Stem Cell Banking Market Size, Share & Industry Analysis By Cell Type (Peripheral Blood Stem Cells, Bone Marrow Cells, Adipose Tissue-Derived Stem Cells, CB/CT Derived Stem Cells, and Others), By Service Type (Sample Preservation and Storage, Sample Analysis, Sample Processing, and Sample Collection and Transportation), By Bank Type (Public, Private, and Hybrid), By Application (Research Applications, Clinical Applications, and Personalized Banking Applications), and Regional Forecast, 2026-2034

Stem Cell Banking Market Size and Industry outlook

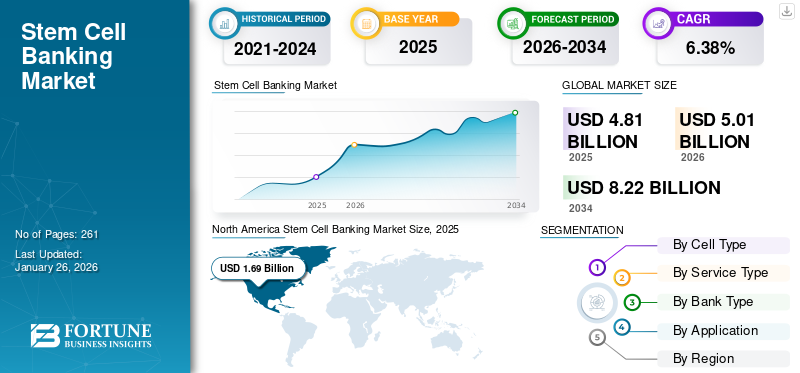

The global stem cell banking market size was valued at USD 4.81 billion in 2025 and is projected to grow from USD 5.01 billion in 2026 to USD 8.22 billion by 2034, exhibiting a CAGR of 6.38% during the forecast period. North America dominated the stem cell banking market with a market share of 35.16% in 2025.

Stem cell banking refers to the process of collecting, processing, and storing stem cells for potential future medical use. The growing prevalence of chronic conditions, including genetic diseases, cancer, cardiovascular disorders, and others resulting in the rising demand for advanced therapies globally. This, along with improvement in stem cell collection, processing, and storage technology, is further supporting the annual collections of stem cells, thereby contributing to the growth of the market.

- For instance, according to 2025 data published by the American Cancer Society (ACS), approximately 2.0 million new cancer cases are projected to occur in the U.S.

Moreover, the increasing initiatives toward improving healthcare infrastructure and R&D funding among governmental organizations and non-governmental organizations, coupled with an improving regulatory framework, are likely to create a favorable environment for banking of stem cells in the market. Furthermore, increasing emphasis on expansion of stem cell applications, such as personalized banking applications and others, among the key companies, such as Cordlife, CBR Systems, Inc., and others, is expected to support the global market growth.

Download Free sample to learn more about this report.

Stem Cell Banking Market Key Takeaways

- 2025 Market Size: USD 4.81 billion

- 2026 Market Size: USD 5.01 billion

- 2034 Forecast Market Size: USD 8.22 billion

- CAGR: 6.38% from 2026–2034

- North America dominated the stem cell banking market with a 35.16% share in 2025.

- The CB/CT-derived stem cells segment held the largest market share of 59.98% in 2026.

- The private banking segment accounted for 63.95% of the market share in 2026.

North America

North America led the global market with USD 1.69 billion in revenue in 2025 and is projected to reach USD 1.77 billion in 2026.

Europe

Europe accounted for 32.07% of the global market in 2025 and is expected to reach USD 1.61 billion in 2026.

Asia Pacific

Asia Pacific was the third-largest regional market, reaching USD 1.23 billion in 2025.

U.S.

The stem cell banking market is estimated to reach USD 1.63 billion by 2026.

Japan

The market is supported by increasing adoption of regenerative medicine and stem cell research initiatives.

Read More

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Diseases to Fuel Market Growth

The growing prevalence of chronic conditions, including genetic disorders, diabetes, cancer, metabolic disorders, and others among the patient population, is resulting in a growing patient pool for stem cell transplantations, subsequently boosting the annual collections of these cells in stem cell banks.

- For instance, according to 2025 data published by the American Society of Hematology, it was reported that approximately 70,000 to 100,000 Americans have sickle cell disease in the U.S.

Additionally, the increasing number of registries of cord blood units and adult donors among the national inventories is also a major contributing factor in improving match rates for patients, especially underrepresented groups. Moreover, increasing awareness about the benefits of biological insurance among families also supports cell banking at birth, further fueling the number of annual collections in the market.

Therefore, the growing prevalence of chronic conditions, coupled with the increasing advancements in stem cell collection, processing storage technology, is expected to drive the adoption rate, thereby contributing to the global stem cell banking market growth.

Other Prominent Drivers

- Growing awareness of regenerative medicine and the therapeutic potential of stem cells

- Rising maternal healthcare awareness and newborn screening programs promoting cord blood/tissue banking

- Investments in biobanking infrastructure, cold-chain logistics, and laboratory automation enhance service capabilities

- Private–public partnerships and government support for biobanking and stem cell research in several countries

Market Restraints

High Cost Associated with Cell Banking to Hamper the Market Growth

There is an increasing awareness and demand for banking of stem cells for potential future use. However, the high cost associated with collecting, processing, and storing these cells is expected to hinder the demand and adoption of this technique.

The banking of these cells requires cryogenic preservation systems, regulatory-grade laboratory infrastructure, and sterile logistics, which are capital-intensive and often necessitate continuous monitoring to maintain cell viability. The sample collection and processing demands advanced expertise among professionals and involves GMP-compliant clean rooms, redundant storage systems, and real-time temperature monitoring, which subsequently increases operational expenditure. The surging operational expenditure further adds to rising upfront costs and annual storage charges, making it difficult to adopt this technique, especially in low- and middle-income countries.

- For instance, according to data published by Cord Blood Banking in 2025, the upfront collection and processing costs range from USD 1,675 to USD 2,820 in the U.S.

Additionally, the high cost associated with importing cryogenic materials, limited cold-chain infrastructure, and inadequate reimbursement policies in emerging nations also limit the adoption rate of these techniques.

Therefore, all the above-mentioned factors are primarily responsible for the limited demand and adoption rate for these cell banking, further anticipated to hinder the market growth.

Market Opportunities

Expansion of Stem Cells Applications to Create Market Opportunities

The widening of the application spectrum for stored stem cells is presenting a lucrative opportunity, shaping the cell banking industry. The biological benefits of stem cells, including their ability to differentiate into various cell types, have enabled their clinical use in emerging therapies for conditions such as myocardial infarction, spinal cord injuries, and liver cirrhosis, among others, within the patient population. As these therapeutic applications expand, the demand for well-characterized, high-quality stem cell lines has increased.

Moreover, there is an increasing demand for cell-based and regenerative therapies, which has led to a rise in the number of stem cell clinical trials involving embryonic, induced, and cord-blood-derived stem cell lines. Additionally, integrating genetic technologies such as CRISPR-CAS9 and stem cell research is likely to widen the potential of allogenic and autologous applications, increasing the demand for storage services among the large and diverse cell banks globally.

- According to data published by Elsevier Inc. in 2025, approximately 115 clinical trials involving human pluripotent stem cells are currently underway worldwide.

Market Challenges

Regulatory & Ethical Considerations to Limit the Market Growth

There is an increasing R&D funding initiatives among governmental and non-governmental organizations to improve banking applications. However, despite the efforts of these organizations, the regulatory and ethical complexity remains one of the crucial challenges limiting the penetration rate of cell banking in the market.

The complex and varied regulatory framework for cell collection, processing, testing, and storage makes cross-border exchanges of these a challenging task. In the U.S., cord blood banks must comply with FDA regulations and Foundation for the Accreditation of Cellular Therapy (FACT) accreditation standards to qualify for therapeutic use. Similarly, the European Tissue and Cells Directive and other national competent authorities impose stringent GMP compliance requirements for stem cells.

Ethical concerns associated with using fetal and embryonic stem cells continue to generate policy restrictions that further affect research and development funding. Therefore, all the above-mentioned factors, coupled with regulatory lag in approval for new stem cell-based therapies, especially in emerging nations, are anticipated to limit the market growth.

- For instance, according to 2025 data published by Springer Nature, countries with stringent stem cell research regulations, such as Germany, France, and others, conducted fewer stem cell clinical trials than other countries.

Stem Cell Banking Market Trends

Increasing Demand for Personalized Banking of Stem Cells

There is a growing awareness and preference toward personalized medicines among individuals and families, thereby augmenting the demand for biological insurance for its potential future use. The benefits of biological insurance, including safety, reduced risk of immune rejection, and maximum compatibility for future therapies, enhance the demand for personalized banking applications for these stem cells globally.

Furthermore, stem cell banks are offering customized services, tailored storage plans, and expanded source types for these cells to the general population. This, along with the advancement of technologies for collecting, processing, and storing these stem cells, is expected to further increase the number of annual collections in public and private stem cell banks worldwide.

- According to 2024 statistics published by Consumer Affairs, it was reported that about 4 million cord blood units were stored in private banks globally.

Other Prominent Trends

- Consolidation and M&A activity among regional banks and global service providers.

- Technological improvements in cryopreservation, automated storage, and sample tracking systems.

- Growth of direct-to-consumer and online enrollment models for private banking.

- Increasing collaboration between hospitals, diagnostic labs, and biobanks to streamline collection and storage.

Download Free sample to learn more about this report.

STEAM CELL BANKING MARKET SEGMENTATION ANALYSIS

By Cell Type

Increasing Storage of CB/CT Units to Boost CB/CT-Derived Stem Cells Segment

Based on cell type, the market is classified into peripheral blood stem cells, bone marrow cells, adipose tissue-derived stem cells, CB/CT-derived stem cells, and others.

To know how our report can help streamline your business, Speak to Analyst

The CB/CT-derived stem cells segment held the largest share 59.98% of the global stem cell banking market in 2026. The growth is attributed to the increasing prevalence of chronic disorders, including genetic disorders, cancer, and others, among the patient population, leading to a growing annual collection of stem cells, such as CB/CT-derived stem cells, globally. This, along with the growing number of key companies offering expanded applications and personalized plans for stem cell storage, is likely to further support segmental growth.

- According to 2020 statistics published by Nature, it was reported that about 800,000 cord blood units were stored in public banks globally.

The adipose tissue-derived stem cells segment is expected to grow at a CAGR of 6.6% over the forecast period.

By Service Type

Growing Number of Clinical Trials Led to the Dominance of the Sample Preservation and Storage Segment

Based on service type, the market is divided into sample preservation and storage, sample analysis, sample processing, and sample collection and transportation.

The sample preservation and storage segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 42.16% share. The dominant share is attributed to the increasing number of clinical trials that require preserved stem cells owing to their use in advanced cell-based therapies, regenerative medicine, and other applications. This, coupled with rising preference toward multi-source and multi-generation preservation, offers storage for various stem cells, such as adipose tissue-derived stem cells, among others.

- For instance, according to data published by Cells4Life Group LLP in 2025, it was reported that approximately 7,600 clinical trials are being conducted among stem cell researchers to investigate the application of stem cell treatments for various conditions globally.

The sample processing segment is expected to grow at a CAGR of 6.2% over the forecast period.

By Bank Type

Increasing Cord Blood Units Storage Led to the Dominance of the Private Segment

Based on bank type, the market is segmented into private, public, and hybrid.

The private segment dominated the global market in 2025. By application, the private segment held the share of 63.95% in 2026. The growth is primarily driven by the increasing prevalence of chronic disorders, including genetic diseases and cardiovascular disorders, resulting in a growing number of annual collections in private stem cell banks globally.

- For instance, according to data published by the Cord Blood Banking Guide in 2021, approximately 500,000 cord blood units were stored in private banks in the U.S.

The hybrid segment is set to flourish with a growth rate of 6.9% over the forecast period.

By Application

Increasing Awareness of Biological Insurance Led to the Personalized Banking Applications Segment’s Dominance

Based on application, the market is segmented into research applications, clinical applications, and personalized banking applications.

The personalized banking applications segment dominated the market in 2025. The increasing preference for personalized medicine, growing therapeutic capabilities, and rising awareness of biological insurance, among others, are some of the crucial factors supporting the segment's growth in the market. Furthermore, the segment is set to hold a 56.16% share in 2026.

- For instance, according to 2021 statistics published by Consumer Affairs, it was reported that over 3.7 million children born chose to bank cord blood units in a private or a public bank in the U.S.

In addition, the research applications segment is projected to grow at a CAGR of 6.1% during the forecast period.

Stem Cell Banking Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Stem Cell Banking Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 1.69 billion in 2025, representing 35.16% of the global industry, and is expected to reach USD 1.77 billion in 2026. The region's dominance is due to certain factors, including increasing prevalence of chronic diseases, growing technological advancements in the stem cell collection, processing, and storage systems, high healthcare expenditure, established private banking structure, increasing number of stem cell collections among these banks, among others. In 2025, the U.S. market is estimated to reach USD 1.63 billion.

- For instance, according to 2021 data published by the Cord Blood Banking Guide, about 30,000 new collections are privately banked annually in the U.S.

Europe and Asia Pacific

Europe recorded a market size of USD 1.54 billion in 2025, capturing 32.07% of the global market share, and is projected to reach USD 1.61 billion in 2026. In 2025, Asia Pacific represented USD 1.23 billion, accounting for 25.58% of the worldwide market, and is projected to grow to USD 1.28 billion in 2026. Other regions, such as Europe and the Asia Pacific, are expected to grow considerably over the forecast period. During the study period, the European region is projected to record a growth rate of 5.3% and reach the valuation of USD 1.54 billion in 2025. This is due to the increasing clinical research activity, growing healthcare investments, improved infrastructure of public and private banks, growing funding initiatives among the stem cell banks in the market. Owing to these factors, countries such as the U.K., France, Germany, are expected to have recorded the valuation of USD 0.29 billion, USD 0.25 billion, and USD 0.33 billion, respectively in 2026. Following Europe, the Asia Pacific market is estimated to reach USD 1.23 billion in 2025 and achieve the position of the third-largest region in the market. India is estimated to have reached USD 0.29 billion in the region, while China is estimated to have touched USD 0.36 billion in 2026.

Latin America and the Middle East & Africa

The Latin America market was valued at USD 0.19 billion in 2025, capturing 3.96% of global revenue, and is estimated to reach USD 0.2 billion in 2026. Middle East & Africa contributed 3.22% to the global market in 2025, with a valuation of USD 0.16 billion, and is projected to reach USD 0.16 billion in 2026. Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness considerable growth in this market. The Latin America market, in 2025, is set to have recorded USD 0.19 billion as its valuation. The growing prevalence of chronic disorders, increasing healthcare investments, and awareness and demand for personalized banking applications are some of the factors supporting the market's growth. In the Middle East & Africa, GCC is set to have touched a value of USD 0.08 billion in 2025.

Competitive Landscape

Key Industry Players

Growing Number of Cell Banking Solutions among the Major Players to Support their Dominance

A diversified technology portfolio for the collection, processing, and storage of stem cells, along with a strong brand presence, is one of the crucial factors supporting the dominant stem cell banking market share. CBR Systems, Inc., LifeCell International Pvt. Ltd., and Cordlife were major players in the market in 2024. Furthermore, the growing focus of key companies on stem cell solution launches is anticipated to support the global market expansion.

- For instance, in October 2024, LifeCell International Pvt. Ltd., launched a stem cell banking solution to strengthen its brand presence.

Other key players, including Cryo-Cell International, Inc., and others, are also growing in the market, primarily owing to their increasing initiatives toward acquisitions & mergers among the other players to increase their market presence globally.

List of Key Stem Cell Banking Companies Profiled

- CBR Systems, Inc. (U.S.)

- LifeCell International Pvt. Ltd. (India)

- Cordlife (Singapore)

- Cryo-Cell International, Inc. (U.S.)

- ViaCord (U.S.)

- Cryoviva (India)

- Biocell (India)

- CryoSave South Africa (Pty) Ltd. (South Africa)

KEY INDUSTRY DEVELOPMENTS

- November 2023 – CryoVault, a stem cell preservation and processing center, was awarded the Best Stem Cell Bank in India. This helped the company to increase its brand presence.

- September 2023 – Cryo-Cell International, Inc., entered a patent option agreement with Duke University, which enables the company to obtain a license to Duke’s patent rights, regulatory data, and proprietary processes related to cord blood, cord tissue, and DUOC-01. This helped the company expand its market presence.

- June 2021 – Generate Life Sciences, a cord blood bank, acquired Cell Care to increase access to reproductive and genetic services among families from pre-conception into adulthood. This supported the company's presence in the market.

- December 2020 – Future Health Biobank acquired the BioEden group to strengthen its business in the tooth stem cell banking sector.

- April 2020 – DKMS Group GmbH established a new DKMS stem cell bank to strengthen its presence in Germany.

REPORT COVERAGE

The market report provides a detailed global market analysis and focuses on key aspects such as leading companies, cell type, service type, bank type, and application. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.38% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Cell Type · Peripheral Blood Stem Cells · Bone Marrow Cells · Adipose Tissue-Derived Stem Cells · CB/CT Derived Stem Cells · Others By Service Type · Sample Preservation and Storage · Sample Analysis · Sample Processing · Sample Collection and Transportation By Bank Type · Public · Private · Hybrid By Application · Research Applications · Clinical Applications · Personalized Banking Applications By Region · North America (By Cell Type, By Service Type, By Bank Type, By Application, and by Country) o U.S. (By Bank Type) o Canada (By Bank Type) · Europe (By Cell Type, By Service Type, By Bank Type, By Application, and by Country/Sub-region) o U.K. (By Bank Type) o Germany (By Bank Type) o France (By Bank Type) o Italy (By Bank Type) o Spain (By Bank Type) o Scandinavia (By Bank Type) o Rest of Europe (By Bank Type) · Asia Pacific (By Cell Type, By Service Type, By Bank Type, By Application, and by Country/Sub-region) o China (By Bank Type) o Japan (By Bank Type) o India (By Bank Type) o Australia (By Bank Type) o Southeast Asia (By Bank Type) o Rest of Asia Pacific (By Bank Type) · Latin America (By Cell Type, By Service Type, By Bank Type, By Application, and by Country/Sub-region) o Brazil (By Bank Type) o Mexico (By Bank Type) o Rest of Latin America (By Bank Type) · Middle East & Africa (By Cell Type, By Service Type, By Bank Type, By Application, and by Country/Sub-region) o GCC (By Bank Type) o South Africa (By Bank Type) o Rest of the Middle East & Africa (By Bank Type) |

Frequently Asked Questions

The global stem cell banking market size is projected to grow from $5.01 billion in 2026 to $8.22 billion by 2034, at a CAGR of 6.38% during the forecast period

In 2025, the North America regional market value stood at USD 1.69 billion.

Growing at a CAGR of 6.38%, the market will exhibit steady growth over the forecast period (2026-2034).

By cell type, the CB/CT-derived stem cells segment was the leading segment in this market in 2025.

The increasing number of stem cell collections is one of the major factors driving the markets growth.

LifeCell International Pvt. Ltd., and Cordlife are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic diseases, growing technological advancements in stem cell technology, and others are some of the factors anticipated to fuel the adoption rate globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us