Sterility Testing Market Size, Share & Industry Analysis, By Type (Kits & Reagents, Instruments, and Services), By Test Type (Membrane Filtration Systems, Incubation and Monitoring Systems, and Others), By Site (In-House Testing and Outsourced Testing), By Application (Pharmaceuticals, Medical Devices, and Others), By End-User (Pharma & Biotech Manufacturers, Medical Device Manufacturers, CDMOs/CMOs & Contract Testing Labs, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

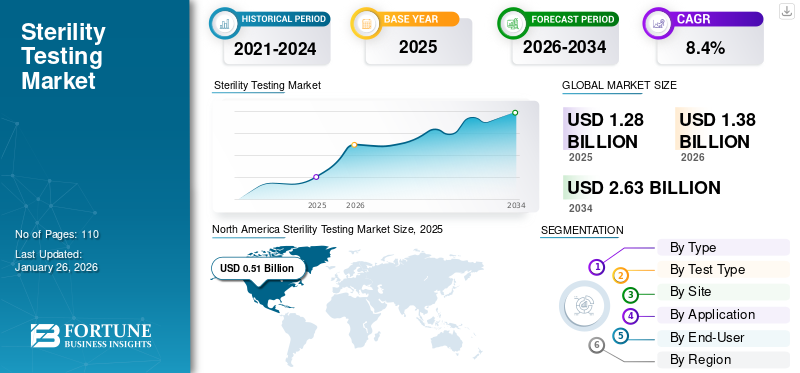

The global sterility testing market size was valued at USD 1.28 billion in 2025. The market is projected to grow from USD 1.38 billion in 2026 to USD 2.63 billion by 2034, exhibiting a CAGR of 8.4% during the forecast period. North America dominated the sterility testing market with a market share of 39.79% in 2025.

Sterility testing is a critical quality assurance process used to confirm that pharmaceutical, biopharmaceutical, and medical device products are free from microorganisms that could endanger patient safety. It employs methodologies such as membrane filtration, direct inoculation, and isolator-based systems to detect potential contamination. Market growth is primarily driven by the increasing production of biologics, vaccines, and combination products that require strict aseptic control. Moreover, the growing regulatory emphasis on contamination prevention, the rising trend of outsourcing quality testing, and the growing use of rapid microbiological methods are further expected to have a positive impact on market growth.

Furthermore, the market is comprised of several major players, including Merck KGaA, Sartorius AG, SKAN AG, Getinge AB, and Fedegari Autoclavi S.p.A., who are at the forefront of the industry. A strong emphasis on extensive investments in new product development is playing a prominent role in helping companies secure substantial market shares.

Download Free sample to learn more about this report.

Sterility Testing Market Key Takeaways

- 2025 Market Size: USD 1.28 billion

- 2026 Market Size: USD 1.38 billion

- 2034 Forecast Market Size: USD 2.63 billion

- CAGR: 8.4% from 2026–2034

- North America dominated the sterility testing market with a 39.79% share in 2025.

- The services segment accounted for a leading 55.69% market share in 2026.

- The membrane filtration systems segment is projected to hold a 66.82% share in 2026.

North America

North America generated USD 0.51 billion in revenue and held a 39.79% market share in 2025.

Asia Pacific

Asia Pacific accounted for USD 0.25 billion and represented 19.70% of the global market in 2025.

Europe

Europe is projected to reach USD 0.40 Billion in 2026, supported by increasing sterile manufacturing activities and rapid adoption of microbiological testing technologies.

U.S.

The market is projected to reach USD 0.51 billion in 2026, supported by strong healthcare infrastructure and automation investments.

Japan

Growing pharmaceutical manufacturing and increasing adoption of sterility testing solutions are supporting market expansion.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Biologics Complexity and Strict Safety Regulations to Drive Market Growth

The growing complexity of sterile manufacturing is driving higher demand for robust sterility assurance throughout both development and commercial production. Moreover, advanced therapies such as biologics, vaccines, and ATMPs heighten batch criticality, necessitating stringent method validation, media fills, and controlled environments. Regulators are reinforcing expectations around data integrity and contamination control frameworks, spurring greater use of isolators, glove integrity testing, and closed-transfer technologies. In addition, contract development and manufacturing organizations (CDMOs) are expanding capacity and implementing rapid testing methods to accelerate product release, thereby catalyzing the global sterility testing market growth.

- For instance, in October 2025, Eli Lilly announced its plan to invest more than USD 1 billion to expand its production facility in India.

MARKET RESTRAINTS

Limited Standardization and Complex Validation Procedures to Hamper Market Growth

The lack of globally harmonized validation protocols for sterility testing presents significant compliance challenges for manufacturers operating across various regulatory regions. Each pharmacopeia, such as the USP, EP, and JP, imposes distinct procedural and documentation requirements, resulting in redundant validation efforts and an increased administrative workload. Additionally, the transfer and implementation of rapid microbiological methods require extensive equivalence and comparability studies, which further increase costs and extend timelines. Furthermore, inconsistencies in environmental monitoring criteria and aseptic process validation standards add to the complexity, delaying product release and heightening regulatory risk.

- For instance, in July 2024, Brassica Pharma received a warning from the FDA for violations of good manufacturing practice (GMP) and environmental regulations.

MARKET OPPORTUNITIES

Adoption of Rapid Microbiological Methods to Create Substantial Growth Opportunities

The market is witnessing a growing adoption of rapid microbiological methods, including bioluminescence, flow cytometry, molecular assays, and automated growth-based systems. These systems enable faster product disposition, reducing timelines from weeks to days while maintaining analytical accuracy, sensitivity, and specificity. Moreover, they support high-risk-based release strategies, earlier detection of deviations, and optimized working capital management. Moreover, the integration of isolator robotics, closed-loop sampling, and electronic batch record systems further minimizes the risks of manual intervention and data integrity issues. Furthermore, the growing introduction of such technologies is also projected to offer considerable opportunities for market growth.

- For instance, in September 2025, Nelson Laboratories, LLC announced the launch of its new RapidCert, a rapid biological indicator (BI) sterility testing. The method incorporates a combination of rapid microbiological methods and traditional BIs.

STERILITY TESTING MARKET TRENDS

Growing Preference for Outsourced Sterility Testing Services is One of the Noticeable Market Trends

Pharmaceutical and biotechnology companies are increasingly turning to specialized contract research and manufacturing organizations for sterility testing services. This growing outsourcing trend is fueled by the high operational and compliance costs associated with maintaining in-house testing facilities, and the increasing focus on rapid and high-throughput microbial analysis. In addition, partnering with external service providers enables manufacturers to leverage advanced isolator technologies, validated rapid microbiological methods, and the expertise of experienced microbiologists without incurring significant capital expenditure.

- For instance, in October 2025, Molded Rubber and Plastic Corporation (MRPC) and Vance Street Capital entered into a strategic collaboration to expand its medical device contract manufacturing facilities.

MARKET CHALLENGES

Shortage of Skilled Microbiologists and Validation Experts to Offer a Substantial Challenge

The sterility testing industry is experiencing a growing shortage of skilled professionals with expertise in aseptic handling, isolator operation, and validation of rapid microbiological methods. As laboratories increasingly adopt automated and digitally integrated systems, the need for cross-trained microbiologists has surged. However, many regions, particularly in emerging markets, face difficulties in training and retaining qualified staff due to limited educational infrastructure and high turnover rates. Furthermore, this talent gap contributes to workflow inefficiencies, variability in test performance, and heightened compliance risks during regulatory audits.

- For instance, according to the Skill India Report 2024, the skill gap in pharmaceutical quality control is very high. The report further states that the employability rate in this sector is estimated at 37%, compared to the national average of 46%.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Substantial Utilization and Recurring Need of Reagents and Kits Accelerated Services Segment Growth

On the basis of type, the market is classified into kits & reagents, instruments, and services.

To know how our report can help streamline your business, Speak to Analyst

The services segment held the highest global sterility testing market share 55.69% in 2026. The services segment represents the largest portion of the sterility testing market due to the higher adoption of services, which is directly associated with the strict implementation of safety regulations. Moreover, the growing preference for outsourcing sterility testing services is also projected to positively impact segment growth. Additionally, the adoption of rapid microbiological methods further drives reagent consumption, as new reagent formulations are validated alongside these instruments.

- For instance, in September 2025, FUJIFILM Wako Pure Chemical Corporation announced the launch of its new RiboNAT rapid sterility test kit, specifically designed for conducting sterility testing in cell therapy applications.

The kits & reagents segment is expected to grow at a CAGR of 7.1% over the forecast period.

By Test Type

Wide Range Applications of Membrane Filtration Systems to Boost Segment Growth

In terms of test type, the market is categorized into membrane filtration systems, incubation and monitoring systems, and others.

The membrane filtration systems segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 66.82% share. The growth of this segment is attributed to its wide adoption, recognition as the pharmacopeial gold standard, and cost efficiency. Moreover, this technique enables the testing of larger sample volumes while ensuring efficient recovery of microorganisms and effective rinsing to remove product residues. Additionally, its compatibility with isolator systems and closed-loop setups ensures compliance with stringent requirements.

- For instance, in September 2019, Charles River Laboratories International, Inc. announced the launch of its new products, including the updated EndoScan-V software solution and Celsis, an automated detection solution for rapid sterility testing. These solutions are especially designed for the pharmaceutical industry.

The incubation and monitoring systems segment is expected to grow at a CAGR of 7.1% over the forecast period.

By Site

High Cost of Maintaining Isolator-Equipped Cleanrooms Boosted Outsourced Testing Segment

In terms of site, the market is categorized into in-house testing and outsourced testing.

The outsourced testing segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 56.18% share. Factors such as stricter regulatory scrutiny, workforce shortages, and the high cost of maintaining isolator-equipped cleanrooms are significantly impacting the adoption of outsourced sterility testing. Moreover, leading service providers such as Charles River Laboratories International, Nelson Labs, SGS, and Eurofins, amongst others, offer validated rapid methods, global capacity, and shorter turnaround times. Furthermore, by partnering with these specialized labs, manufacturers can improve production efficiency while ensuring consistent quality and regulatory compliance, positioning outsourced testing as the fastest-growing segment.

- For instance, in November 2023, BSI and Nelson Labs entered into a strategic collaboration to expand their global network of outsourced sterility testing.

The in-house testing segment is expected to grow at a CAGR of 7.6% over the forecast period.

By Application

Increasing Regulatory Emphasis Boosted Pharmaceutical Segment Growth

In terms of application, the market is categorized into pharmaceuticals, medical devices, and others.

The pharmaceutical segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 71.92% share. The pharmaceutical sector has witnessed significant growth in biologics, biosimilars, and advanced therapies, which has consequently expanded the number of batches subjected to sterility testing. Furthermore, the increasing regulatory emphasis on contamination control, coupled with the expansion of global sterile manufacturing facilities, is expected to further boost the substantial market share of the segment during the forecast period.

The medical devices segment is expected to grow at a CAGR of 8.3% over the forecast period.

By End-User

Larger Production Volumes Coupled with Robust Quality Check Operations Boosted Pharma & Biotech Manufacturers Segment Growth

Based on end-user, the market is segmented into pharma & biotech manufacturers, medical device manufacturers, CDMOs/CMOs & contract testing labs, and others.

In 2024, the global market was dominated by the pharma & biotech manufacturers segment. Certain factors, such as higher production volumes, substantial investments in sterility testing, and a strong emphasis on validation, are playing a prominent role in driving segment growth. Furthermore, these facilities operate under rigorous quality control requirements. Moreover, pharmaceutical and biotechnology manufacturers continue to invest heavily in automation, isolator technology, and rapid microbial detection systems to sustain regulatory compliance.

- In October 2025, Recipharm announced the opening of its new sterility labs in India.

In addition, CDMOs/CMOs & contract testing labs are projected to grow at a CAGR of 8.8% during the study period.

Sterility Testing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Sterility Testing Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

North America maintained a strong presence in the global market, reaching USD 0.51 billion in 2025, accounting for 39.79% share, and is expected to reach USD 0.55 billion in 2026. The growth of the market in the region is attributed to substantial production of pharmaceutical products and medical devices, strong regulatory emphasis on sterility regulations, and technological advancements. In 2026, the U.S. market is estimated to reach USD 0.51 billion, attributed to a well-established healthcare infrastructure, extensive investments in sterilization, and a high focus on automation.

- For instance, in March 2025, Nelson Labs launched rapid sterility testing services at three laboratories located in Europe and the U.S.

Asia Pacific

The Asia Pacific market accounted for USD 0.25 billion in 2025, representing 19.70% of the global industry, and is expected to reach USD 0.28 billion in 2026. Asia Pacific is expected to exhibit the fastest CAGR during the forecast period. Europe is also projected to witness a notable growth in the coming years. During the forecast period, the region is projected to record a growth rate of 7.4% and reach a valuation of USD 0.40 billion by 2025. This is primarily due to the high production batches, increasing pharmaceutical manufacturing, and new product introductions. Backed by these factors, countries including the U.K. are anticipated to record the valuation of USD 0.08 billion, Germany to record USD 0.11 billion, and France to record USD 0.06 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 0.25 billion in 2025. In the region, India and China are both estimated to reach USD 0.04 billion and USD 0.08 billion, respectively, in 2026.

Latin America and Middle East & Africa

Latin America contributed 5.32% to the global market in 2025, with a valuation of USD 0.07 billion, and is projected to reach USD 0.07 billion in 2026. In 2025, Middle East & Africa represented USD 0.05 billion, accounting for 3.84% of the worldwide market, and is projected to grow to USD 0.05 billion in 2026. Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space. The market in Latin America in 2025 is set to reach a valuation of USD 0.07 billion, driven by the consolidation of healthcare infrastructure and extensive investments in superior healthcare facilities. In the Middle East & Africa, the GCC is set to reach a value of USD 0.03 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Emphasis on Strategic Partnership and Extensive Investments are Assisting Market Players to Maintain Their Market Position

The global sterility testing market exhibits a semi-concentrated structure, with numerous small- to mid-sized companies actively operating worldwide. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Merck KGaA, Sartorius AG, SKAN AG, Getinge AB, and Fedegari Autoclavi S.p.A. are some of the dominating players in the market. A comprehensive range of sterility testing technologies, continual innovation, and extensive focus on research & development are a few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include Charles River Laboratories International, Inc., Thermo Fisher Scientific Inc., Hardy Diagnostics, and others. These companies are undertaking various strategic initiatives, such as partnerships with healthcare providers to enhance their market presence.

LIST OF KEY STERILITY TESTING MARKET COMPANIES PROFILED

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- SKAN AG (Switzerland)

- Getinge AB (Sweden)

- Fedegari Autoclavi S.p.A. (Italy)

- Extract Technology Limited (U.K.)

- bioMérieux SA (France)

- Charles River Laboratories International, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Hardy Diagnostics (U.S.)

- Danaher (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Symcel entered into a strategic collaboration with Johnson & Johnson, aiming to expand and validate its next-generation platform for rapid sterility testing. With the help of this collaboration, Symcel plans to implement its new platform following regulatory approvals.

- March 2025: Sysmex Corporation and Japan Tissue Engineering Co., Ltd. signed a strategic partnership to implement sterility testing for cell therapy and regenerative medicine.

- October 2024: Rapid Micro Biosystems, Inc. announced the launch of direct rapid sterility technology for biologics and sterile injectables.

- October 2024: LGM Pharmaceuticals announced the expansion of its analytical and rapid sterility testing capabilities.

- June 2022: STEMart announced the launch of its new sterility and microbiology testing services, especially for medical devices.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type · Kits & Reagents · Instruments · Services By Test Type · Membrane Filtration Systems · Incubation and Monitoring Systems · Others By Site · In-House Testing · Outsourced Testing By Application · Pharmaceuticals · Medical Devices · Others By End User · Pharma & Biotech Manufacturers · Medical Device Manufacturers · CDMOs/CMOs & Contract Testing Labs · Others By Geography · North America (By Type, Test Type, Site, Application, End User, and Country) o U.S. § By Type o Canada § By Type · Europe (By Type, Test Type, Site, Application, End User, and Country/Sub-region) o Germany § By Type o U.K. § By Type o France § By Type o Spain § By Type o Italy § By Type o Scandinavia § By Type o Rest of Europe § By Type · Asia Pacific (By Type, Test Type, Site, Application, End User, and Country/Sub-region) o China § By Type o Japan § By Type o India § By Type o Australia § By Type o Southeast Asia § By Type o Rest of Asia Pacific § By Type · Latin America (By Type, Test Type, Site, Application, End User, and Country/Sub-region) o Brazil § By Type o Mexico § By Type o Rest of Latin America § By Product Type · Middle East and Africa (By Type, Test Type, Site, Application, End User, and Country/Sub-region) o GCC § By Type o Saudi Arabia § By Type o Rest of Middle East and Africa § By Type |

Frequently Asked Questions

The global sterility testing market size was valued at USD 1.28 billion in 2025. The market is projected to grow from USD 1.38 billion in 2026 to USD 2.63 billion by 2034, exhibiting a CAGR of 8.4% during the forecast period.

In 2025, the market value stood at USD 0.51 billion.

The market is expected to exhibit a CAGR of 8.4% during the forecast period (2026-2034).

The services segment led the market by type.

The key factors driving the market are the rising emphasis on sterilization regulations and significant investments in new product development.

Merck KGaA, Sartorius AG, SKAN AG, Getinge AB, and Fedegari Autoclavi S.p.A. are some of the prominent players in the market.

North America dominated the market in 2025.

Technological advancements and the rising production of medical devices are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us