, software-enabled control (traction/control logic), efficiency optimization, and modular architectures to shorten OEM development cycles and improve machine performance and drivability.

LIST OF KEY HYDROSTATIC TRANSMISSION MARKET COMPANIES PROFILED

- Eaton Corporation plc (U.S.)

- Parker Hannifin Corporation (U.S.)

- Dana Incorporated (U.S.)

- Danfoss / Sauer-Danfoss Inc. (Denmark)

- Bosch Rexroth AG (Germany)

- Linde Hydraulics GmbH & Co. KG (Germany)

- Hydro-Gear Corp. (U.S.)

- Tuff Torq Corporation (U.S.)

- Poclain Hydraulics (U.S.)

- Carraro Drive Tech (Italy)

KEY INDUSTRY DEVELOPMENTS

- February 2025- Poclain Hydraulics continued promoting its HEVO technology platform, which integrates high-pressure hydrostatic components and dual pressure distribution strategies to boost torque output by up to 30% while maximizing energy savings in demanding applications. This highlights innovation trends in hydrostatic transmission performance and efficiency.

- January 2025- Eaton expanded its focus on smart hydraulics and condition-monitoring technologies within its hydraulic systems portfolio, strengthening its position as one of the foremost suppliers of hydraulic and hydrostatic components. These advancements include digital diagnostic and energy-efficiency features designed to enhance reliability and lower lifecycle costs for off-highway equipment.

- October 2025- Bosch Rexroth continued to emphasize next-generation connected industrial hydraulics, integrating intelligent software and simulation tools into its hydraulic product suite to enhance performance benchmarking and future-proof solutions across mobile and industrial applications. These developments mark a push toward networked, software-enabled hydrostatic and hydraulic systems.

- December 2025- Parker Hannifin’s Hydraulic Systems Division reinforced its position as a leading provider of fully integrated hydraulic and electromechanical subsystems. The division continues to expand its portfolio of mobile and industrial hydraulics solutions designed for complex applications in off-highway, construction, and industrial equipment, reflecting ongoing demand for integrated hydrostatic and fluid power technologies.

- October 2025- Eaton introduced advanced condition-monitoring technologies within its hydraulic systems portfolio to provide predictive maintenance capabilities and enhanced operational reliability for hydrostatic transmission applications. This move reinforces Eaton’s strategy to integrate digital diagnostics and energy-efficiency enhancements into its core hydraulic solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.4% from 2025-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Transmission Type, By Component, By Power Output, By Application, and By Region |

|

By Transmission Type |

· Closed-Loop Hydrostatic Transmission · Open-Loop Hydrostatic Transmission |

|

By Component |

· Hydraulic Pumps · Hydraulic Motors · Control & Auxiliary Components |

|

By Power Output |

· Low Power (Up to ~30 kW) · Medium Power (~30–100 kW) · High Power (Above ~100 kW) |

|

By Application |

· Agricultural Machinery · Construction Equipment · Industrial & Material Handling Equipment · Others |

|

By Geography |

· North America (By Transmission Type, By Component, By Power Output, By Application, and by Country) o U.S. (By Transmission Type) o Canada (By Transmission Type) o Mexico (By Transmission Type) · Europe (By Transmission Type, By Component, By Power Output, By Application, and by Country) o Germany (By Transmission Type) o U.K. (By Transmission Type) o France (By Transmission Type) o Rest of Europe (By Transmission Type) · Asia Pacific (By Transmission Type, By Component, By Power Output, By Application, and by Country) o China (By Transmission Type) o Japan (By Transmission Type) o India (By Transmission Type) o Rest of Asia Pacific (By Transmission Type) · Rest of the World (By Transmission Type, By Component, By Power Output, By Application, and by Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.88 billion in 2025 and is projected to reach USD 3.53 billion by 2034.

In 2025, the market value stood at USD 0.79 billion.

The market is expected to exhibit a CAGR of 7.4% during the forecast period of 2026-2034

The agricultural machinery segment led the market by application.

Increasing adoption of advanced agricultural and construction machinery is the key factor driving the market growth.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us