Stabilizer Bar, Bushings & Mounting Systems Market Size, Share & Industry Analysis, By Component Type (Stabilizer Bars (Anti-Roll Bars), Bushings, and Mounting Systems), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Sales Channel (OEM / Factory-Fit and Aftermarket / Replacement), By Material Type (Steel, Aluminum & Lightweight Alloys, and Elastomers & Composites), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

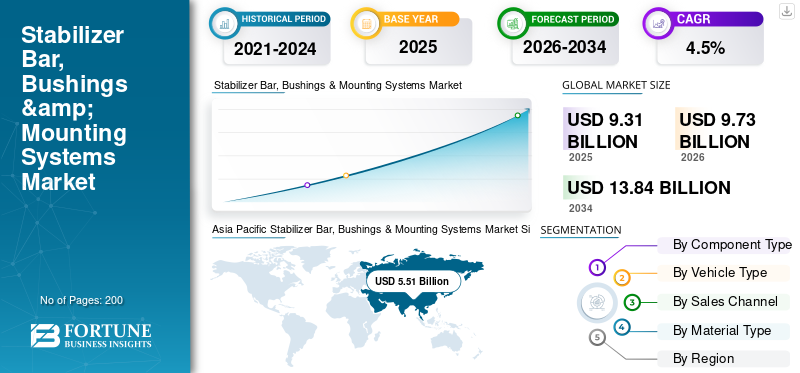

The global stabilizer bar, bushings & mounting systems market size was valued at USD 9.31 billion in 2025. The market is projected to grow from USD 9.73 billion in 2026 to USD 13.84 billion by 2034, exhibiting a CAGR of 4.5% during the forecast period. Asia Pacific dominated the global stabilizer bar, bushings & mounting systems market with a market share of 59.18% in 2025.

The growth of stabilizer bar, bushings & mounting systems market is driven by rising vehicle production, stricter expectations for improved handling stability and safety, and the continued expansion of the SUV/LCV mix, which increases stabilizer-system loading and bushing wear. OEMs increasingly prefer system-level sourcing (including bars, rubber bushings, and supports/mounts) from established Tier suppliers to reduce complexity, ensure NVH compliance, and improve packaging efficiency. Electrification is also influencing designs through the use of lightweight tubular bars, optimized mounts, and durability-focused elastomer materials to manage mass and noise. Manufacturers are investing in digital engineering and manufacturing feedback to raise productivity, predict fatigue life, and enhance consistency across global plants.

- For instance, in September 2025, NHK Spring presented its strategy briefing, highlighting DX initiatives to strengthen competitiveness, including product design methods and manufacturing feedback systems, which support the more efficient product development and manufacturability of components, such as stabilizer bars.

Download Free sample to learn more about this report.

STABILIZER BAR, BUSHINGS & MOUNTING SYSTEMS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 9.31 Billion

- 2026 Market Size: USD 9.73 Billion

- 2034 Forecast Market Size: USD 13.84 Billion

- CAGR: 4.5% from 2026–2034

- Asia Pacific dominated the market with a 59.18% share in 2025.

- The stabilizer bars segment accounted for the largest market share in 2025.

- The SUV segment is projected to grow at a CAGR of 6.3% during the forecast period.

North America

North America held a significant share, supported by SUV demand and a large aftermarket base.

Europe

Europe recorded steady growth due to safety regulations and rising aftermarket demand.

Asia Pacific

Asia Pacific led the market with a 59.18% share in 2025, driven by strong vehicle production.

U.S.

The market is driven by strong SUV and pickup sales and growing bushing replacement demand.

Japan

The market benefits from advanced suspension systems and increasing use of lightweight materials.

Read More

STABILIZER BAR, BUSHINGS & MOUNTING SYSTEMS MARKET TRENDS

Lightweight Suspension Engineering Gaining Momentum Across Vehicle Platforms Emerges as a Market Trend

Automotive manufacturers are increasingly prioritizing lightweight suspension components to meet fuel-efficiency targets and offset battery weight in electric vehicles. This trend is accelerating the adoption of hollow stabilizer bars, aluminum mounts, and optimized elastomer bushings that reduce mass while maintaining torsional stiffness and NVH performance. Lightweight solutions also support modular vehicle architectures, allowing OEMs to standardize components across platforms. As regulatory pressure on emissions and energy efficiency intensifies globally, suppliers investing in material innovation and structural optimization are gaining stronger OEM alignment and increased visibility in long-term programs. In May 2024, Hyundai Mobis announced the development of lightweight chassis and suspension components using optimized materials to support next-generation EV platforms.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Vehicle Production and SUV Penetration to Drive Market Growth

Growth in global vehicle production, particularly in SUVs and light commercial vehicles, continues to drive demand for stabilizer bar, bushings & mounting systems. SUVs require stronger and often thicker stabilizer systems to manage higher center-of-gravity dynamics, directly increasing component content per vehicle. Expanding vehicle assembly in Asia Pacific, Mexico, and Eastern Europe further supports OEM volumes, while higher vehicle parc sizes reinforce replacement demand for wear-prone bushings. This sustained production and mix shift provides a stable demand base for both OEM-supplied and aftermarket stabilizer system components. In January 2024, OICA reported global motor vehicle production exceeding 92 million units in 2023, with SUVs representing a growing share of output across major regions. This drives the stabilizer bar, bushings & mounting systems market growth.

MARKET RESTRAINTS

Cost Pressure from Raw Material Prices and Elastomer Volatility Limits Margins

Volatility in steel, aluminum, and synthetic rubber prices remains a key restraint for stabilizer bar and bushing manufacturers. These components are material-intensive, and sudden cost fluctuations can compress margins, particularly under fixed-price OEM supply contracts. Elastomer compounds used in bushings are also sensitive to oil-derived input costs and environmental compliance requirements, increasing formulation expenses. Smaller suppliers with limited pricing power face a greater risk to their profitability, while OEM cost-down expectations further constrain pass-through mechanisms, slowing investment capacity in certain regions.

MARKET OPPORTUNITIES

Aftermarket Replacement Demand Creates Long-Term Revenue Potential

The growing global vehicle parc and longer vehicle ownership cycles are creating significant growth opportunities in the aftermarket sectors, particularly for stabilizer bar, bushings & mounting systems that experience regular wear and tear. Harsh road conditions, increased SUV weight, and aging suspension systems all contribute to accelerating the replacement frequency, especially in emerging markets. Performance upgrades and preventive maintenance practices also support aftermarket sales. Suppliers with strong distribution networks, branded elastomer products, and regional manufacturing footprints are well-positioned to capture recurring revenue beyond initial vehicle production cycles. In October 2024, Tenneco highlighted increased aftermarket demand for chassis and suspension replacement components as vehicles age and maintenance intervals extend globally.

MARKET CHALLENGES

Design Complexity and NVH Expectations Increase Engineering Challenges

Meeting rising expectations for ride comfort, noise vibration and harshness NVH reduction, and durability across diverse vehicle platforms presents a significant engineering challenge. Stabilizer systems must strike a balance between stiffness and flexibility while integrating seamlessly with increasingly compact suspension layouts. Electric vehicles further intensify NVH sensitivity due to quieter powertrains, placing higher demands on bushing materials and mounting precision. Achieving consistent global quality while customizing designs for regional road conditions increases development time and validation costs, especially for suppliers serving multiple OEM platforms simultaneously.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component Type

Higher Structural Load Management Strengthens Stabilizer Bars Segment Leadership

Based on component type, the market is segmented into stabilizer bars (anti-roll bars), bushings, and mounting systems.

Stabilizer bars dominate the market due to their critical structural role in controlling body roll, improving vehicle stability, and ensuring safe handling across passenger and commercial vehicles. The increased production of passenger cars and light commercial vehicles has led to a rise in demand for thicker, hollow, and high-strength stabilizer bars that can handle higher center-of-gravity loads. Their higher material content and engineering complexity also translate into greater value contribution per vehicle compared to bushings or mounts.

- In March 2024, Mubea highlighted its stabilizer systems as a core product line, supporting global OEM platforms, and emphasized lightweight yet high-strength bar designs.

The bushings segment is projected to grow at a CAGR of 5.1% over the forecast period.

By Vehicle Type

Large Installed Base Keeps Hatchbacks & Sedans Segment Dominant

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

Hatchbacks & sedans continue to dominate the market due to their large global installed base, especially in the Asia Pacific and Europe regions. High production volumes and widespread fitment of stabilizer bars ensure sustained demand from both OEMs and the aftermarket.

SUVs are the fastest-growing segment, driven by consumer preference for higher ride height and utility, which increases the load on stabilizer systems and the value of components per vehicle. This shift significantly boosts demand for reinforced bars and durable bushings.

- In January 2024, OICA reported that global SUV production continued to rise as a share of total vehicle output, supporting increased demand for higher suspension systems.

The SUV segment is projected to grow at a CAGR of 6.3% over the forecast period.

By Sales Channel

Integral Suspension Installation and Platform Standardization Drives OEM/Factory-fit Segment Growth

Based on sales channel, the market is segmented into OEM/factory-fit and aftermarket/replacement.

OEM/factory-fit segment dominates the market as stabilizer bar, bushings, and mounting systems are integral suspension components installed during vehicle assembly. Demand closely tracks global vehicle production and platform standardization trends, favoring large Tier-1 suppliers that can deliver system-level solutions at scale. The aftermarket sector is the fastest growing, supported by aging vehicle fleets, increased SUV weight, and frequent bushing wear that drives regular replacement cycles.

- In October 2024, Tenneco stated that aging global vehicle fleets are driving higher aftermarket demand for chassis and suspension replacement components.

The aftermarket/replacement segment is projected to grow at the higher CAGR of 6.5% over the forecast period.

By Material Type

To know how our report can help streamline your business, Speak to Analyst

Steel Segment Dominates the Market Driven by its Superior Torsional Strength and Cost Efficiency

Based on material type, the market is segmented into steel, aluminum & lightweight alloys, and elastomers & composites.

Steel remains the dominant material due to its superior torsional strength, fatigue resistance, and cost efficiency in stabilizer bars and mounting brackets. However, aluminum and lightweight alloys are the fastest-growing segment as OEMs seek to reduce mass to meet emission norms and offset the weight of EV batteries. Adoption is particularly strong in premium vehicles and electric platforms, where lightweight suspension components contribute to efficiency and ride refinement.

- In April 2024, NHK Spring disclosed its focus on advanced materials and lightweight chassis components to support electrified vehicle platforms.

The aluminum & lightweight alloys segment is projected to grow at a CAGR of 7.8% over the forecast period.

STABILIZER BAR, BUSHINGS & MOUNTING SYSTEMS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

Asia Pacific Stabilizer Bar, Bushings & Mounting Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America displays steady growth supported by strong SUV and pickup truck penetration, higher suspension load requirements, and a mature aftermarket ecosystem. OEM demand is driven by platform renewals and localization of component sourcing, while aftermarket growth benefits from aging vehicle fleets and high annual mileage. The adoption of lightweight materials and performance-oriented suspension tuning further supports value growth. The region maintains stable demand across passenger vehicles and LCVs, with replacement bushings and mounting systems contributing significantly to recurring revenue. North America holds the largest stabilizer bar, bushings & mounting systems market share.

U.S.

The U.S. stabilizer bar, bushings & mounting systems market is driven by the dominance of SUV and pickup sales, increasing stabilizer system loads, and a large aging vehicle parc. Strong aftermarket penetration and frequent bushing replacement support sustained demand beyond OEM volumes.

Europe

Europe’s growth is shaped by stringent safety and emissions regulations, high expectations for ride comfort, and an aging vehicle fleet that supports aftermarket demand. OEM volumes are stable, with growing SUV penetration offsetting slower growth in hatchbacks. Electrification trends encourage lightweight stabilizer bars and advanced elastomer bushings to reduce NVH. Aftermarket demand increasingly outweighs OEM sales due to extended vehicle lifecycles, particularly in Western Europe, reinforcing long-term replacement-driven market expansion.

U.K.

The U.K. market benefits from a large in-use vehicle base and strong aftermarket activity. Rising SUV adoption and longer vehicle ownership cycles support consistent demand for stabilizer bushings and mounting components.

Germany

Germany remains a high-value market driven by premium vehicle production, advanced suspension engineering, and early adoption of lightweight stabilizer systems. Strong OEM integration and quality-focused aftermarket demand sustain growth.

Asia Pacific

Asia Pacific dominates global demand due to high vehicle production volumes across China, Japan, and India. This growth is fueled by rising SUV penetration, expanding middle-class vehicle ownership, and the continuous introduction of new OEM platforms. While OEM demand leads, aftermarket opportunities are expanding rapidly as vehicle parc sizes grow. Cost-efficient steel stabilizer bars dominate, but aluminum and advanced elastomer adoption are increasing, particularly in EVs and premium vehicles.

China

China leads the region with massive vehicle production, high SUV penetration, and rapid EV adoption. The demand is driven by OEM volumes and growing aftermarket replacement for bushings in high-usage urban vehicles.

Japan

Japan’s market is supported by advanced suspension engineering, consistent OEM output, and a mature aftermarket. Lightweight materials and durability-focused bushings are increasingly adopted for comfort and efficiency.

India

India is one of the fastest-growing markets, driven by rising SUV sales, an expanding vehicle parc, and improving road infrastructure. Both OEM demand and aftermarket replacement for bushings are increasing rapidly.

Rest of the World

The rest of the world region, encompassing Latin America, the Middle East, and Africa, exhibits moderate yet improving growth. Expanding vehicle assembly, rising motorization rates, and harsh road conditions drive demand for durable stabilizer systems and frequent bushing replacement. OEM demand remains dominant, and aftermarket growth is accelerating as vehicle parc sizes increase and maintenance awareness improves, supporting long-term stabilizer bar, bushings & mounting systems market expansion from a smaller base.

COMPETITIVE LANDSCAPE

Key Industry Players

Structural Engineering Excellence, Lightweighting Innovation, and Global OEM Integration Shape Stabilizer System Competitiveness

Strong engineering capabilities, material innovation, and deep integration with OEM suspension platforms define the global stabilizer bar, bushings & mounting systems market trends. Leading suppliers such as ZF, Mubea, NHK Spring, Sogefi, Tenneco, Benteler, and Rassini compete through high-strength stabilizer designs, advanced elastomer formulations, and lightweight mounting solutions that strike a balance between durability and NVH performance. Companies enhance their competitiveness by expanding their global manufacturing footprints, standardizing modular stabilizer systems, and investing in digital simulation for fatigue and noise optimization. Strategic collaborations with OEMs focus on platform-level suspension integration, electrification readiness, and localized production to reduce costs and supply-chain risk. In August 2025, NHK Spring highlighted investments in digital engineering and advanced material processing to enhance stabilizer system performance and global competitiveness.

LIST OF KEY STABILIZER BAR, BUSHINGS & MOUNTING SYSTEMS COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- thyssenkrupp Automotive Technology (Germany)

- Benteler International AG (Austria)

- Schaeffler AG (Germany)

- Dana Incorporated (U.S.)

- Tenneco Inc. (U.S.)

- Mubea – Muhr und Bender KG (Germany)

- NHK Spring Co., Ltd. (Japan)

- Sogefi S.p.A. (Italy)

- Aisin Corporation (Japan)

- Sumitomo Riko Company Limited (Japan)

- Toyoda Gosei Co., Ltd. (Japan)

- Chuo Spring Co., Ltd. (Japan)

- Hitachi Astemo, Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, the U.S. Defense Logistics Agency posted a procurement for an NSN BAR, STABILIZER under a set-aside solicitation, indicating continued institutional demand for stabilizer-bar components in fleet sustainment supply chains. Such tenders/awards are a visible signal of ongoing replacement demand beyond passenger-car OEM cycles.

- In October 2025, Continental’s ContiTech aftermarket business announced a major product portfolio expansion for chassis and steering spare parts, including over 1,000 new items in 2025, as well as the planned addition of 27 new hydraulic bushings at the beginning of the year. The program supports broader coverage of Europe’s passenger-car parc, including EVs.

- In August 2025, News industry reporting highlighted global innovations in stabilizer bar technology, including the use of lightweight materials and electronically controlled systems, signaling an accelerated evolution in suspension control and performance across various vehicle platforms.

- In June 2025, News, thyssenkrupp Automotive Technology announced a major realignment to create focused business units, including springs & stabilizers, aiming to boost customer focus, profitability, and potential future partnerships in stabilizer bar supply and aftermarket services.

- In May 2025, NHK Spring announced the expansion of its joint development efforts with automotive OEMs by integrating stabilizer bar design with springs and seats, leveraging its unique engineering ecosystem to improve ride comfort and EV compatibility through enhanced R&D and set-based design approaches.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component Type, By Vehicle Type, By Sales Channel, By Material Type, and By Region. |

|

By Component Type |

· Stabilizer Bars (Anti-Roll Bars) · Bushings · Mounting Systems |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Sales Channel |

· OEM / Factory-Fit · Aftermarket / Replacement |

|

By Material Type |

· Steel · Aluminum & Lightweight Alloys · Elastomers & Composites |

|

By Geography |

· North America (By Component Type, By Vehicle Type, By Sales Channel, By Material Type, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Component Type, By Vehicle Type, By Sales Channel, By Material Type, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Component Type, By Vehicle Type, By Sales Channel, By Material Type, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World ( By Component Type, By Vehicle Type, By Sales Channel, and By Material Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.31 billion in 2025 and is projected to reach USD 13.84 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 5.51 billion.

The market is expected to grow at a CAGR of 4.5% during the forecast period of 2026-2034.

The OEM/Factory-Fit segment led the market by sales channel.

Rising global vehicle production and the increasing penetration of SUVs are the key factors driving the market.

Key players in the market include ZF Friedrichshafen AG, Schaeffler Group, Benteler International AG, Magna International Inc., and American Axle & Manufacturing Holdings, Inc.

Asia Pacific accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us