Spectrometry Market Size, Share & Industry Analysis, By Component (Products {Instruments [Mass Spectrometers, Molecular Spectrometers, Atomic Spectrometers, and Others] and Consumables}, and Software & Services), By Type (Mass Spectrometry {MALDI–TOF, Quadrupole, Triple Quadrupole, Orbitrap, & Others}, Molecular Spectrometry {UV-Visible (UV-Vis) Spectroscopy, Near-Infrared Spectroscopy, Infrared Spectroscopy, and Others}, Atomic Spectrometry {Atomic Absorption Spectroscopy, Atomic Emission Spectroscopy, & Others}, and Others), By Application, By End User, and Regional Forecast, 2026-2034

Spectrometry Market Size and Future Outlook

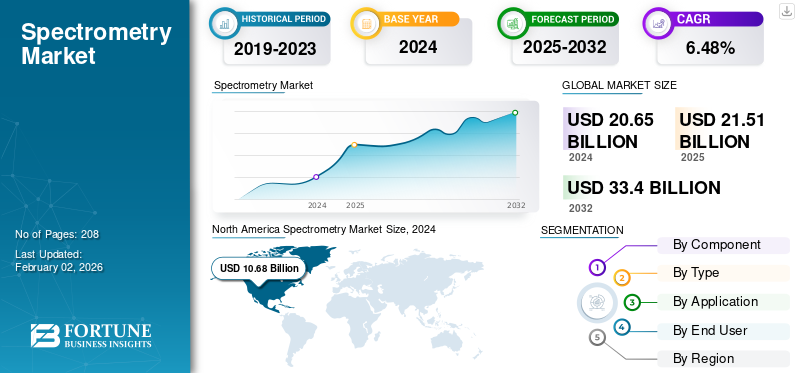

The global spectrometry market size was valued at USD 21.51 billion in 2025. The market is projected to grow from USD 22.51 billion in 2026 to USD 40.29 billion by 2034, exhibiting a CAGR of 7.55% during the forecast period. North America dominated the global spectrometry market with a market share of 51.82% in 2025.

Spectroscopy is used for analyzing protein and nucleic acid concentrations, verifying the purity of raw materials and products, and characterizing the structure, aggregation, and stability of drugs. The critical role of spectrometry in biotherapeutics and clinical diagnostics is anticipated to drive market growth. With the rapid growth of cell and gene therapies, mRNA, and complex protein therapeutics, there is a need for advanced tools to analyze large and heterogeneous drug modalities. Additionally, innovative product launches are expected to bridge these gaps, further supporting the market's growth.

- For instance, in October 2025, Waters Corporation launched Waters Xevo Charge Detection Mass Spectrometer (CDMS), designed to analyze a broad range of mega-mass biomolecules central to next-generation therapeutics and structural biology.

Key industry players, such as Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Shimadzu Corporation, Bruker, and PerkinElmer, are directing their investment toward innovative product launches, reinforcing their market presence and technological leadership.

Download Free sample to learn more about this report.

Spectrometry Market Key Takeaways

- 2025 Market Size: USD 21.51 billion

- 2026 Market Size: USD 22.51 billion

- 2034 Forecast Market Size: USD 40.29 billion

- CAGR: 7.55% from 2025–2032

- North America dominated the spectrometry market with a 51.82% share in 2025.

- The mass spectrometry (MS) segment is projected to account for a 41.31% market share in 2026.

- The pharmaceutical & biotechnology companies segment is projected to hold a 42.47% market share in 2026.

North America

North America dominated the market with a 51.82% share in 2025, reaching USD 11.15 billion and projected to grow to USD 11.69 billion in 2026.

Asia Pacific

Asia Pacific accounted for 15.92% of the global market in 2025, reaching USD 3.42 billion, and is expected to grow to USD 3.60 billion in 2026.

Europe

Europe captured 25.81% of the global market in 2025, generating USD 5.55 billion in revenue, and is projected to reach USD 5.80 billion in 2026.

U.S.

The market projected to reach USD 10.84 billion by 2026.

Japan

The market projected to reach USD 1.1 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Applications for Proteomics and Genomics to Drive Market Growth

Technological advancements in spectrometry are improving sensitivity and precision, allowing scientists to detect small molecules and subtle structural changes. This higher accuracy has enabled researchers to study low-level genes and proteins more effectively, thereby enhancing applications in genomics and proteomics.

Furthermore, as omics research expands, the demand for advanced laboratory instruments for better resolution and faster analysis continues to increase. This growing need encourages manufacturers to develop and launch innovative spectrometry products, which is driving the growth of the global spectrometry market.

- For instance, in June 2025, Thermo Fisher Scientific Inc. launched two new mass spectrometers, the Orbitrap Astral Zoom and the Orbitrap Excedion Pro, designed to advance research in proteomics, biopharmaceutical development, and the study of complex diseases.

MARKET RESTRAINTS

Shortages of Skilled Personnel to Restrict Market Growth

One of the key factors restraining market growth is the shortage of skilled lab technicians and trained personnel. This limits the ability of laboratories to use fully advanced spectrometry systems. Many instruments require specialized knowledge for operation, data analysis, and maintenance. This results in slower testing, increases workload for existing staff, and raises the risk of errors. As a result, the spectrometry market growth is hindered by the shortage of human expertise.

- For instance, in July 2024, Siemens Healthineers and The Harris Poll published a survey highlighting prolonged understaffing issues among clinical laboratory personnel.

MARKET OPPORTUNITIES

Increasing Demand for Precise Diagnostics Tests to Offer Lucrative Avenues for Market Growth

The increasing burden of various diseases and the growing demand for highly accurate and precise diagnostic tests, such as those for therapeutic drug monitoring, toxicology screens, and others, are offering significant avenues for market growth. These spectrometry instruments deliver quantitative precision and multiplexing, cutting turnaround time in laboratory settings. Recognizing these advantages, many key companies are directing their resources toward new product development for diagnostics, followed by approval from regulatory bodies.

- For instance, in December 2024, F. Hoffmann-La Roche received CE mark approval for its cobas Mass Spec solution, which includes the cobas i 601 analyser and the first Ionify reagent pack, featuring four assays for steroid hormones.

GLOBAL SPECTROMETRY MARKET TRENDS:

Shift toward Automation and AI Integration is a Prominent Market Trend Observed

A notable trend in the spectrometry market is the integration of artificial intelligence (AI) and automation to enhance data accuracy and streamline workflow. Spectrometers are being equipped with AI-driven software for automated peak detection, spectral interpretation, and real-time quality control. These capabilities support faster drug discovery and diagnostic testing while lowering operational costs. As a result, many key countries are investing heavily in AI-integration activities to maximize operational efficiency.

- For instance, in October 2025, HyperSpectral, an AI-powered spectral intelligence company, received USD 7.0 million in Series A-2 capital funding. The company’s platform combines chemical physics and materials-science-based spectroscopy with advanced AI algorithms trained for rapid, non-invasive detection of bacteriological pathogens without specialized lab preparation.

MARKET CHALLENGES

High Cost of Spectrometry Systems to Pose a Significant Challenge for the Small and Mid-Size Laboratories

The high cost of spectrometry systems poses a significant challenge for small and mid-sized laboratories. These instruments require substantial upfront investment, followed by recurring expenses for maintenance, calibration, and consumables. High ownership costs also delay instrument upgrades and inhibit smaller facilities from competing with well-funded research centers. As a result, the adoption of spectrometry technologies slows down, restricting overall market growth.

- For example, in July 2025, Rigaku Holdings Corporation reported that benchtop spectrometry systems can cost ranging from USD 30.0 million to USD 150.0 million. Such high prices can hinder the adoption of these spectrometry systems in mid-sized and small laboratories, posing a critical challenge to their adoption.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Increasing Product Launches Propelled Product Segment Growth

Based on component, the market is divided into products and software & services.

To know how our report can help streamline your business, Speak to Analyst

The product segment is projecteed to dominate the market with a share of 74.74% in 2026 due to the high prices of spectrometry equipment and the large volumes in which these systems are procured. With continuous advancements in technology and frequent equipment upgrades, the segment is poised to witness the largest contribution in the market. Additionally, growing research in pharmaceuticals, biotechnology, and clinical diagnostics increases the need for high-performance instruments, in turn driving the demand for products. Key companies are launching continuous product updates to provide innovative solutions, which further strengthen the market position of the segment.

- For instance, in August 2025, Horiba launched its Aqualog-Next A-TEEM Spectrometer. The flagship Aqualog platform of the company's spectrometer aimed to assist analysts working in water research and environmental analysis.

By Type

Various Advantages Associated with Mass Spectroscopy Led the Segment’s Growth

Based on type, the market is segmented into mass spectrometry (MS), molecular spectrometry, atomic spectrometry, and others.

The global spectrometry market was dominated by the mass spectrometry segment, primarily due to its superior sensitivity and accuracy in detecting and quantifying complex molecules. Its wide application in proteomics, metabolomics, clinical diagnostics, and food safety and environmental monitoring has strengthened the segment’s position, as it offers advantages over other methods, resulting in dominance of the segment. As a result, the segment is set to hold a 41.31% share of the market in 2026. Additionally, the development of hybrid systems, ion mobility, and high-resolution instruments has further accelerated segment performance. The technologically advanced product launches by key companies further boost the segment's growth.

- For example, in July 2025, SPECTRO launched the SPECTROGREEN MS, a cutting-edge quadrupole ICP mass spectrometer for high-performance, trace-level elemental analysis across various applications.

In addition, molecular spectrometry is projected to grow at a CAGR of 5.95% during the study period.

By Application

Heavy Reliance On Spectrometry Instruments Boosted the Drug Discovery & Development Segment Growth

Based on application, the market is segmented into drug discovery & development, proteomics & metabolomics, clinical chemistry & toxicology, pharmacokinetics/ADME studies, and others.

The drug discovery & development segment is projecteed to dominate the market with a share of 30.23% in 2026. The dominance of the segment can be attributed to heavy reliance on spectrometry instruments to identify and validate new drug molecules. Techniques, such as LC-MS and GC-MS, are essential for studying molecular structures, impurities, and metabolites during both preclinical and clinical phases. Moreover, the growing focus on precision medicine and quality control drives continuous investment in high-performance spectrometry systems for drug development and research, making this segment the largest in the market.

- For instance, in February 2022, the Biophysical Journal published the article ‘Raman spectro-microscopy to improve gene therapy vehicle design for CRISPR/Cas9 delivery’ reported how spectroscopy can be utilized to improve gene therapy vectors.

The proteomics & metabolomics segment is projected to grow at a CAGR of 8.52% during the study period.

By End User

High Throughput Utilization by Pharmaceutical & Biotechnology Companies Led the Segment Growth ‘s

On the basis of end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, clinical laboratories & diagnostic centers, and others.

The pharmaceutical & biotechnology companies segment is projecteed to dominate the market with a share of 42.47% in 2026. Spectrometry plays a key role in identifying active compounds, studying pharmacokinetics, which is critical for drug discoveries. These pharmaceutical and biotechnology companies are the epicenter that requires high-performance mass and molecular spectrometers, driving the growth of the segment.

For instance, in June 2025, SCIEX, in collaboration with Evosep Biosystems, expanded access to SCIEX mass spectrometry systems for the Pharmaceutical and biotech industries, enabling standardized high-throughput proteomics.

The clinical laboratories & diagnostic centers segment is projected to grow at a CAGR of 8.56% during the study period.

Spectrometry Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

In 2025, the North America market stood at USD 11.15 Billion, representing 51.82% of global demand, and is projected to grow to USD 11.69 Billion in 2026. The market in North America is poised for robust growth in the region due to the increasing prevalence of cardiovascular diseases, resulting in a large patient pool. Additionally, technological advancements and the rapid adoption of these advanced systems are expected to drive market growth in the region. Underscoring this growth opportunity, various companies are participating in strategic initiatives to expand product offerings. In 2025, the U.S. market is estimated to reach USD 10.84 billion by 2026 The U.S. is anticipated to witness market growth due to increasing research initiatives for proteomics and genomics and expanding applications of these spectrometry in clinical diagnostics.

North America Spectrometry Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- For instance, in June 2021, the U.S. National Science Foundation invested USD 40.0 million in advancing biomolecular research. The investment aimed to enable researchers to access ultra-high-field nuclear magnetic resonance spectrometers to study the structure, dynamics, and interactions of biological systems and small molecules. Such rising investment is driving growth in the region.

Europe

The Europe region captured 25.81% of the global market in 2025, generating USD 5.55 Billion in revenue, and is projected to reach USD 5.8 Billion in 2026. Market growth is supported by the introduction of supportive regulations aimed at enhancing drug quality standards, alongside increasing biopharmaceutical production and the expansion of proteomics and metabolomics research activities. The region’s well-established regulatory environment and strong presence of pharmaceutical and biotechnology companies continue to foster innovation and product development. Growing investments in advanced research infrastructure and analytical technologies further strengthen market demand. The U.K., Germany, and France are expected to remain key contributors, reaching market valuations of USD 1.34 billion, USD 1.21 billion by 2026 and USD 0.90 billion, respectively, in 2025.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 3.42 Billion in 2025, accounting for 15.92% share, and is expected to reach USD 3.6 Billion in 2026, making it the third-largest regional market globally. Growth is driven by rapid industrialization, increasing government funding for life sciences research, and rising investments by contract development and manufacturing organizations (CDMOs). The region is benefiting from expanding pharmaceutical manufacturing capabilities, improving healthcare infrastructure, and growing research activities across emerging economies. Supportive government initiatives and the increasing focus on biotechnology innovation continue to create favorable conditions for market expansion. The Japan market is valued at USD 1.10 billion by 2026, the China market is valued at USD 0.67 billion by 2026, and the India market is valued at USD 0.65 billion by 2026.

Latin America and the Middle East & Africa

The Middle East & Africa market accounted for USD 0.53 Billion in 2025, representing 2.45% of the global industry, and is expected to reach USD 0.54 Billion in 2026. In 2025, Latin America represented USD 0.86 Billion, accounting for 4.00% of the worldwide market, and is projected to grow to USD 0.89 Billion in 2026. Improving healthcare infrastructure, increased analytical testing capacity are anticipated to drive growth in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.25 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Acquisitions by Key Players Drives Competitive Landscape

The global spectrometry market has a semi-consolidated market structure, comprising prominent players such as Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Shimadzu Corporation, and Bruker. The significant share of these companies in the market is due to numerous strategic activities, such as new product launches, collaborations, and strategic acquisitions, which aim to expand their market presence.

- For instance, in November 2025, Veloxity Labs acquired the ZenoTOF 8600 mass spectrometer system from SCIEX. The development strengthened the company’s position while complementing its existing product offering in LC–MS/MS (triple quadrupole) platforms.

Other notable players in the global market include PerkinElmer, Waters Corporation, and JEOL Ltd. These companies are anticipated to prioritize new product launches and collaborations to boost their global spectrometry market share during the forecast period.

LIST OF KEY SPECTROMETRY COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Shimadzu Corporation (Japan)

- Bruker (Germany)

- PerkinElmer (U.S.)

- Waters Corporation (U.S.)

- JEOL Ltd. (Japan)

- Hitachi, Ltd. (Japan)

- Rigaku Holdings Corporation (Japan)

- HORIBA Group (Japan)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Bruker Corporation launched timsMetabo, a 4D metabolomics mass spectrometer with enhanced sensitivity, separation power, and annotation capabilities for small molecules.

- June 2024: BioPharmaSpec invested in instrumentation, including mass spectrometers, including Waters Select Series CYCLIC Ion Mobility Separation (IMS) High Definition LC-MS/MS with ECD, SCIEX ZenoTOF 7600 LC-MS/MS with EAD, Waters Xevo TQ Absolute, and Waters Xevo G3 LC-MS/MS Q-TOFs to support its clients in their product development goals.

- June 2024: Agilent Technologies Inc. launched its spectrometry products, namely the 7010D Triple Quadrupole GC/MS System, at a press conference during the ASMS Conference on Mass Spectrometry and Allied Topics.

- October 2023: Revvity, Inc. collaborated with SCIEX to advance its mass spectrometry solutions. The strategic collaboration combined Revvity’s expertise and resources with SCIEX’s innovative mass spectrometry solutions.

- August 2020: Shimadzu Corporation collaborated with HORIBA, Ltd, for the development and sales of LC-Raman analytical and measuring instruments that combine Shimadzu’s high-performance liquid chromatographs with HORIBA’s Raman spectrometers.

REPORT COVERAGE

The global market analysis provides a detailed study of the market size & forecast by all segments included in the report. The report also provides insights into market dynamics and trends, as well as opportunities expected to drive the market during the forecast period. The global report also includes an overview of technological advancements, strategic collaborations, key product launches, mergers & acquisitions, and key industry developments. The global market forecast also provides a detailed competitive landscape, including market share and profiles of major industry players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Attribute |

Details |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.55% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Type, Application, End User, and Region |

|

By Component |

Products

|

|

By Type |

Mass Spectrometry (MS)

Molecular Spectrometry

Atomic Emission Spectroscopy

|

|

By Application |

Drug Discovery & Development

|

|

By End User |

Pharmaceutical & Biotechnology Companies

|

|

By Geography |

North America (By Component, Type, Application, End User, and Country)

Europe (By Component, Type, Technology, End User, and Country/Sub-region)

Asia Pacific (By Component, Type, Application, End User, and Country/Sub-region)

Latin America (By Component, Type, Application, End User, and Country/Sub-region)

Middle East & Africa (By Component, Type, Application, End User, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights states that the global market value stood at USD 21.51 billion in 2025 and is projected to reach USD 40.29 billion by 2034.

In 2025, the market value stood at USD 11.15 billion.

The market is expected to exhibit a CAGR of 7.55% during the forecast period (2026-2034).

The product segment led the market in terms of components.

The expanding applications in proteomics and clinical diagnostics are key factors driving market growth

Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Shimadzu Corporation, and Bruker are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 208

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us